Analysis of Capital Gains Tax and Fringe Benefits Tax Under Law

VerifiedAdded on 2023/06/03

|12

|3076

|477

Report

AI Summary

This report provides a detailed analysis of the capital gains tax (CGT) and fringe benefits tax (FBT) implications for the assessment year 2017/18, focusing on the taxation of capital assets and fringe benefits. It identifies assets sold by the taxpayer, including land, shares, a painting, a violin, and an antique bed, determining their CGT status based on acquisition dates and usage. The report outlines the steps for computing capital gains and losses, considering proceeds, cost base, and available discounts. It also examines the FBT consequences for an employer providing car and loan fringe benefits to an employee, calculating the taxable value and potential deductions. The analysis is grounded in relevant tax legislation, including the Income Tax Assessment Act 1997 (ITAA 1997) and the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986), and relevant tax rulings, offering a comprehensive overview of the taxation principles involved.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

It is known that the client has sold certain assets. In this backdrop, the objective is to highlight

the tax consequences to the taxpayer of these sold/disposed capital assets during the assessment

year i.e. 2017/18. In this regards, the hosts of aspects related to the transactions will be critically

analysed based on the relevant tax rulings and tax legislation.

Nature of Receipts

The main aspect to understand is that the taxpayer is not running a business and does not intent

to run an asset trading operation so as to generate ordinary income. However, she has many

collections as well as investments, among which she has sold a land block, shares of four

distinguish companies, a famous painting by Australian artist and a violin which she has used for

her interest. Moreover, there is also an asset called as antique bed which has been taken by

someone (Stolen). These assets are considered as capital assets of the taxpayer and liquidation of

these have resulted in capital receipts. These receipts are non-taxable under ordinary concepts

under s. 6(5) Income Tax Assessment Act 1997 but the underlying capital gains will be taxed as

per the provisions of Capital Gains Tax (CGT) (Woellner, 2017).

Exemption of CGT

The assets will be exempted from CGT only if they are classified as pre-CGT asset. This class of

assets are procured at the time when the capital gains were not considered for taxation which is

before September 20, 1985 (Sadiq, et.al., 2015). The assets whose ownership was assumed

before this specified era of CGT enforceability will not be taxed irrespective of the amount of

gains/losses, ownership or asset type or holding period and so forth. Further, special type of CGT

exemption would be applied on the capital assets which are categorised as collectables or

personal use asset. These two capital assets will only be taxed when the below highlighted

condition is satisfied (Nethercott, Richardson and Devos, 2016).

Collectables: Purchase price must be in excess of $500 (s. 118 (10) ITAA 1997)

Personal use item: Purchase price must be in excess of $10,000 (s. 108-20(1) ITAA 1997)

1

It is known that the client has sold certain assets. In this backdrop, the objective is to highlight

the tax consequences to the taxpayer of these sold/disposed capital assets during the assessment

year i.e. 2017/18. In this regards, the hosts of aspects related to the transactions will be critically

analysed based on the relevant tax rulings and tax legislation.

Nature of Receipts

The main aspect to understand is that the taxpayer is not running a business and does not intent

to run an asset trading operation so as to generate ordinary income. However, she has many

collections as well as investments, among which she has sold a land block, shares of four

distinguish companies, a famous painting by Australian artist and a violin which she has used for

her interest. Moreover, there is also an asset called as antique bed which has been taken by

someone (Stolen). These assets are considered as capital assets of the taxpayer and liquidation of

these have resulted in capital receipts. These receipts are non-taxable under ordinary concepts

under s. 6(5) Income Tax Assessment Act 1997 but the underlying capital gains will be taxed as

per the provisions of Capital Gains Tax (CGT) (Woellner, 2017).

Exemption of CGT

The assets will be exempted from CGT only if they are classified as pre-CGT asset. This class of

assets are procured at the time when the capital gains were not considered for taxation which is

before September 20, 1985 (Sadiq, et.al., 2015). The assets whose ownership was assumed

before this specified era of CGT enforceability will not be taxed irrespective of the amount of

gains/losses, ownership or asset type or holding period and so forth. Further, special type of CGT

exemption would be applied on the capital assets which are categorised as collectables or

personal use asset. These two capital assets will only be taxed when the below highlighted

condition is satisfied (Nethercott, Richardson and Devos, 2016).

Collectables: Purchase price must be in excess of $500 (s. 118 (10) ITAA 1997)

Personal use item: Purchase price must be in excess of $10,000 (s. 108-20(1) ITAA 1997)

1

Hence, it can be said that when the assets belonging to the above particular category would fulfil

the requisite condition then, the asset’s capital gains/loss will not be exempted from CGT

(Reuters, 2017).

Determination of CGT

There are different steps which are followed to compute the capital gains or capital losses from

the liquidation of the capital asset (Gilders, et. al., 2015). However, the main aspect in this

regards is to determine the nature of the transaction and its subclass so as to find the exact

procedure of determining the capital gains or losses. The complete summary of these transactions

are highlighted in s. 104-5, ITAA 1997 (Coleman, 2016). The assets disposal of the given case is

a CGT event and the subclass is A1. According to this subclass, the two central elements of the

computation of capital gains/losses are listed below (Hodgson, Mortimer and Butler, 2016).

Proceeds received from sale

Cost Base

Proceeds received from the sale can be contractual payment which the taxpayer will receive as

the sale income. Further, when there is an involuntary disposal has been occurred of the asset

then the income received from related insurance claim will also be considered as proceeds from

asset (Gilders, et. al., 2015).

