Taxation | Assignment | New

VerifiedAdded on 2022/09/14

|10

|2063

|14

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION

Taxation

Name of the Student

Name of the University

Author Note

Taxation

Name of the Student

Name of the University

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION

1)

Issue

Which of the income are required to be included within the tax return pertaining to Anna for the

year ending on 30th June 2019. Whether any of the expenses incurred by Anna is allowable as deduction

in the same year.

Rule

Any receipt received by a taxpayer, which can be treated as an income even in the absence of any

statutory provision recognising the same as income would be rendered as ordinary income as provided in

ITAA97, s 6-5.

As per the legal principles enumerated in the decision of Dean & Anor v FC of T 97 ATC 4762,

income accrued from personal exertion would be required to be treated as an ordinary income and any e

receipt incurred as a remuneration for employment would be included in the same.

PAYG withheld are required to be adjusted with the net tax liability and needs to be treated as a

credit for the taxpayer as provided in ITAA97, s 18-15.

Interest from bank is required to be treated as and ordinary income as for the legal principle

enumerated in Riches v Westminster Bank Ltd [1947] AC 390.

Amount received by way of dividend is required to be included in the taxable income in case of

resident individuals as provided in ITAA36, s 44.

Income from exploitation of land is required to be treated as an ordinary taxable income as per

the legal rule established in the case of Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932)

2 ATD 1.

1)

Issue

Which of the income are required to be included within the tax return pertaining to Anna for the

year ending on 30th June 2019. Whether any of the expenses incurred by Anna is allowable as deduction

in the same year.

Rule

Any receipt received by a taxpayer, which can be treated as an income even in the absence of any

statutory provision recognising the same as income would be rendered as ordinary income as provided in

ITAA97, s 6-5.

As per the legal principles enumerated in the decision of Dean & Anor v FC of T 97 ATC 4762,

income accrued from personal exertion would be required to be treated as an ordinary income and any e

receipt incurred as a remuneration for employment would be included in the same.

PAYG withheld are required to be adjusted with the net tax liability and needs to be treated as a

credit for the taxpayer as provided in ITAA97, s 18-15.

Interest from bank is required to be treated as and ordinary income as for the legal principle

enumerated in Riches v Westminster Bank Ltd [1947] AC 390.

Amount received by way of dividend is required to be included in the taxable income in case of

resident individuals as provided in ITAA36, s 44.

Income from exploitation of land is required to be treated as an ordinary taxable income as per

the legal rule established in the case of Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932)

2 ATD 1.

2TAXATION

Expense that are accrued to a person by virtue of his income earning process or is a consequence

of the same would be allowed as a deduction as per ITAA97, s 8.1

Any expense that has been incurred for a public or private purpose would not be allowed as a

deduction. This can be supported with the case of Lodge v Federal Commissioner of Taxation [1972]

HCA 49.

Travelling from work to other place relating to work is required to be treated as an deductible

expense as per the case of Taylor v Provan [1975] AC 194. Travel from home to work is not deductible in

its general senses, but the same is to be treated as deductible in special circumstances where there is an

on-call duty as per the case of FC of T v Collings 76 ATC 4254.

Expense for a suit or any other items of conventional nature are not to be included allowed as a

deduction under ITAA97, s 8.1. This can further be supported with the case of Mansfield v FC of T 96

ATC 4001.

Depreciation of an asset using the Prime Cost Method = Cost x (Days held / 365) x (100% /

Effective life in years)

Expenses incurred for home office will not be allowed as a deduction under ITAA97, s 8.1 as can

be supported by the case of Handley v FC of T 81 ATC 4165.

