Taxation Consequences on Disposal of Assets and Fringe Benefit Tax Calculation

VerifiedAdded on 2023/06/04

|11

|2195

|476

AI Summary

The article discusses the taxation consequences based on the type and nature of transactions done in regards to disposal of selected few assets. It also explains how to calculate Fringe Benefit Tax payable based on the benefits extended to employees. The article covers the relevant laws, classifications of receipts, CGT applicability, computation essentials, and application of the same. The subject is taxation, and the course code is not mentioned. The course name and college/university are not mentioned either.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Question 1

Issue

The issue is to extend advice to client (taxpayer) about her taxation consequences based on the

type and nature of the transactions which have been done in regards to disposal of selected few

assets.

Law

Classification of Receipts

The derived receipts from disposal of an asset can be either capital receipt or revenue receipt.

The determination of type of receipt is an imperative factor because if the receipt is categorised

as revenue receipts, then the relevant taxation consequences applied on the receipts would be

under s. 6(5), ITAA 1997. However, when the receipts are capital receipts, then the relevant tax

legislation is Capital Gains Tax (CGT) (Sadiq, et.al., 2015). The main aspect to draw the exact

type of receipt is the source and intention of the taxpayer while disposing the assets. If the

taxpayer is running a business which includes trading assets, then the receipts will be revenue

receipts and business transaction will be deriving ordinary income (Barkoczy, 2017). Further,

when the taxpayer does not engage in business based on trading assets and disposes the capital

assets then the derived sale proceeds will result in either capital gains or capital losses which will

be taxed as per CGT (Nethercott, Richardson and Devos, 2016).

CGT Applicability

The CGT would be applied on those assets which are not pre-CGT asset (purchased before

September 20, 1985) as these belong to the period which is after the CGT legislation was

implemented. This would be the first step to check the whether the disposed asset is pre-CGT or

not (Hodgson, Mortimer and Butler, 2016).

There are some cases where CGT will not be applicable even though they are not pre-CGT asset.

Likewise, if an asset is collectable of the taxpayer then CGT will be enforceable only if the total

amount spent by taxpayer for procuring the asset is higher than $ 500 as described in s. 118(10)

ITAA 1997 (Sadiq, et.al., 2015). Also, if an asset is personal use asset of the taxpayer then CGT

1

Issue

The issue is to extend advice to client (taxpayer) about her taxation consequences based on the

type and nature of the transactions which have been done in regards to disposal of selected few

assets.

Law

Classification of Receipts

The derived receipts from disposal of an asset can be either capital receipt or revenue receipt.

The determination of type of receipt is an imperative factor because if the receipt is categorised

as revenue receipts, then the relevant taxation consequences applied on the receipts would be

under s. 6(5), ITAA 1997. However, when the receipts are capital receipts, then the relevant tax

legislation is Capital Gains Tax (CGT) (Sadiq, et.al., 2015). The main aspect to draw the exact

type of receipt is the source and intention of the taxpayer while disposing the assets. If the

taxpayer is running a business which includes trading assets, then the receipts will be revenue

receipts and business transaction will be deriving ordinary income (Barkoczy, 2017). Further,

when the taxpayer does not engage in business based on trading assets and disposes the capital

assets then the derived sale proceeds will result in either capital gains or capital losses which will

be taxed as per CGT (Nethercott, Richardson and Devos, 2016).

CGT Applicability

The CGT would be applied on those assets which are not pre-CGT asset (purchased before

September 20, 1985) as these belong to the period which is after the CGT legislation was

implemented. This would be the first step to check the whether the disposed asset is pre-CGT or

not (Hodgson, Mortimer and Butler, 2016).

There are some cases where CGT will not be applicable even though they are not pre-CGT asset.

Likewise, if an asset is collectable of the taxpayer then CGT will be enforceable only if the total

amount spent by taxpayer for procuring the asset is higher than $ 500 as described in s. 118(10)

ITAA 1997 (Sadiq, et.al., 2015). Also, if an asset is personal use asset of the taxpayer then CGT

1

will be enforceable only if the total amount spent by taxpayer for procuring the asset is higher

than $ 10,000 as described in s. 108-20(1) ITAA 1997.

Computation Essentials

The capital assets disposal (for the given case) is termed as a CGT event and falls under A1

event and therefore, the formula has been taken for A1 event only under s. 104(5) ITAA 1997

(Nethercott, Richardson and Devos, 2016). This implies that cost base of asset and income from

disposed assets constitutes the two main factors for capital gains or losses computation. The cost

base comprises five elements which are listed below under s.110 (25) ITAA 1997 (Wilmot,

2014) (Gilders, et. al., 2015).

