HI6028 Taxation Assignment: Capital Gains, Fringe Benefits Analysis

VerifiedAdded on 2019/09/25

|11

|2619

|137

Report

AI Summary

This report, prepared for a taxation assignment, delves into two key areas: capital gains tax and fringe benefits tax. The first case study examines Fred's capital gains from selling a holiday home, detailing the calculation of taxable income using both discount and indexation methods, considering acquisition costs, legal fees, and capital losses. The second case study focuses on fringe benefits, exploring the tax implications of benefits such as company cars and interest-free loans provided to employees, specifically Emma. The report calculates fringe benefit values based on car expenses and loan amounts. It addresses the taxability of these benefits and the relevant provisions of the Income Tax Assessment Act, providing a comprehensive analysis of tax liabilities for both the individual and the employer. The report also covers the importance of maintaining proper documentation for tax purposes.

Running Head: TAXATION ASSIGNMENT

HI6028 TAXATION ASSIGNMENT

[Document subtitle]

HI6028 TAXATION ASSIGNMENT

[Document subtitle]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION ASSIGNMENT 1

Contents

Case Study 1: Capital Gain Taxation...............................................................................................2

Case Study 2: Fringe Benefits.........................................................................................................7

REFERENCES..............................................................................................................................11

Contents

Case Study 1: Capital Gain Taxation...............................................................................................2

Case Study 2: Fringe Benefits.........................................................................................................7

REFERENCES..............................................................................................................................11

TAXATION ASSIGNMENT 2

Case Study 1: Capital Gain Taxation

FACTS:

Fred is an assessee of a resident.

He has sold a home of Holiday. It means he has a residence where he actually resides.

The holiday home is situated in the Blue Mountain.

The agreement of sale occurred in the month of August of 2015.

The consideration of actual sales was received in the month of February of 2016.

The consideration of sales was $ 8, 00, 000.

The cost which was occurred in order to sell the property of house was $1100 (the legal

fee is comprehensive of the tax of goods and services).

The purchase was done in the month of March of 1987.

The cost of the property of house in order to purchase was $10000.

The stamp duty which was paid on the purchase of the house property was $2000

(consideration is 2 %).

The fees which were paid legally was $2000.

Fred also has capital loss worth $10, 000.

The loss of capital occurred because of the sale of shares.

ASSUMPTIONS:

The property of the house is situated within the authorities of taxation.

According to revenue authorities, the year of assessment begins from July 1 and ends

June 30.

An assessee lives in his residence which is unlike the Holiday home.

Case Study 1: Capital Gain Taxation

FACTS:

Fred is an assessee of a resident.

He has sold a home of Holiday. It means he has a residence where he actually resides.

The holiday home is situated in the Blue Mountain.

The agreement of sale occurred in the month of August of 2015.

The consideration of actual sales was received in the month of February of 2016.

The consideration of sales was $ 8, 00, 000.

The cost which was occurred in order to sell the property of house was $1100 (the legal

fee is comprehensive of the tax of goods and services).

The purchase was done in the month of March of 1987.

The cost of the property of house in order to purchase was $10000.

The stamp duty which was paid on the purchase of the house property was $2000

(consideration is 2 %).

The fees which were paid legally was $2000.

Fred also has capital loss worth $10, 000.

The loss of capital occurred because of the sale of shares.

ASSUMPTIONS:

The property of the house is situated within the authorities of taxation.

According to revenue authorities, the year of assessment begins from July 1 and ends

June 30.

An assessee lives in his residence which is unlike the Holiday home.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION ASSIGNMENT 3

An assessee has not invested further from the consideration of sale in order to save the

tax.

ANSWER

Taxation point, August 2015. According to the Income Tax Assessment Act 1937, the taxation

point in the case of selling the properties of real estate unlike the ones who held it in order to use

it personally during the time of registration of the contract agreement with the local authorities.

It becomes difficult for the Fred in order to find the taxation point of an event of Capital Gain

Taxation. It has some implications in order to calculate the tax liability.

