HI6028 Taxation Theory, Practice & Law Assignment: Tax Implications

VerifiedAdded on 2023/06/04

|13

|3198

|230

Homework Assignment

AI Summary

This assignment solution addresses taxation implications for a client, focusing on capital gains tax (CGT) and fringe benefits tax (FBT). Question 1 analyzes the sale of various assets, including vacant land, an antique bed, a painting, shares, and a violin, determining CGT liabilities based on acquisition dates, holding periods, and relevant tax laws. It calculates capital gains, considers pre-CGT assets, and applies rebates where applicable. Question 2 examines fringe benefits provided by an employer, Rapid Heat, to an employee, Jasmine, including car fringe benefits, loan fringe benefits, and expense fringe benefits. The solution assesses FBT consequences, calculates taxable values, and considers tax deductions for loan usage. The assignment references relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986), along with relevant rulings and case law.

Taxation Theory, Practice & Law

STUDENT NAME/ID

[Pick the date]

STUDENT NAME/ID

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

Issue

The issue is to consult the taxpayer about her taxation implications for year 2017/18 on the

account of received capital proceeds from the disposal of the capital assets belonging to

taxpayer.

Law

When the taxpayer does not carry a business course of action of trading the assets for deriving

the assessable income, then the disposal of assets would be considered as capital receipts not

revenue receipts (Barkoczy, 2017). Therefore, the applicable taxation treatment would be Capital

Gains Tax (CGT).

1) Pre-CGT assets

The CGT will not be imposed on the received capital gains when the disposed asset is a pre-CGT

asset (Deutsch, et.al., 2015). The assets that are purchased before September 20, 1985 are named

as pre-CGT asset (s. 149 (10), ITAA 1997 (Coleman, 2016). Thus, the first step would be to

decide whether the asset is pre-CGT asset or not.

2) Transaction

The exact procedure for calculating the capital gains/losses from the asset disposal would be

decided based on the type of transaction (Nethercott, Richardson & Devos, 2016). For the given

scenarios, the transaction is considered as CGT event (TYPE A1) and hence, the income resulted

from disposal of the respective capital asset would be used to deduct the cost base of the capital

asset (S. 104 (5), ITAA 1997) (Woellner, 2017).

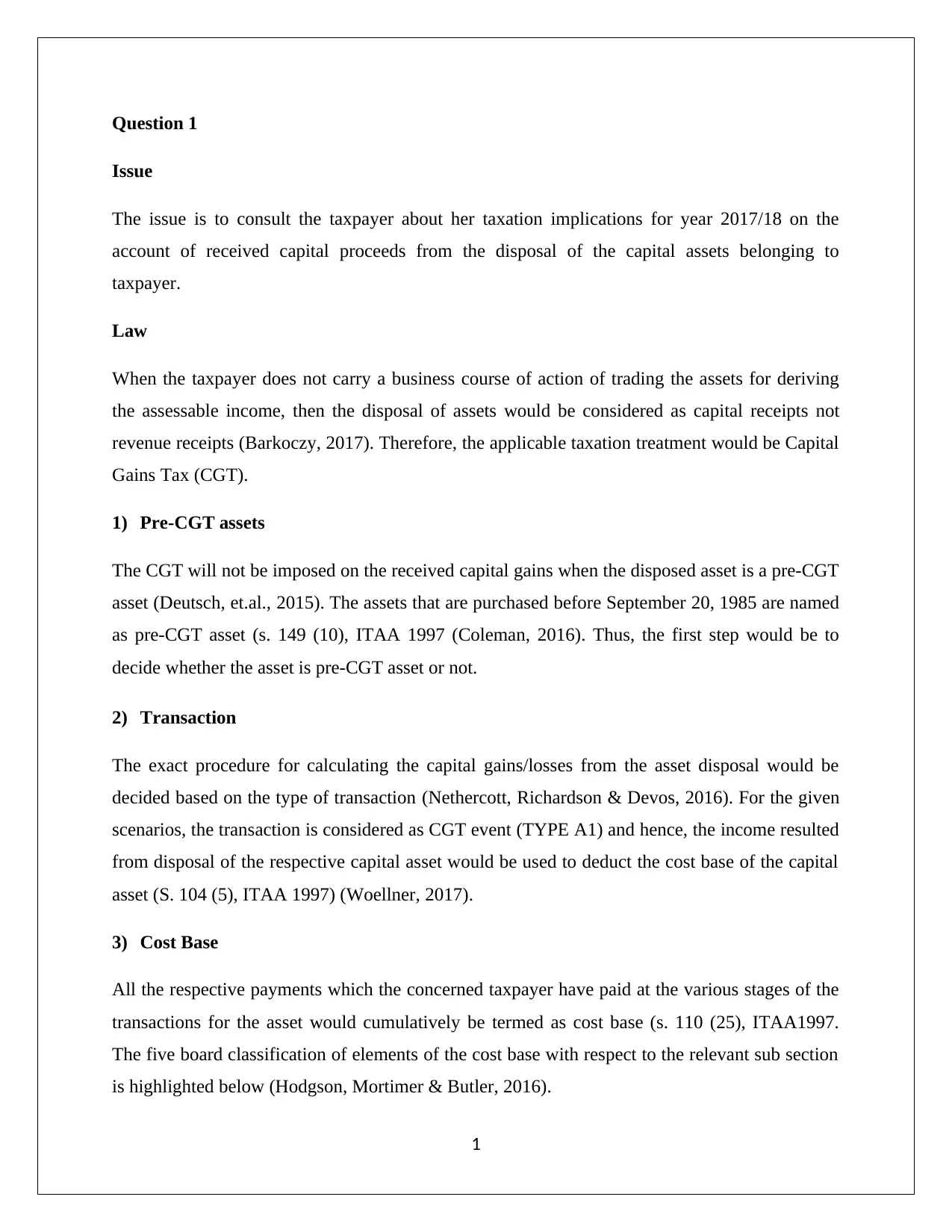

3) Cost Base

All the respective payments which the concerned taxpayer have paid at the various stages of the

transactions for the asset would cumulatively be termed as cost base (s. 110 (25), ITAA1997.

