ACCT 2301 Taxation Project: Computing Income, Liabilities and Advice

VerifiedAdded on 2023/05/28

|22

|1980

|344

Project

AI Summary

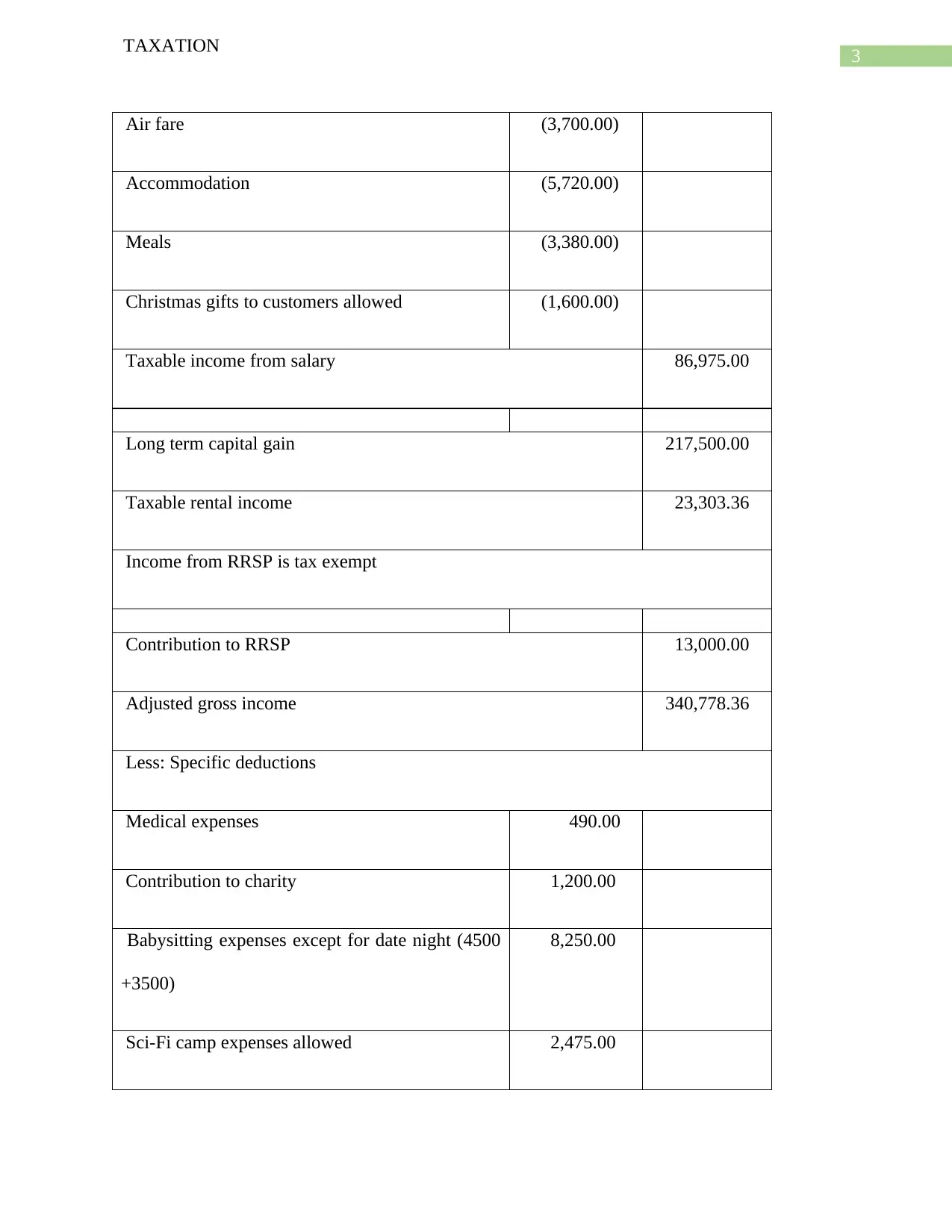

This project focuses on computing the income and tax liabilities for Steve and Brenda, providing tax planning advice to minimize their tax obligations. The project details Steve's salary, bonus, contributions, and benefits, along with long-term capital gains and rental income. It also covers Brenda's business income, capital gains, and specific deductions. The federal tax owing is calculated for both individuals, and recommendations are provided, including maintaining receipts, using vehicle log books, paying salaries to reduce business profit, investing in tax-deductible schemes, maintaining proper books of accounts, and maximizing contributions to registered retirement funds. Notes clarify the treatment of expenditures, business expenses, contributions, tuition fees, and charitable contributions in the calculations.

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.