UK Taxation: Personal and Capital Gains Tax Analysis of Nina & Patrick

VerifiedAdded on 2020/09/17

|10

|2368

|32

Homework Assignment

AI Summary

This assignment delves into the UK taxation system, analyzing the tax liabilities of Nina and Patrick under various scenarios. It begins with a personal tax computation for Nina, a sole trader, and Patrick, an employee, calculating their income tax and National Insurance contributions. The assignment then explores the impact of increasing Patrick's salary and the implications of forming a partnership, recalculating tax liabilities under each scenario. Finally, it examines capital gains tax arising from the sale of a factory and plant & machinery, including the application of capital gains tax relief. The analysis covers income tax, National Insurance contributions, and capital gains tax, providing a comprehensive overview of UK taxation principles and their application to specific financial situations. The assignment highlights the importance of strategic financial planning to minimize tax liabilities and maximize net income, referencing relevant tax regulations and case studies.

TAXATION

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................3

(A)...........................................................................................................................................3

(B)...........................................................................................................................................3

PART 3............................................................................................................................................5

(A)...........................................................................................................................................5

(B)...........................................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

PART 1............................................................................................................................................1

PART 2............................................................................................................................................3

(A)...........................................................................................................................................3

(B)...........................................................................................................................................3

PART 3............................................................................................................................................5

(A)...........................................................................................................................................5

(B)...........................................................................................................................................7

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

In order to promote public welfare and economic growth, UK has a taxation system

wherein various kinds of taxes are being charged by the government such as income tax,

corporate tax, capital gain tax and many others. UK government obtain maximum revenue

through income tax evidencing it from the year 2016/17, it had collected total of £182 billion

(Income tax, 2016). Income tax is levied by the government on personal income of the

individual. It follows progressive structure wherein as the level of income increases, tax rates

also goes up. The current assignment study will apply various taxation rules and regulations to

determine tax liabilities.

PART 1

Personal tax computation

As per the case study provided, Nina Simon (Aged 43) had married Patrick (Aged 46)

and has two children, Suzie (aged 16) and Anthony (aged 14). Patrick is playing the role of

administrator and dealing duties around payroll, bookkeeping and debtor/creditor management.

According to the draft budget, expected budgeted figure for the year ended 5th April 2017 is

£198,300 and Patrick is getting a salary of £28,000 during this period. Personal tax liability of

both Nina and Patrick is performed below:

For taxation year 2016/17, sole trader’s tax-free allowance is £11,000 but subjected to the

restriction that income must not go beyond the total limit of £100,000. The tax band for the sole

trader is as follows:

Band Taxable income Taxation rate

Basic rate £0 to £32,000 20%

Higher rate £32,001-£150,000 40%

Additional rate Over £150,000 45%

Being a sole trader; it is necessary for Nina to register herself under National Insurance

Contribution with HMRC (Her Majesty Revenue and Custom) and pay class 2 & class 4 NICs if

profit goes beyond the limit of £5,965 and £8,060 a year for FY 2016/17.

Personal tax contribution of Nina Simon

Particulars Working Amount

Page 1 of 13

In order to promote public welfare and economic growth, UK has a taxation system

wherein various kinds of taxes are being charged by the government such as income tax,

corporate tax, capital gain tax and many others. UK government obtain maximum revenue

through income tax evidencing it from the year 2016/17, it had collected total of £182 billion

(Income tax, 2016). Income tax is levied by the government on personal income of the

individual. It follows progressive structure wherein as the level of income increases, tax rates

also goes up. The current assignment study will apply various taxation rules and regulations to

determine tax liabilities.

PART 1

Personal tax computation

As per the case study provided, Nina Simon (Aged 43) had married Patrick (Aged 46)

and has two children, Suzie (aged 16) and Anthony (aged 14). Patrick is playing the role of

administrator and dealing duties around payroll, bookkeeping and debtor/creditor management.