The five board classification of elements of the cost base with respect to the relevant sub section

is highlighted below (Hodgson, Mortimer & Butler, 2016).

1

Issue

The issue is to consult the taxpayer about her taxation implications for year 2017/18 on the

account of received capital proceeds from the disposal of the capital assets belonging to

taxpayer.

Law

When the taxpayer does not carry a business course of action of trading the assets for deriving

the assessable income, then the disposal of assets would be considered as capital receipts not

revenue receipts (Barkoczy, 2017). Therefore, the applicable taxation treatment would be Capital

Gains Tax (CGT).

1) Pre-CGT assets

The CGT will not be imposed on the received capital gains when the disposed asset is a pre-CGT

asset (Deutsch, et.al., 2015). The assets that are purchased before September 20, 1985 are named

as pre-CGT asset (s. 149 (10), ITAA 1997 (Coleman, 2016). Thus, the first step would be to

decide whether the asset is pre-CGT asset or not.

2) Transaction

The exact procedure for calculating the capital gains/losses from the asset disposal would be

decided based on the type of transaction (Nethercott, Richardson & Devos, 2016). For the given

scenarios, the transaction is considered as CGT event (TYPE A1) and hence, the income resulted

from disposal of the respective capital asset would be used to deduct the cost base of the capital

asset (S. 104 (5), ITAA 1997) (Woellner, 2017).

3) Cost Base

All the respective payments which the concerned taxpayer have paid at the various stages of the

transactions for the asset would cumulatively be termed as cost base (s. 110 (25), ITAA1997.

The five board classification of elements of the cost base with respect to the relevant sub section

is highlighted below (Hodgson, Mortimer & Butler, 2016).

1

4) Applicable rebate %

The rebate (50%) will only be applicable on long term capital gains (Reuters, 2017). Hence, it is

essential to differentiate between long term and short term capital gains. The best way to

ascertain this is to find the holding period of the asset by the taxpayer (Nethercott, Richardson &

Devos, 2016).

Holding period of asset > 1 year: Long term capital gains

Holding period of asset < 1 year: Short term capital gains

Further, no rebate will be applicable on short term capital gains (Deutsch, et.al., 2015).

5) Balancing the capital losses

The taxpayer will either receive capital gains or capital losses from the disposal of assets. When

the taxpayer has earned capital losses, then it is essential to balance the capital losses with capital

gains which are derived from similar capital asset disposal (Krever, 2017). Further, when only

capital losses are received by taxpayer, then these capital losses will be taken to the next year. It

means the unbalanced capital losses will be transferred to the next year and will be adjusted with

capital gains of next year (Wilmot, 2014).

6) Consideration of proceeds

As per TR 94/29, the income which would be derived from sale of asset will be realised for CGT

consequences in the same year in which the contract of sale has been entered into by the parties

(Coleman, 2016). This aspect will remain unchanged when the income will be received in next

year and enactment of contract has been done in present income year (Sadiq, et.al., 2015).

2

The rebate (50%) will only be applicable on long term capital gains (Reuters, 2017). Hence, it is

essential to differentiate between long term and short term capital gains. The best way to

ascertain this is to find the holding period of the asset by the taxpayer (Nethercott, Richardson &

Devos, 2016).

Holding period of asset > 1 year: Long term capital gains

Holding period of asset < 1 year: Short term capital gains

Further, no rebate will be applicable on short term capital gains (Deutsch, et.al., 2015).

5) Balancing the capital losses

The taxpayer will either receive capital gains or capital losses from the disposal of assets. When

the taxpayer has earned capital losses, then it is essential to balance the capital losses with capital

gains which are derived from similar capital asset disposal (Krever, 2017). Further, when only

capital losses are received by taxpayer, then these capital losses will be taken to the next year. It

means the unbalanced capital losses will be transferred to the next year and will be adjusted with

capital gains of next year (Wilmot, 2014).

6) Consideration of proceeds

As per TR 94/29, the income which would be derived from sale of asset will be realised for CGT

consequences in the same year in which the contract of sale has been entered into by the parties

(Coleman, 2016). This aspect will remain unchanged when the income will be received in next

year and enactment of contract has been done in present income year (Sadiq, et.al., 2015).