In the given case, the contract agreement for the sale of the property was registered in the month

of August of 2015. Therefore, the liability of capital gain taxation begins from the year of

assessment i.e. 2016-17 which means the financial year 2015-16. The liabilities have to be paid

in the particular year when the settlement takes place. In the given case, the settlement was done

in the month of February of 2016. The capital gain tax payment will be paid in the assessment

year 2016-17.

The property of the house which is taxable is owned for the time period of more than 12 months.

There are two methods which can be used in order to compute the capital gain taxation i.e. the

method of discount and indexation (Harding, M. 2013).

Further, the table shows the computation by using both the methods:

DISCOUNT METHOD

Consideration of sale 800000

Less cost incurred Legal expenses (1100)

An assessee has not invested further from the consideration of sale in order to save the

tax.

ANSWER

Taxation point, August 2015. According to the Income Tax Assessment Act 1937, the taxation

point in the case of selling the properties of real estate unlike the ones who held it in order to use

it personally during the time of registration of the contract agreement with the local authorities.

It becomes difficult for the Fred in order to find the taxation point of an event of Capital Gain

Taxation. It has some implications in order to calculate the tax liability.

In the given case, the contract agreement for the sale of the property was registered in the month

of August of 2015. Therefore, the liability of capital gain taxation begins from the year of

assessment i.e. 2016-17 which means the financial year 2015-16. The liabilities have to be paid

in the particular year when the settlement takes place. In the given case, the settlement was done

in the month of February of 2016. The capital gain tax payment will be paid in the assessment

year 2016-17.

The property of the house which is taxable is owned for the time period of more than 12 months.

There are two methods which can be used in order to compute the capital gain taxation i.e. the

method of discount and indexation (Harding, M. 2013).

Further, the table shows the computation by using both the methods:

DISCOUNT METHOD

Consideration of sale 800000

Less cost incurred Legal expenses (1100)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION ASSIGNMENT 4