Cost base includes associated costs or expenses that have been imposed on the taxpayer and

hence, all these payment has been paid by taxpayer only at the different stage of asset

procurement or selling as highlighted in s. 110 (25) ITAA 1997. There are five key components

which are associated with the cost base and are listed below (Krever, 2017).

It is essential to note that it is not necessary that all the five components of cost base are present

for every asset. Hence, in that case, the sum of the available component costs would become the

2

the requisite condition then, the asset’s capital gains/loss will not be exempted from CGT

(Reuters, 2017).

Determination of CGT

There are different steps which are followed to compute the capital gains or capital losses from

the liquidation of the capital asset (Gilders, et. al., 2015). However, the main aspect in this

regards is to determine the nature of the transaction and its subclass so as to find the exact

procedure of determining the capital gains or losses. The complete summary of these transactions

are highlighted in s. 104-5, ITAA 1997 (Coleman, 2016). The assets disposal of the given case is

a CGT event and the subclass is A1. According to this subclass, the two central elements of the

computation of capital gains/losses are listed below (Hodgson, Mortimer and Butler, 2016).

Proceeds received from sale

Cost Base

Proceeds received from the sale can be contractual payment which the taxpayer will receive as

the sale income. Further, when there is an involuntary disposal has been occurred of the asset

then the income received from related insurance claim will also be considered as proceeds from

asset (Gilders, et. al., 2015).

Cost base includes associated costs or expenses that have been imposed on the taxpayer and

hence, all these payment has been paid by taxpayer only at the different stage of asset

procurement or selling as highlighted in s. 110 (25) ITAA 1997. There are five key components

which are associated with the cost base and are listed below (Krever, 2017).

It is essential to note that it is not necessary that all the five components of cost base are present

for every asset. Hence, in that case, the sum of the available component costs would become the

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost base of asset. The calculated capital gains will be brought to adjust any present capital losses

which is either carry forwarded from previous year or derived from sale of asset under s. 102(5)

ITAA 1997 (Coleman, 2016). Further, if no capital losses are available then the capital gains will

be taken for concession based on the discount method. For long term capital gains which are

derived from the asset with reported holding period of more than 1 year would be entitled for a

net discount of 50%. (Krever, 2017). Furthermore, for short term capital gains which are derived

from the asset which are reporting holding period of less than 1 year, no discount on capital gains

would be available.

Consideration of Proceeds

According to the understanding drawn from TR 94/29, the taxpayer has to include the payment

which has been mentioned in the contract of sale of the asset irrespective of the timing of the

payment received (Sadiq et, al., 2015). It provides the clue that if the contract has been made

such a way that contract has been signed in the current year but taxpayer will be able to get the

payment in next year or later, then the consideration of the sale proceeds will be done in the year

of contract enactment (Reuters, 2017).

Taxpayer has disposed five assets during FY2017/18 at different point of time. The first step is to

determine which of them are categorised as pre-CGT asset because if the fall in pre-CGT asset

then no need to find capital gains/losses because they are exempted from CGT implication. The

key decision factor is buying date which represent that date which are prior to September 20,

1985 will refer to pre-CGT asset and thus, CGT exempted.

Painting

3

which is either carry forwarded from previous year or derived from sale of asset under s. 102(5)

ITAA 1997 (Coleman, 2016). Further, if no capital losses are available then the capital gains will

be taken for concession based on the discount method. For long term capital gains which are

derived from the asset with reported holding period of more than 1 year would be entitled for a

net discount of 50%. (Krever, 2017). Furthermore, for short term capital gains which are derived

from the asset which are reporting holding period of less than 1 year, no discount on capital gains

would be available.

Consideration of Proceeds

According to the understanding drawn from TR 94/29, the taxpayer has to include the payment

which has been mentioned in the contract of sale of the asset irrespective of the timing of the

payment received (Sadiq et, al., 2015). It provides the clue that if the contract has been made

such a way that contract has been signed in the current year but taxpayer will be able to get the

payment in next year or later, then the consideration of the sale proceeds will be done in the year

of contract enactment (Reuters, 2017).

Taxpayer has disposed five assets during FY2017/18 at different point of time. The first step is to

determine which of them are categorised as pre-CGT asset because if the fall in pre-CGT asset

then no need to find capital gains/losses because they are exempted from CGT implication. The

key decision factor is buying date which represent that date which are prior to September 20,

1985 will refer to pre-CGT asset and thus, CGT exempted.

