Holmes Institute HI6028 Taxation Law Assignment T3 2019

VerifiedAdded on 2022/08/20

|12

|2873

|27

Homework Assignment

AI Summary

This assignment addresses various aspects of Australian taxation law, covering ordinary income, fringe benefits, and capital gains tax (CGT). The first part examines the tax implications of income earned from personal services, including tips and employment income, and the treatment of gifts. It references key cases and legislation such as ITAA 1997 and FBTAA 1986. The second part delves into CGT, differentiating between pre-CGT and post-CGT assets and explaining the tax treatment of personal use assets. It also covers small business CGT concessions, including asset ownership exemptions and retirement exemptions, as well as the rules for collectables. The assignment provides practical application through case studies, analyzing scenarios involving employment income, gifts, and asset disposals, and determining the relevant tax implications for each. The document is a solution to the assignment brief provided, aiming to demonstrate understanding of the Australian tax system and its application to real-world scenarios.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Will the income have earned from personal services and employment is included for

assessment under the “sec 6-5 ITAA 1997” as taxable ordinary receipts.

Rule:

For an amount to be held as ordinary earnings the receipts should satisfy the two

prerequisites. The sum is ought to be convertible in cash and it is required to be a real gain for

the taxpayer (Basu 2016). There are namely two step approach that is used in ascertaining

whether the amount will be held as ordinary income from personal exertion.

a. Recognizing whether the activity is undertaken by the taxpayer; and

b. Determining whether the receipts amounts to the reward of doing that specific

activity.

Tips are usually viewed as the gift given by third party and it is included in taxable

income of taxpayer for tax purpose since it is a voluntary payment. In “Penn v Spiers &

Pond Ltd (1908)” tips are usually made due to the extent of service rendered establishes a

link among the service given which makes it as the ordinary earnings under “sec 6-5” (Miller

and Oats 2016).

Receipts which a taxpayer earns from the personal service and employment takes into

account the income from both employment as well as service which may be considered

taxable as the ordinary earnings and statutory earnings (Dietsch and Rixen 2014). In

“Moorhouse v Dooland (1955)” income derived from the direct or indirect sources based on

the quality of taxpayer’s personal exertion it will be regarded as ordinary earnings under “sec

6-5”.

Answer to question 1:

Issues:

Will the income have earned from personal services and employment is included for

assessment under the “sec 6-5 ITAA 1997” as taxable ordinary receipts.

Rule:

For an amount to be held as ordinary earnings the receipts should satisfy the two

prerequisites. The sum is ought to be convertible in cash and it is required to be a real gain for

the taxpayer (Basu 2016). There are namely two step approach that is used in ascertaining

whether the amount will be held as ordinary income from personal exertion.

a. Recognizing whether the activity is undertaken by the taxpayer; and

b. Determining whether the receipts amounts to the reward of doing that specific

activity.

Tips are usually viewed as the gift given by third party and it is included in taxable

income of taxpayer for tax purpose since it is a voluntary payment. In “Penn v Spiers &

Pond Ltd (1908)” tips are usually made due to the extent of service rendered establishes a

link among the service given which makes it as the ordinary earnings under “sec 6-5” (Miller

and Oats 2016).

Receipts which a taxpayer earns from the personal service and employment takes into

account the income from both employment as well as service which may be considered

taxable as the ordinary earnings and statutory earnings (Dietsch and Rixen 2014). In

“Moorhouse v Dooland (1955)” income derived from the direct or indirect sources based on

the quality of taxpayer’s personal exertion it will be regarded as ordinary earnings under “sec

6-5”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

A receipt would not be treated as ordinary income given the receipts does not form

the part of taxpayer’s employment or product of service. When a taxpayer is given a gift that

is related to personal qualities it is not viewed as ordinary income and will not be viewed

chargeable under sec 6-5 for the receiver. At the time of differentiating amongst the non-

taxable personal gift and the chargeable voluntary payments for service, the federal court

have placed greater emphasis on the nature of receipts in the hand of recipient instead of the

emphasizing on the motive of the giver. In “FC of T v Scott (1966)” where a taxpayer

receives solicited gift it cannot be treated as ordinary income for the reason that it was

prompted by gratitude for certain service, since there is a need for other factors as well

(Kaldor 2014). This involves whether the gifts were anticipated since anticipated gifts is very

much an ordinary earnings under “sec 6-5 ITAA 1997”.