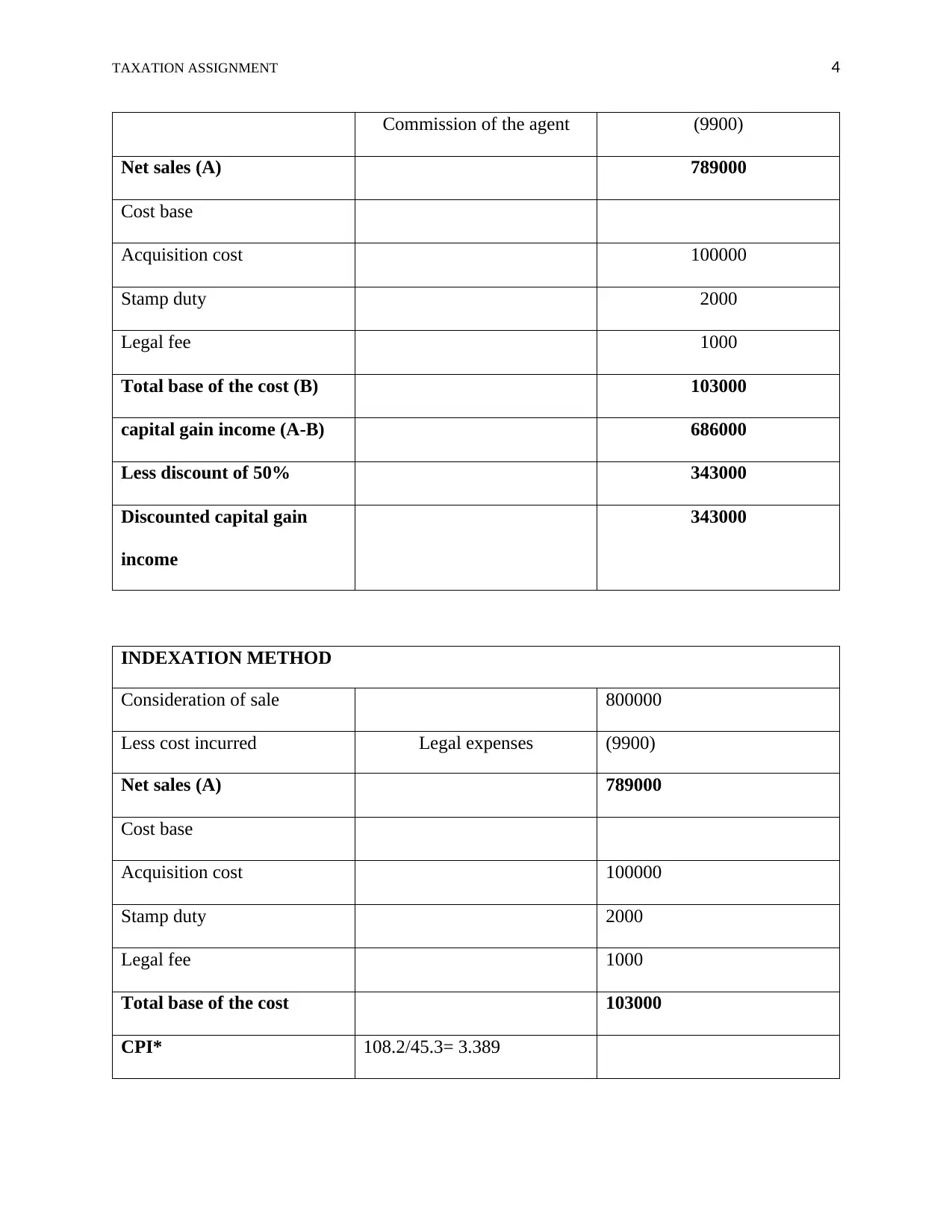

Commission of the agent (9900)

Net sales (A) 789000

Cost base

Acquisition cost 100000

Stamp duty 2000

Legal fee 1000

Total base of the cost (B) 103000

capital gain income (A-B) 686000

Less discount of 50% 343000

Discounted capital gain

income

343000

INDEXATION METHOD

Consideration of sale 800000

Less cost incurred Legal expenses (9900)

Net sales (A) 789000

Cost base

Acquisition cost 100000

Stamp duty 2000

Legal fee 1000

Total base of the cost 103000

CPI* 108.2/45.3= 3.389

Commission of the agent (9900)

Net sales (A) 789000

Cost base

Acquisition cost 100000

Stamp duty 2000

Legal fee 1000

Total base of the cost (B) 103000

capital gain income (A-B) 686000

Less discount of 50% 343000

Discounted capital gain

income

343000

INDEXATION METHOD

Consideration of sale 800000

Less cost incurred Legal expenses (9900)

