Taxation: Computation of Taxable Income and Fringe Benefit

VerifiedAdded on 2023/06/10

|8

|1712

|395

AI Summary

This report discusses the computation of taxable income and fringe benefit in Australian taxation. It explains the legal provisions related to Medicare levy and Medicare levy surcharge. It also provides a calculation of assessable income, taxable income, and tax liability. Additionally, it discusses the computation of taxable value of fringe benefit using the statutory formula method. The report provides relevant examples and exemptions related to fringe benefits.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Contents

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

Question No 1 Taxable Income Computation:.......................................................................2

Question No 2 Computation of Taxable Value of Fringe Benefit:........................................5

CONCLUSON.................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION...........................................................................................................................2

TASK...............................................................................................................................................2

Question No 1 Taxable Income Computation:.......................................................................2

Question No 2 Computation of Taxable Value of Fringe Benefit:........................................5

CONCLUSON.................................................................................................................................6

REFERENCES................................................................................................................................7

INTRODUCTION

Taxation simply means imposition of the tax on income earned by various groups such as

individual, companies, partnership firms etc. The purpose of taxation to generate revenue for the

government department so that they can meet out their expenditure towards the public welfare.

In this statement income tax has been calculated in different case scenario and also fringe

benefits to be computed using the multiple information.

TASK

Question No 1 Taxable Income Computation:

Legal provisions with respect to Medicare levy and Medicare levy Surcharge:

Medicare levy is something which every taxpayer needs to pay irrespective of the fact

that whether these individuals hold the private health insurance facility or not. Medicare

levy will be imposed on the taxable income without any threshold limit but there is a

limit to impose such surcharge if income exceeded certain limit. The Medicare levy

surcharge are being imposed on the citizen of Australia whose earnings are being

exceeded beyond $ 90000 on every financial year but they don’t have private hospital

insurance. The purpose of levying such a surcharge to ensure that the individual who are

earning higher will take health insurance cover from the private hospital (Lang, Pistone,

and Spies, 2020). The limit for implementing the MLS is $90000 for singles and in case

of couples or families such limit will be extend to $180000. It means that if income

exceeded the above limit then MLS will be applicable on that and paid along with income

tax. The rate of MLS has been 1%, 1.25%, 1.50% respectively depending upon the

income of the individual. If a person wants to avoid MLS, then a valid hospital insurance

cover to avoid the same and it is necessary that such cover must be through registered

Australian health fund.

The following are certain categories which are being exempted from the payment of MLS

mentioned below:

Does not entitled for any medical benefits.

Person is of Foreign resident for the purpose of taxation.

Person who is blind permanently and also the pensioner.

The person who has obtained sickness allowance from the centre link.

Taxation simply means imposition of the tax on income earned by various groups such as

individual, companies, partnership firms etc. The purpose of taxation to generate revenue for the

government department so that they can meet out their expenditure towards the public welfare.

In this statement income tax has been calculated in different case scenario and also fringe

benefits to be computed using the multiple information.

TASK

Question No 1 Taxable Income Computation:

Legal provisions with respect to Medicare levy and Medicare levy Surcharge:

Medicare levy is something which every taxpayer needs to pay irrespective of the fact

that whether these individuals hold the private health insurance facility or not. Medicare

levy will be imposed on the taxable income without any threshold limit but there is a

limit to impose such surcharge if income exceeded certain limit. The Medicare levy

surcharge are being imposed on the citizen of Australia whose earnings are being

exceeded beyond $ 90000 on every financial year but they don’t have private hospital

insurance. The purpose of levying such a surcharge to ensure that the individual who are

earning higher will take health insurance cover from the private hospital (Lang, Pistone,

and Spies, 2020). The limit for implementing the MLS is $90000 for singles and in case

of couples or families such limit will be extend to $180000. It means that if income

exceeded the above limit then MLS will be applicable on that and paid along with income

tax. The rate of MLS has been 1%, 1.25%, 1.50% respectively depending upon the

income of the individual. If a person wants to avoid MLS, then a valid hospital insurance

cover to avoid the same and it is necessary that such cover must be through registered

Australian health fund.