Elements of Cost Base

The income from disposal will be held realised for computation in the same financial year in

which it has been formed despite the factor that payment will not be received in that financial

year as explained under TR 94/29 (Reuters, 2017).

Any previous capital losses or derived capital losses must be balanced with capital gains

received under s. 102-5 ITAA 1997. If no gains are derived, then the capital losses which are

unadjusted will be carried forward to next tax year (Hodgson, Mortimer and Butler, 2016).

Holding period of asset that exceeds duration of 1 year will result in long term capital gains

when disposed. In such case, only 50% of capital gains or losses will be contributed in the

net capital gains or losses for CGT (Sadiq, et.al., 2015).

Application

2

than $ 10,000 as described in s. 108-20(1) ITAA 1997.

Computation Essentials

The capital assets disposal (for the given case) is termed as a CGT event and falls under A1

event and therefore, the formula has been taken for A1 event only under s. 104(5) ITAA 1997

(Nethercott, Richardson and Devos, 2016). This implies that cost base of asset and income from

disposed assets constitutes the two main factors for capital gains or losses computation. The cost

base comprises five elements which are listed below under s.110 (25) ITAA 1997 (Wilmot,

2014) (Gilders, et. al., 2015).

Elements of Cost Base

The income from disposal will be held realised for computation in the same financial year in

which it has been formed despite the factor that payment will not be received in that financial

year as explained under TR 94/29 (Reuters, 2017).

Any previous capital losses or derived capital losses must be balanced with capital gains

received under s. 102-5 ITAA 1997. If no gains are derived, then the capital losses which are

unadjusted will be carried forward to next tax year (Hodgson, Mortimer and Butler, 2016).

Holding period of asset that exceeds duration of 1 year will result in long term capital gains

when disposed. In such case, only 50% of capital gains or losses will be contributed in the

net capital gains or losses for CGT (Sadiq, et.al., 2015).

Application

2

For the given scenario, the applicable tax legislation is CGT as the taxpayer has capital assets

which she has disposed. Also, she has not carried any business activity by engaging in asset sale.

Whether the asset is pre-CGT or not is represented in the table given below.

Land Block: Block of land has been sold in year 2017/18 but taxpayer will be able to receive

the sale proceeds in 2018/19 and thus, as per TR 94/29, the expected CGT consequences will be

realised in 2017/18 only. The capital losses which are carried forward from last year would be

cancelled from the produced capital gains. Further, as indicated from the above, the holding

period of asset is higher than a year and 50% discount will be provided as exhibited below.

Antique Bed: CGT will be enforceable only if the total amount spent by taxpayer for procuring

the asset (collectable) is higher than $ 500. It is apparent that the procuring amount is $3500 for

antique bed. It indicates that the requisite condition is met and thus, CGT will be applicable.

3

which she has disposed. Also, she has not carried any business activity by engaging in asset sale.

Whether the asset is pre-CGT or not is represented in the table given below.

Land Block: Block of land has been sold in year 2017/18 but taxpayer will be able to receive

the sale proceeds in 2018/19 and thus, as per TR 94/29, the expected CGT consequences will be

realised in 2017/18 only. The capital losses which are carried forward from last year would be

cancelled from the produced capital gains. Further, as indicated from the above, the holding

period of asset is higher than a year and 50% discount will be provided as exhibited below.

Antique Bed: CGT will be enforceable only if the total amount spent by taxpayer for procuring

the asset (collectable) is higher than $ 500. It is apparent that the procuring amount is $3500 for

antique bed. It indicates that the requisite condition is met and thus, CGT will be applicable.

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Shares: None of the shares fall in the category of pre-CGT asset and cannot escape CGT

liability. However, discount under s.115-25 would be applicable to shares leading to long term

capital gains while not being provided to those which would yield short term capital gains.

Painting: It is categorised as a pre-CGT asset and thereby immune from application of CGT.

4

liability. However, discount under s.115-25 would be applicable to shares leading to long term

capital gains while not being provided to those which would yield short term capital gains.

Painting: It is categorised as a pre-CGT asset and thereby immune from application of CGT.

4

Violin: Violin can be identified both as a collectable or a personal use item. The latter seems

more suitable considering that the client is using the violin on continuous basis for personal

entertainment. Further, the cost price of the violin does not exceed $ 10,000 and hence immune

from CGT application.