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Application

Assets

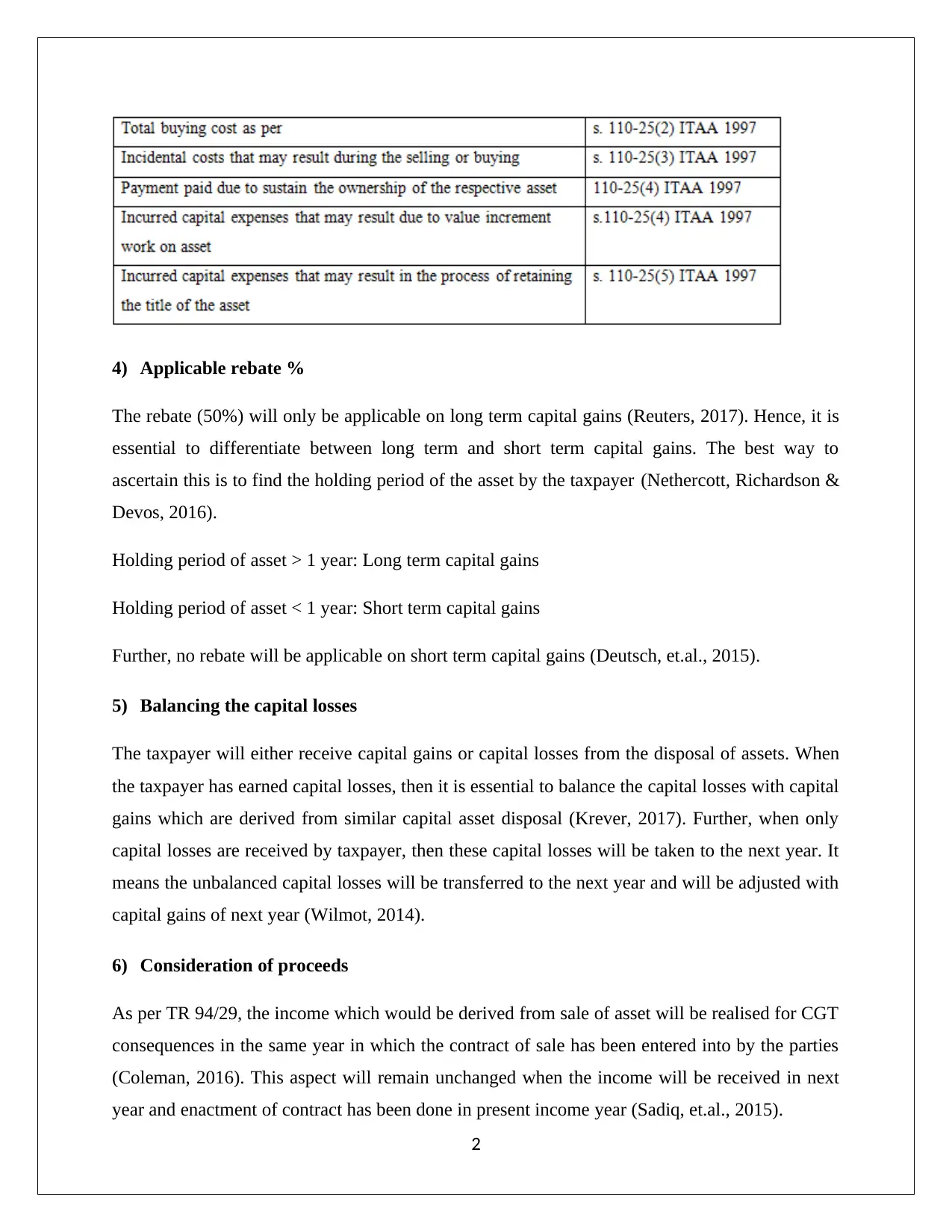

1) Block of vacant land

Acquisition date: 2001

The date itself defines that block of land is not a pre-CGT asset. Hence, CGT treatment would be

levied on the received capital gains or losses. Further, the taxpayer has sold the land block which

indicates that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the

asset will be calculated. The income of sale of land will be received in next year while the

contract of sale has been made in 2017/18. However, the income will be realised in the

assessment year only. The capital losses ($7000) of last year will also be balanced with the

obtained capital gains. At last, 50% rebate will be directed on the long term capital gains to find

the net capital gains from block land sale (Holding period of asset > 1 year: Long term capital

gains).