The following are certain categories which are being exempted from the payment of MLS

mentioned below:

Does not entitled for any medical benefits.

Person is of Foreign resident for the purpose of taxation.

Person who is blind permanently and also the pensioner.

The person who has obtained sickness allowance from the centre link.

The person who can claim medical treatment on Veterans affairs repatriation

health card or with the help of defence force arrangements (Liu, Bai, and Liu,

2021).

In implementing the MLS, the following income needs to be considered:

In determining the surcharges, the Australian taxation office would have considered the

following points:

The taxable income of the person.

Any type of fringe benefits they are entitled.

Total losses on the investment made.

Foreign employment income which is exempt from tax.

The share of net income of the trust which is not otherwise included in their

taxable income (Noonan and Plekhanova, 2020).

Superannuation contributions which are being reportable.

From the point of view of ATO, the individuals are not required to pay the MLS if their

family income crosses the limit set under the law but the individual income for the

purpose of MLS is lower than $22398 as on December 2019.

Calculation of Assessable income, taxable income, tax liability etc. on the basis of

information given:

The taxation has been calculated for Leonne who wants to file his tax returns for the

period 2021 -2022 on the basis of the information she has furnished. The information

furnished by her are mentioned below:

Her taxable income is being $104000

Deduction she holds $4000 throughput the year

Hold the student loan HECS from the Griffith University of $37000

Hold the superannuation guarantee which is 10 % of her salary to the particular

nominated fund.

Hold the passive income of $7000 from the investments she has made in shares in

the same financial year.

Assessable Income:

The assessable income of Leonne for the Period 2021-2022 will be shows below:

Particular Computation of Income

health card or with the help of defence force arrangements (Liu, Bai, and Liu,

2021).

In implementing the MLS, the following income needs to be considered:

In determining the surcharges, the Australian taxation office would have considered the

following points:

The taxable income of the person.

Any type of fringe benefits they are entitled.

Total losses on the investment made.

Foreign employment income which is exempt from tax.

The share of net income of the trust which is not otherwise included in their

taxable income (Noonan and Plekhanova, 2020).

Superannuation contributions which are being reportable.

From the point of view of ATO, the individuals are not required to pay the MLS if their

family income crosses the limit set under the law but the individual income for the

purpose of MLS is lower than $22398 as on December 2019.

Calculation of Assessable income, taxable income, tax liability etc. on the basis of

information given:

The taxation has been calculated for Leonne who wants to file his tax returns for the

period 2021 -2022 on the basis of the information she has furnished. The information

furnished by her are mentioned below:

Her taxable income is being $104000

Deduction she holds $4000 throughput the year

Hold the student loan HECS from the Griffith University of $37000

Hold the superannuation guarantee which is 10 % of her salary to the particular

nominated fund.

Hold the passive income of $7000 from the investments she has made in shares in

the same financial year.

Assessable Income:

The assessable income of Leonne for the Period 2021-2022 will be shows below:

Particular Computation of Income

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

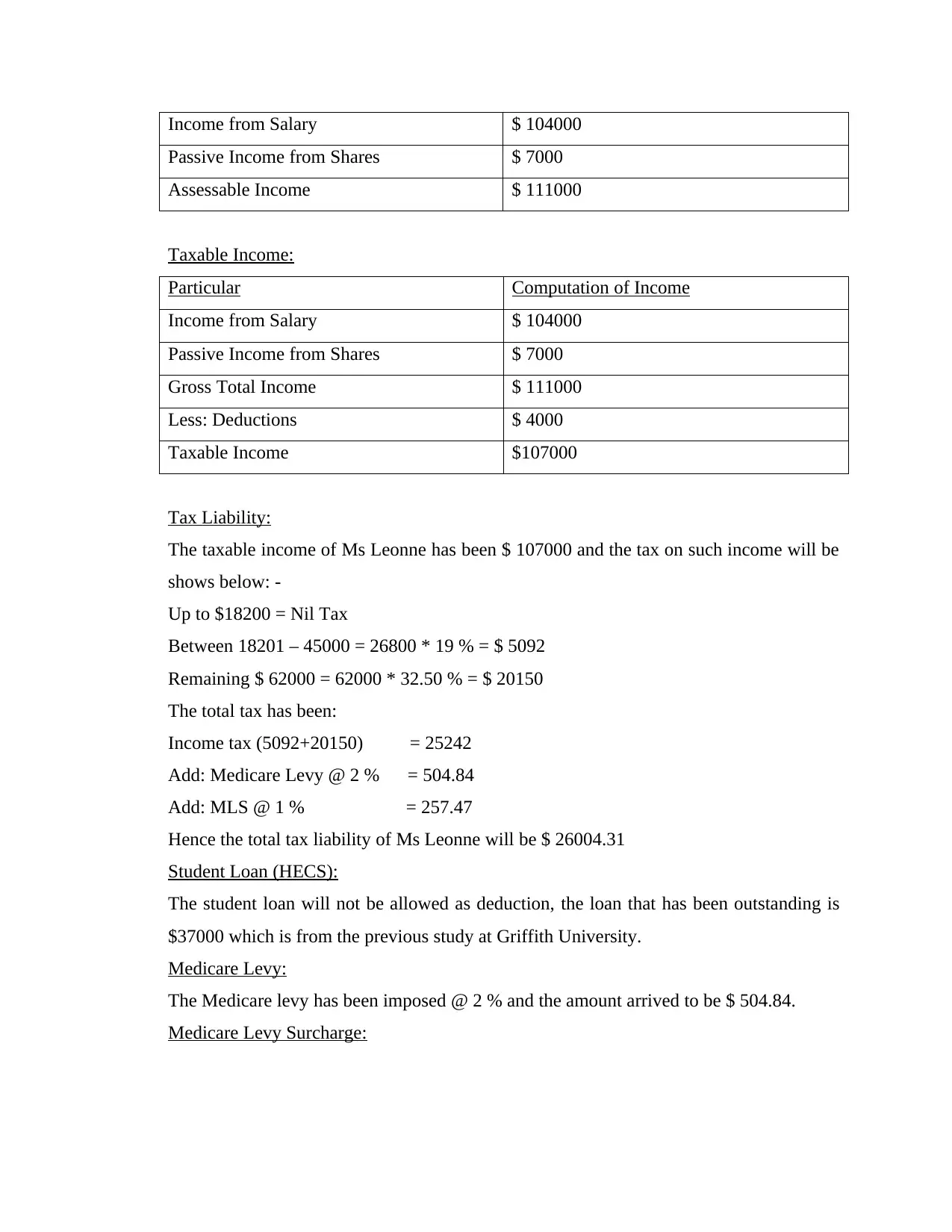

Income from Salary $ 104000

Passive Income from Shares $ 7000

Assessable Income $ 111000

Taxable Income:

Particular Computation of Income

Income from Salary $ 104000

Passive Income from Shares $ 7000

Gross Total Income $ 111000

Less: Deductions $ 4000

Taxable Income $107000

Tax Liability:

The taxable income of Ms Leonne has been $ 107000 and the tax on such income will be

shows below: -

Up to $18200 = Nil Tax

Between 18201 – 45000 = 26800 * 19 % = $ 5092

Remaining $ 62000 = 62000 * 32.50 % = $ 20150

The total tax has been:

Income tax (5092+20150) = 25242

Add: Medicare Levy @ 2 % = 504.84

Add: MLS @ 1 % = 257.47

Hence the total tax liability of Ms Leonne will be $ 26004.31

Student Loan (HECS):

The student loan will not be allowed as deduction, the loan that has been outstanding is

$37000 which is from the previous study at Griffith University.

