Taxation and Capital Gain Computation for John Volkler and Carlton

VerifiedAdded on 2023/06/08

|6

|2065

|421

AI Summary

This article discusses the taxation and capital gain computation for John Volkler and Carlton in Australia. For John Volkler, his assessable income includes his salary, payment of child's school fees, and rent receipts. For Carlton, his net capital gain is AUD 525,000 under the discounting method. The article also explains how the tax treatment would differ if Carlton sold the property to his daughter or if the owner of the property was a company.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

PART A - 20 marks

John Volkler is a South African resident who specialises in assaying the value of diamonds.

In 2017, he signed a contract in Johannesburg with the Norfolk Diamond Company to work

for that company’s head office in Johannesburg and to visit its various branch offices

throughout the world. He spent two months in the company’s Sydney office assaying the

value of diamonds from 1 July to 1 September. During this period, he stayed in a motel paid

by the company. His salary, equivalent to $9,000 for the two months, was paid directly into

his Johannesburg bank account by the parent South African company. Later John

successfully applied for a continuing job position in the company’s Sydney office, and was

transferred to the position on 1 October 2017. John was accompanied by his wife and child to

Australia. They decided not to sell their house in Johannesburg and chose to rent it out for

$1,500 per month. The Norfolk Diamond Company offered John the following remuneration

package:

(a) Salary of $110,000 per annum;

(b) Payment of child’s school fees $15,000;

(c) Laptop computer provided $1,899;

(d) Professional development allowance $750 per annum;

(e) All expenses include GST where applicable.

Determine what amounts will form part of John’s assessable income for the 2017/18 taxation

year. Fully explain your answer. If you feel you need further information to be able to

adequately answer the question, indicate what information you require and why it is required.

Solution to PART A

The solution has been provided here-in-under. Further an analysis of each items has been

provided as notes to the solution:

Computation of Taxation Income

Name Mr. John Volker

Status Individual

FY 2017-18

AY 2018-19

Resident

Citizen South African

John Volkler is a South African resident who specialises in assaying the value of diamonds.

In 2017, he signed a contract in Johannesburg with the Norfolk Diamond Company to work

for that company’s head office in Johannesburg and to visit its various branch offices

throughout the world. He spent two months in the company’s Sydney office assaying the

value of diamonds from 1 July to 1 September. During this period, he stayed in a motel paid

by the company. His salary, equivalent to $9,000 for the two months, was paid directly into

his Johannesburg bank account by the parent South African company. Later John

successfully applied for a continuing job position in the company’s Sydney office, and was

transferred to the position on 1 October 2017. John was accompanied by his wife and child to

Australia. They decided not to sell their house in Johannesburg and chose to rent it out for

$1,500 per month. The Norfolk Diamond Company offered John the following remuneration

package:

(a) Salary of $110,000 per annum;

(b) Payment of child’s school fees $15,000;

(c) Laptop computer provided $1,899;

(d) Professional development allowance $750 per annum;

(e) All expenses include GST where applicable.

Determine what amounts will form part of John’s assessable income for the 2017/18 taxation

year. Fully explain your answer. If you feel you need further information to be able to

adequately answer the question, indicate what information you require and why it is required.

Solution to PART A

The solution has been provided here-in-under. Further an analysis of each items has been

provided as notes to the solution:

Computation of Taxation Income

Name Mr. John Volker

Status Individual

FY 2017-18

AY 2018-19

Resident

Citizen South African

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Sl No Particulars Amount Amount

1 Salary (2 Months) 7000

2 Salary (9 Months) 82500

3 Payment of child school Fees 15000 0

4 Laptop Computer Provided 1899 0

5 Professional development fees 750 0

6 Rent receipts 13500

7 Total taxable icome 103000

8 Fringe benefits 17649

During the year under consideration, Mr. John Walker a south African citizen who came to

Australia for 2 months and later settled permanently for the year under consideration. In the

first step, it shall be worthwhile to determine the residential status of Mr. John.

In terms of Section 6(1) of the Act 1or Australian Income Tax Act as amended various years

and under the important rulings to determine residency for tax purpose, various tests have

been defined to determine the residency of an individual.