Painting

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

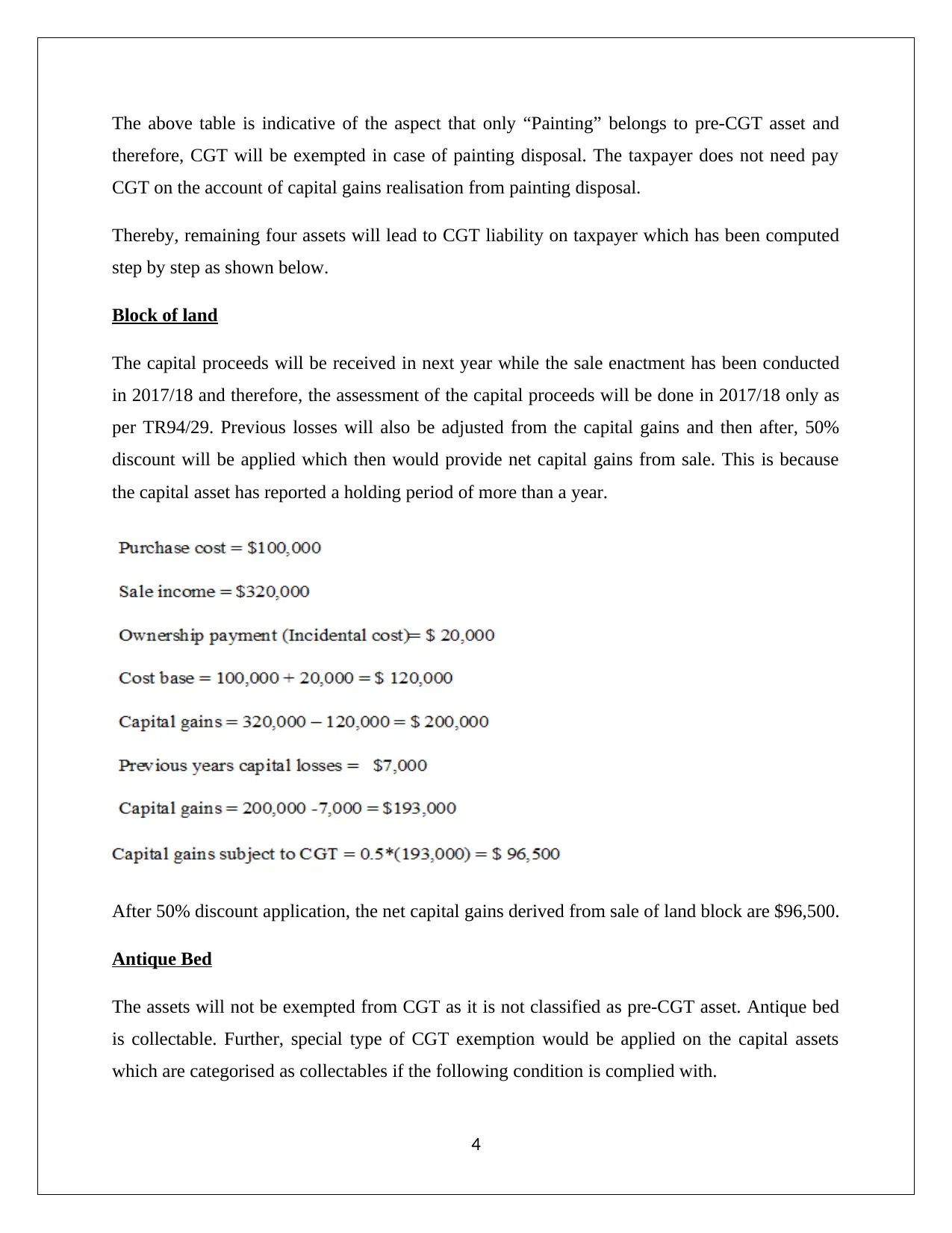

The above table is indicative of the aspect that only “Painting” belongs to pre-CGT asset and

therefore, CGT will be exempted in case of painting disposal. The taxpayer does not need pay

CGT on the account of capital gains realisation from painting disposal.

Thereby, remaining four assets will lead to CGT liability on taxpayer which has been computed

step by step as shown below.