Application

Receipts

Wages (income from personal exertion, ordinary income). $160,000

As any receipt received by a taxpayer, which can be treated as an income even in the absence of

any statutory provision recognising the same as income would be rendered as ordinary income as

provided in ITAA97, s 6-5. As per the legal principles enumerated in the decision of Dean & Anor v FC

Expense that are accrued to a person by virtue of his income earning process or is a consequence

of the same would be allowed as a deduction as per ITAA97, s 8.1

Any expense that has been incurred for a public or private purpose would not be allowed as a

deduction. This can be supported with the case of Lodge v Federal Commissioner of Taxation [1972]

HCA 49.

Travelling from work to other place relating to work is required to be treated as an deductible

expense as per the case of Taylor v Provan [1975] AC 194. Travel from home to work is not deductible in

its general senses, but the same is to be treated as deductible in special circumstances where there is an

on-call duty as per the case of FC of T v Collings 76 ATC 4254.

Expense for a suit or any other items of conventional nature are not to be included allowed as a

deduction under ITAA97, s 8.1. This can further be supported with the case of Mansfield v FC of T 96

ATC 4001.

Depreciation of an asset using the Prime Cost Method = Cost x (Days held / 365) x (100% /

Effective life in years)

Expenses incurred for home office will not be allowed as a deduction under ITAA97, s 8.1 as can

be supported by the case of Handley v FC of T 81 ATC 4165.

Application

Receipts

Wages (income from personal exertion, ordinary income). $160,000

As any receipt received by a taxpayer, which can be treated as an income even in the absence of

any statutory provision recognising the same as income would be rendered as ordinary income as

provided in ITAA97, s 6-5. As per the legal principles enumerated in the decision of Dean & Anor v FC

3TAXATION

of T 97 ATC 4762, income accrued from personal exertion would be required to be treated as an ordinary

income and any e receipt incurred as a remuneration for employment would be included in the same.

PAYG withheld amounting to $47,000 are required to be adjusted with the net tax liability and

needs to be treated as a credit for Anna. This is because PAYG withheld are required to be adjusted with

the net tax liability and needs to be treated as a credit for the taxpayer as provided in ITAA97, s 18-15.

Interest from Bank (50% needs to be taken as it is a joint account with Alan) resulting to $1,400.

This is because Interest from bank is required to be treated as and ordinary income as for the legal

principle enumerated in Riches v Westminster Bank Ltd [1947] AC 390.

Franked dividend from QBE Insurance:

Taxable amount = 4200 * (30/70)

= $ 1800

Dividend from AMP

Franked = 1400 * (30/70)

= $ 600

Unfranked = 700

This is because Amount received by way of dividend is required to be included in the taxable

income in case of resident individuals as provided in ITAA36, s 44.

Fees from overseas client received during holidays (taxable) = $ 3500

Fees for advising a neighbor (taxable) = $ 500

Price for writing the article to local newspaper (taxable) = $ 5,000

of T 97 ATC 4762, income accrued from personal exertion would be required to be treated as an ordinary

income and any e receipt incurred as a remuneration for employment would be included in the same.

PAYG withheld amounting to $47,000 are required to be adjusted with the net tax liability and

needs to be treated as a credit for Anna. This is because PAYG withheld are required to be adjusted with

the net tax liability and needs to be treated as a credit for the taxpayer as provided in ITAA97, s 18-15.

Interest from Bank (50% needs to be taken as it is a joint account with Alan) resulting to $1,400.

This is because Interest from bank is required to be treated as and ordinary income as for the legal

principle enumerated in Riches v Westminster Bank Ltd [1947] AC 390.

Franked dividend from QBE Insurance:

Taxable amount = 4200 * (30/70)

= $ 1800

Dividend from AMP

Franked = 1400 * (30/70)

= $ 600

Unfranked = 700

This is because Amount received by way of dividend is required to be included in the taxable

income in case of resident individuals as provided in ITAA36, s 44.

Fees from overseas client received during holidays (taxable) = $ 3500

Fees for advising a neighbor (taxable) = $ 500

Price for writing the article to local newspaper (taxable) = $ 5,000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION

Expenses

Cost of Anna’s ticket = not deductible

Accommodation and incidentals were paid off by cash received from client in Hong Kong 3,500

= not deductible.

