Provisions available for the purpose by the law in Taxation Question 1 3

8 Pages1476 Words247 Views

Added on 2019-10-31

About This Document

Taxation Question 1 3 Detail of the case 3 Provisions available for the purpose by the law 3 Applicability in present 3 Question 2 4 Details of the case 4 Provisions available for the purpose by the law 5 Applicability of the law to the present case 5 Question-3 5 Provisions available for the purpose by the law 6 Applicability of the provisions in the present case 6 Question-4 6 Case 6 Provisions available for the purpose by the law 6 Applicability in present 6 Question- 5

Provisions available for the purpose by the law in Taxation Question 1 3

Added on 2019-10-31

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.

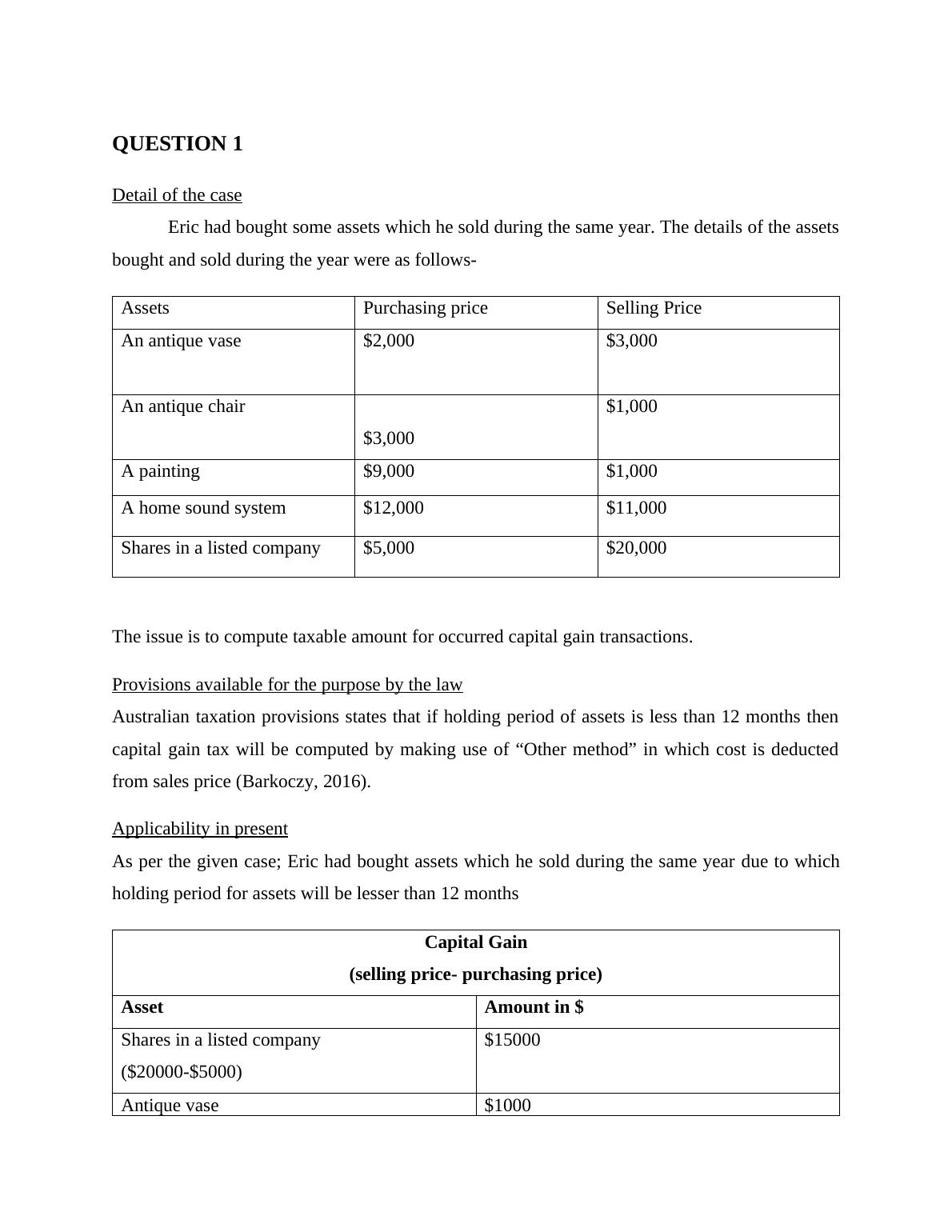

HI6028 Taxation Theory, Practice & Law T2 2017 Individual Assignment Question 1: Calculating the net capital loss or gain from the bought and sold by Eric

|8

|2435

|402

Taxation theory TAXATION THEORY Answer 1 For over twelve months Eric has bought some assets which have not been mentioned in the time span exceeded

|8

|2525

|81

HI6028 Taxation Theory, Practice & Law T2 2017 Individual Assignment

|14

|2884

|103

HI6028 Assignment On Taxation Theory, Practice & Law

|9

|1683

|55

Taxation Practice, Theory and Law - Assignment

|10

|1898

|113

HI6028 - Taxation Theory, Practice & Law

|10

|2254

|159