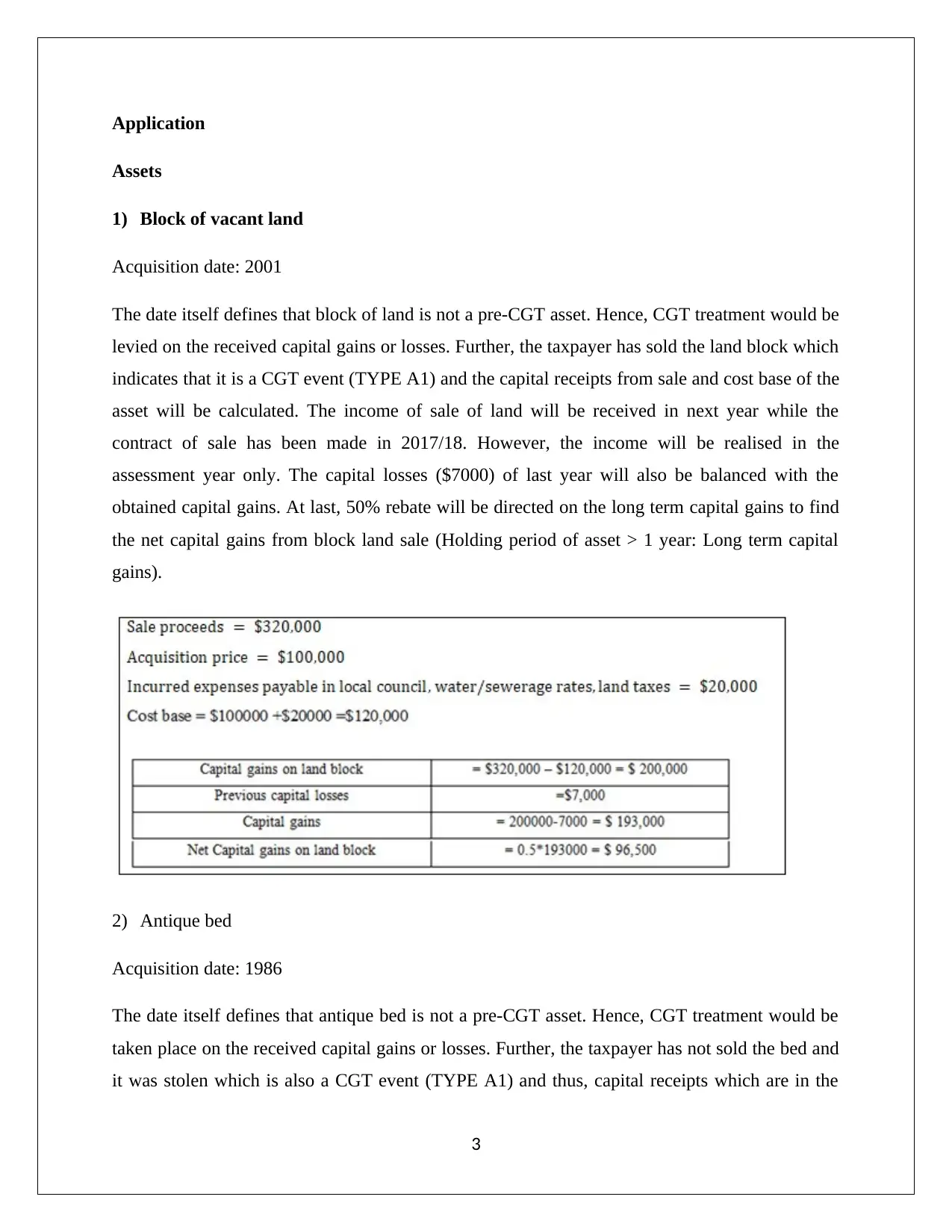

2) Antique bed

Acquisition date: 1986

The date itself defines that antique bed is not a pre-CGT asset. Hence, CGT treatment would be

taken place on the received capital gains or losses. Further, the taxpayer has not sold the bed and

it was stolen which is also a CGT event (TYPE A1) and thus, capital receipts which are in the

3

Assets

1) Block of vacant land

Acquisition date: 2001

The date itself defines that block of land is not a pre-CGT asset. Hence, CGT treatment would be

levied on the received capital gains or losses. Further, the taxpayer has sold the land block which

indicates that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the

asset will be calculated. The income of sale of land will be received in next year while the

contract of sale has been made in 2017/18. However, the income will be realised in the

assessment year only. The capital losses ($7000) of last year will also be balanced with the

obtained capital gains. At last, 50% rebate will be directed on the long term capital gains to find

the net capital gains from block land sale (Holding period of asset > 1 year: Long term capital

gains).

2) Antique bed

Acquisition date: 1986

The date itself defines that antique bed is not a pre-CGT asset. Hence, CGT treatment would be

taken place on the received capital gains or losses. Further, the taxpayer has not sold the bed and

it was stolen which is also a CGT event (TYPE A1) and thus, capital receipts which are in the

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

form of amount received from insurance claim and cost base of the asset will be calculated for

capital gains/losses.

Antique items are categorised as collectables and it is important to check the validity of the

pivotal condition of the collectable for the applicability of capital gain tax liability. The CGT is

imposed on the capital gains/loss on the asset which is acquired for at least $500 or more. The

taxpayer procured the antique bed for her collection for $3500 which is clearly fulfilled the

pivotal condition of CGT application for collectables.

The capital losses ($1500) of the last year will also be balanced with the obtained capital gains.

At last, 50% rebate will be directed on the long term capital gains to find the net capital gains

from antique bed (Holding period of asset > 1 year: Long term capital gains).

3) Painting

Acquisition date: May 2, 1985

The date itself defines that painting is a pre-CGT asset. Hence, CGT treatment would not be

taken place on the received capital gains or losses.

4

capital gains/losses.

Antique items are categorised as collectables and it is important to check the validity of the

pivotal condition of the collectable for the applicability of capital gain tax liability. The CGT is

imposed on the capital gains/loss on the asset which is acquired for at least $500 or more. The

taxpayer procured the antique bed for her collection for $3500 which is clearly fulfilled the

pivotal condition of CGT application for collectables.

The capital losses ($1500) of the last year will also be balanced with the obtained capital gains.

At last, 50% rebate will be directed on the long term capital gains to find the net capital gains

from antique bed (Holding period of asset > 1 year: Long term capital gains).

3) Painting

Acquisition date: May 2, 1985

The date itself defines that painting is a pre-CGT asset. Hence, CGT treatment would not be

taken place on the received capital gains or losses.