As a common rule, the FBT is levied on employer and not on the employee under

“sec 66 (1) FBTAA 1986”. The main reason is taxes are imposed based on the provision of

fringe benefit and not on those that are receiver of service. Accordingly, within “sec 136 (1)

FBTAA” fringe benefit is existent when a benefit is given to an employee all through the

taxation year by the employer or an associate that relates to the employment of the employee

(Mumford 2017). In “sec 136 (1) FBTAA” the benefit normally includes right, privilege,

service or facility given within the arrangement in relation to the work done. In

“Indooroopily Children’s Service v FC of T (2007)” a fringe benefit will only happen when

the benefit is related to employee. There should always be a sufficient material relation

among the employment and benefit given.

Commonly, money that is given to the taxpayer from the family member relating to

the personal reasons and gift does not relates to any income generating acts, is not viewed as

income. Such kind of gift is not usually included in the tax return of the taxpayer.

A receipt would not be treated as ordinary income given the receipts does not form

the part of taxpayer’s employment or product of service. When a taxpayer is given a gift that

is related to personal qualities it is not viewed as ordinary income and will not be viewed

chargeable under sec 6-5 for the receiver. At the time of differentiating amongst the non-

taxable personal gift and the chargeable voluntary payments for service, the federal court

have placed greater emphasis on the nature of receipts in the hand of recipient instead of the

emphasizing on the motive of the giver. In “FC of T v Scott (1966)” where a taxpayer

receives solicited gift it cannot be treated as ordinary income for the reason that it was

prompted by gratitude for certain service, since there is a need for other factors as well

(Kaldor 2014). This involves whether the gifts were anticipated since anticipated gifts is very

much an ordinary earnings under “sec 6-5 ITAA 1997”.

As a common rule, the FBT is levied on employer and not on the employee under

“sec 66 (1) FBTAA 1986”. The main reason is taxes are imposed based on the provision of

fringe benefit and not on those that are receiver of service. Accordingly, within “sec 136 (1)

FBTAA” fringe benefit is existent when a benefit is given to an employee all through the

taxation year by the employer or an associate that relates to the employment of the employee

(Mumford 2017). In “sec 136 (1) FBTAA” the benefit normally includes right, privilege,

service or facility given within the arrangement in relation to the work done. In

“Indooroopily Children’s Service v FC of T (2007)” a fringe benefit will only happen when

the benefit is related to employee. There should always be a sufficient material relation

among the employment and benefit given.

Commonly, money that is given to the taxpayer from the family member relating to

the personal reasons and gift does not relates to any income generating acts, is not viewed as

income. Such kind of gift is not usually included in the tax return of the taxpayer.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Application:

The case study opens up with the scenario that Emmi working on part-time purpose in

Crown Melbourne restaurant receives cash tips from customers that amounted to $335. Tips

received by Emmi is viewed as gift given by third party and it should be included in her

taxable income for tax purpose since it is a voluntary payment (Akhmadeev et al. 2016).

Quoting “Penn v Spiers & Pond Ltd (1908)” the tips of $335 establishes a link among the

service rendered by Emmi which makes it as the ordinary earnings under “sec 6-5”.

Furthermore, income amounting to $25,000 was received by Emmi from her work in

Crown Melbourne restaurants. The receipt of $25,000 earned by Emmi is related to her

personal service and employment. Referring to “Moorhouse v Dooland (1955)” the sum will

be considered as income derived from the direct sources based on the quality of Emmi’s

personal exertion. Therefore, it will be regarded as ordinary earnings under “sec 6-5”.