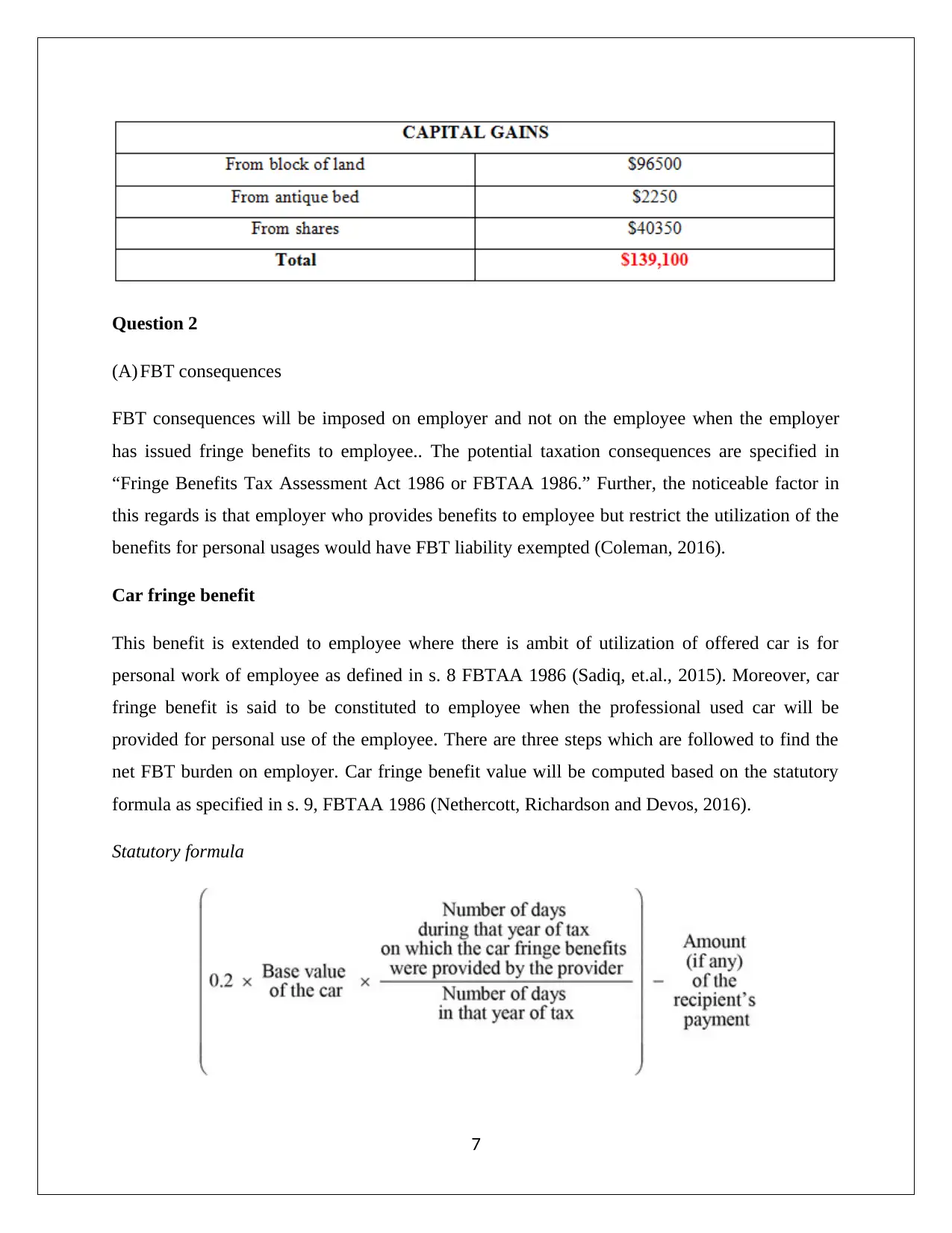

Block of land

The capital proceeds will be received in next year while the sale enactment has been conducted

in 2017/18 and therefore, the assessment of the capital proceeds will be done in 2017/18 only as

per TR94/29. Previous losses will also be adjusted from the capital gains and then after, 50%

discount will be applied which then would provide net capital gains from sale. This is because

the capital asset has reported a holding period of more than a year.

After 50% discount application, the net capital gains derived from sale of land block are $96,500.

Antique Bed

The assets will not be exempted from CGT as it is not classified as pre-CGT asset. Antique bed

is collectable. Further, special type of CGT exemption would be applied on the capital assets

which are categorised as collectables if the following condition is complied with.

4

therefore, CGT will be exempted in case of painting disposal. The taxpayer does not need pay

CGT on the account of capital gains realisation from painting disposal.

Thereby, remaining four assets will lead to CGT liability on taxpayer which has been computed

step by step as shown below.

Block of land

The capital proceeds will be received in next year while the sale enactment has been conducted

in 2017/18 and therefore, the assessment of the capital proceeds will be done in 2017/18 only as

per TR94/29. Previous losses will also be adjusted from the capital gains and then after, 50%

discount will be applied which then would provide net capital gains from sale. This is because

the capital asset has reported a holding period of more than a year.

After 50% discount application, the net capital gains derived from sale of land block are $96,500.

Antique Bed

The assets will not be exempted from CGT as it is not classified as pre-CGT asset. Antique bed

is collectable. Further, special type of CGT exemption would be applied on the capital assets

which are categorised as collectables if the following condition is complied with.

4

Collectables: Purchase price must be in excess of $500 (s. 118 (10) ITAA 1997)