The primary test encompasses a resides test wherein one need to assess whether one resides

in Australia under a permanent nature with a full intent or not. If this test is not satisfied ,

other tests need to be looked upon for determining the residency of an individual

If you fail to satisfy the first test, then other three statutory tests need to be taken into

consideration for determining residency:-

(a) Domicile Test: Under this test, one needs to analyse whether one has a permanent abode

in the form of a house, bungalow owned by him/ her in Australia. If the individual

satisfies this test, he shall be treated as resident of Australia and his worldwide income

shall be taxable in Australia.

(b) 183-days Test: The second test is the simplest step wherein you count the no of days of

stay of an individual in any part of the country. If the stay during the year exceeds 183

days then the individual is considered as tax resident of Australia and accordingly his pan

world income is taxable.

(c) Superannuation test: Under the third test, one needs to harp on whether common wealth

government employees who are treated as resident of Australia for tax purpose if they are

working for Australian overseas.

If any of the three tests specified above, an individual is considered as tax resident of

Australia and is required to pay tax under the Act.

Since, Mr. John satisfies the above test. His pan world income shall be taxable in Australia

and he shall be considered as Australian Tax resident for the concerned year.

1 https://www.quillgroup.com.au/blog/australian-resident-for-tax-purposes-explained/

1 Salary (2 Months) 7000

2 Salary (9 Months) 82500

3 Payment of child school Fees 15000 0

4 Laptop Computer Provided 1899 0

5 Professional development fees 750 0

6 Rent receipts 13500

7 Total taxable icome 103000

8 Fringe benefits 17649

During the year under consideration, Mr. John Walker a south African citizen who came to

Australia for 2 months and later settled permanently for the year under consideration. In the

first step, it shall be worthwhile to determine the residential status of Mr. John.

In terms of Section 6(1) of the Act 1or Australian Income Tax Act as amended various years

and under the important rulings to determine residency for tax purpose, various tests have

been defined to determine the residency of an individual.

The primary test encompasses a resides test wherein one need to assess whether one resides

in Australia under a permanent nature with a full intent or not. If this test is not satisfied ,

other tests need to be looked upon for determining the residency of an individual

If you fail to satisfy the first test, then other three statutory tests need to be taken into

consideration for determining residency:-

(a) Domicile Test: Under this test, one needs to analyse whether one has a permanent abode

in the form of a house, bungalow owned by him/ her in Australia. If the individual

satisfies this test, he shall be treated as resident of Australia and his worldwide income

shall be taxable in Australia.

(b) 183-days Test: The second test is the simplest step wherein you count the no of days of

stay of an individual in any part of the country. If the stay during the year exceeds 183

days then the individual is considered as tax resident of Australia and accordingly his pan

world income is taxable.

(c) Superannuation test: Under the third test, one needs to harp on whether common wealth

government employees who are treated as resident of Australia for tax purpose if they are

working for Australian overseas.

If any of the three tests specified above, an individual is considered as tax resident of

Australia and is required to pay tax under the Act.

Since, Mr. John satisfies the above test. His pan world income shall be taxable in Australia

and he shall be considered as Australian Tax resident for the concerned year.

1 https://www.quillgroup.com.au/blog/australian-resident-for-tax-purposes-explained/

Treatment of Assessable Income

(a) Salaries: Salaries2 received from employer are chargeable to tax under the Income Tax

Assessment Act, 1997. Further, the employer gets the deduction for the same as expense

in his / her return.

(b) Payment of child’s school fees:3 Payment of child’s school fees by the employer is

treated as fringe benefit under the Australian Income Assessment Act and the same is

taxable in the hands of the employer at a predefined rate. Further, employee is required

to report the same in his tax return as Fringe Benefits received from employer.

(c) Laptop computer: The same has been provided for official purpose and has been

assumed to be used for official purpose and hence shall not be treated as assessable

income of Mr. John. Further, employer shall be able to take GST credits of the same and

shall depreciation on the asset over a period of 4 years under Australian rax act.

(d) Professional development allowance: The same shall not be treated as income of the

individual as the said has been paid as training of the employee and it is a part of training

imparted by the employer to make one fit for the job. Further, employer shall be able to

claim GST credits for the same.

(e) Rent receipt in South Africa shall be taxable in Australia as pan income of a resident is

taxable in Australia.

Information further required

(a) No information about taxability of rent receipt in South Africa;

(b) Expenses incurred towards earning those rent;

(c) Bank interest;

(d) Other income in South Africa

PART B - 10 marks

Carlton is an accountant that purchased a vacant block of land in North Melbourne and built a

house on the land twenty years ago. At the time, the land was valued at $90,000 and the cost

of construction was $60,000. The property has been rented out since construction was

completed. On 1 August of the current tax year, Carlton sold the property at auction for

$1,200,000.