There was an instance in the case study where Emmi received a perfume that worth

$250 from a regular customer during Christmas. The receipt of gift cannot be treated as

ordinary income since the receipt of perfume does not form the part of Emmi’s employment

or product of service. The perfume given as a gift to Emmi is related to personal qualities and

it should not be viewed as ordinary income. Referring to “FC of T v Scott (1966)” the

perfume is a solicited gift and will not be viewed chargeable under “sec 6-5” for Emmi.

The case study of Emmi provides that she was given by her employer a monthly

entertainment expenses. A sum of $380 was also spent by Emmi’s employer for her the

consumed. Within “sec 136 (1) FBTAA” the entertainment expenses and food consumed by

Emmi is a fringe benefit that relates to her employment (Tuomala 2016). Mentioning the

Application:

The case study opens up with the scenario that Emmi working on part-time purpose in

Crown Melbourne restaurant receives cash tips from customers that amounted to $335. Tips

received by Emmi is viewed as gift given by third party and it should be included in her

taxable income for tax purpose since it is a voluntary payment (Akhmadeev et al. 2016).

Quoting “Penn v Spiers & Pond Ltd (1908)” the tips of $335 establishes a link among the

service rendered by Emmi which makes it as the ordinary earnings under “sec 6-5”.

Furthermore, income amounting to $25,000 was received by Emmi from her work in

Crown Melbourne restaurants. The receipt of $25,000 earned by Emmi is related to her

personal service and employment. Referring to “Moorhouse v Dooland (1955)” the sum will

be considered as income derived from the direct sources based on the quality of Emmi’s

personal exertion. Therefore, it will be regarded as ordinary earnings under “sec 6-5”.

There was an instance in the case study where Emmi received a perfume that worth

$250 from a regular customer during Christmas. The receipt of gift cannot be treated as

ordinary income since the receipt of perfume does not form the part of Emmi’s employment

or product of service. The perfume given as a gift to Emmi is related to personal qualities and

it should not be viewed as ordinary income. Referring to “FC of T v Scott (1966)” the

perfume is a solicited gift and will not be viewed chargeable under “sec 6-5” for Emmi.

The case study of Emmi provides that she was given by her employer a monthly

entertainment expenses. A sum of $380 was also spent by Emmi’s employer for her the

consumed. Within “sec 136 (1) FBTAA” the entertainment expenses and food consumed by

Emmi is a fringe benefit that relates to her employment (Tuomala 2016). Mentioning the

5TAXATION LAW

verdict in “Indooroopily Children’s Service v FC of T (2007)” the food and entertainment

benefit is in respect of the employment of Emmi. The benefits hold a sufficient material

relation among the employment and benefit given. Within the “sec 66 (1) FBTAA 1986” the

employer of Emmi will be considered taxable for the value of fringe benefit given to her

during the taxable FBT year.