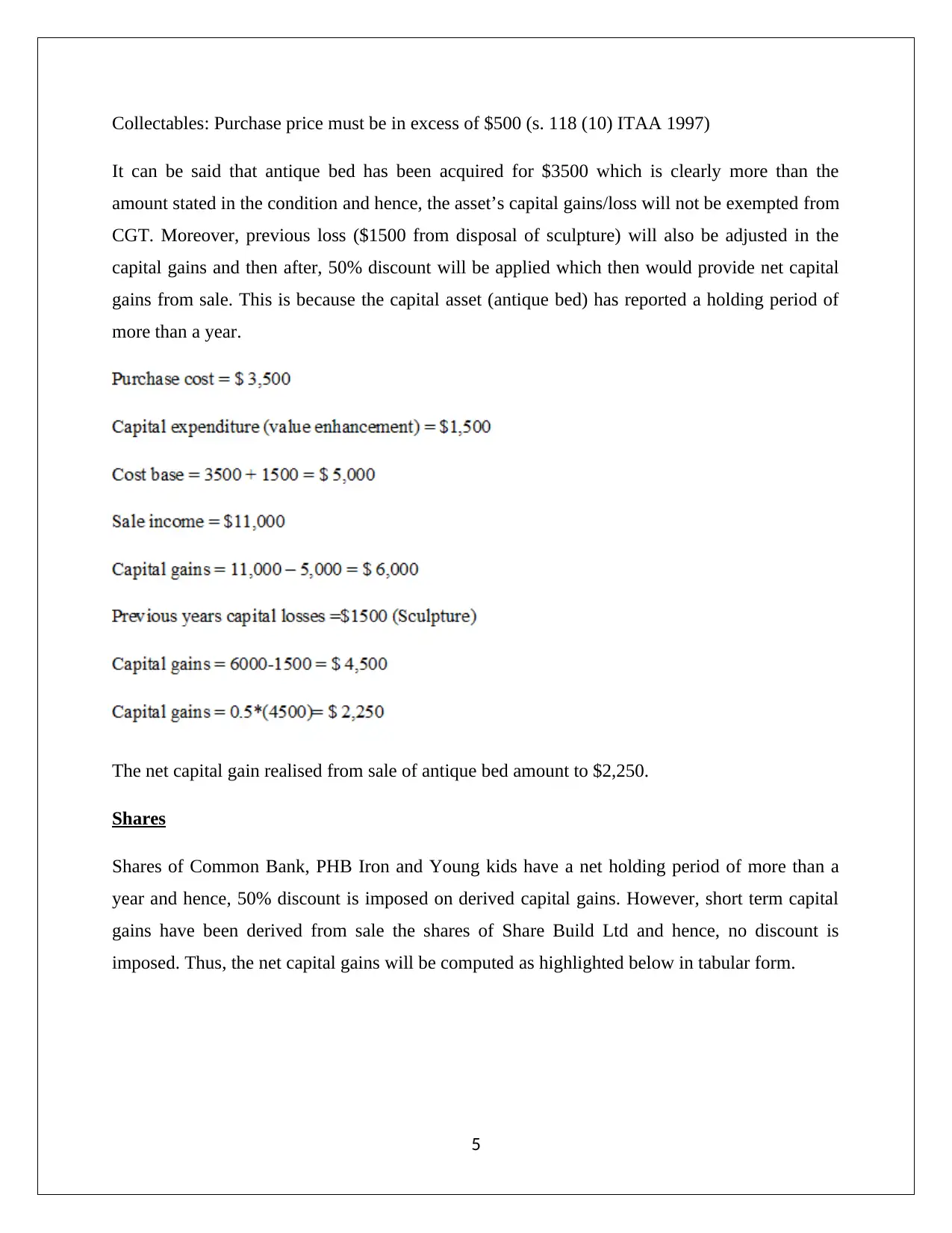

It can be said that antique bed has been acquired for $3500 which is clearly more than the

amount stated in the condition and hence, the asset’s capital gains/loss will not be exempted from

CGT. Moreover, previous loss ($1500 from disposal of sculpture) will also be adjusted in the

capital gains and then after, 50% discount will be applied which then would provide net capital

gains from sale. This is because the capital asset (antique bed) has reported a holding period of

more than a year.

The net capital gain realised from sale of antique bed amount to $2,250.

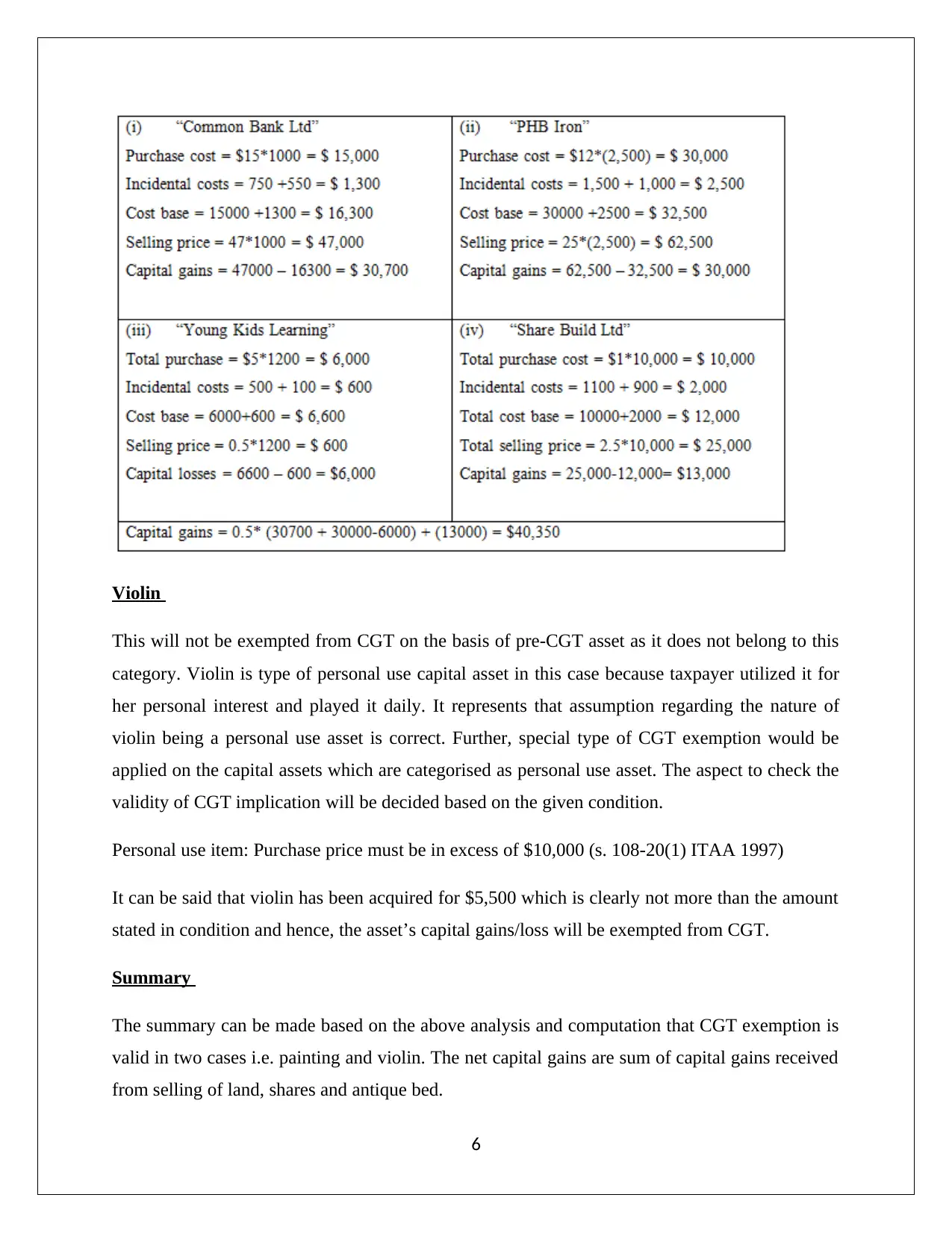

Shares

Shares of Common Bank, PHB Iron and Young kids have a net holding period of more than a

year and hence, 50% discount is imposed on derived capital gains. However, short term capital

gains have been derived from sale the shares of Share Build Ltd and hence, no discount is

imposed. Thus, the net capital gains will be computed as highlighted below in tabular form.