Conclusion

Cumulative capital gains

Question 2

Issue

Fringe Benefit Tax payable (FBT payable) would be computed based on the given information in

which the employer ‘Rapid Heat has extended three benefits to employee “Jasmine.”

Law

The “Fringe Benefit Tax Assessment Act 1986 (FBTAA 1986)” is used to analyse the given

benefit based on the relevant sections (Reuters, 2017).

Car fringe benefit:

As per s. 7 FBTAA1986, if employer has issued the permission to employee to take the car for

his/her own work, then it is assumed that car fringe benefits are extended (Deutsch, et.al., 2015).

The FBT will be payable by employer and the beneficiary who takes the car in use for personal

purposes will not be held responsible for FBT burden. The total amount of car fringe benefit for

5

more suitable considering that the client is using the violin on continuous basis for personal

entertainment. Further, the cost price of the violin does not exceed $ 10,000 and hence immune

from CGT application.

Conclusion

Cumulative capital gains

Question 2

Issue

Fringe Benefit Tax payable (FBT payable) would be computed based on the given information in

which the employer ‘Rapid Heat has extended three benefits to employee “Jasmine.”

Law

The “Fringe Benefit Tax Assessment Act 1986 (FBTAA 1986)” is used to analyse the given

benefit based on the relevant sections (Reuters, 2017).

Car fringe benefit:

As per s. 7 FBTAA1986, if employer has issued the permission to employee to take the car for

his/her own work, then it is assumed that car fringe benefits are extended (Deutsch, et.al., 2015).

The FBT will be payable by employer and the beneficiary who takes the car in use for personal

purposes will not be held responsible for FBT burden. The total amount of car fringe benefit for

5

personal use of the employee will be calculated through statutory procedure s. 9, FBTAA 1986

(Woellner, 2017).

When the employee does not contribute in car purchase then the last variable will become zero.

The base value is the amount which would be determined after eliminating the minor repair

expenses from the total buying cost of car. The available days will also comprise of the period

when car is not used but was available for use (such as in airport parking) and when it has been

shifted to garage on the account of minor repair (Nethercott, Richardson and Devos, 2016).

Loan fringe benefit

For assessment year 2017/18, the standard benchmark rate of interest for providing the loan is

5.25% per annum which has been specified by Reserve Bank of Australia. The loan which has

been given in year 2017/18 at a lower interest rate than the benchmark rate will lead to extension

of loan fringe benefit. The FBT burden is imposed on employer only (Wilmot, 2014). Moreover,

the loan which has been realised by employee for production of ordinary income purpose, then

the loan amount will lead to production of FBT deduction for employer. However, this deduction

would not be available when the loan has been realised by associate of employee for the same

purpose (Reuters, 2017).

Expense fringe benefit

Making the payment of personal nature expenses of employee or providing lower price of

company’s product would amount to expense fringe benefit (Gilders, et. al., 2015).

For all the above three benefits gross up factor (based on type of goods) will be included while

calculating the taxable value of fringe benefit. Further, the FBT rate for the assessment year will

also be applied on the taxable value for computing the net FBT payable (Woellner, 2017).

6

(Woellner, 2017).

When the employee does not contribute in car purchase then the last variable will become zero.

The base value is the amount which would be determined after eliminating the minor repair

expenses from the total buying cost of car. The available days will also comprise of the period

when car is not used but was available for use (such as in airport parking) and when it has been

shifted to garage on the account of minor repair (Nethercott, Richardson and Devos, 2016).

Loan fringe benefit

For assessment year 2017/18, the standard benchmark rate of interest for providing the loan is

5.25% per annum which has been specified by Reserve Bank of Australia. The loan which has

been given in year 2017/18 at a lower interest rate than the benchmark rate will lead to extension

of loan fringe benefit. The FBT burden is imposed on employer only (Wilmot, 2014). Moreover,

the loan which has been realised by employee for production of ordinary income purpose, then

the loan amount will lead to production of FBT deduction for employer. However, this deduction

would not be available when the loan has been realised by associate of employee for the same

purpose (Reuters, 2017).

Expense fringe benefit

Making the payment of personal nature expenses of employee or providing lower price of

company’s product would amount to expense fringe benefit (Gilders, et. al., 2015).

For all the above three benefits gross up factor (based on type of goods) will be included while

calculating the taxable value of fringe benefit. Further, the FBT rate for the assessment year will

also be applied on the taxable value for computing the net FBT payable (Woellner, 2017).