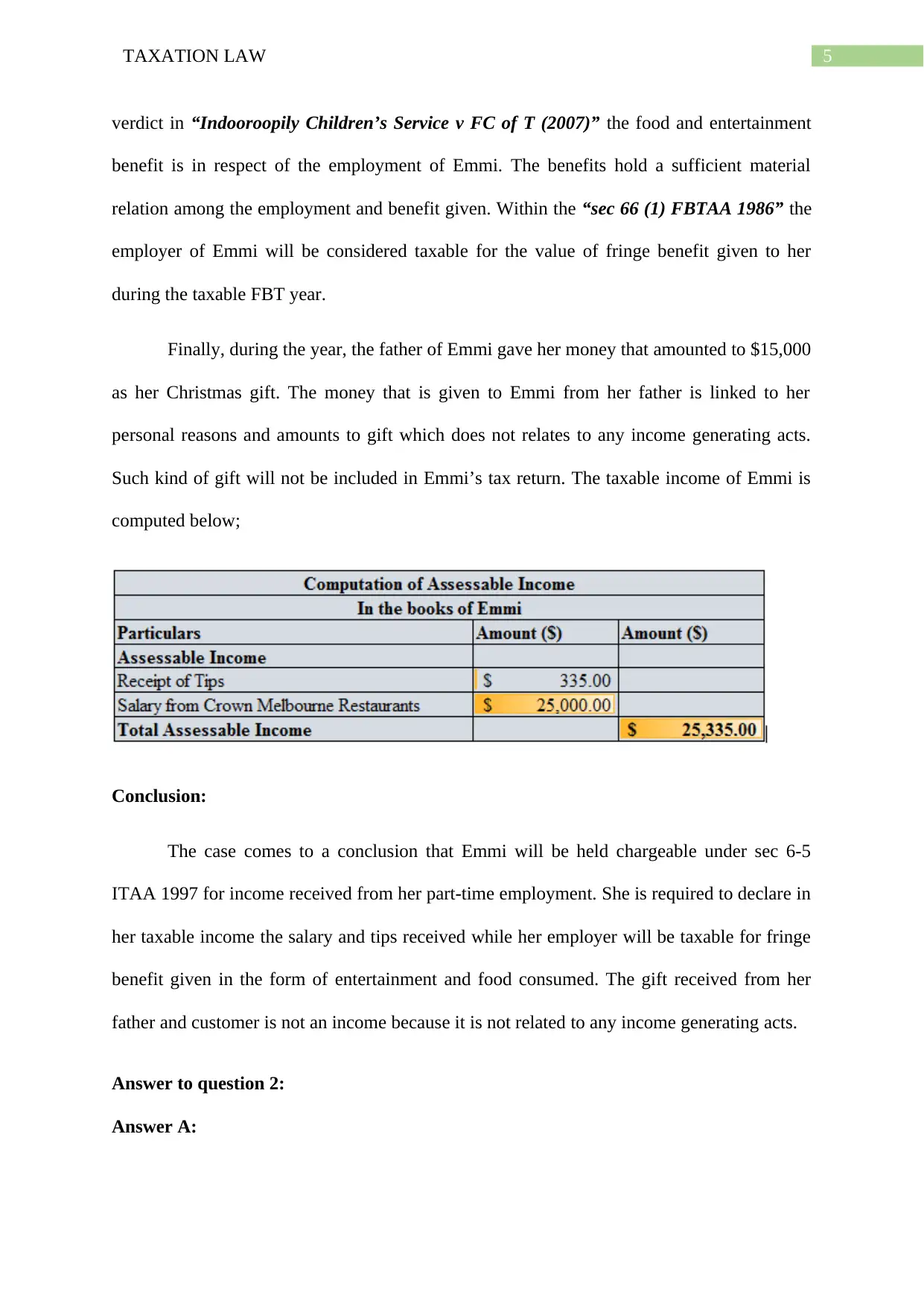

Finally, during the year, the father of Emmi gave her money that amounted to $15,000

as her Christmas gift. The money that is given to Emmi from her father is linked to her

personal reasons and amounts to gift which does not relates to any income generating acts.

Such kind of gift will not be included in Emmi’s tax return. The taxable income of Emmi is

computed below;

Conclusion:

The case comes to a conclusion that Emmi will be held chargeable under sec 6-5

ITAA 1997 for income received from her part-time employment. She is required to declare in

her taxable income the salary and tips received while her employer will be taxable for fringe

benefit given in the form of entertainment and food consumed. The gift received from her

father and customer is not an income because it is not related to any income generating acts.

Answer to question 2:

Answer A:

verdict in “Indooroopily Children’s Service v FC of T (2007)” the food and entertainment

benefit is in respect of the employment of Emmi. The benefits hold a sufficient material

relation among the employment and benefit given. Within the “sec 66 (1) FBTAA 1986” the

employer of Emmi will be considered taxable for the value of fringe benefit given to her

during the taxable FBT year.