(a) What are Carlton’s net capital gain or net capital loss for the year ended 30 June of

the current tax year;

(b) How would your answer to (a) differ if Carlton sold the property to his daughter for

$200,000;

2 https://www.legislation.gov.au/Details/C2017C00282

3 https://www.bdo.com.au/getattachment/b16e4011-2649-48f0-b378-77129c0764b1/attachment.aspx

(a) Salaries: Salaries2 received from employer are chargeable to tax under the Income Tax

Assessment Act, 1997. Further, the employer gets the deduction for the same as expense

in his / her return.

(b) Payment of child’s school fees:3 Payment of child’s school fees by the employer is

treated as fringe benefit under the Australian Income Assessment Act and the same is

taxable in the hands of the employer at a predefined rate. Further, employee is required

to report the same in his tax return as Fringe Benefits received from employer.

(c) Laptop computer: The same has been provided for official purpose and has been

assumed to be used for official purpose and hence shall not be treated as assessable

income of Mr. John. Further, employer shall be able to take GST credits of the same and

shall depreciation on the asset over a period of 4 years under Australian rax act.

(d) Professional development allowance: The same shall not be treated as income of the

individual as the said has been paid as training of the employee and it is a part of training

imparted by the employer to make one fit for the job. Further, employer shall be able to

claim GST credits for the same.

(e) Rent receipt in South Africa shall be taxable in Australia as pan income of a resident is

taxable in Australia.

Information further required

(a) No information about taxability of rent receipt in South Africa;

(b) Expenses incurred towards earning those rent;

(c) Bank interest;

(d) Other income in South Africa

PART B - 10 marks

Carlton is an accountant that purchased a vacant block of land in North Melbourne and built a

house on the land twenty years ago. At the time, the land was valued at $90,000 and the cost

of construction was $60,000. The property has been rented out since construction was

completed. On 1 August of the current tax year, Carlton sold the property at auction for

$1,200,000.

(a) What are Carlton’s net capital gain or net capital loss for the year ended 30 June of

the current tax year;

(b) How would your answer to (a) differ if Carlton sold the property to his daughter for

$200,000;

2 https://www.legislation.gov.au/Details/C2017C00282

3 https://www.bdo.com.au/getattachment/b16e4011-2649-48f0-b378-77129c0764b1/attachment.aspx