Net sales (A) 789000

Cost base

Acquisition cost 100000

Stamp duty 2000

Legal fee 1000

Total base of the cost 103000

CPI* 108.2/45.3= 3.389

TAXATION ASSIGNMENT 5

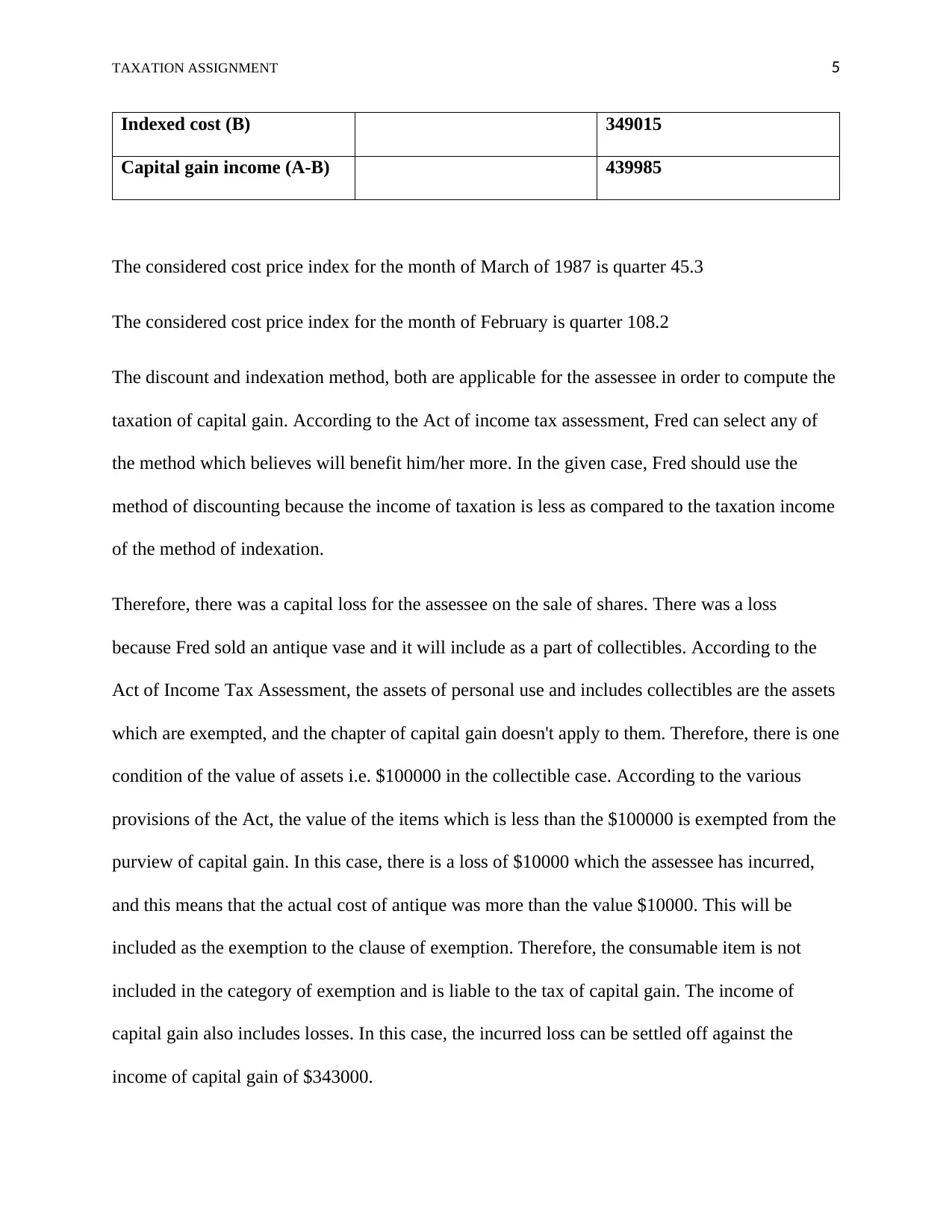

Indexed cost (B) 349015

Capital gain income (A-B) 439985

The considered cost price index for the month of March of 1987 is quarter 45.3

The considered cost price index for the month of February is quarter 108.2

The discount and indexation method, both are applicable for the assessee in order to compute the

taxation of capital gain. According to the Act of income tax assessment, Fred can select any of

the method which believes will benefit him/her more. In the given case, Fred should use the

method of discounting because the income of taxation is less as compared to the taxation income

of the method of indexation.

Therefore, there was a capital loss for the assessee on the sale of shares. There was a loss

because Fred sold an antique vase and it will include as a part of collectibles. According to the

Act of Income Tax Assessment, the assets of personal use and includes collectibles are the assets

which are exempted, and the chapter of capital gain doesn't apply to them. Therefore, there is one

condition of the value of assets i.e. $100000 in the collectible case. According to the various

provisions of the Act, the value of the items which is less than the $100000 is exempted from the

purview of capital gain. In this case, there is a loss of $10000 which the assessee has incurred,

and this means that the actual cost of antique was more than the value $10000. This will be

included as the exemption to the clause of exemption. Therefore, the consumable item is not

included in the category of exemption and is liable to the tax of capital gain. The income of

capital gain also includes losses. In this case, the incurred loss can be settled off against the

income of capital gain of $343000.

Indexed cost (B) 349015

Capital gain income (A-B) 439985

The considered cost price index for the month of March of 1987 is quarter 45.3

The considered cost price index for the month of February is quarter 108.2

The discount and indexation method, both are applicable for the assessee in order to compute the

taxation of capital gain. According to the Act of income tax assessment, Fred can select any of

the method which believes will benefit him/her more. In the given case, Fred should use the

method of discounting because the income of taxation is less as compared to the taxation income

of the method of indexation.