According to the draft budget, expected budgeted figure for the year ended 5th April 2017 is

£198,300 and Patrick is getting a salary of £28,000 during this period. Personal tax liability of

both Nina and Patrick is performed below:

For taxation year 2016/17, sole trader’s tax-free allowance is £11,000 but subjected to the

restriction that income must not go beyond the total limit of £100,000. The tax band for the sole

trader is as follows:

Band Taxable income Taxation rate

Basic rate £0 to £32,000 20%

Higher rate £32,001-£150,000 40%

Additional rate Over £150,000 45%

Being a sole trader; it is necessary for Nina to register herself under National Insurance

Contribution with HMRC (Her Majesty Revenue and Custom) and pay class 2 & class 4 NICs if

profit goes beyond the limit of £5,965 and £8,060 a year for FY 2016/17.

Personal tax contribution of Nina Simon

Particulars Working Amount

Page 1 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Expected trading profit for the

year 2016/17

£198,300

Less: Tax

Personal tax allowance Not available because

198300>100,000

-

Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £48,300*45% £21,735

Total tax liability due £75,335

National Insurance

Contribution

Class 2 NICs£198,300>£5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% (£198,300 - £43,000)*2% £3,106

Total NICs £6,396.2

Total deductions £81731.2

Net income £116,568.8

Personal tax contribution of Patrick

Particulars Working Amount

Income from salary £28,000

Less: Tax-free allowance £11,000

Taxable amount £17,000

Tax

£0 to £32,000@20% £17,000*20% £3,400

National Insurance

contribution (NIC)

(£28,000-£8040)*12% £2,392.8

Page 2 of 13

year 2016/17

£198,300

Less: Tax

Personal tax allowance Not available because

198300>100,000

-

Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £48,300*45% £21,735

Total tax liability due £75,335

National Insurance

Contribution

Class 2 NICs£198,300>£5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% (£198,300 - £43,000)*2% £3,106

Total NICs £6,396.2

Total deductions £81731.2

Net income £116,568.8

Personal tax contribution of Patrick

Particulars Working Amount

Income from salary £28,000

Less: Tax-free allowance £11,000

Taxable amount £17,000

Tax

£0 to £32,000@20% £17,000*20% £3,400

National Insurance

contribution (NIC)

(£28,000-£8040)*12% £2,392.8

Page 2 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total deductions £5,792.8

Net income £22,207.2

PART 2

(A).

If Patrick’s salary is increased by £25,000 with total salary of £53,000, then Nina would

be able to minimize its trading profit further by £25,000. Thus, due to the reduction of trading

profit from the business, she can reduce its taxation liability by (£25,000*45%) = £11,250 shows

a significant decline (Boczko, 2016). Thus, it is a way available to her to reduce its taxation

liability. However, on the other side, paying high salary above the market rate will increase

Patrick’s taxable income and as a result, he would need to pay high tax. In such case, Patrick will

need to pay 20% on £15000 and on rest £10,000, he will pay an increased tax rate @ 40%.

(B).

Partnership is a business that is owned, administrated and managed by two or more

person. All the partners run the business jointly and held combined responsibility to run the

operation and share profits equally or in agreed profit/loss sharing ratio. All the partners are

accountable to pay income tax on their respected profit gained (Browne and Phillips, 2017). In

the given situation, Nina can involve Patrick as a partner in the business from 6th April 2016 and

after the partnership, business profit will be share in the ratio of 70:30. The rate of income tax for

partners is mentioned below:

Taxable income (FY 2016/17) Rate

£0 to £32,000 20%

£32,001-£150,000 40%

Above £150,000 45%

In UK, Partners usually pay NIC on their respected profitability share from the

partnership. It is a compulsory or mandatory payment required to be made by them against

certain state based benefits (Egger and et.al., 2015). Individuals above 16 years need to make

contribution to NI at following rates:

Type of NI

contribution

Amount needs to be paid for FY 2016/17

Page 3 of 13

Net income £22,207.2

PART 2

(A).

If Patrick’s salary is increased by £25,000 with total salary of £53,000, then Nina would

be able to minimize its trading profit further by £25,000. Thus, due to the reduction of trading

profit from the business, she can reduce its taxation liability by (£25,000*45%) = £11,250 shows

a significant decline (Boczko, 2016). Thus, it is a way available to her to reduce its taxation

liability. However, on the other side, paying high salary above the market rate will increase

Patrick’s taxable income and as a result, he would need to pay high tax. In such case, Patrick will

need to pay 20% on £15000 and on rest £10,000, he will pay an increased tax rate @ 40%.