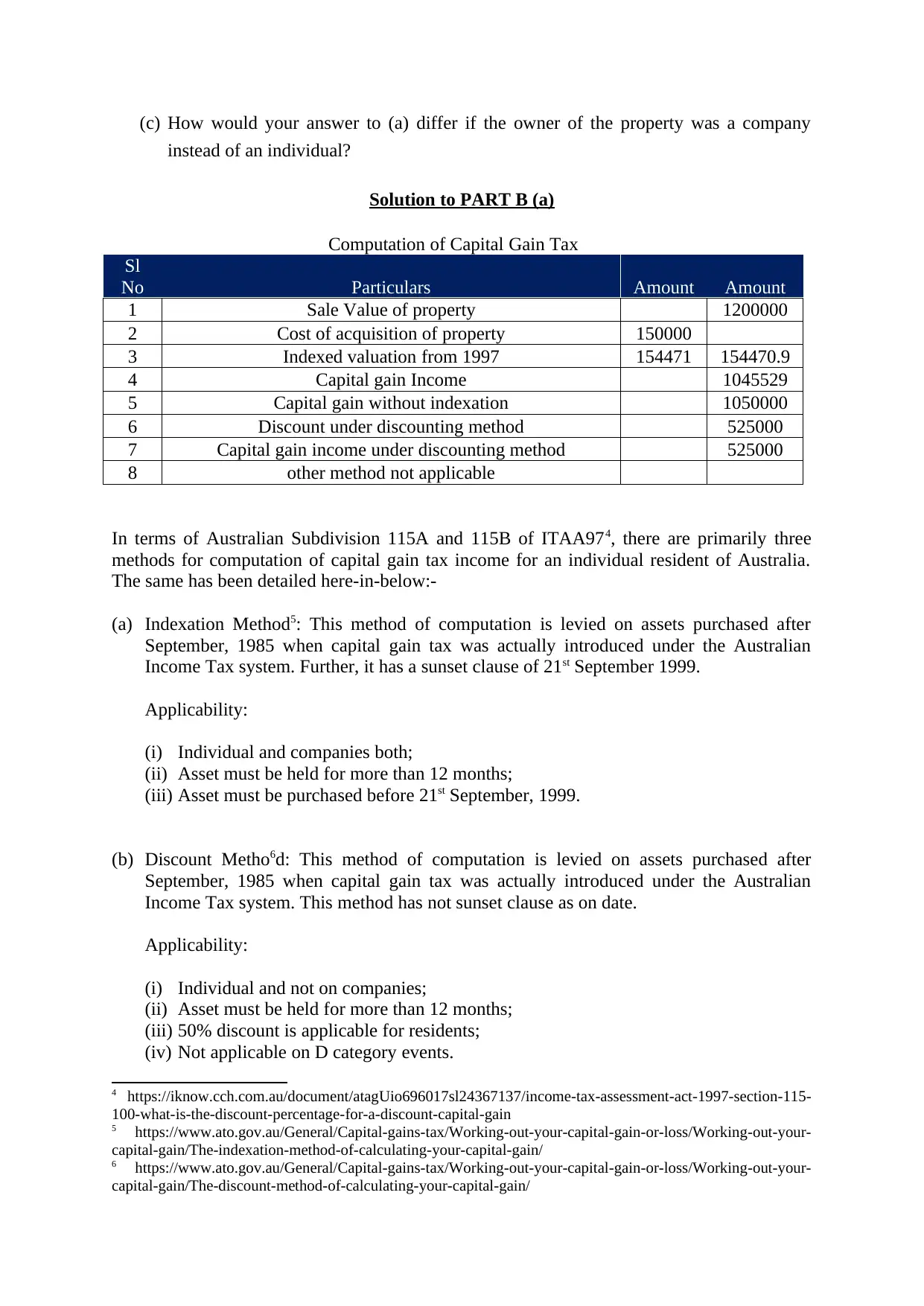

(c) How would your answer to (a) differ if the owner of the property was a company

instead of an individual?

Solution to PART B (a)

Computation of Capital Gain Tax

Sl

No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

5 Capital gain without indexation 1050000

6 Discount under discounting method 525000

7 Capital gain income under discounting method 525000

8 other method not applicable

In terms of Australian Subdivision 115A and 115B of ITAA974, there are primarily three

methods for computation of capital gain tax income for an individual resident of Australia.

The same has been detailed here-in-below:-

(a) Indexation Method5: This method of computation is levied on assets purchased after

September, 1985 when capital gain tax was actually introduced under the Australian

Income Tax system. Further, it has a sunset clause of 21st September 1999.

Applicability:

(i) Individual and companies both;

(ii) Asset must be held for more than 12 months;

(iii) Asset must be purchased before 21st September, 1999.

(b) Discount Metho6d: This method of computation is levied on assets purchased after

September, 1985 when capital gain tax was actually introduced under the Australian

Income Tax system. This method has not sunset clause as on date.

Applicability:

(i) Individual and not on companies;

(ii) Asset must be held for more than 12 months;

(iii) 50% discount is applicable for residents;

(iv) Not applicable on D category events.

4 https://iknow.cch.com.au/document/atagUio696017sl24367137/income-tax-assessment-act-1997-section-115-

100-what-is-the-discount-percentage-for-a-discount-capital-gain

5 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The-indexation-method-of-calculating-your-capital-gain/

6 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The-discount-method-of-calculating-your-capital-gain/

instead of an individual?

Solution to PART B (a)

Computation of Capital Gain Tax

Sl

No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

5 Capital gain without indexation 1050000

6 Discount under discounting method 525000

7 Capital gain income under discounting method 525000

8 other method not applicable

In terms of Australian Subdivision 115A and 115B of ITAA974, there are primarily three

methods for computation of capital gain tax income for an individual resident of Australia.

The same has been detailed here-in-below:-

(a) Indexation Method5: This method of computation is levied on assets purchased after

September, 1985 when capital gain tax was actually introduced under the Australian

Income Tax system. Further, it has a sunset clause of 21st September 1999.

Applicability:

(i) Individual and companies both;

(ii) Asset must be held for more than 12 months;

(iii) Asset must be purchased before 21st September, 1999.