Therefore, there was a capital loss for the assessee on the sale of shares. There was a loss

because Fred sold an antique vase and it will include as a part of collectibles. According to the

Act of Income Tax Assessment, the assets of personal use and includes collectibles are the assets

which are exempted, and the chapter of capital gain doesn't apply to them. Therefore, there is one

condition of the value of assets i.e. $100000 in the collectible case. According to the various

provisions of the Act, the value of the items which is less than the $100000 is exempted from the

purview of capital gain. In this case, there is a loss of $10000 which the assessee has incurred,

and this means that the actual cost of antique was more than the value $10000. This will be

included as the exemption to the clause of exemption. Therefore, the consumable item is not

included in the category of exemption and is liable to the tax of capital gain. The income of

capital gain also includes losses. In this case, the incurred loss can be settled off against the

income of capital gain of $343000.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION ASSIGNMENT 6

The loss which was incurred on the sale of the vase which was antique will not make any

difference in the income because the taxable income is same.

If the authorities of revenue overlook the case, Fred the assessee is liable in order to generate all

required documents which will justify the consideration of sales or the cost of purchase of the

asset of capital gain. If the assessee fails in order to this, then the department of revenue can

generate the demand which will be paid with the required interest and penalty. It is advisable in

order to keep the file which will be containing all the important documents in order to justify the

income which will be shown at the end of the year. It has been mentioned in the law that it is

compulsory to maintain the laws in any language which can be easily translated to the English

language.

There are some records which are to be maintained in the taxation of capital gain by the assessee

and the records are as follows (Stanley, J., & McCue, P. 2014):

The receipts of acknowledgment while purchasing or transferring the property.

Borrowed money. The expended interest which is related to the sold assets in the working

capital gain.

Bills or any other important papers in order to justify the payment to the agents, legal

advisors, etc. and another cost which is incurred in advertising.

Receipts of the insurance premium paid and the various other taxes and rates.

Reports of valuation by the registered and recognized valuers of the income tax.

Repairing works job card or the contracts of maintenance.

Statements of the bank which will reinforce the above-given transactions.

The loss which was incurred on the sale of the vase which was antique will not make any

difference in the income because the taxable income is same.

If the authorities of revenue overlook the case, Fred the assessee is liable in order to generate all

required documents which will justify the consideration of sales or the cost of purchase of the

asset of capital gain. If the assessee fails in order to this, then the department of revenue can

generate the demand which will be paid with the required interest and penalty. It is advisable in

order to keep the file which will be containing all the important documents in order to justify the

income which will be shown at the end of the year. It has been mentioned in the law that it is

compulsory to maintain the laws in any language which can be easily translated to the English

language.

There are some records which are to be maintained in the taxation of capital gain by the assessee

and the records are as follows (Stanley, J., & McCue, P. 2014):

The receipts of acknowledgment while purchasing or transferring the property.

Borrowed money. The expended interest which is related to the sold assets in the working

capital gain.

Bills or any other important papers in order to justify the payment to the agents, legal

advisors, etc. and another cost which is incurred in advertising.

Receipts of the insurance premium paid and the various other taxes and rates.

Reports of valuation by the registered and recognized valuers of the income tax.

Repairing works job card or the contracts of maintenance.

Statements of the bank which will reinforce the above-given transactions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION ASSIGNMENT 7

Case Study 2: Fringe Benefits

If there is a payment transaction between the employee and the employer, then the income of

salary is taxable. If the amount is paid indirectly or directly by the employee to the employee,

then it is to be shown as the salary income of the employee. Most of the time, in multi-national

or big organizations the employers provide various facilities to their employees apart from the

package of salary, for example, house, car, etc. in order to build the reputation of the

organization. These are measured as the fringe benefits which are further included in the taxable

income of salary. Therefore, it can also be understood in a way like it is a complete package of

salary which the employee gets from the employer in terms of company' scheme for

hospitalization, medical insurance, schemes for holidays, loans which are interest-free, pension

plans, etc. It is not important that there is a relation between the employee and employer (Soled

et al., 2016). The fringe benefits can be passed among the two contractors who are independent

and will also be the recipient of these benefits and will account the fair market value in order to

be accounted as part of taxable income. The different countries or states have the different

framework of the law for the taxation of fringe benefits. For example, in India, the taxation of

fringe benefits has been invalidated. Some of the benefits of category which are exempted are

medical facilities, taxes for federal employment, etc. (ATO, 2015).