Travel between home and office for week-end work 150 = deductible

Travel to Client Meeting at Client’s office (not reimbursed by employer) 75 = deductible

Heavy Jacket to be worn for client meetings only, during winter 1,200 = not deductible

Home Laundry of her Logo shirt mixed with other clothes twice a week 50 weeks = not

deductible

Dry Cleaning of Suites 1,650 being a Solicitor, it is compulsory for Anna to wear suit to office

every day = not deductible.

Laptop bought (100% work related) on 1/7/2018 4,500 = deductible

Depreciated over 2 years Using (Straight line method) = deductible

Amount to be deducted = Cost x (Days held / 365) x (100% / Effective life in years) =

4500*1*100%/4 = $1125

Repairs to Laptop (dropped Accidentally on 8/10/2018) 450 = deductible

Monitor for Laptop (Bought on 1/11/2018) 310 = deductible

Bar Association annual subscription 1,300 = deductible

Professional Indemnity Insurance (Paid Monthly) 1,800 = deductible

Book “Concise Australian Commercial Law” 140 = deductible

Book “How to make profits in a falling share market” 225 = not deductible

Expenses

Cost of Anna’s ticket = not deductible

Accommodation and incidentals were paid off by cash received from client in Hong Kong 3,500

= not deductible.

Travel between home and office for week-end work 150 = deductible

Travel to Client Meeting at Client’s office (not reimbursed by employer) 75 = deductible

Heavy Jacket to be worn for client meetings only, during winter 1,200 = not deductible

Home Laundry of her Logo shirt mixed with other clothes twice a week 50 weeks = not

deductible

Dry Cleaning of Suites 1,650 being a Solicitor, it is compulsory for Anna to wear suit to office

every day = not deductible.

Laptop bought (100% work related) on 1/7/2018 4,500 = deductible

Depreciated over 2 years Using (Straight line method) = deductible

Amount to be deducted = Cost x (Days held / 365) x (100% / Effective life in years) =

4500*1*100%/4 = $1125

Repairs to Laptop (dropped Accidentally on 8/10/2018) 450 = deductible

Monitor for Laptop (Bought on 1/11/2018) 310 = deductible

Bar Association annual subscription 1,300 = deductible

Professional Indemnity Insurance (Paid Monthly) 1,800 = deductible

Book “Concise Australian Commercial Law” 140 = deductible

Book “How to make profits in a falling share market” 225 = not deductible

5TAXATION

New chair for Anna’s home office 175 = not deductible

Paid to fix her garage door at home 400 = not deductible

Child care Expenses while working 9,000 = not deductible

Bank charges (on her savings account where wages are credited) 120 = deductible

Bank charges on Home Loan (Investment Property) 96 = deductible

Investment Property

Receipts

Rental Income from Property (950*30) (taxable) = $28500 this is because income from

exploitation of land is required to be treated as an ordinary taxable income as per the legal rule

established in the case of Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

Expenses

Deductible interest = 960000 * 4.5% = $ 43200

Stamp duty of $38,690 = deductible

Solicitors fee of $1,500 = deductible

Loan processing fee of $750 = deductible

Repair of Air conditioner $ 900 = deductible

The expense towards the stove is not deductible.

Council Rate 1,376 = deductible

Strata 3,298 = deductible

Repairs due to tenant damage (March 2019) 1,670 = deductible

New chair for Anna’s home office 175 = not deductible

Paid to fix her garage door at home 400 = not deductible

Child care Expenses while working 9,000 = not deductible

Bank charges (on her savings account where wages are credited) 120 = deductible

Bank charges on Home Loan (Investment Property) 96 = deductible

Investment Property

Receipts

Rental Income from Property (950*30) (taxable) = $28500 this is because income from

exploitation of land is required to be treated as an ordinary taxable income as per the legal rule

established in the case of Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

Expenses

Deductible interest = 960000 * 4.5% = $ 43200

Stamp duty of $38,690 = deductible

Solicitors fee of $1,500 = deductible

Loan processing fee of $750 = deductible

Repair of Air conditioner $ 900 = deductible

The expense towards the stove is not deductible.