5

It can be said that antique bed has been acquired for $3500 which is clearly more than the

amount stated in the condition and hence, the asset’s capital gains/loss will not be exempted from

CGT. Moreover, previous loss ($1500 from disposal of sculpture) will also be adjusted in the

capital gains and then after, 50% discount will be applied which then would provide net capital

gains from sale. This is because the capital asset (antique bed) has reported a holding period of

more than a year.

The net capital gain realised from sale of antique bed amount to $2,250.

Shares

Shares of Common Bank, PHB Iron and Young kids have a net holding period of more than a

year and hence, 50% discount is imposed on derived capital gains. However, short term capital

gains have been derived from sale the shares of Share Build Ltd and hence, no discount is

imposed. Thus, the net capital gains will be computed as highlighted below in tabular form.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Violin

This will not be exempted from CGT on the basis of pre-CGT asset as it does not belong to this

category. Violin is type of personal use capital asset in this case because taxpayer utilized it for

her personal interest and played it daily. It represents that assumption regarding the nature of

violin being a personal use asset is correct. Further, special type of CGT exemption would be

applied on the capital assets which are categorised as personal use asset. The aspect to check the

validity of CGT implication will be decided based on the given condition.

Personal use item: Purchase price must be in excess of $10,000 (s. 108-20(1) ITAA 1997)

It can be said that violin has been acquired for $5,500 which is clearly not more than the amount

stated in condition and hence, the asset’s capital gains/loss will be exempted from CGT.

Summary

The summary can be made based on the above analysis and computation that CGT exemption is

valid in two cases i.e. painting and violin. The net capital gains are sum of capital gains received

from selling of land, shares and antique bed.

6

This will not be exempted from CGT on the basis of pre-CGT asset as it does not belong to this

category. Violin is type of personal use capital asset in this case because taxpayer utilized it for

her personal interest and played it daily. It represents that assumption regarding the nature of

violin being a personal use asset is correct. Further, special type of CGT exemption would be

applied on the capital assets which are categorised as personal use asset. The aspect to check the

validity of CGT implication will be decided based on the given condition.

Personal use item: Purchase price must be in excess of $10,000 (s. 108-20(1) ITAA 1997)

It can be said that violin has been acquired for $5,500 which is clearly not more than the amount

stated in condition and hence, the asset’s capital gains/loss will be exempted from CGT.

Summary

The summary can be made based on the above analysis and computation that CGT exemption is

valid in two cases i.e. painting and violin. The net capital gains are sum of capital gains received

from selling of land, shares and antique bed.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 2

(A) FBT consequences

FBT consequences will be imposed on employer and not on the employee when the employer

has issued fringe benefits to employee.. The potential taxation consequences are specified in

“Fringe Benefits Tax Assessment Act 1986 or FBTAA 1986.” Further, the noticeable factor in

this regards is that employer who provides benefits to employee but restrict the utilization of the

benefits for personal usages would have FBT liability exempted (Coleman, 2016).

Car fringe benefit

This benefit is extended to employee where there is ambit of utilization of offered car is for

personal work of employee as defined in s. 8 FBTAA 1986 (Sadiq, et.al., 2015). Moreover, car

fringe benefit is said to be constituted to employee when the professional used car will be

provided for personal use of the employee. There are three steps which are followed to find the

net FBT burden on employer. Car fringe benefit value will be computed based on the statutory

formula as specified in s. 9, FBTAA 1986 (Nethercott, Richardson and Devos, 2016).

Statutory formula

7

(A) FBT consequences

FBT consequences will be imposed on employer and not on the employee when the employer

has issued fringe benefits to employee.. The potential taxation consequences are specified in

“Fringe Benefits Tax Assessment Act 1986 or FBTAA 1986.” Further, the noticeable factor in

this regards is that employer who provides benefits to employee but restrict the utilization of the

benefits for personal usages would have FBT liability exempted (Coleman, 2016).

Car fringe benefit

This benefit is extended to employee where there is ambit of utilization of offered car is for

personal work of employee as defined in s. 8 FBTAA 1986 (Sadiq, et.al., 2015). Moreover, car

fringe benefit is said to be constituted to employee when the professional used car will be

provided for personal use of the employee. There are three steps which are followed to find the

net FBT burden on employer. Car fringe benefit value will be computed based on the statutory

formula as specified in s. 9, FBTAA 1986 (Nethercott, Richardson and Devos, 2016).

Statutory formula

7

Description of variables

Base value of the car: This is the amount which will be computed based on the total amount

spent by the employer while procuring the car and also, the minor repairing expense incurred

on car that borne by employer (Deutsch, et.al., 2015).

