Taxation Law Assignment: Capital Gains and Fringe Benefits

VerifiedAdded on 2019/10/31

|8

|1476

|247

Homework Assignment

AI Summary

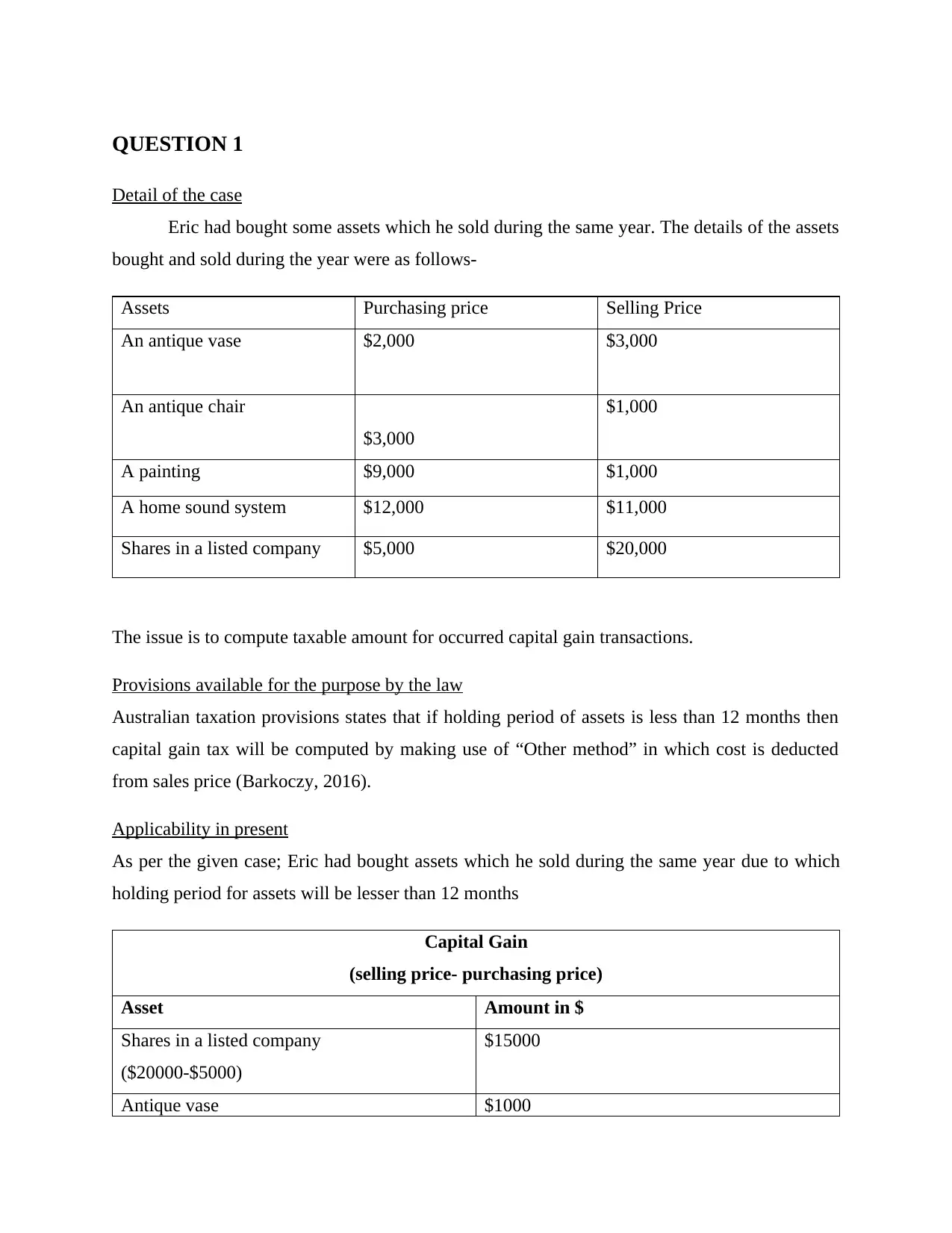

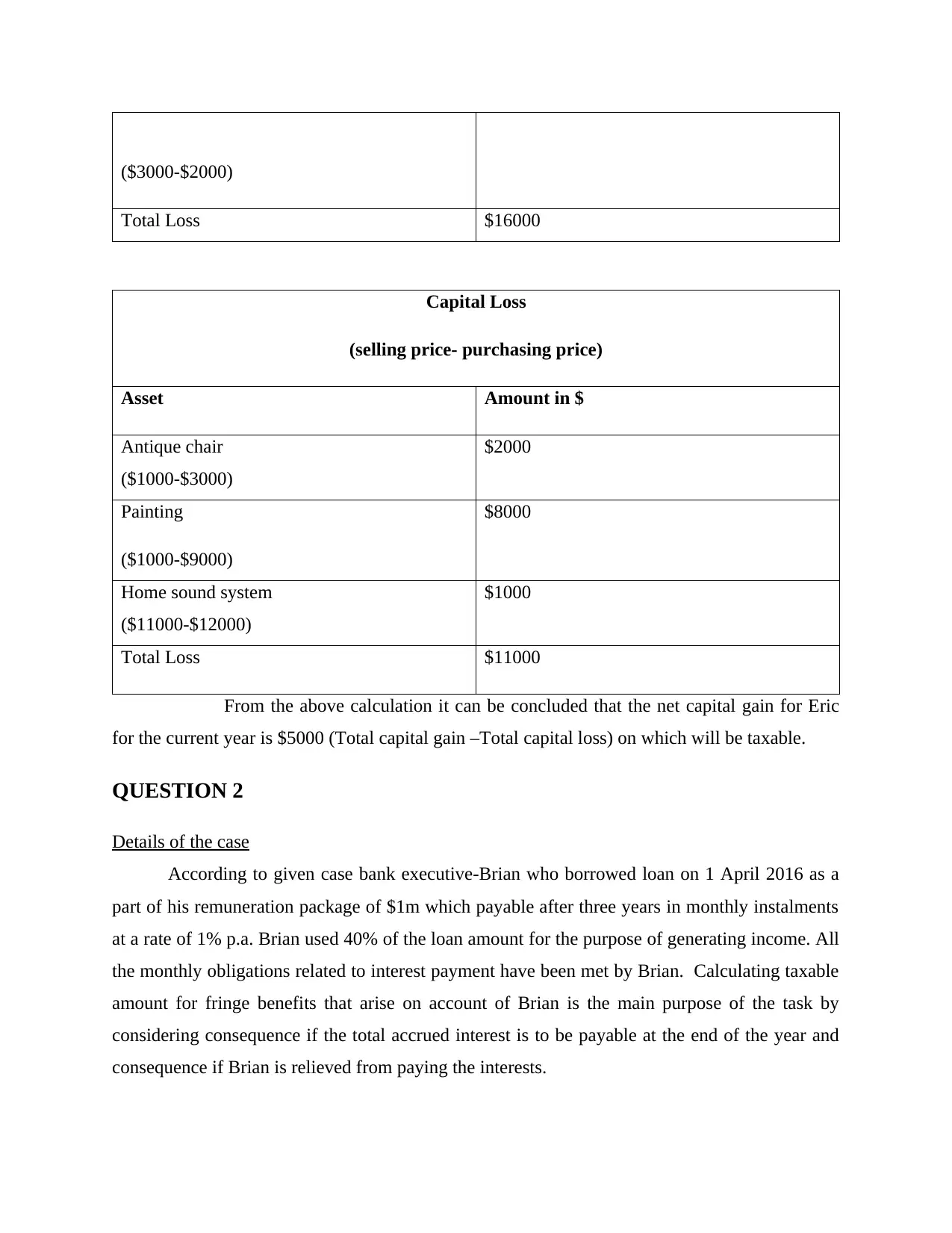

This document presents a comprehensive solution to a taxation assignment, addressing various aspects of Australian tax law. The assignment covers the computation of taxable amounts for capital gains transactions, considering assets like shares, antique items, and home sound systems. It delves into fringe benefits, analyzing the taxable value of loans provided to bank executives and the impact of interest rates. The solution also examines the allocation of gains and losses for joint tenants in a rental property, considering partnership agreements. Furthermore, it explores tax implications related to agreements made by an employer with employees and the taxation of income from timber extraction, including royalty payments and lump-sum receipts. The solution references relevant Australian taxation provisions, including TR 93/32 and TR 95/6, to support its analysis and conclusions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.