Council Rate 1,376 = deductible

Strata 3,298 = deductible

Repairs due to tenant damage (March 2019) 1,670 = deductible

6TAXATION

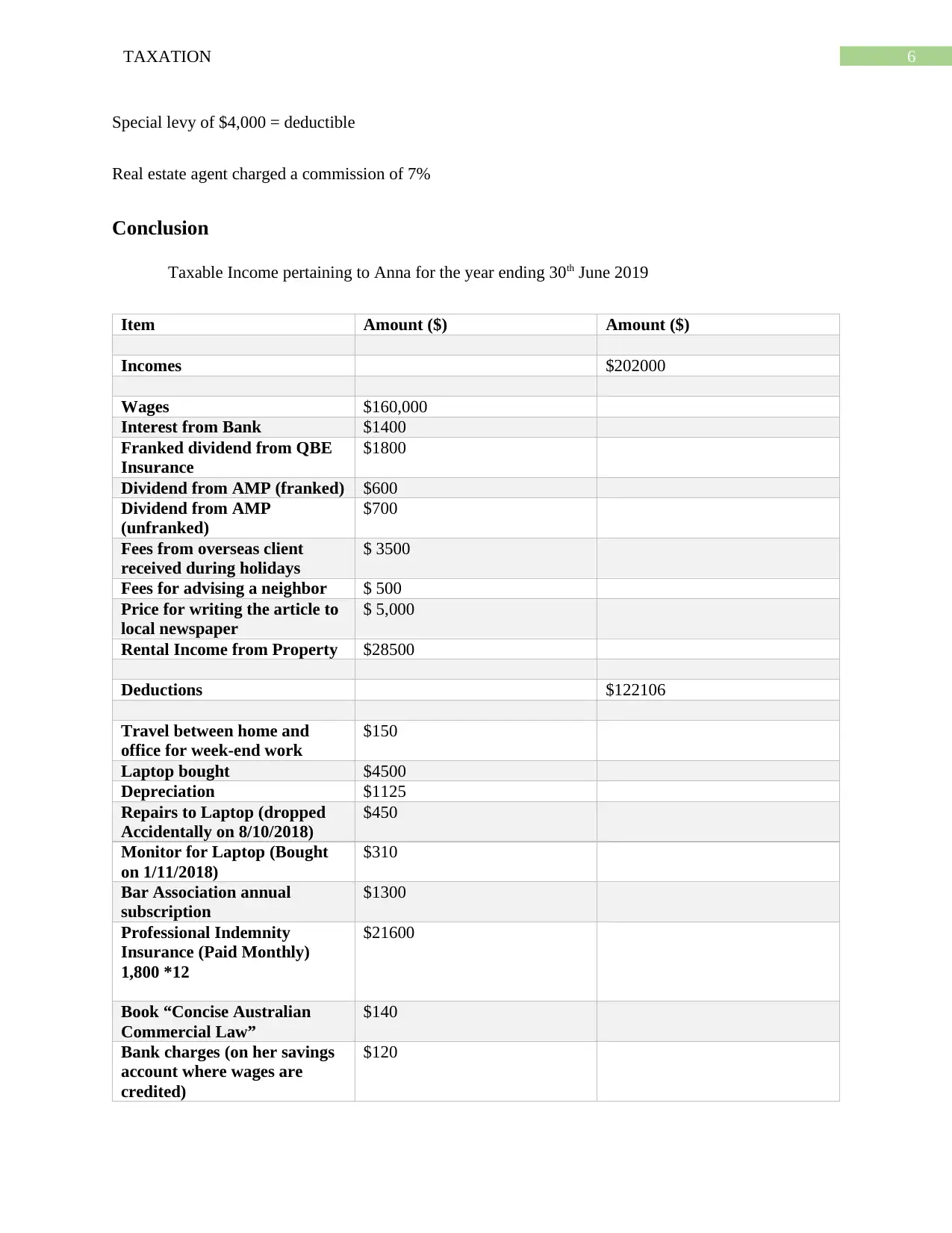

Special levy of $4,000 = deductible

Real estate agent charged a commission of 7%

Conclusion

Taxable Income pertaining to Anna for the year ending 30th June 2019

Item Amount ($) Amount ($)

Incomes $202000

Wages $160,000

Interest from Bank $1400

Franked dividend from QBE

Insurance

$1800

Dividend from AMP (franked) $600

Dividend from AMP

(unfranked)

$700

Fees from overseas client

received during holidays

$ 3500

Fees for advising a neighbor $ 500

Price for writing the article to

local newspaper

$ 5,000

Rental Income from Property $28500

Deductions $122106

Travel between home and

office for week-end work

$150

Laptop bought $4500

Depreciation $1125

Repairs to Laptop (dropped

Accidentally on 8/10/2018)

$450

Monitor for Laptop (Bought

on 1/11/2018)

$310

Bar Association annual

subscription

$1300

Professional Indemnity

Insurance (Paid Monthly)

1,800 *12

$21600

Book “Concise Australian

Commercial Law”

$140

Bank charges (on her savings

account where wages are

credited)

$120

Special levy of $4,000 = deductible

Real estate agent charged a commission of 7%

Conclusion

Taxable Income pertaining to Anna for the year ending 30th June 2019

Item Amount ($) Amount ($)

Incomes $202000

Wages $160,000

Interest from Bank $1400

Franked dividend from QBE

Insurance

$1800

Dividend from AMP (franked) $600

Dividend from AMP

(unfranked)

$700

Fees from overseas client

received during holidays

$ 3500

Fees for advising a neighbor $ 500

Price for writing the article to

local newspaper

$ 5,000

Rental Income from Property $28500

Deductions $122106

Travel between home and

office for week-end work

$150

Laptop bought $4500

Depreciation $1125

Repairs to Laptop (dropped

Accidentally on 8/10/2018)

$450

Monitor for Laptop (Bought

on 1/11/2018)

$310

Bar Association annual

subscription

$1300

Professional Indemnity

Insurance (Paid Monthly)

1,800 *12

$21600

Book “Concise Australian

Commercial Law”

$140

Bank charges (on her savings

account where wages are

credited)

