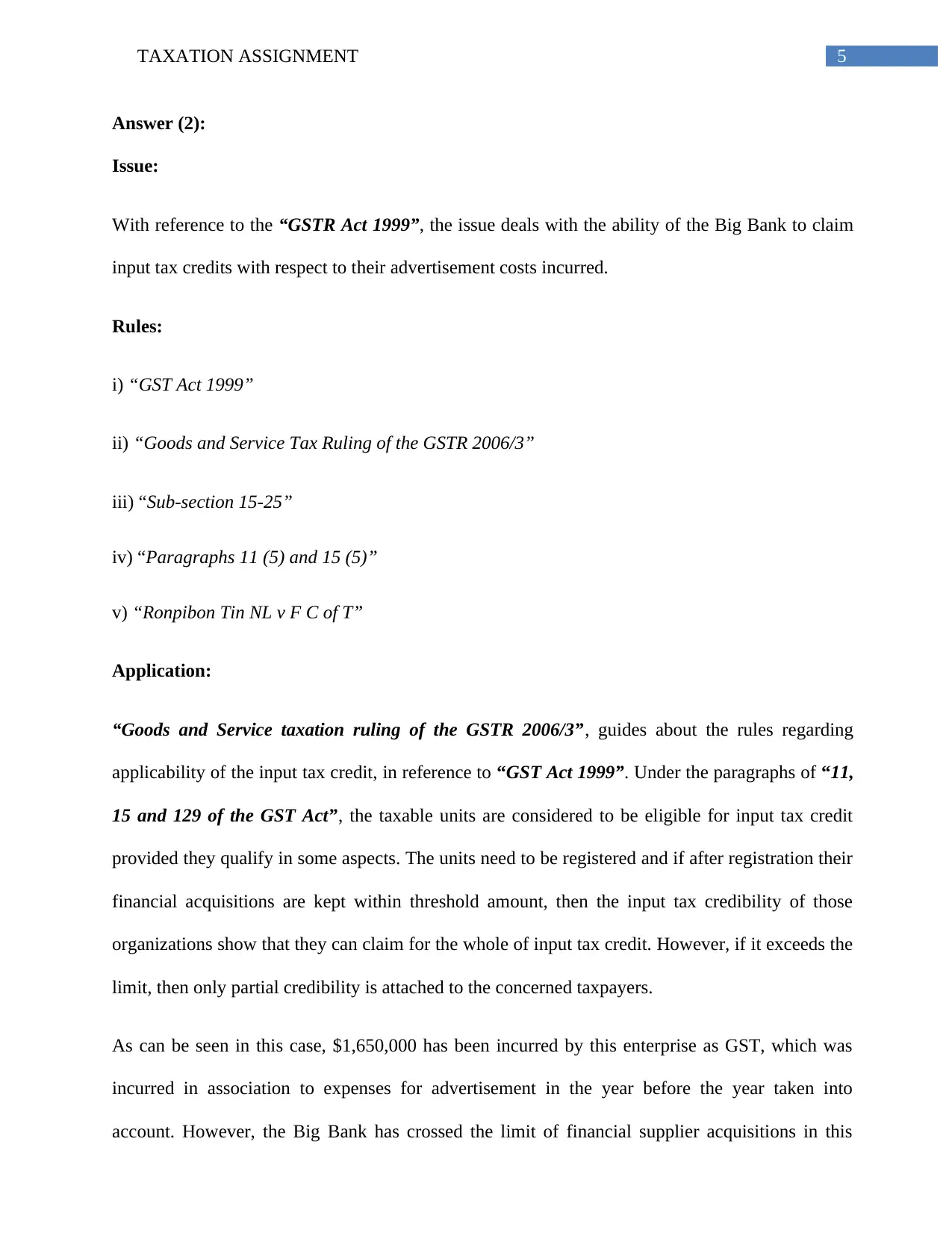

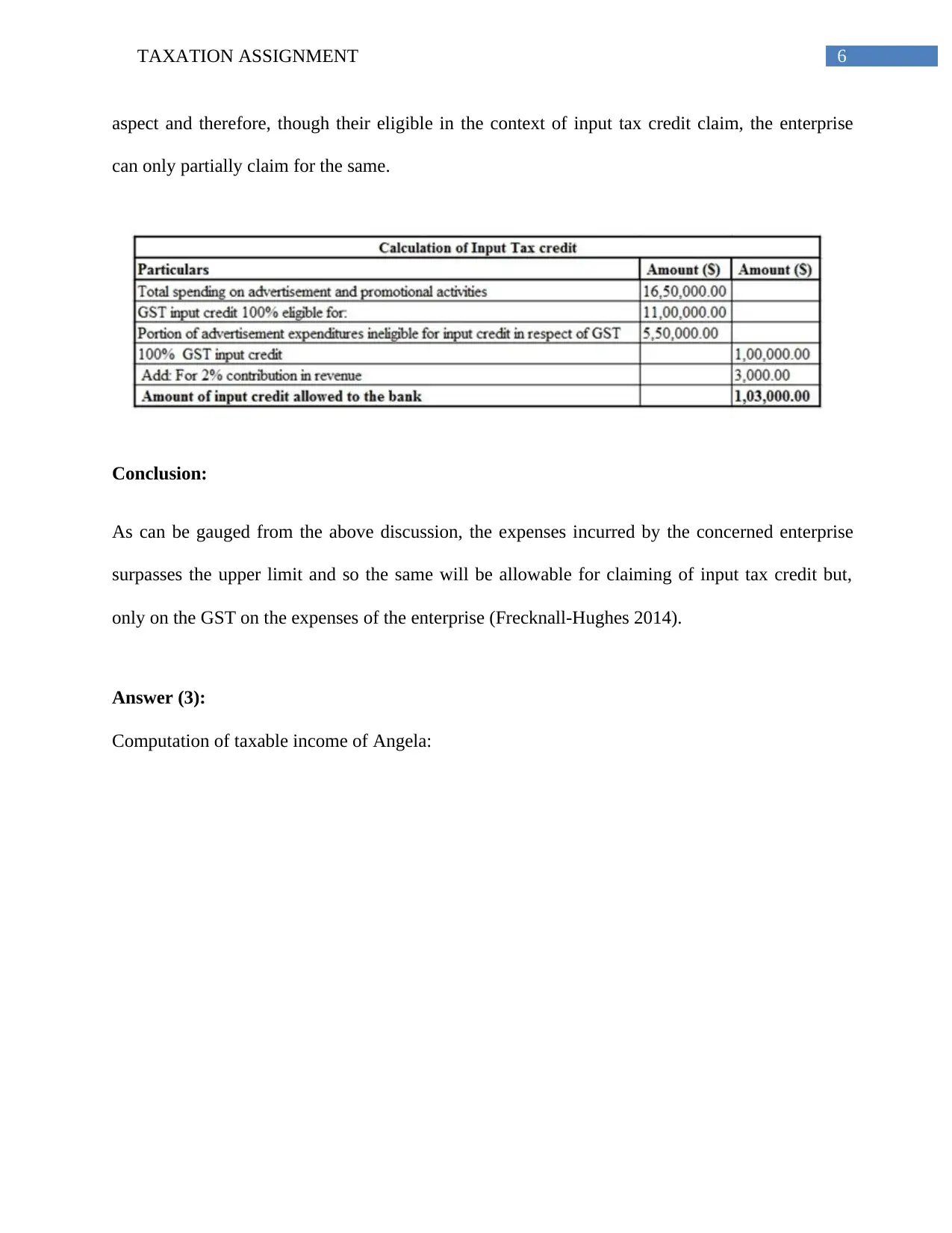

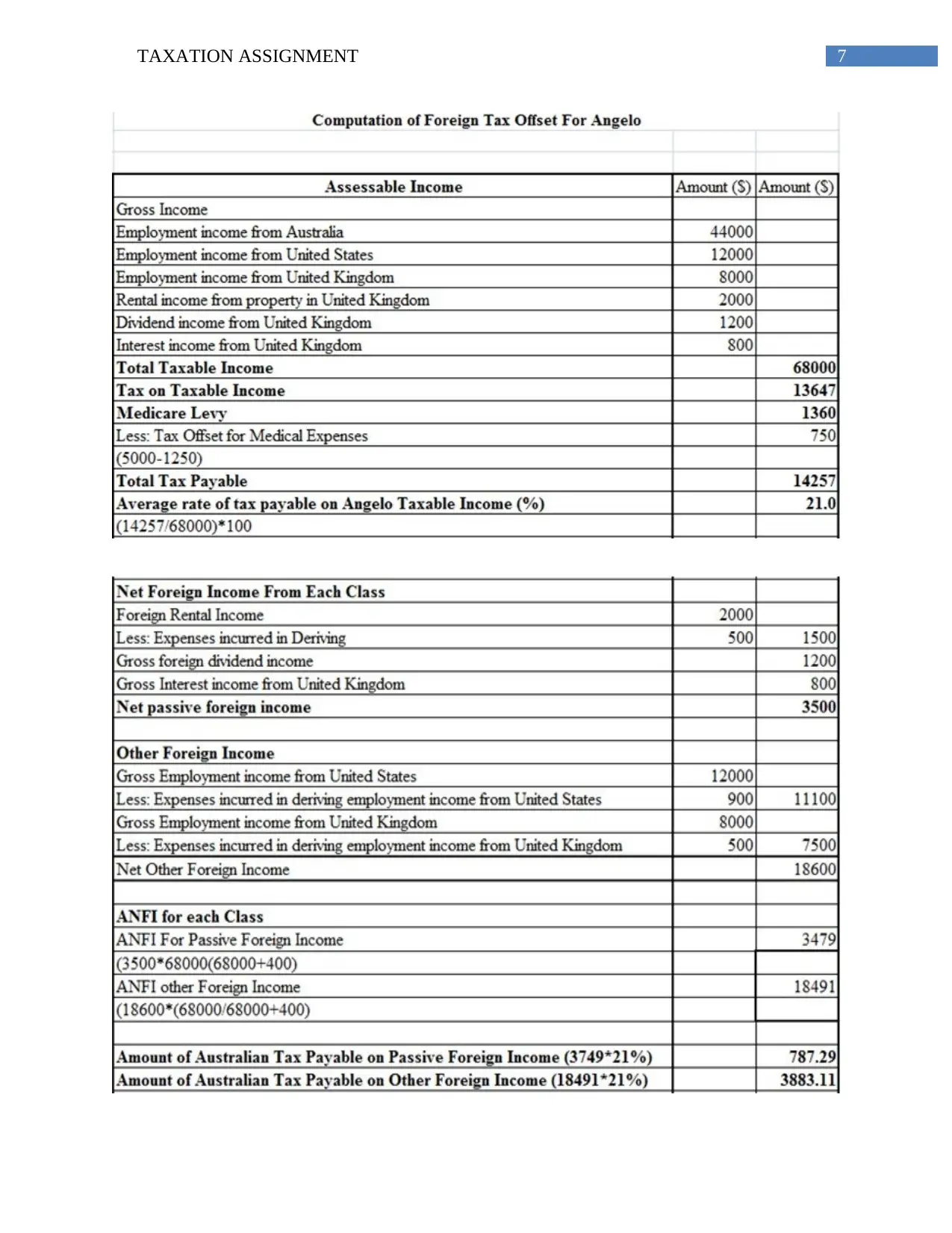

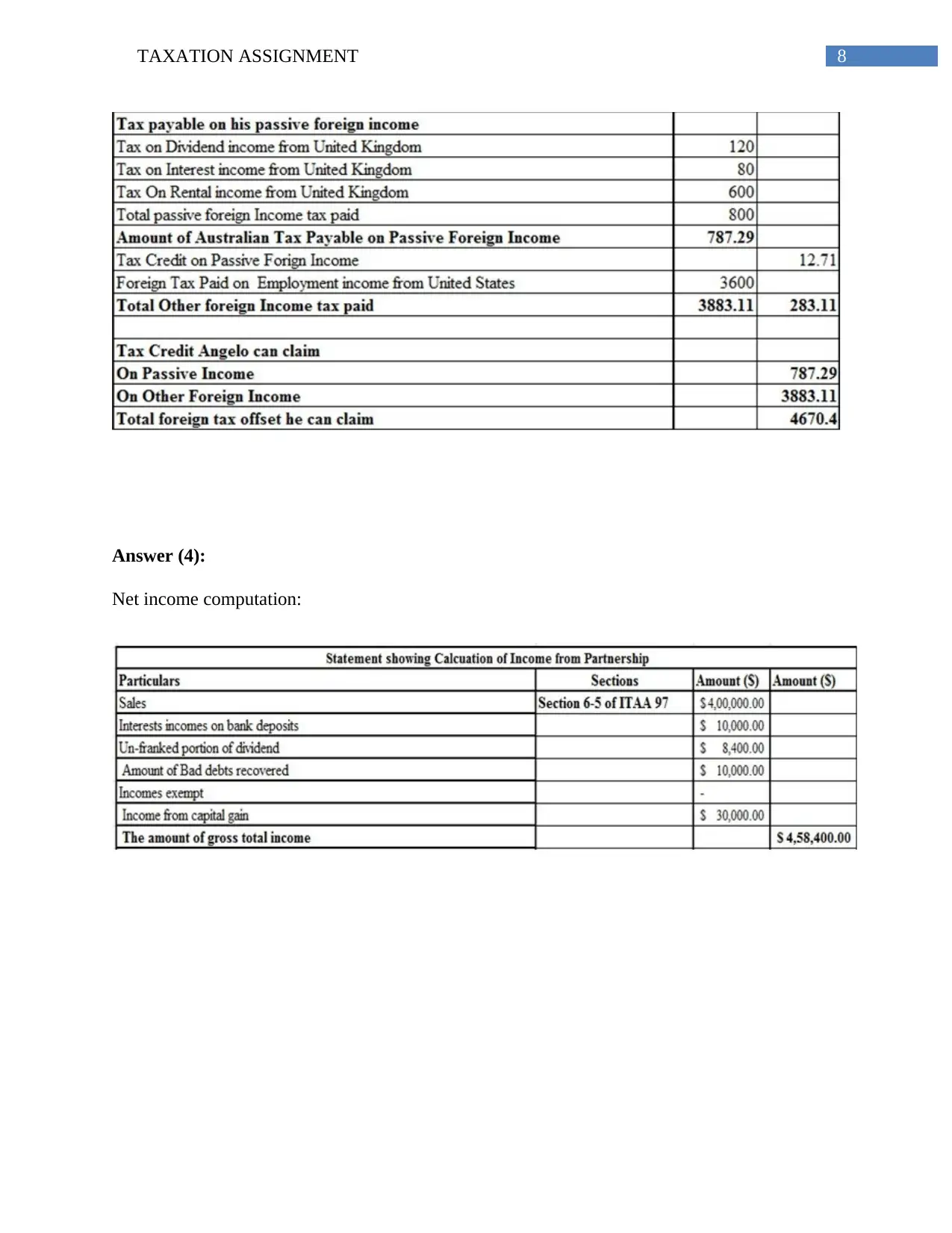

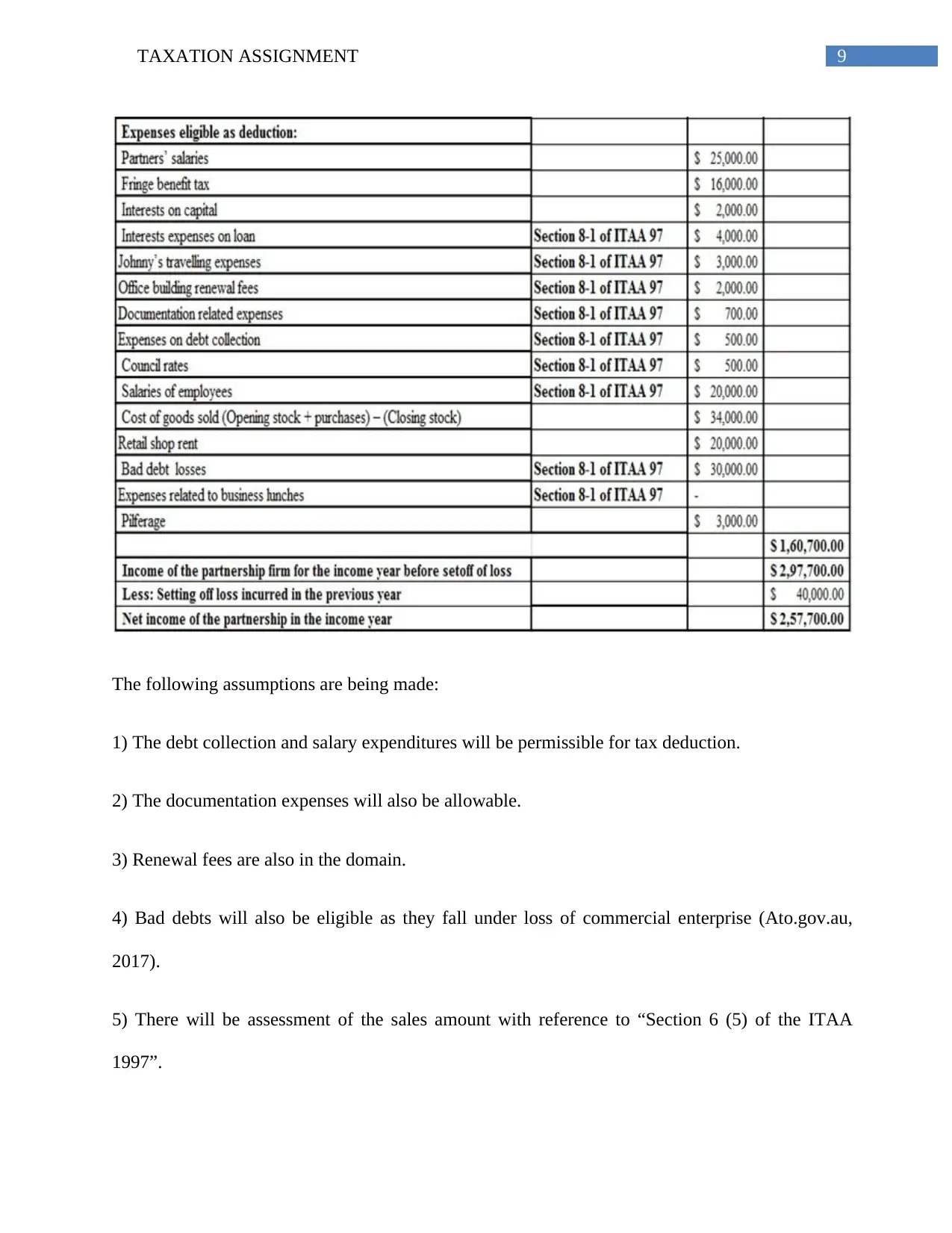

The assignment content discusses three different scenarios related to legal expenditures of solicitor hiring, input tax credit claim for advertisement costs, and computation of taxable income. In the first scenario, it is concluded that the expenses of solicitor hiring for commercial functionalities will be treated as allowable deductions with reference to Section 8(1) of the ITAA 1997. The second scenario deals with the issue of claiming input tax credits by a Big Bank regarding their advertisement costs, and it is concluded that only partial credibility can be claimed due to exceeding the threshold amount. The third scenario computes the taxable income of Angela, assuming debt collection and salary expenditures are permissible for tax deduction, documentation expenses are allowable, renewal fees are eligible, bad debts fall under loss of commercial enterprise, and sales amount is assessed with reference to Section 6(5) of the ITAA 1997.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)