In Australia, the taxation of fringe benefits is bear by the employer. The Act of income tax

assessment has demonstrated some provisions which are related to the taxability and

changeability of the taxation of fringe benefit (ATO, 2015).

In this case, the employee has received the car from the employer for the official use and in order

to commute from the home to office.

It has been assumed that the car might be from the categories which are given below:

Case Study 2: Fringe Benefits

If there is a payment transaction between the employee and the employer, then the income of

salary is taxable. If the amount is paid indirectly or directly by the employee to the employee,

then it is to be shown as the salary income of the employee. Most of the time, in multi-national

or big organizations the employers provide various facilities to their employees apart from the

package of salary, for example, house, car, etc. in order to build the reputation of the

organization. These are measured as the fringe benefits which are further included in the taxable

income of salary. Therefore, it can also be understood in a way like it is a complete package of

salary which the employee gets from the employer in terms of company' scheme for

hospitalization, medical insurance, schemes for holidays, loans which are interest-free, pension

plans, etc. It is not important that there is a relation between the employee and employer (Soled

et al., 2016). The fringe benefits can be passed among the two contractors who are independent

and will also be the recipient of these benefits and will account the fair market value in order to

be accounted as part of taxable income. The different countries or states have the different

framework of the law for the taxation of fringe benefits. For example, in India, the taxation of

fringe benefits has been invalidated. Some of the benefits of category which are exempted are

medical facilities, taxes for federal employment, etc. (ATO, 2015).

In Australia, the taxation of fringe benefits is bear by the employer. The Act of income tax

assessment has demonstrated some provisions which are related to the taxability and

changeability of the taxation of fringe benefit (ATO, 2015).

In this case, the employee has received the car from the employer for the official use and in order

to commute from the home to office.

It has been assumed that the car might be from the categories which are given below:

TAXATION ASSIGNMENT 8

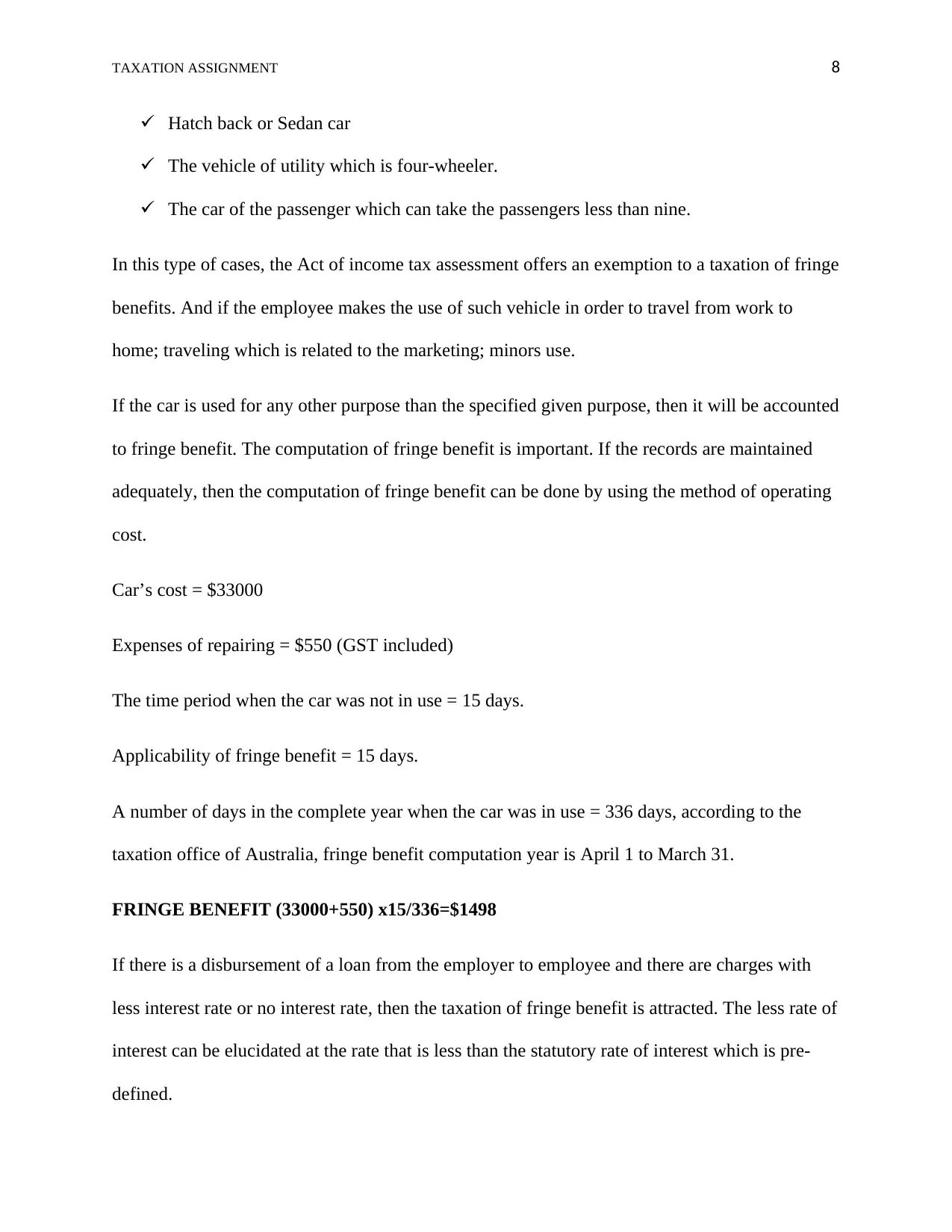

Hatch back or Sedan car

The vehicle of utility which is four-wheeler.

The car of the passenger which can take the passengers less than nine.

In this type of cases, the Act of income tax assessment offers an exemption to a taxation of fringe

benefits. And if the employee makes the use of such vehicle in order to travel from work to

home; traveling which is related to the marketing; minors use.

If the car is used for any other purpose than the specified given purpose, then it will be accounted

to fringe benefit. The computation of fringe benefit is important. If the records are maintained

adequately, then the computation of fringe benefit can be done by using the method of operating

cost.

Car’s cost = $33000

Expenses of repairing = $550 (GST included)

The time period when the car was not in use = 15 days.

Applicability of fringe benefit = 15 days.

A number of days in the complete year when the car was in use = 336 days, according to the

taxation office of Australia, fringe benefit computation year is April 1 to March 31.

FRINGE BENEFIT (33000+550) x15/336=$1498

If there is a disbursement of a loan from the employer to employee and there are charges with

less interest rate or no interest rate, then the taxation of fringe benefit is attracted. The less rate of

interest can be elucidated at the rate that is less than the statutory rate of interest which is pre-

defined.

Hatch back or Sedan car

The vehicle of utility which is four-wheeler.

The car of the passenger which can take the passengers less than nine.

In this type of cases, the Act of income tax assessment offers an exemption to a taxation of fringe

benefits. And if the employee makes the use of such vehicle in order to travel from work to

home; traveling which is related to the marketing; minors use.

If the car is used for any other purpose than the specified given purpose, then it will be accounted

to fringe benefit. The computation of fringe benefit is important. If the records are maintained

adequately, then the computation of fringe benefit can be done by using the method of operating

cost.

Car’s cost = $33000

Expenses of repairing = $550 (GST included)

The time period when the car was not in use = 15 days.

Applicability of fringe benefit = 15 days.

A number of days in the complete year when the car was in use = 336 days, according to the

taxation office of Australia, fringe benefit computation year is April 1 to March 31.

FRINGE BENEFIT (33000+550) x15/336=$1498

If there is a disbursement of a loan from the employer to employee and there are charges with

less interest rate or no interest rate, then the taxation of fringe benefit is attracted. The less rate of

interest can be elucidated at the rate that is less than the statutory rate of interest which is pre-

defined.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TAXATION ASSIGNMENT 9

It is important to understand the usage of the loan with its purpose and nature. The forms of

advance salary and the loan's part to the employee will fall in the purview of taxation of fringe

benefit.