4

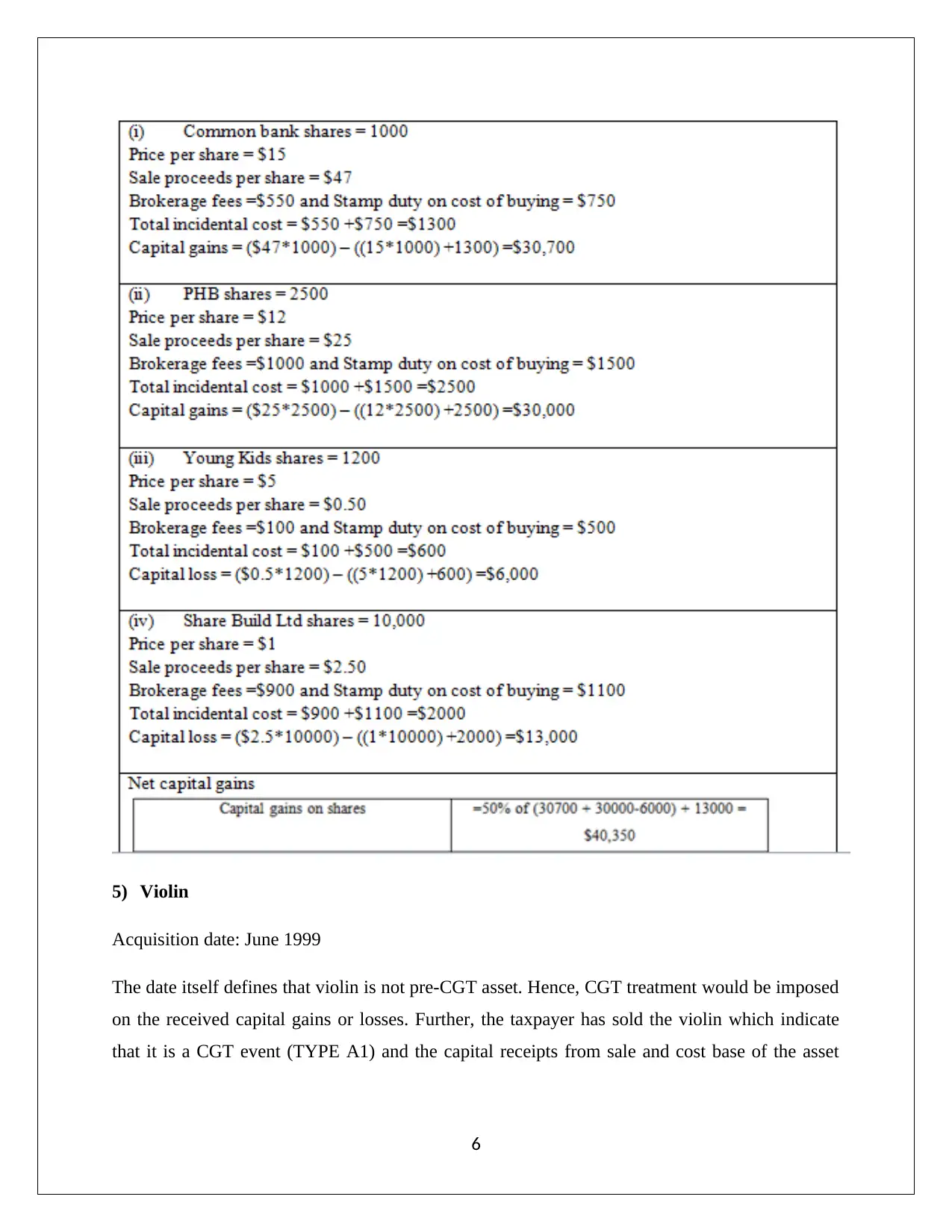

4) Shares

Acquisition date: After September 1985

The date itself defines that shares are not pre-CGT assets. Hence, CGT treatment would be

imposed on the received capital gains or losses. Further, the taxpayer has sold the shares which

indicate that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the

asset will be calculated. At last, 50% rebate will be directed on the long term capital gains (initial

three shares) to find the net capital gains from shares sale (Holding period of asset > 1 year:

Long term capital gains). Further, shares acquired of Share Build Ltd would short term capital

gains and 0% rebate will be directed. (Holding period of asset < 1 year: short term capital gains).

5

Acquisition date: After September 1985

The date itself defines that shares are not pre-CGT assets. Hence, CGT treatment would be

imposed on the received capital gains or losses. Further, the taxpayer has sold the shares which

indicate that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the

asset will be calculated. At last, 50% rebate will be directed on the long term capital gains (initial

three shares) to find the net capital gains from shares sale (Holding period of asset > 1 year:

Long term capital gains). Further, shares acquired of Share Build Ltd would short term capital

gains and 0% rebate will be directed. (Holding period of asset < 1 year: short term capital gains).

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5) Violin

Acquisition date: June 1999

The date itself defines that violin is not pre-CGT asset. Hence, CGT treatment would be imposed

on the received capital gains or losses. Further, the taxpayer has sold the violin which indicate

that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the asset

6

Acquisition date: June 1999

The date itself defines that violin is not pre-CGT asset. Hence, CGT treatment would be imposed

on the received capital gains or losses. Further, the taxpayer has sold the violin which indicate

that it is a CGT event (TYPE A1) and the capital receipts from sale and cost base of the asset

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

will be calculated. Further, it can be seen that violin which she has sold for $5,500 is not a

collectable as it is a personal use asset. The supportive factors are underlying below.

She herself plays violin

The frequency of playing violin is quite often or rather regular

She used to play violin for personal enjoyment/entertainment

The condition to check the CGT implication applicability for personal use asset is that the asset

must be bought for a price higher than $10,000. Thus, the condition is not true for the present

scenario as the buying cost is lower than $10,000 and hence, CGT is not applicable.