(B).

Partnership is a business that is owned, administrated and managed by two or more

person. All the partners run the business jointly and held combined responsibility to run the

operation and share profits equally or in agreed profit/loss sharing ratio. All the partners are

accountable to pay income tax on their respected profit gained (Browne and Phillips, 2017). In

the given situation, Nina can involve Patrick as a partner in the business from 6th April 2016 and

after the partnership, business profit will be share in the ratio of 70:30. The rate of income tax for

partners is mentioned below:

Taxable income (FY 2016/17) Rate

£0 to £32,000 20%

£32,001-£150,000 40%

Above £150,000 45%

In UK, Partners usually pay NIC on their respected profitability share from the

partnership. It is a compulsory or mandatory payment required to be made by them against

certain state based benefits (Egger and et.al., 2015). Individuals above 16 years need to make

contribution to NI at following rates:

Type of NI

contribution

Amount needs to be paid for FY 2016/17

Page 3 of 13

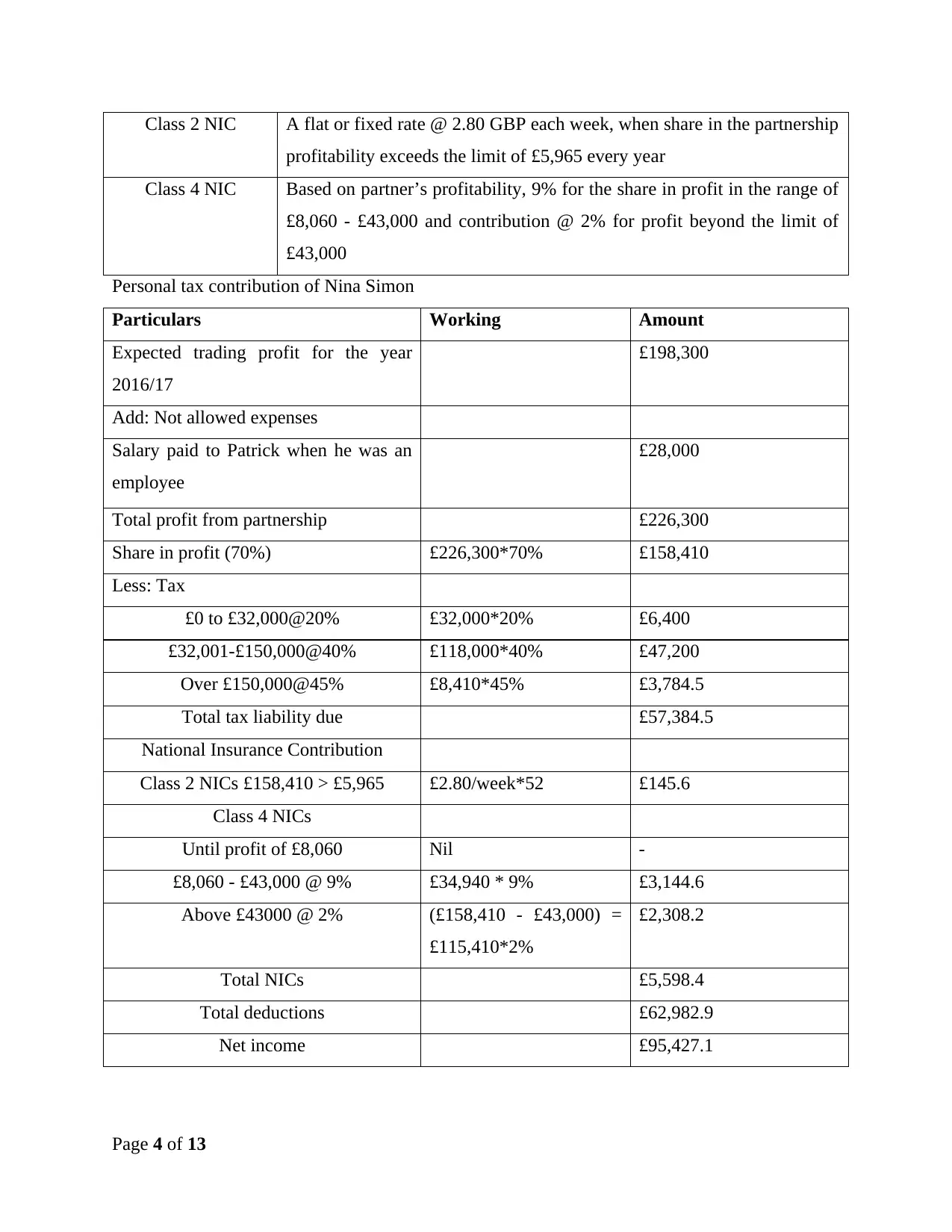

Class 2 NIC A flat or fixed rate @ 2.80 GBP each week, when share in the partnership

profitability exceeds the limit of £5,965 every year

Class 4 NIC Based on partner’s profitability, 9% for the share in profit in the range of

£8,060 - £43,000 and contribution @ 2% for profit beyond the limit of

£43,000

Personal tax contribution of Nina Simon

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: Not allowed expenses

Salary paid to Patrick when he was an

employee

£28,000

Total profit from partnership £226,300

Share in profit (70%) £226,300*70% £158,410

Less: Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £8,410*45% £3,784.5

Total tax liability due £57,384.5

National Insurance Contribution

Class 2 NICs £158,410 > £5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% (£158,410 - £43,000) =

£115,410*2%

£2,308.2

Total NICs £5,598.4

Total deductions £62,982.9

Net income £95,427.1

Page 4 of 13

profitability exceeds the limit of £5,965 every year

Class 4 NIC Based on partner’s profitability, 9% for the share in profit in the range of

£8,060 - £43,000 and contribution @ 2% for profit beyond the limit of

£43,000

Personal tax contribution of Nina Simon

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: Not allowed expenses

Salary paid to Patrick when he was an

employee

£28,000

Total profit from partnership £226,300

Share in profit (70%) £226,300*70% £158,410

Less: Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £8,410*45% £3,784.5

Total tax liability due £57,384.5

National Insurance Contribution

Class 2 NICs £158,410 > £5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% (£158,410 - £43,000) =