The computation of fringe benefit is given below-

The difference among the interest rate which is statutory and prevails in the market which can be

determinate by the bank of Apex and the lending rate which is being offered by the bank which

is nationalized and the interest which is actual will be accrued from the end of the employee.

Emma has got a loan of $500000 from the employer who has been used in order to purchase the

private asset worth $450000 and the shares worth $50000 by the husband. These are used for the

personal use. The fringe benefit can also be used by the family of the employee. Therefore, in

this case, the benefit was diverted to the employee's husband. This further forms the taxation part

for the employer. The shares which were purchased by the employee were embraced in the

income generating asset. Therefore, in the given case, the interest cannot be allowed on the

benefit of the loan as a part of reduction to the fringe benefit.

FRINGE BENEFIT FOR LOAN = $500000 x213/366=$290984

The employer deals with bathtub trading. The price for the general public of the bathtub worth

$2600. The discount which was given to Emma worth $1300. There is no consideration of cost

price. The loss of opportunity is the advantage for the employer.

FRINGE BENEFIT IN THE GIVEN CASE IS $1300

The shares which were purchased by the employee, the cost of interest (500000 x 4.5%*213/366

x 50000/500000 will be deducted from the fringe benefit i.e. $13094

Net fringe benefit = 290984 – 13094 = $277890

It is important to understand the usage of the loan with its purpose and nature. The forms of

advance salary and the loan's part to the employee will fall in the purview of taxation of fringe

benefit.

The computation of fringe benefit is given below-

The difference among the interest rate which is statutory and prevails in the market which can be

determinate by the bank of Apex and the lending rate which is being offered by the bank which

is nationalized and the interest which is actual will be accrued from the end of the employee.

Emma has got a loan of $500000 from the employer who has been used in order to purchase the

private asset worth $450000 and the shares worth $50000 by the husband. These are used for the

personal use. The fringe benefit can also be used by the family of the employee. Therefore, in

this case, the benefit was diverted to the employee's husband. This further forms the taxation part

for the employer. The shares which were purchased by the employee were embraced in the

income generating asset. Therefore, in the given case, the interest cannot be allowed on the

benefit of the loan as a part of reduction to the fringe benefit.

FRINGE BENEFIT FOR LOAN = $500000 x213/366=$290984

The employer deals with bathtub trading. The price for the general public of the bathtub worth

$2600. The discount which was given to Emma worth $1300. There is no consideration of cost

price. The loss of opportunity is the advantage for the employer.

FRINGE BENEFIT IN THE GIVEN CASE IS $1300

The shares which were purchased by the employee, the cost of interest (500000 x 4.5%*213/366

x 50000/500000 will be deducted from the fringe benefit i.e. $13094

Net fringe benefit = 290984 – 13094 = $277890

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION ASSIGNMENT 10

The compensation of authorities of revenue from the planning of tax was done by the fringe

benefits taxation by the big organization. The organizations used to provide various packages of

salary which contains more fringe benefits than the salary. The employees can file for a low rate

of return on income. The government found the leakage in the revenue and established the

taxation of fringe benefit which was charged on the employer for the convenience of

administration. According to the provision of on –compliance, the organization is liable for the

provisions of penalty and interests. It is necessary for the employees and employers to maintain

the records in order to file the return on fringe benefit. In the case of scrutiny, these records will

be shown to the authorities of revenue. Therefore, after the establishment of FBT, various mal

practices can now be avoided (Faccio, M., & Xu, J. 2015).

The compensation of authorities of revenue from the planning of tax was done by the fringe

benefits taxation by the big organization. The organizations used to provide various packages of

salary which contains more fringe benefits than the salary. The employees can file for a low rate

of return on income. The government found the leakage in the revenue and established the

taxation of fringe benefit which was charged on the employer for the convenience of

administration. According to the provision of on –compliance, the organization is liable for the

provisions of penalty and interests. It is necessary for the employees and employers to maintain

the records in order to file the return on fringe benefit. In the case of scrutiny, these records will

be shown to the authorities of revenue. Therefore, after the establishment of FBT, various mal

practices can now be avoided (Faccio, M., & Xu, J. 2015).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.