Number of availability days during the tax year is time during the given assessment year

when private usage is permissible. The car would still be available to employee when it is

sent to garage for repairs provided those are minor in nature. Also, availability is not

adversely impacted if the car has been parked by employee and gone out of town (Gilders, et.

al., 2015).

Amount which has been contributed by the recipient employee while procuring the car

(Barkoczy, 2017).

Rapid Heat extends car (procured for $33000) to Jasmine for personal work. Further, amount

which has been contributed by the recipient Jasmine while procuring the car is zero. The count

of days in 2017/2018 on which car is available to Jasmine is 335 days. The number of days in tax

assessment year is 365 days.

Computation

Loan Fringe Benefit

8

Base value of the car: This is the amount which will be computed based on the total amount

spent by the employer while procuring the car and also, the minor repairing expense incurred

on car that borne by employer (Deutsch, et.al., 2015).

Number of availability days during the tax year is time during the given assessment year

when private usage is permissible. The car would still be available to employee when it is

sent to garage for repairs provided those are minor in nature. Also, availability is not

adversely impacted if the car has been parked by employee and gone out of town (Gilders, et.

al., 2015).

Amount which has been contributed by the recipient employee while procuring the car

(Barkoczy, 2017).

Rapid Heat extends car (procured for $33000) to Jasmine for personal work. Further, amount

which has been contributed by the recipient Jasmine while procuring the car is zero. The count

of days in 2017/2018 on which car is available to Jasmine is 335 days. The number of days in tax

assessment year is 365 days.

Computation

Loan Fringe Benefit

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

In accordance with s. 16, FBTAA 1986, providing a loan to employee either with no interest or

with less interest rate (compared with RBA’s rate) is specified as loan fringe benefit (Nethercott,

Richardson and Devos, 2016). The objective behind providing less interest rate loan is to

minimize the interest burden on employee. The rate defined by RBA (FY 2018) is 5.25% per

annum. Therefore, any interest rate which is lesser than RBA’s interest rate will constitute

extension of loan fringe benefit to employee. The deduction will be offered to employer

(taxpayer of FBT) when the less interest rate loan will be used for obtaining assessable income

by employee (Deutsch, et.al., 2015). However, deduction will not be offered to employer when

the amount is used by concerned associates of the employee irrespective of the underlying

purpose of use (Sadiq et, al., 2015).

Rapid Heat extends loan to Jasmine for personal work. The days on which loan is available to

Jasmine is 212 days. The number of days in tax assessment year is 365 days. The gross up rate is

taken for type II goods for March 31, 2018. Further, the FBT rate taken into account is 47% for

March 31, 2018.

Computation

It is apparent from case study that 90% loan is used to procure a holiday home which may bring

in assessable income for Jasmine. The employer can avail deduction on this loan portion if that

happens. However, 10% of loan is provided to husband by Jasmine which will not create any

availability of deduction for Rapid Heat despite there being a possibility of dividend income. It is

because the loan has been utilized by her husband not by Jasmine.

9

with less interest rate (compared with RBA’s rate) is specified as loan fringe benefit (Nethercott,

Richardson and Devos, 2016). The objective behind providing less interest rate loan is to

minimize the interest burden on employee. The rate defined by RBA (FY 2018) is 5.25% per

annum. Therefore, any interest rate which is lesser than RBA’s interest rate will constitute

extension of loan fringe benefit to employee. The deduction will be offered to employer

(taxpayer of FBT) when the less interest rate loan will be used for obtaining assessable income

by employee (Deutsch, et.al., 2015). However, deduction will not be offered to employer when

the amount is used by concerned associates of the employee irrespective of the underlying

purpose of use (Sadiq et, al., 2015).

Rapid Heat extends loan to Jasmine for personal work. The days on which loan is available to

Jasmine is 212 days. The number of days in tax assessment year is 365 days. The gross up rate is

taken for type II goods for March 31, 2018. Further, the FBT rate taken into account is 47% for

March 31, 2018.

Computation

It is apparent from case study that 90% loan is used to procure a holiday home which may bring

in assessable income for Jasmine. The employer can avail deduction on this loan portion if that

happens. However, 10% of loan is provided to husband by Jasmine which will not create any

availability of deduction for Rapid Heat despite there being a possibility of dividend income. It is

because the loan has been utilized by her husband not by Jasmine.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