£115,410*2%

£2,308.2

Total NICs £5,598.4

Total deductions £62,982.9

Net income £95,427.1

Page 4 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

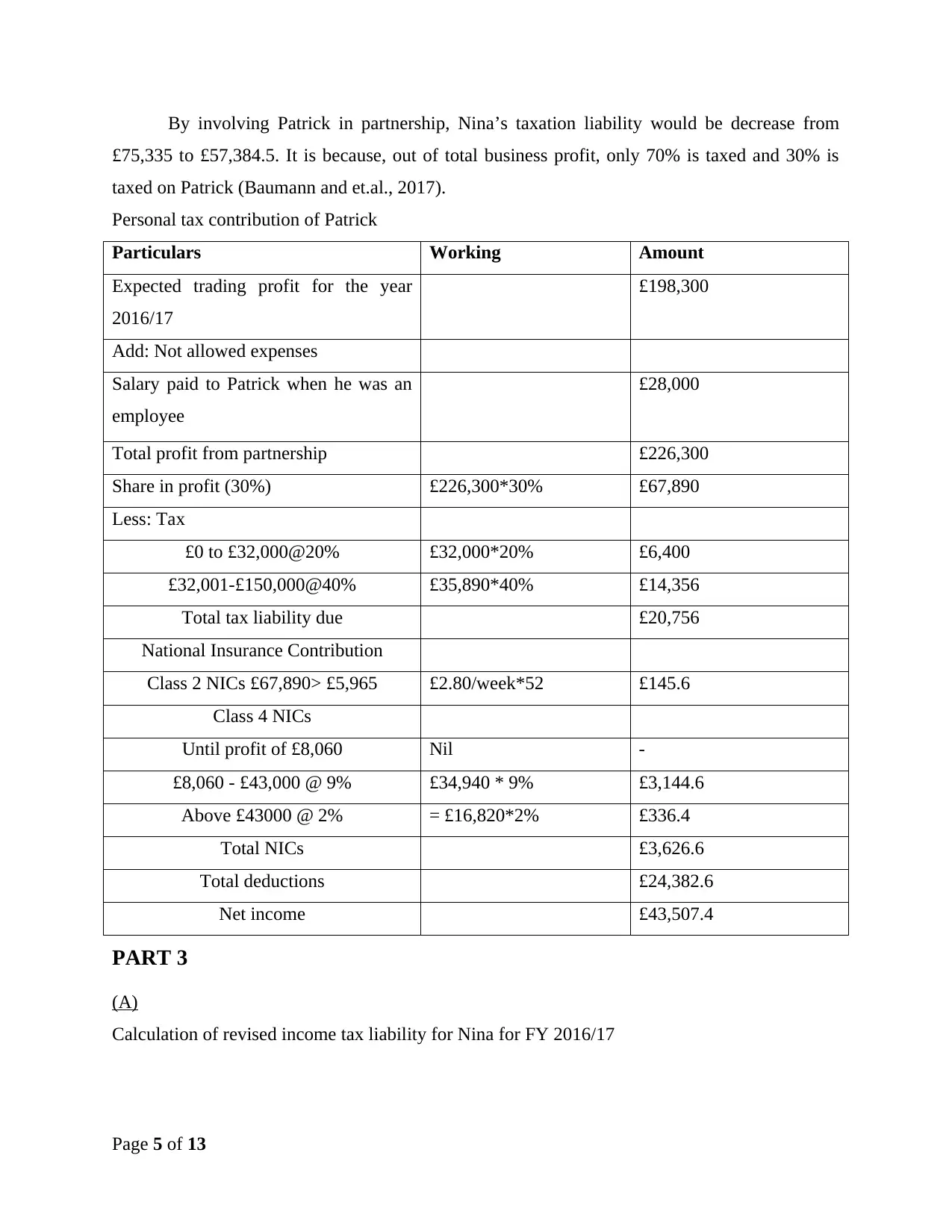

By involving Patrick in partnership, Nina’s taxation liability would be decrease from

£75,335 to £57,384.5. It is because, out of total business profit, only 70% is taxed and 30% is

taxed on Patrick (Baumann and et.al., 2017).

Personal tax contribution of Patrick

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: Not allowed expenses

Salary paid to Patrick when he was an

employee

£28,000

Total profit from partnership £226,300

Share in profit (30%) £226,300*30% £67,890

Less: Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £35,890*40% £14,356

Total tax liability due £20,756

National Insurance Contribution

Class 2 NICs £67,890> £5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% = £16,820*2% £336.4

Total NICs £3,626.6

Total deductions £24,382.6

Net income £43,507.4

PART 3

(A)

Calculation of revised income tax liability for Nina for FY 2016/17

Page 5 of 13

£75,335 to £57,384.5. It is because, out of total business profit, only 70% is taxed and 30% is

taxed on Patrick (Baumann and et.al., 2017).

Personal tax contribution of Patrick

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: Not allowed expenses

Salary paid to Patrick when he was an

employee

£28,000

Total profit from partnership £226,300

Share in profit (30%) £226,300*30% £67,890

Less: Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £35,890*40% £14,356

Total tax liability due £20,756

National Insurance Contribution

Class 2 NICs £67,890> £5,965 £2.80/week*52 £145.6

Class 4 NICs

Until profit of £8,060 Nil -

£8,060 - £43,000 @ 9% £34,940 * 9% £3,144.6

Above £43000 @ 2% = £16,820*2% £336.4

Total NICs £3,626.6

Total deductions £24,382.6

Net income £43,507.4

PART 3

(A)