Capital Gains (Cumulative)

Conclusion

Taxpayer has cumulative capital gains of $139,100 from the disposal of block of vacant land,

shares and antique bed and the CGT will be applicable on the calculated capital gains only.

Further, disposal of painting and violin does not result any CGT implication on taxpayer as

painting is a pre-CGT asset and violin is a personal use asset which does not satisfy the requisite

condition for CGT implication.

Question 2

Issue

The issue is to analyse the given benefits by Rapid Heat to Jasmine during the assessment year

and also their respective FBT consequences. Further, the tax deduction claim would also be

analysed for the loan amount which is utilized by Jasmine in different ways.

Law

The set of potential personal benefits (not in form of cash) which are provided to the employees

are called as fringe benefits. Any benefits which are provided to employee for office/professional

7

collectable as it is a personal use asset. The supportive factors are underlying below.

She herself plays violin

The frequency of playing violin is quite often or rather regular

She used to play violin for personal enjoyment/entertainment

The condition to check the CGT implication applicability for personal use asset is that the asset

must be bought for a price higher than $10,000. Thus, the condition is not true for the present

scenario as the buying cost is lower than $10,000 and hence, CGT is not applicable.

Capital Gains (Cumulative)

Conclusion

Taxpayer has cumulative capital gains of $139,100 from the disposal of block of vacant land,

shares and antique bed and the CGT will be applicable on the calculated capital gains only.

Further, disposal of painting and violin does not result any CGT implication on taxpayer as

painting is a pre-CGT asset and violin is a personal use asset which does not satisfy the requisite

condition for CGT implication.

Question 2

Issue

The issue is to analyse the given benefits by Rapid Heat to Jasmine during the assessment year

and also their respective FBT consequences. Further, the tax deduction claim would also be

analysed for the loan amount which is utilized by Jasmine in different ways.

Law

The set of potential personal benefits (not in form of cash) which are provided to the employees

are called as fringe benefits. Any benefits which are provided to employee for office/professional

7

work are not categorised as fringe benefit (Woellner, 2017). There is a separate taxation law to

treat the tax implication on employee and employer for fringe benefit which is known as “Fringe

Benefits Tax Assessment Act 1986 (FBTAA 1986).” This tax is applicable on employer not on

the employee (Reuters, 2017).

“Car Fringe Benefit”

The critical condition that must be satisfied for providing car fringe benefit is that the employer

must issue car to employee so that the employee can use the car as per his/her choice for personal

work. According to s.7, FBTAA 1986, the car fringe benefits will not be given to employee by

their employer when the usage of offered car is restricted to office purpose only (Nethercott,

Richardson & Devos, 2016). The extension of car and authority to use the car for personal

interest work may be provided either in oral form or in written form. Furthermore, the way of

action of the employer may also provide sufficient clue that employer has issued car to employee

for personal work. In this regards, the practice of car parking at employee’s own garage or at

house implies that the employee directly get the permission to use the car due to presence of

implicit permission of the employee (Hodgson,Mortimer & Butler, 2016). Capital value of car is

a function of purchasing price which has been paid on behalf of the employer and the respective

amount called deductions which are also paid by the employer in order to pay the minor repair

expenses. According to s.9, FBTAA 1986 the deduction on days would not be imposed from

total period of personal utilization when the car is not present for her and sent for minor repairing

(Gilders, et. al., 2015). Further, the inclusion of the utilization would be followed means the

actual use of car is not essential for computing the total period of car utilization for personal

work (Krever, 2017).

“Loan Fringe Benefit”

According to s. 16, FBTAA loan fringe benefit is issued when the employer has taken

concessional rate of interest as compared with the statutory interest rate while extending loan to

employee to complete the personal level work. The statutory interest rate for year 2017/18 is

5.25% pa which has been declared by Reserve Bank of Australia as per TD 2017/3 (Barkoczy,

2017). Further, the usage of loan by employee for personal work is imperative to analyse since if

the loan amount has been used for assessable income generation then deduction will be available

8

treat the tax implication on employee and employer for fringe benefit which is known as “Fringe

Benefits Tax Assessment Act 1986 (FBTAA 1986).” This tax is applicable on employer not on

the employee (Reuters, 2017).

“Car Fringe Benefit”

The critical condition that must be satisfied for providing car fringe benefit is that the employer

must issue car to employee so that the employee can use the car as per his/her choice for personal

work. According to s.7, FBTAA 1986, the car fringe benefits will not be given to employee by

their employer when the usage of offered car is restricted to office purpose only (Nethercott,

Richardson & Devos, 2016). The extension of car and authority to use the car for personal

interest work may be provided either in oral form or in written form. Furthermore, the way of

action of the employer may also provide sufficient clue that employer has issued car to employee

for personal work. In this regards, the practice of car parking at employee’s own garage or at

house implies that the employee directly get the permission to use the car due to presence of

implicit permission of the employee (Hodgson,Mortimer & Butler, 2016). Capital value of car is

a function of purchasing price which has been paid on behalf of the employer and the respective

amount called deductions which are also paid by the employer in order to pay the minor repair

expenses. According to s.9, FBTAA 1986 the deduction on days would not be imposed from

total period of personal utilization when the car is not present for her and sent for minor repairing

(Gilders, et. al., 2015). Further, the inclusion of the utilization would be followed means the

actual use of car is not essential for computing the total period of car utilization for personal

work (Krever, 2017).