(b) Discount Metho6d: This method of computation is levied on assets purchased after

September, 1985 when capital gain tax was actually introduced under the Australian

Income Tax system. This method has not sunset clause as on date.

Applicability:

(i) Individual and not on companies;

(ii) Asset must be held for more than 12 months;

(iii) 50% discount is applicable for residents;

(iv) Not applicable on D category events.

4 https://iknow.cch.com.au/document/atagUio696017sl24367137/income-tax-assessment-act-1997-section-115-

100-what-is-the-discount-percentage-for-a-discount-capital-gain

5 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The-indexation-method-of-calculating-your-capital-gain/

6 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The-discount-method-of-calculating-your-capital-gain/

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

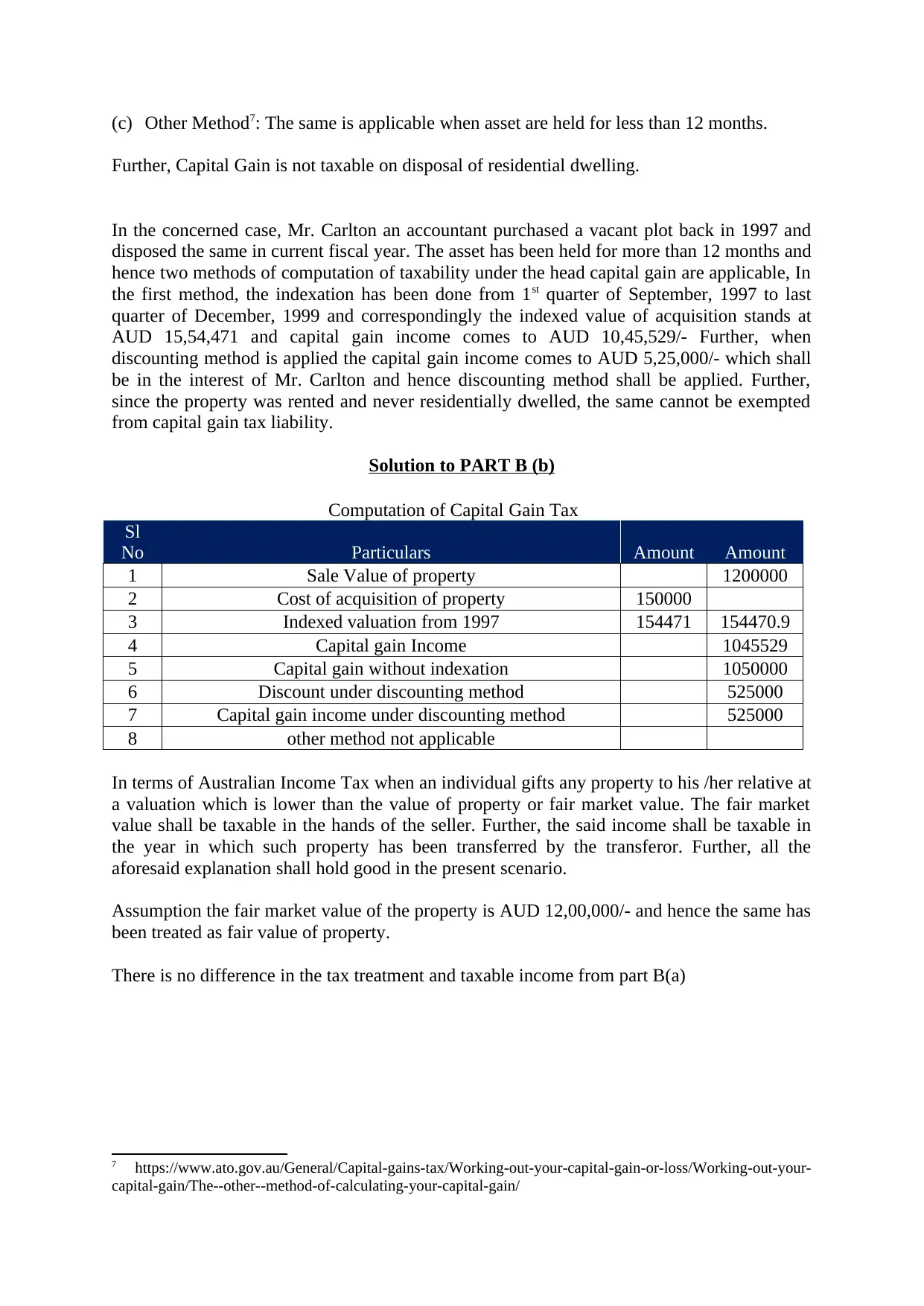

(c) Other Method7: The same is applicable when asset are held for less than 12 months.