Calculation of revised income tax liability for Nina for FY 2016/17

Page 5 of 13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

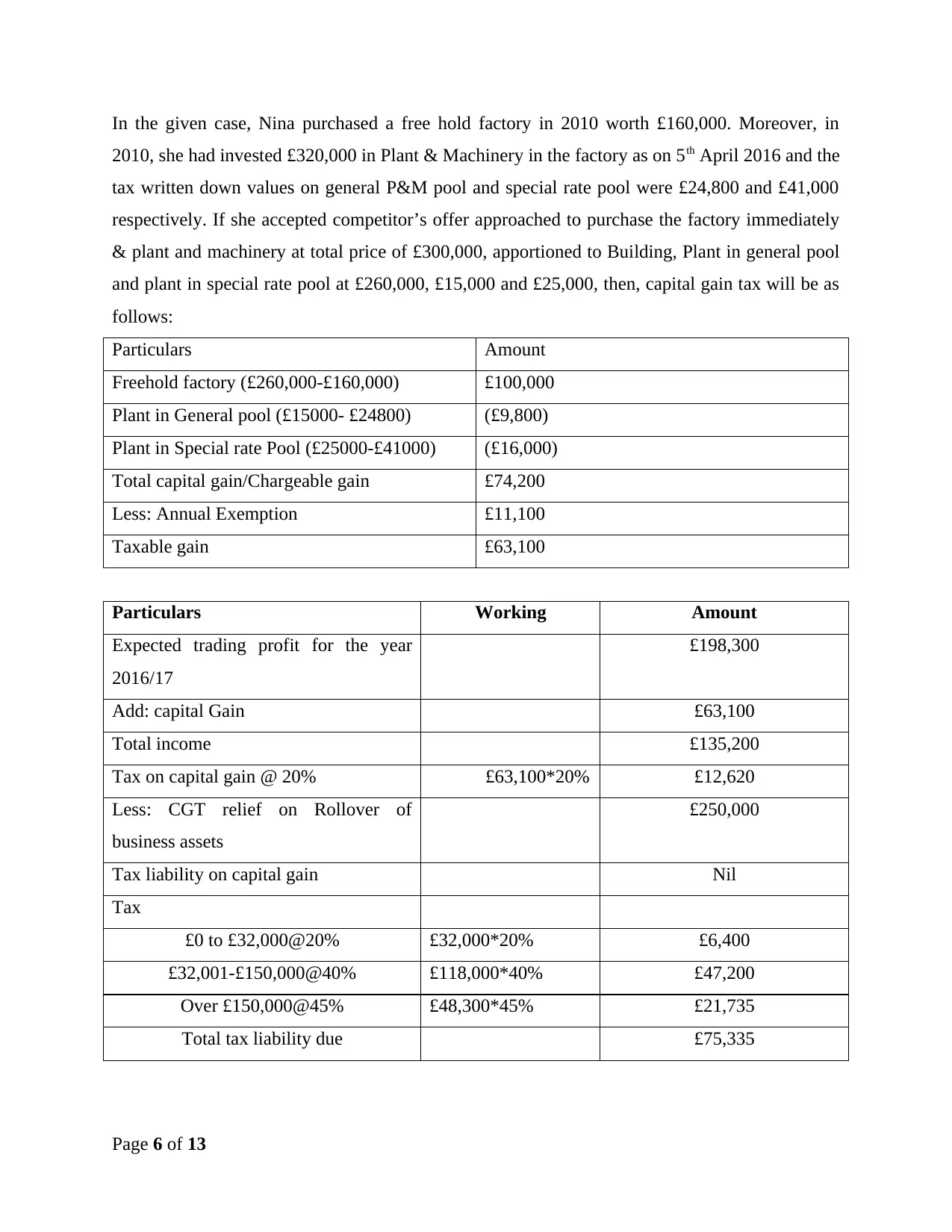

In the given case, Nina purchased a free hold factory in 2010 worth £160,000. Moreover, in

2010, she had invested £320,000 in Plant & Machinery in the factory as on 5th April 2016 and the

tax written down values on general P&M pool and special rate pool were £24,800 and £41,000

respectively. If she accepted competitor’s offer approached to purchase the factory immediately

& plant and machinery at total price of £300,000, apportioned to Building, Plant in general pool

and plant in special rate pool at £260,000, £15,000 and £25,000, then, capital gain tax will be as

follows:

Particulars Amount

Freehold factory (£260,000-£160,000) £100,000

Plant in General pool (£15000- £24800) (£9,800)

Plant in Special rate Pool (£25000-£41000) (£16,000)

Total capital gain/Chargeable gain £74,200

Less: Annual Exemption £11,100

Taxable gain £63,100

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: capital Gain £63,100

Total income £135,200

Tax on capital gain @ 20% £63,100*20% £12,620

Less: CGT relief on Rollover of

business assets

£250,000

Tax liability on capital gain Nil

Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £48,300*45% £21,735

Total tax liability due £75,335

Page 6 of 13

2010, she had invested £320,000 in Plant & Machinery in the factory as on 5th April 2016 and the

tax written down values on general P&M pool and special rate pool were £24,800 and £41,000

respectively. If she accepted competitor’s offer approached to purchase the factory immediately