“Loan Fringe Benefit”

According to s. 16, FBTAA loan fringe benefit is issued when the employer has taken

concessional rate of interest as compared with the statutory interest rate while extending loan to

employee to complete the personal level work. The statutory interest rate for year 2017/18 is

5.25% pa which has been declared by Reserve Bank of Australia as per TD 2017/3 (Barkoczy,

2017). Further, the usage of loan by employee for personal work is imperative to analyse since if

the loan amount has been used for assessable income generation then deduction will be available

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for employer as highlighted in s. 19, FBTAA 1986 (Wilmot, 2014) . Further, when the employee

provides the loan amount to other family member then deduction will not be present for claim on

the part of the employer irrespective of the utilization of that loan amount by family member or

associates of the employee (Nethercott, Richardson & Devos, 2016).

“Expenses Fringe Benefits”

Employer pays expenses of employee which are clearly personal in nature hence would be

considered as expense fringe benefit (Sadiq, et.al., 2015). The expense payment by providing the

concession in the product of the company then it is sub category of internal expense fringe

benefit. This benefit reduces the personal nature liability of the employee via issuing this benefit

(Deutsch, et.al., 2015).

Application

(a) FBT consequences

“Car Fringe Benefit”

Rapid Heat (employer) has allowed Jasmine (employee) to use company’s car for her personal

work. The car cost is $33,000 and has issued to her on May 1, 2017. Jasmine has commenced

utilizing the car for her own private work on May 1, 2017. The Fringe Benefit Tax (FBT)

liability has been imposed on Rapid Heat as it has issued car fringe benefit to Jasmine. The net

FBT payable is computed as highlighted below based on the requisite variables.

Car has subjected to minor repairing while utilizing by Jasmine and Rapid Heat has paid the

minor repair expense. The base/capital value of car is computed below.

Period of personal utilization

The taxpayer employer provide car to her for the complete financial years except April month

and therefore, the total period of personal utilization of car would be 365 days – 30 days (April)

= 335 days.

9

provides the loan amount to other family member then deduction will not be present for claim on

the part of the employer irrespective of the utilization of that loan amount by family member or

associates of the employee (Nethercott, Richardson & Devos, 2016).

“Expenses Fringe Benefits”

Employer pays expenses of employee which are clearly personal in nature hence would be

considered as expense fringe benefit (Sadiq, et.al., 2015). The expense payment by providing the

concession in the product of the company then it is sub category of internal expense fringe

benefit. This benefit reduces the personal nature liability of the employee via issuing this benefit

(Deutsch, et.al., 2015).

Application

(a) FBT consequences

“Car Fringe Benefit”

Rapid Heat (employer) has allowed Jasmine (employee) to use company’s car for her personal

work. The car cost is $33,000 and has issued to her on May 1, 2017. Jasmine has commenced

utilizing the car for her own private work on May 1, 2017. The Fringe Benefit Tax (FBT)

liability has been imposed on Rapid Heat as it has issued car fringe benefit to Jasmine. The net

FBT payable is computed as highlighted below based on the requisite variables.

Car has subjected to minor repairing while utilizing by Jasmine and Rapid Heat has paid the

minor repair expense. The base/capital value of car is computed below.

Period of personal utilization

The taxpayer employer provide car to her for the complete financial years except April month

and therefore, the total period of personal utilization of car would be 365 days – 30 days (April)

= 335 days.