Medicare Levy:

The Medicare levy has been imposed @ 2 % and the amount arrived to be $ 504.84.

Medicare Levy Surcharge:

Passive Income from Shares $ 7000

Assessable Income $ 111000

Taxable Income:

Particular Computation of Income

Income from Salary $ 104000

Passive Income from Shares $ 7000

Gross Total Income $ 111000

Less: Deductions $ 4000

Taxable Income $107000

Tax Liability:

The taxable income of Ms Leonne has been $ 107000 and the tax on such income will be

shows below: -

Up to $18200 = Nil Tax

Between 18201 – 45000 = 26800 * 19 % = $ 5092

Remaining $ 62000 = 62000 * 32.50 % = $ 20150

The total tax has been:

Income tax (5092+20150) = 25242

Add: Medicare Levy @ 2 % = 504.84

Add: MLS @ 1 % = 257.47

Hence the total tax liability of Ms Leonne will be $ 26004.31

Student Loan (HECS):

The student loan will not be allowed as deduction, the loan that has been outstanding is

$37000 which is from the previous study at Griffith University.

Medicare Levy:

The Medicare levy has been imposed @ 2 % and the amount arrived to be $ 504.84.

Medicare Levy Surcharge:

The Medicare levy has been imposed @ 1 % since the taxable income exceeds $ 90000

and Ms Leonne does not have Private Health cover. Therefore, MLS has been levied

upon them and the surcharge that has been arrived to be $ 257.47.

Question No 2 Computation of Taxable Value of Fringe Benefit:

Fringe Benefit is the benefit that has been granted by the employer to their employees but in

a different form other than payment of salary (Ontario Fair Tax Commission, 2019). For the

purpose of Fringe benefit tax, an employee includes the following

Current, Future and past employees of the organisation.

The director of the organisation.

The trust beneficiary who is working in the business.

Some of the examples of Fringe benefits are being laid down under:

Car facility provided to employee that can be used by him for personal purpose also.

The discounted loan or the loan at lower then market rate has been provided to the

employee.

Gym membership has been provided to employee.

Providing free tickets for concerts to employees for entertainment purpose.

Reimbursement of expenses facility are being provided to employee such as school fees,

tuition fees etc. of their children (Reimert and Rust, 2022).

The following are being not considered as Fringe Benefits:

Salary and wages paid to employees and workers.

The contribution that has been made by the employer for super funds.

The benefits that are being provided to volunteer and contractors.

Exempt benefits that are being granted to religious institutions for their religious

practitioners.

The shares that are being received by the employees under amalgamation or mergers &

acquisitions etc.

In the given case the fringe benefit that has been provided by Nasir to his employee Rajesh has

been the usage of car of personal use. In order to compute the taxable value of car fringe

benefits, the employer may use either of the following models:

The statutory formula method which is based on the cost price of the car and

and Ms Leonne does not have Private Health cover. Therefore, MLS has been levied

upon them and the surcharge that has been arrived to be $ 257.47.

Question No 2 Computation of Taxable Value of Fringe Benefit:

Fringe Benefit is the benefit that has been granted by the employer to their employees but in

a different form other than payment of salary (Ontario Fair Tax Commission, 2019). For the

purpose of Fringe benefit tax, an employee includes the following

Current, Future and past employees of the organisation.

The director of the organisation.

The trust beneficiary who is working in the business.

Some of the examples of Fringe benefits are being laid down under:

Car facility provided to employee that can be used by him for personal purpose also.

The discounted loan or the loan at lower then market rate has been provided to the

employee.

Gym membership has been provided to employee.

Providing free tickets for concerts to employees for entertainment purpose.

Reimbursement of expenses facility are being provided to employee such as school fees,

tuition fees etc. of their children (Reimert and Rust, 2022).

The following are being not considered as Fringe Benefits:

Salary and wages paid to employees and workers.

The contribution that has been made by the employer for super funds.

The benefits that are being provided to volunteer and contractors.