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Application

(A) Calculation of the FBT payable for the benefits

Car fringe benefit: Rapid Heat issued a car to Jasmine clearly for personal work and thus,

fringe benefit tax would be payable by Rapid Heat. Moreover, the procurement amount and the

minor repair expenses have been paid by Rapid Heat only which will be used to find the exact

base value of car. No deductions are available for the parking of car at airport and the time taken

for minor repairs at garage.

Loan fringe benefit: Rapid Heat issued loan to Jasmine, clearly for personal work and at

concessional interest rate which is 4.25% whereby the standard benchmark rate for 2017/18 is

5.25% p.a. Thus, loan fringe benefit tax would be payable by Rapid Heat.

Tax deduction claim:

7

(A) Calculation of the FBT payable for the benefits

Car fringe benefit: Rapid Heat issued a car to Jasmine clearly for personal work and thus,

fringe benefit tax would be payable by Rapid Heat. Moreover, the procurement amount and the

minor repair expenses have been paid by Rapid Heat only which will be used to find the exact

base value of car. No deductions are available for the parking of car at airport and the time taken

for minor repairs at garage.

Loan fringe benefit: Rapid Heat issued loan to Jasmine, clearly for personal work and at

concessional interest rate which is 4.25% whereby the standard benchmark rate for 2017/18 is

5.25% p.a. Thus, loan fringe benefit tax would be payable by Rapid Heat.

Tax deduction claim:

7

90% of loan ($450,000) has spent by Jasmine to purchase a holiday home. This purchase may

offer her rent income (ordinary income) if she decided to rent it. In this case, the tax deduction

claim can be requested by Rapid Heat.

10% of loan ($50,000) has spent by her husband because she has given this amount to him to buy

shares. This share purchase may offer dividend but no tax deduction claim is available because

the purchase has been done by her husband.