$120

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION

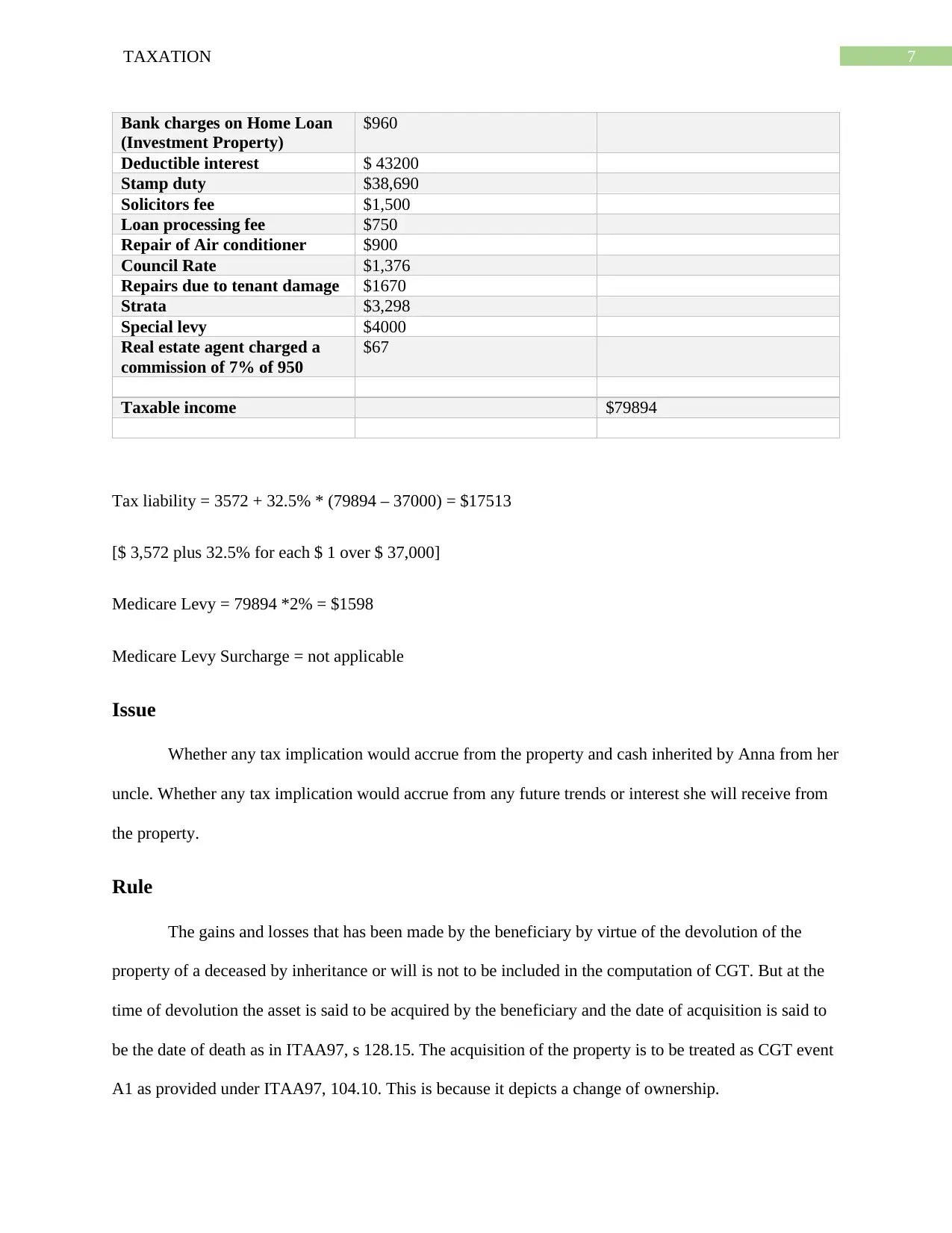

Bank charges on Home Loan

(Investment Property)

$960

Deductible interest $ 43200

Stamp duty $38,690

Solicitors fee $1,500

Loan processing fee $750

Repair of Air conditioner $900

Council Rate $1,376

Repairs due to tenant damage $1670

Strata $3,298

Special levy $4000

Real estate agent charged a

commission of 7% of 950

$67

Taxable income $79894

Tax liability = 3572 + 32.5% * (79894 – 37000) = $17513

[$ 3,572 plus 32.5% for each $ 1 over $ 37,000]

Medicare Levy = 79894 *2% = $1598

Medicare Levy Surcharge = not applicable

Issue

Whether any tax implication would accrue from the property and cash inherited by Anna from her

uncle. Whether any tax implication would accrue from any future trends or interest she will receive from

the property.

Rule

The gains and losses that has been made by the beneficiary by virtue of the devolution of the

property of a deceased by inheritance or will is not to be included in the computation of CGT. But at the

time of devolution the asset is said to be acquired by the beneficiary and the date of acquisition is said to

be the date of death as in ITAA97, s 128.15. The acquisition of the property is to be treated as CGT event

A1 as provided under ITAA97, 104.10. This is because it depicts a change of ownership.