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

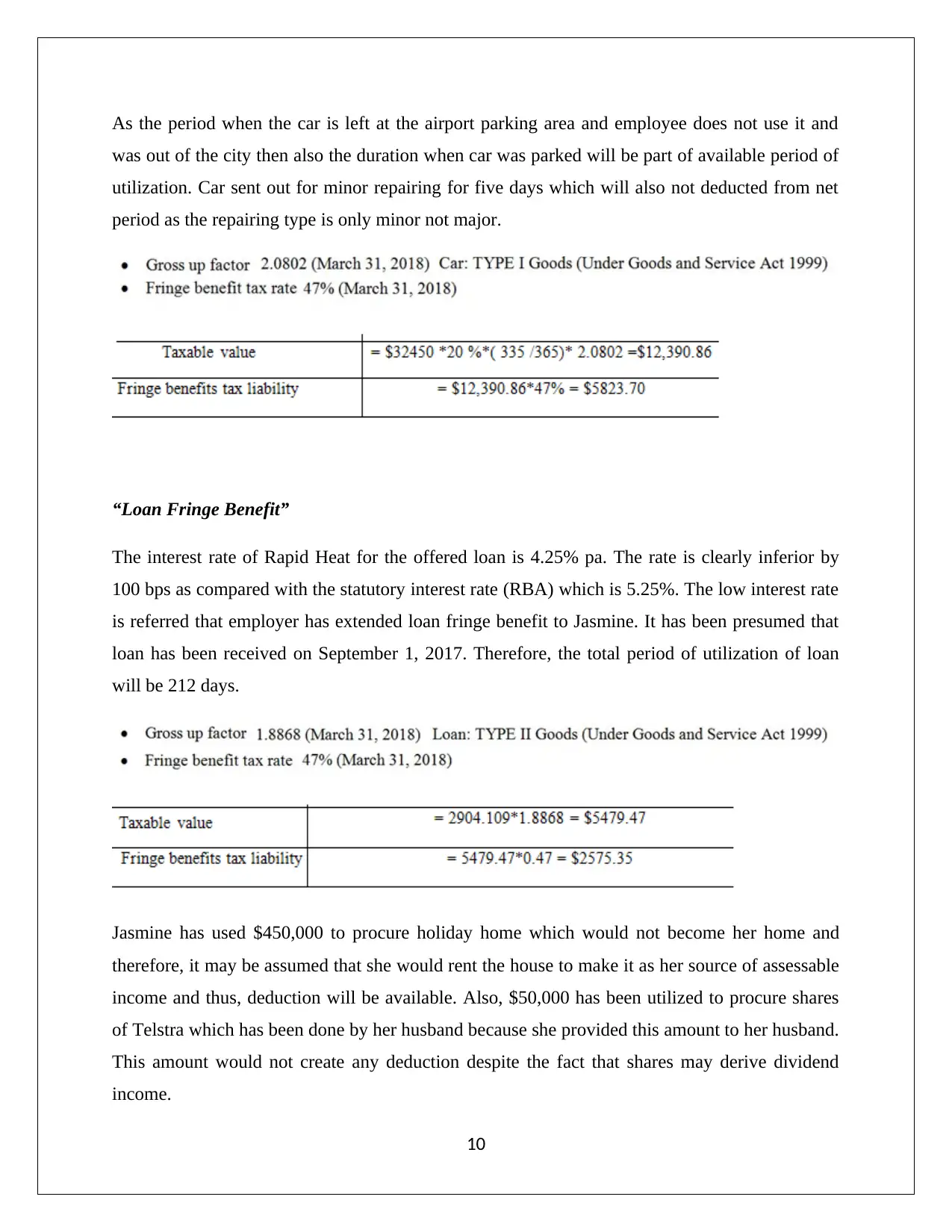

As the period when the car is left at the airport parking area and employee does not use it and

was out of the city then also the duration when car was parked will be part of available period of

utilization. Car sent out for minor repairing for five days which will also not deducted from net

period as the repairing type is only minor not major.

“Loan Fringe Benefit”

The interest rate of Rapid Heat for the offered loan is 4.25% pa. The rate is clearly inferior by

100 bps as compared with the statutory interest rate (RBA) which is 5.25%. The low interest rate

is referred that employer has extended loan fringe benefit to Jasmine. It has been presumed that

loan has been received on September 1, 2017. Therefore, the total period of utilization of loan

will be 212 days.

Jasmine has used $450,000 to procure holiday home which would not become her home and

therefore, it may be assumed that she would rent the house to make it as her source of assessable

income and thus, deduction will be available. Also, $50,000 has been utilized to procure shares

of Telstra which has been done by her husband because she provided this amount to her husband.

This amount would not create any deduction despite the fact that shares may derive dividend

income.

10

was out of the city then also the duration when car was parked will be part of available period of

utilization. Car sent out for minor repairing for five days which will also not deducted from net

period as the repairing type is only minor not major.

“Loan Fringe Benefit”

The interest rate of Rapid Heat for the offered loan is 4.25% pa. The rate is clearly inferior by

100 bps as compared with the statutory interest rate (RBA) which is 5.25%. The low interest rate

is referred that employer has extended loan fringe benefit to Jasmine. It has been presumed that

loan has been received on September 1, 2017. Therefore, the total period of utilization of loan

will be 212 days.

Jasmine has used $450,000 to procure holiday home which would not become her home and

therefore, it may be assumed that she would rent the house to make it as her source of assessable

income and thus, deduction will be available. Also, $50,000 has been utilized to procure shares

of Telstra which has been done by her husband because she provided this amount to her husband.

This amount would not create any deduction despite the fact that shares may derive dividend

income.

10

“Expenses Fringe Benefits”

Rapid Heat which provides heater to customer for a net price of $2600 has provided 50%

discount and provided it to Jasmine for $1300. The reason behind 50% discount is to reduce the

personal nature expenses liability of her and hence, it will be termed as expense fringe benefit.

Further, this internal expense fringe benefit would minimize the personal expenses of employee

and raise FBT implication on employer.

(b) The nature of utilization of the loan amount has been changed which means the share which

are previously used by Jasmine’s husband is now being used by Jasmine. In this case, the

deduction is applicable because the dividend income that would be generated from the shares

will become part of the assessable income of employee Jasmine. Thereby, the respective

deduction will be imposed which also lower down the net FBT liability which has been

raised from loan fringe benefit.

Conclusion

The FBT implications are imposed for all the three fringe benefits which are car, loan and

expense. The FBT payable for each of the given cases is listed below.

FBT liability for car fringe benefit =$5823.70

FBT liability for loan fringe benefit = $2575.35

FBT liability for expenses fringe benefit =$635.5

11

Rapid Heat which provides heater to customer for a net price of $2600 has provided 50%

discount and provided it to Jasmine for $1300. The reason behind 50% discount is to reduce the

personal nature expenses liability of her and hence, it will be termed as expense fringe benefit.

Further, this internal expense fringe benefit would minimize the personal expenses of employee

and raise FBT implication on employer.

(b) The nature of utilization of the loan amount has been changed which means the share which

are previously used by Jasmine’s husband is now being used by Jasmine. In this case, the

deduction is applicable because the dividend income that would be generated from the shares

will become part of the assessable income of employee Jasmine. Thereby, the respective

deduction will be imposed which also lower down the net FBT liability which has been

raised from loan fringe benefit.

Conclusion

The FBT implications are imposed for all the three fringe benefits which are car, loan and

expense. The FBT payable for each of the given cases is listed below.

FBT liability for car fringe benefit =$5823.70

FBT liability for loan fringe benefit = $2575.35

FBT liability for expenses fringe benefit =$635.5

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.