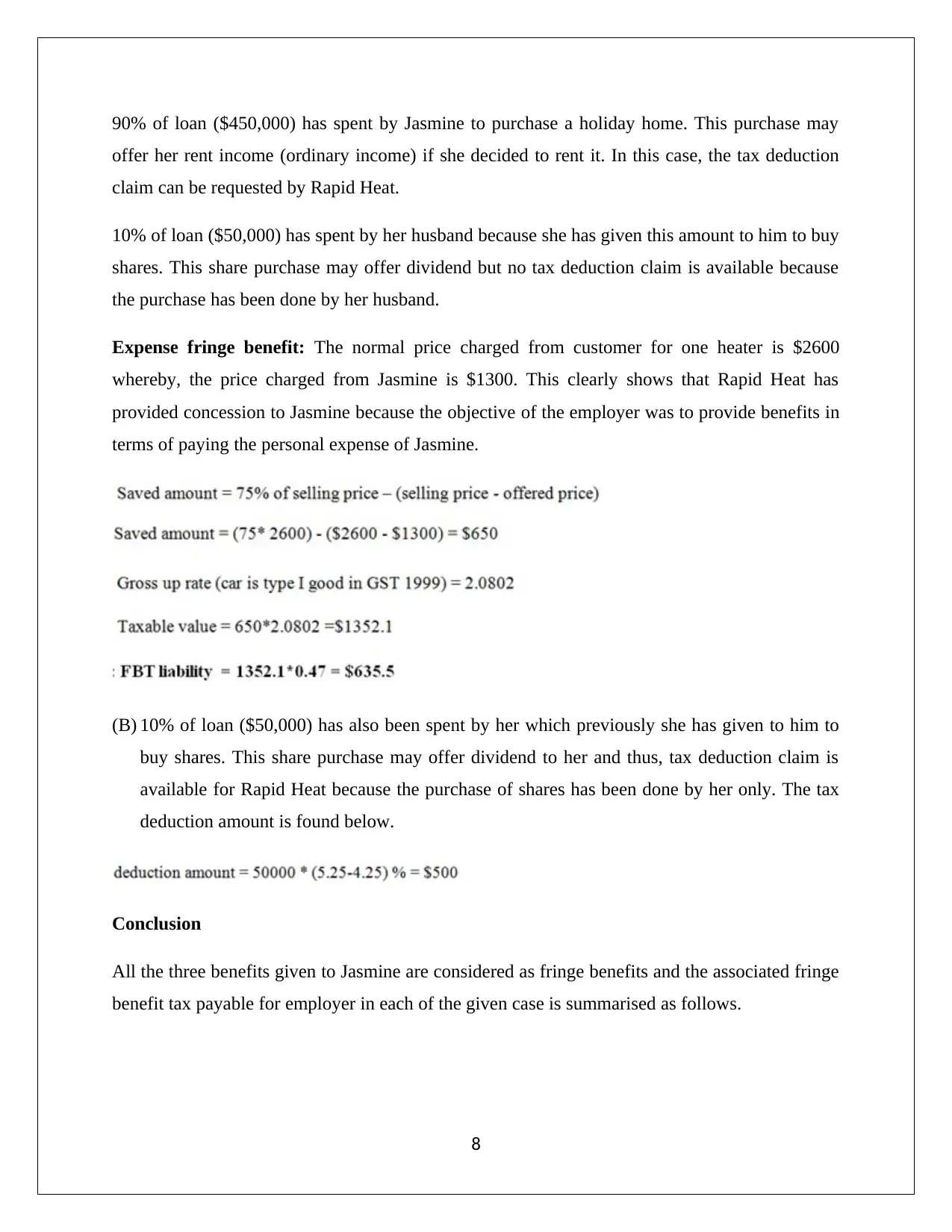

Expense fringe benefit: The normal price charged from customer for one heater is $2600

whereby, the price charged from Jasmine is $1300. This clearly shows that Rapid Heat has

provided concession to Jasmine because the objective of the employer was to provide benefits in

terms of paying the personal expense of Jasmine.

(B) 10% of loan ($50,000) has also been spent by her which previously she has given to him to

buy shares. This share purchase may offer dividend to her and thus, tax deduction claim is

available for Rapid Heat because the purchase of shares has been done by her only. The tax

deduction amount is found below.

Conclusion

All the three benefits given to Jasmine are considered as fringe benefits and the associated fringe

benefit tax payable for employer in each of the given case is summarised as follows.

8

offer her rent income (ordinary income) if she decided to rent it. In this case, the tax deduction

claim can be requested by Rapid Heat.

10% of loan ($50,000) has spent by her husband because she has given this amount to him to buy

shares. This share purchase may offer dividend but no tax deduction claim is available because

the purchase has been done by her husband.

Expense fringe benefit: The normal price charged from customer for one heater is $2600

whereby, the price charged from Jasmine is $1300. This clearly shows that Rapid Heat has

provided concession to Jasmine because the objective of the employer was to provide benefits in

terms of paying the personal expense of Jasmine.

(B) 10% of loan ($50,000) has also been spent by her which previously she has given to him to

buy shares. This share purchase may offer dividend to her and thus, tax deduction claim is

available for Rapid Heat because the purchase of shares has been done by her only. The tax

deduction amount is found below.

Conclusion

All the three benefits given to Jasmine are considered as fringe benefits and the associated fringe

benefit tax payable for employer in each of the given case is summarised as follows.

8

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

References

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Nethercott, L., Richardson, G., and Devos, K. (2016) Australian Taxation Study Manual 2016.

8th ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

10

Barkoczy, S. (2017) Core Tax Legislation and Study Guide 2017. 2nd ed. Sydney: Oxford

University Press Australia.

Deutsch, R., Freizer, M., Fullerton, I., Hanley, P., and Snape, T. (2015) Australian tax handbook.

8th ed. Pymont: Thomson Reuters.

Gilders, F., Taylor, J., Walpole, M., Burton, M. and Ciro, T. (2016) Understanding taxation law

2016. 9th ed. Sydney: LexisNexis/Butterworths.

Hodgson, H., Mortimer, C. and Butler, J. (2016) Tax Questions and Answers 2016. 6th ed.

Sydney: Thomson Reuters.

Nethercott, L., Richardson, G., and Devos, K. (2016) Australian Taxation Study Manual 2016.

8th ed. Sydney: Oxford University Press.

Reuters, T. (2017) Australian Tax Legislation (2017). 4th ed. Sydney. THOMSON REUTERS.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., Obst, W., and Ting, A.

(2015) Principles of Taxation Law 2015. 7th ed. Pymont: Thomson Reuters.

Wilmot, C. (2014) FBT Compliance guide. 6th ed. North Ryde: CCH Australia Limited.

Woellner, R., Barkoczy, S., Murphy, S. and Pinto, D. (2017). Australian Taxation Law Select

Legislation and Commentary Curtin 2017. 2nd ed. Sydney: Oxford University Press Australia.

10

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.