Bank charges on Home Loan

(Investment Property)

$960

Deductible interest $ 43200

Stamp duty $38,690

Solicitors fee $1,500

Loan processing fee $750

Repair of Air conditioner $900

Council Rate $1,376

Repairs due to tenant damage $1670

Strata $3,298

Special levy $4000

Real estate agent charged a

commission of 7% of 950

$67

Taxable income $79894

Tax liability = 3572 + 32.5% * (79894 – 37000) = $17513

[$ 3,572 plus 32.5% for each $ 1 over $ 37,000]

Medicare Levy = 79894 *2% = $1598

Medicare Levy Surcharge = not applicable

Issue

Whether any tax implication would accrue from the property and cash inherited by Anna from her

uncle. Whether any tax implication would accrue from any future trends or interest she will receive from

the property.

Rule

The gains and losses that has been made by the beneficiary by virtue of the devolution of the

property of a deceased by inheritance or will is not to be included in the computation of CGT. But at the

time of devolution the asset is said to be acquired by the beneficiary and the date of acquisition is said to

be the date of death as in ITAA97, s 128.15. The acquisition of the property is to be treated as CGT event

A1 as provided under ITAA97, 104.10. This is because it depicts a change of ownership.

8TAXATION

Again, future income from the property would be treated as an ordinary income as the same

would be available from the exploitation of the property as has been held in the case of Adelaide Fruit and

Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

Application

Hence, the property that would be received by Anna as an inheritance from her uncle would be

required to be treated as a CGT event A1 and the same would be disregarded. However, all the future

income are required to be treated as an ordinary income.

Conclusion

The inheriting of the property would be a CGT event A1. The cash receipt would be disregarded.

The future income would be assessable.

3)

Whether the tax situation pertaining to Anna can be improved in anyway without any additional

expenses being incurred and by rearranging the income she has already incurred. She could have reduced

her tax liability by rearranging the expenses. She could have not taken her family on a holiday while

visiting the client overseas. This would have given her the opportunity to claim accommodation as well as

other expenses overseas as deductible.

Again, future income from the property would be treated as an ordinary income as the same

would be available from the exploitation of the property as has been held in the case of Adelaide Fruit and

Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1.

Application

Hence, the property that would be received by Anna as an inheritance from her uncle would be

required to be treated as a CGT event A1 and the same would be disregarded. However, all the future

income are required to be treated as an ordinary income.

Conclusion

The inheriting of the property would be a CGT event A1. The cash receipt would be disregarded.

The future income would be assessable.

3)

Whether the tax situation pertaining to Anna can be improved in anyway without any additional

expenses being incurred and by rearranging the income she has already incurred. She could have reduced

her tax liability by rearranging the expenses. She could have not taken her family on a holiday while

visiting the client overseas. This would have given her the opportunity to claim accommodation as well as

other expenses overseas as deductible.

9TAXATION

Reference

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Dean & Anor v FC of T 97 ATC 4762

FC of T v Collings 76 ATC 4254

Handley v FC of T 81 ATC 4165

Lodge v Federal Commissioner of Taxation [1972] HCA 49

Mansfield v FC of T 96 ATC 4001

Riches v Westminster Bank Ltd [1947] AC 390

Taylor v Provan [1975] AC 194

The Income Tax Assessment Act 1936(Cth)

The Income Tax Assessment Act 1997(Cth)

Reference

Adelaide Fruit and Produce Exchange Co Ltd v DFC of T (1932) 2 ATD 1

Dean & Anor v FC of T 97 ATC 4762

FC of T v Collings 76 ATC 4254

Handley v FC of T 81 ATC 4165

Lodge v Federal Commissioner of Taxation [1972] HCA 49

Mansfield v FC of T 96 ATC 4001

Riches v Westminster Bank Ltd [1947] AC 390

Taylor v Provan [1975] AC 194

The Income Tax Assessment Act 1936(Cth)

The Income Tax Assessment Act 1997(Cth)

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.