Exempt benefits that are being granted to religious institutions for their religious

practitioners.

The shares that are being received by the employees under amalgamation or mergers &

acquisitions etc.

In the given case the fringe benefit that has been provided by Nasir to his employee Rajesh has

been the usage of car of personal use. In order to compute the taxable value of car fringe

benefits, the employer may use either of the following models:

The statutory formula method which is based on the cost price of the car and

The operating cost method which is based on operating cost of running the car

(Stashchuk, Boiar, and Zintso, 2021).

By applying the statutory cost formula, the value of fringe benefit that has been provided by

Nasir to his employee that is Rajesh is $42000. However, the Rajesh has been contributed $ 2500

towards the cost of running the car. Therefore, the value of Fringe benefits will be $39500.

CONCLUSON

The above repost shows the computation of total income based upon the Australian taxation

relating to income tax. The another issue discuss in the report is fringe benefit tax relating to car

facility that has been granted by the employer to his employee. Both the cases are discussed in

the above statement considering Australian taxation regarding income tax.

(Stashchuk, Boiar, and Zintso, 2021).

By applying the statutory cost formula, the value of fringe benefit that has been provided by

Nasir to his employee that is Rajesh is $42000. However, the Rajesh has been contributed $ 2500

towards the cost of running the car. Therefore, the value of Fringe benefits will be $39500.

CONCLUSON

The above repost shows the computation of total income based upon the Australian taxation

relating to income tax. The another issue discuss in the report is fringe benefit tax relating to car

facility that has been granted by the employer to his employee. Both the cases are discussed in

the above statement considering Australian taxation regarding income tax.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Lang, M., Pistone, P., and Spies, K. eds., 2020. Introduction to European tax law on direct

taxation. Spiramus Press Ltd.

Liu, J., Bai, J., and Liu, X., 2021. Impact of energy structure on carbon emission and economy of

China in the scenario of carbon taxation. Science of the Total Environment, 762,

p.143093.

Noonan, C. and Plekhanova, V., 2020. Taxation of Digital Services Under Trade

Agreements. Journal of International Economic Law, 23(4), pp.1015-1039.

Ontario Fair Tax Commission, 2019. Fair taxation in a changing world. In Fair Taxation in a

Changing World. University of Toronto Press.

Reimert, E. and Rust, A. eds., 2022. Klaus Vogel on double taxation conventions. Kluwer Law

International BV.

Stashchuk, O., Boiar, A., and Zintso, Y., 2021. Analysis of fiscal efficiency of taxation in the

system of filling budget funds in Ukraine. Ad alta: Journal of interdisciplinary

research, (1 (11)), pp.47-51.

Wasylenko, M., 2019. Taxation and economic development: The state of the economic literature.

In Handbook on Taxation (pp. 309-328). Routledge.

Books and Journals

Lang, M., Pistone, P., and Spies, K. eds., 2020. Introduction to European tax law on direct

taxation. Spiramus Press Ltd.

Liu, J., Bai, J., and Liu, X., 2021. Impact of energy structure on carbon emission and economy of

China in the scenario of carbon taxation. Science of the Total Environment, 762,

p.143093.

Noonan, C. and Plekhanova, V., 2020. Taxation of Digital Services Under Trade

Agreements. Journal of International Economic Law, 23(4), pp.1015-1039.

Ontario Fair Tax Commission, 2019. Fair taxation in a changing world. In Fair Taxation in a

Changing World. University of Toronto Press.

Reimert, E. and Rust, A. eds., 2022. Klaus Vogel on double taxation conventions. Kluwer Law

International BV.

Stashchuk, O., Boiar, A., and Zintso, Y., 2021. Analysis of fiscal efficiency of taxation in the

system of filling budget funds in Ukraine. Ad alta: Journal of interdisciplinary

research, (1 (11)), pp.47-51.

Wasylenko, M., 2019. Taxation and economic development: The state of the economic literature.

In Handbook on Taxation (pp. 309-328). Routledge.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.