Further, Capital Gain is not taxable on disposal of residential dwelling.

In the concerned case, Mr. Carlton an accountant purchased a vacant plot back in 1997 and

disposed the same in current fiscal year. The asset has been held for more than 12 months and

hence two methods of computation of taxability under the head capital gain are applicable, In

the first method, the indexation has been done from 1st quarter of September, 1997 to last

quarter of December, 1999 and correspondingly the indexed value of acquisition stands at

AUD 15,54,471 and capital gain income comes to AUD 10,45,529/- Further, when

discounting method is applied the capital gain income comes to AUD 5,25,000/- which shall

be in the interest of Mr. Carlton and hence discounting method shall be applied. Further,

since the property was rented and never residentially dwelled, the same cannot be exempted

from capital gain tax liability.

Solution to PART B (b)

Computation of Capital Gain Tax

Sl

No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

5 Capital gain without indexation 1050000

6 Discount under discounting method 525000

7 Capital gain income under discounting method 525000

8 other method not applicable

In terms of Australian Income Tax when an individual gifts any property to his /her relative at

a valuation which is lower than the value of property or fair market value. The fair market

value shall be taxable in the hands of the seller. Further, the said income shall be taxable in

the year in which such property has been transferred by the transferor. Further, all the

aforesaid explanation shall hold good in the present scenario.

Assumption the fair market value of the property is AUD 12,00,000/- and hence the same has

been treated as fair value of property.

There is no difference in the tax treatment and taxable income from part B(a)

7 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The--other--method-of-calculating-your-capital-gain/

Further, Capital Gain is not taxable on disposal of residential dwelling.

In the concerned case, Mr. Carlton an accountant purchased a vacant plot back in 1997 and

disposed the same in current fiscal year. The asset has been held for more than 12 months and

hence two methods of computation of taxability under the head capital gain are applicable, In

the first method, the indexation has been done from 1st quarter of September, 1997 to last

quarter of December, 1999 and correspondingly the indexed value of acquisition stands at

AUD 15,54,471 and capital gain income comes to AUD 10,45,529/- Further, when

discounting method is applied the capital gain income comes to AUD 5,25,000/- which shall

be in the interest of Mr. Carlton and hence discounting method shall be applied. Further,

since the property was rented and never residentially dwelled, the same cannot be exempted

from capital gain tax liability.

Solution to PART B (b)

Computation of Capital Gain Tax

Sl

No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

5 Capital gain without indexation 1050000

6 Discount under discounting method 525000

7 Capital gain income under discounting method 525000

8 other method not applicable

In terms of Australian Income Tax when an individual gifts any property to his /her relative at

a valuation which is lower than the value of property or fair market value. The fair market

value shall be taxable in the hands of the seller. Further, the said income shall be taxable in

the year in which such property has been transferred by the transferor. Further, all the

aforesaid explanation shall hold good in the present scenario.

Assumption the fair market value of the property is AUD 12,00,000/- and hence the same has

been treated as fair value of property.

There is no difference in the tax treatment and taxable income from part B(a)

7 https://www.ato.gov.au/General/Capital-gains-tax/Working-out-your-capital-gain-or-loss/Working-out-your-