& plant and machinery at total price of £300,000, apportioned to Building, Plant in general pool

and plant in special rate pool at £260,000, £15,000 and £25,000, then, capital gain tax will be as

follows:

Particulars Amount

Freehold factory (£260,000-£160,000) £100,000

Plant in General pool (£15000- £24800) (£9,800)

Plant in Special rate Pool (£25000-£41000) (£16,000)

Total capital gain/Chargeable gain £74,200

Less: Annual Exemption £11,100

Taxable gain £63,100

Particulars Working Amount

Expected trading profit for the year

2016/17

£198,300

Add: capital Gain £63,100

Total income £135,200

Tax on capital gain @ 20% £63,100*20% £12,620

Less: CGT relief on Rollover of

business assets

£250,000

Tax liability on capital gain Nil

Tax

£0 to £32,000@20% £32,000*20% £6,400

£32,001-£150,000@40% £118,000*40% £47,200

Over £150,000@45% £48,300*45% £21,735

Total tax liability due £75,335

Page 6 of 13

According to the calculations performed, there will be no impact on the new business

opportunity on Nina’s taxation liability because all the capital gain she used to replace other

factory and plant & machinery, hence, she would not be liable to pay any tax on the same

(Griffith, Hines and Sørensen, 2010). As a result, her tax liability remains fixed to that of earlier

worth £75,335.

(B)

As per capital gain calculation, she can get CGT relief on the plant in general and special

pool as she had incurred capital loss of £9,800 and £16,000 on such assets that can be set off

from the chargeable gain worth £100,000 on freehold property. Thus, overall, only chargeable

gain worth £74,200 will be taxed (Bankman and et.al., 2017).

CGT rules in UK provide relief on rollover/handover, as per which, if CGT is used to

replace with a new business assets before three years after the disposal then tax relief is available

on the same (Capital Gain Tax, 2017). Here, in the case, out of the money received through sale,

if she purchase a 52-year lease in nearby replacement factory worth £200,000 and additionally

pay a cost of £50,000, then, she can easily get tax relief on the same. Other CGT relief includes

rollover that is incorporation relief, means if chargeable assets is transferred to another company

for trade, Disincorporation means transfer of goodwill & land & property in business transfer to

shareholders (Capital Gains Tax relief, 2017). Besides this, entrepreneur’s relief and holdover

gifts are also the tax reliefs available on CGT.

CONCLUSION

From the discussion, it is clear that as per current situation, Nina and Patrick are liable to

pay tax worth £75,335 and £3,400. If she raised Patrick salary by £25,000, than Nina can reduce

its taxation liability by £11,250. However, if couple decided to make partnership agreement in

70:30, then Nina can reduce its taxation liability from £75,335 to £57,384.5 and Patrick would

need to pay tax worth £20,756. Lastly, it is examined that on capital gain, Nina is allowed to set

off losses on plant in general and special pool against profit earned on freehold property.

Moreover, she can get CGT relief on rollover of business assets.

Page 7 of 13

opportunity on Nina’s taxation liability because all the capital gain she used to replace other

factory and plant & machinery, hence, she would not be liable to pay any tax on the same

(Griffith, Hines and Sørensen, 2010). As a result, her tax liability remains fixed to that of earlier

worth £75,335.

(B)

As per capital gain calculation, she can get CGT relief on the plant in general and special

pool as she had incurred capital loss of £9,800 and £16,000 on such assets that can be set off

from the chargeable gain worth £100,000 on freehold property. Thus, overall, only chargeable

gain worth £74,200 will be taxed (Bankman and et.al., 2017).