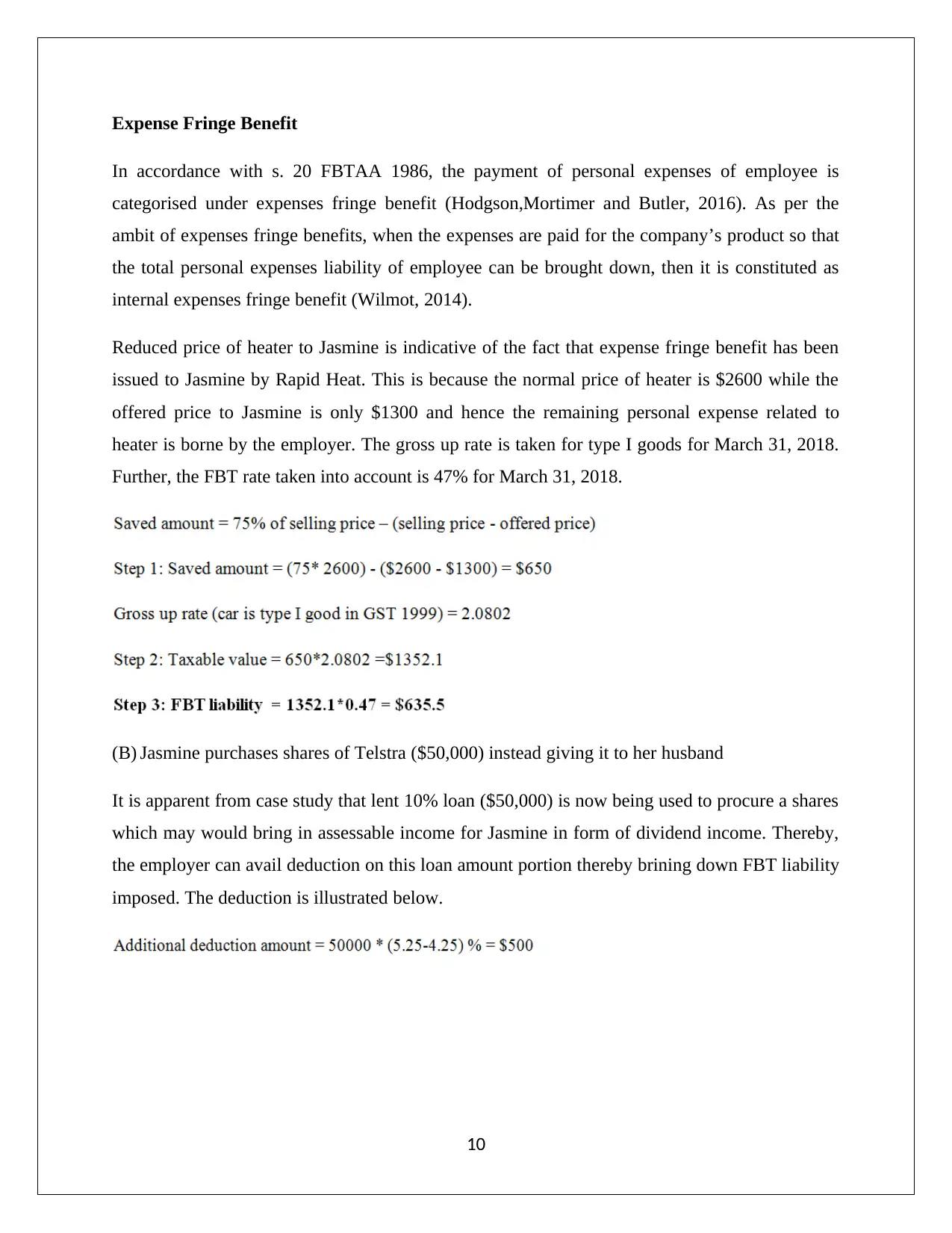

Expense Fringe Benefit

In accordance with s. 20 FBTAA 1986, the payment of personal expenses of employee is

categorised under expenses fringe benefit (Hodgson,Mortimer and Butler, 2016). As per the

ambit of expenses fringe benefits, when the expenses are paid for the company’s product so that

the total personal expenses liability of employee can be brought down, then it is constituted as

internal expenses fringe benefit (Wilmot, 2014).

Reduced price of heater to Jasmine is indicative of the fact that expense fringe benefit has been

issued to Jasmine by Rapid Heat. This is because the normal price of heater is $2600 while the

offered price to Jasmine is only $1300 and hence the remaining personal expense related to

heater is borne by the employer. The gross up rate is taken for type I goods for March 31, 2018.

Further, the FBT rate taken into account is 47% for March 31, 2018.

(B) Jasmine purchases shares of Telstra ($50,000) instead giving it to her husband

It is apparent from case study that lent 10% loan ($50,000) is now being used to procure a shares

which may would bring in assessable income for Jasmine in form of dividend income. Thereby,

the employer can avail deduction on this loan amount portion thereby brining down FBT liability

imposed. The deduction is illustrated below.

10

In accordance with s. 20 FBTAA 1986, the payment of personal expenses of employee is

categorised under expenses fringe benefit (Hodgson,Mortimer and Butler, 2016). As per the

ambit of expenses fringe benefits, when the expenses are paid for the company’s product so that

the total personal expenses liability of employee can be brought down, then it is constituted as

internal expenses fringe benefit (Wilmot, 2014).

Reduced price of heater to Jasmine is indicative of the fact that expense fringe benefit has been

issued to Jasmine by Rapid Heat. This is because the normal price of heater is $2600 while the

offered price to Jasmine is only $1300 and hence the remaining personal expense related to

heater is borne by the employer. The gross up rate is taken for type I goods for March 31, 2018.

Further, the FBT rate taken into account is 47% for March 31, 2018.

(B) Jasmine purchases shares of Telstra ($50,000) instead giving it to her husband

It is apparent from case study that lent 10% loan ($50,000) is now being used to procure a shares

which may would bring in assessable income for Jasmine in form of dividend income. Thereby,

the employer can avail deduction on this loan amount portion thereby brining down FBT liability

imposed. The deduction is illustrated below.

10

References

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2017) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., and Devos, K. (2016) Australian Taxation Study Manual 2016.

8th ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

Barkoczy, S. (2017) Foundation of Taxation Law 2017. 9th ed. Sydney: Oxford University Press.

Coleman, C. (2016) Australian Tax Analysis. 4th ed. Sydney: Thomson Reuters (Professional)

Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Krever, R. (2017) Australian Taxation Law Cases 2017. 2nd ed. Brisbane: THOMSON

LAWBOOK Company.

Nethercott, L., Richardson, G., and Devos, K. (2016) Australian Taxation Study Manual 2016.

8th ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.