capital-gain/The--other--method-of-calculating-your-capital-gain/

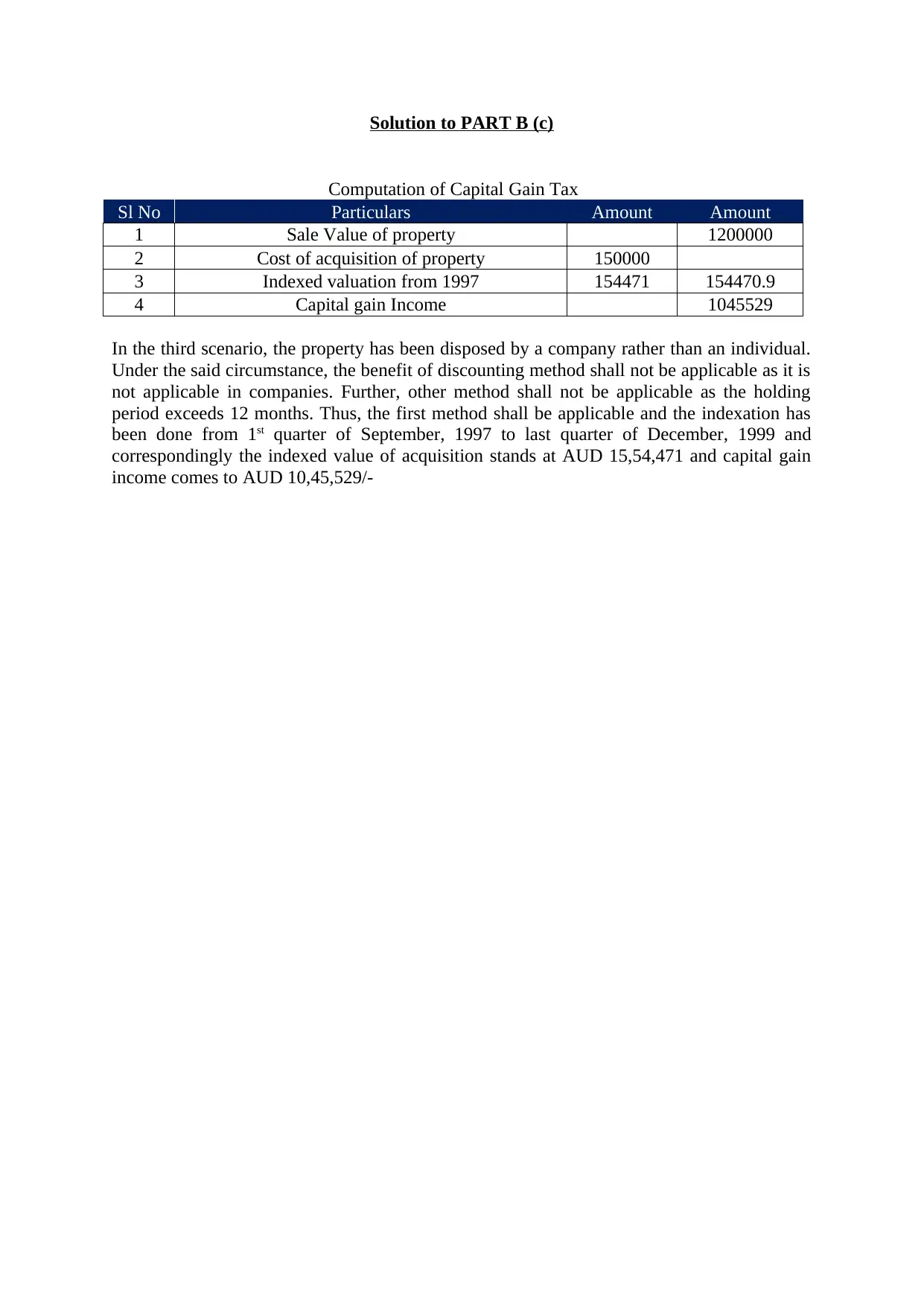

Solution to PART B (c)

Computation of Capital Gain Tax

Sl No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

In the third scenario, the property has been disposed by a company rather than an individual.

Under the said circumstance, the benefit of discounting method shall not be applicable as it is

not applicable in companies. Further, other method shall not be applicable as the holding

period exceeds 12 months. Thus, the first method shall be applicable and the indexation has

been done from 1st quarter of September, 1997 to last quarter of December, 1999 and

correspondingly the indexed value of acquisition stands at AUD 15,54,471 and capital gain

income comes to AUD 10,45,529/-

Computation of Capital Gain Tax

Sl No Particulars Amount Amount

1 Sale Value of property 1200000

2 Cost of acquisition of property 150000

3 Indexed valuation from 1997 154471 154470.9

4 Capital gain Income 1045529

In the third scenario, the property has been disposed by a company rather than an individual.

Under the said circumstance, the benefit of discounting method shall not be applicable as it is

not applicable in companies. Further, other method shall not be applicable as the holding

period exceeds 12 months. Thus, the first method shall be applicable and the indexation has

been done from 1st quarter of September, 1997 to last quarter of December, 1999 and

correspondingly the indexed value of acquisition stands at AUD 15,54,471 and capital gain

income comes to AUD 10,45,529/-

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.