CGT rules in UK provide relief on rollover/handover, as per which, if CGT is used to

replace with a new business assets before three years after the disposal then tax relief is available

on the same (Capital Gain Tax, 2017). Here, in the case, out of the money received through sale,

if she purchase a 52-year lease in nearby replacement factory worth £200,000 and additionally

pay a cost of £50,000, then, she can easily get tax relief on the same. Other CGT relief includes

rollover that is incorporation relief, means if chargeable assets is transferred to another company

for trade, Disincorporation means transfer of goodwill & land & property in business transfer to

shareholders (Capital Gains Tax relief, 2017). Besides this, entrepreneur’s relief and holdover

gifts are also the tax reliefs available on CGT.

CONCLUSION

From the discussion, it is clear that as per current situation, Nina and Patrick are liable to

pay tax worth £75,335 and £3,400. If she raised Patrick salary by £25,000, than Nina can reduce

its taxation liability by £11,250. However, if couple decided to make partnership agreement in

70:30, then Nina can reduce its taxation liability from £75,335 to £57,384.5 and Patrick would

need to pay tax worth £20,756. Lastly, it is examined that on capital gain, Nina is allowed to set

off losses on plant in general and special pool against profit earned on freehold property.

Moreover, she can get CGT relief on rollover of business assets.

Page 7 of 13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bankman, J., and et.al., 2017. Federal Income Taxation. Wolters Kluwer Law & Business.

Baumann, F., and et.al 2017. Tax enforcement and corporate profit shifting. Applied Economics

Letters. 24(13). pp.902-905.

Boczko, T., 2016. Managing Your Money: A Practical Guide to Personal Finance. Palgrave

Macmillan.

Browne, J. and Phillips, D., 2017. Estimating the size and nature of responses to changes in

income tax rates on top incomes in the UK: a panel analysis (No. W17/13). Institute for

Fiscal Studies.

Egger, P. and et.al., 2015. Consequences of the New UK Tax Exemption System: Evidence from

Micro‐level Data. The Economic Journal. 125(589). pp.1764-1789.

Griffith, R., Hines, J. and Sørensen, P.B., 2010. International capital taxation. Dimensions of Tax

Design: The Mirrlees Review. 6(3). pp. 914-996.

Online

Capital Gain Tax. 2017. [Online]. Available through:

<https://www.gov.uk/government/publications/rates-and-allowances-capital-gains-tax/

capital-gains-tax-rates-and-annual-tax-free-allowances>.

Capital Gains Tax reliefs. 2017. [Online]. Available through:

https://www.rossmartin.co.uk/private-client-a-estate-planning/capital-gains-tax/1495-

an-index-to-capital-gains-tax-reliefs.

Income tax. 2016. [Online]. Available through :< https://www.citizensadvice.org.uk/tax/income-

tax-how-much-should-you-pay/income-tax/#h-how-income-tax-is-calculated>.

Page 8 of 13

Books and Journals

Bankman, J., and et.al., 2017. Federal Income Taxation. Wolters Kluwer Law & Business.

Baumann, F., and et.al 2017. Tax enforcement and corporate profit shifting. Applied Economics

Letters. 24(13). pp.902-905.

Boczko, T., 2016. Managing Your Money: A Practical Guide to Personal Finance. Palgrave

Macmillan.

Browne, J. and Phillips, D., 2017. Estimating the size and nature of responses to changes in

income tax rates on top incomes in the UK: a panel analysis (No. W17/13). Institute for

Fiscal Studies.

Egger, P. and et.al., 2015. Consequences of the New UK Tax Exemption System: Evidence from

Micro‐level Data. The Economic Journal. 125(589). pp.1764-1789.

Griffith, R., Hines, J. and Sørensen, P.B., 2010. International capital taxation. Dimensions of Tax

Design: The Mirrlees Review. 6(3). pp. 914-996.

Online

Capital Gain Tax. 2017. [Online]. Available through:

<https://www.gov.uk/government/publications/rates-and-allowances-capital-gains-tax/

capital-gains-tax-rates-and-annual-tax-free-allowances>.

Capital Gains Tax reliefs. 2017. [Online]. Available through:

https://www.rossmartin.co.uk/private-client-a-estate-planning/capital-gains-tax/1495-

an-index-to-capital-gains-tax-reliefs.

Income tax. 2016. [Online]. Available through :< https://www.citizensadvice.org.uk/tax/income-

tax-how-much-should-you-pay/income-tax/#h-how-income-tax-is-calculated>.

Page 8 of 13

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.