Finally, during the year, the father of Emmi gave her money that amounted to $15,000

as her Christmas gift. The money that is given to Emmi from her father is linked to her

personal reasons and amounts to gift which does not relates to any income generating acts.

Such kind of gift will not be included in Emmi’s tax return. The taxable income of Emmi is

computed below;

Conclusion:

The case comes to a conclusion that Emmi will be held chargeable under sec 6-5

ITAA 1997 for income received from her part-time employment. She is required to declare in

her taxable income the salary and tips received while her employer will be taxable for fringe

benefit given in the form of entertainment and food consumed. The gift received from her

father and customer is not an income because it is not related to any income generating acts.

Answer to question 2:

Answer A:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

As a common rule CGT is normally applicable on the assets which is purchased or

other events that happens following the date of 20 September 1985. So, the expressions “pre-

CGT” and “post-CGT” is very frequently put into use by the taxpayers to refer the assets

which is purchased or events that happens prior to following that date (Twite 2015). The

CGT system is simply based on the realised capital gains or loss that happens following the

disposal of asset or from other specific events.

The case study of Liu explains that during 1981 she has purchased a house that cost

her $55,000. Throughout that period, she used the house as her main residence. While in the

present tax year she has undertaken the decision of selling her main residence. It must be

noted that the house is a “pre-CGT asset” because it was purchased by Liu before the 20

September 1985. Hence, the capital gains made from selling the property will be excluded

from CGT.

Answer B:

The first step in ascertaining whether the transaction or events is regarded as the

subject of CGT is to understand whether the CGT event has taken place. A “CGT event A1”

happens with in “sec 104-10 (1)” when the asset is disposed. According to “subdivision 108-

C” a personal use asset is normally regarded as non-collectable asset that is kept under the

possession of taxpayer for their private enjoyment (Fane and Richardson 2015). The

examples of this assets are boats, motor vehicles, furniture, electrical goods and household

items. In the event if a taxpayer sells a personal use asset and incurs a capital loss, the loss is

not entitled to offset against the capital gains. Rather under “sec 108-20 (1)” the loss should

be ignored.

Likewise, Liu sold a car during the year for $8,000. The car had the purchase value of

$37,000 when Liu bought it in 2011. It can be said that the car is a personal use asset under

As a common rule CGT is normally applicable on the assets which is purchased or

other events that happens following the date of 20 September 1985. So, the expressions “pre-

CGT” and “post-CGT” is very frequently put into use by the taxpayers to refer the assets

which is purchased or events that happens prior to following that date (Twite 2015). The

CGT system is simply based on the realised capital gains or loss that happens following the

disposal of asset or from other specific events.

The case study of Liu explains that during 1981 she has purchased a house that cost

her $55,000. Throughout that period, she used the house as her main residence. While in the

present tax year she has undertaken the decision of selling her main residence. It must be

noted that the house is a “pre-CGT asset” because it was purchased by Liu before the 20

September 1985. Hence, the capital gains made from selling the property will be excluded

from CGT.

Answer B:

The first step in ascertaining whether the transaction or events is regarded as the

subject of CGT is to understand whether the CGT event has taken place. A “CGT event A1”

happens with in “sec 104-10 (1)” when the asset is disposed. According to “subdivision 108-

C” a personal use asset is normally regarded as non-collectable asset that is kept under the

possession of taxpayer for their private enjoyment (Fane and Richardson 2015). The

examples of this assets are boats, motor vehicles, furniture, electrical goods and household

items. In the event if a taxpayer sells a personal use asset and incurs a capital loss, the loss is

not entitled to offset against the capital gains. Rather under “sec 108-20 (1)” the loss should

be ignored.

Likewise, Liu sold a car during the year for $8,000. The car had the purchase value of

$37,000 when Liu bought it in 2011. It can be said that the car is a personal use asset under

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

the “subdivision 108-C”. The disposal of car resulted in “CGT event A1” within “sec 104-

10”. In the event of selling the car, Liu has suffered a capital loss. Under the “sec 108-20

(1)”, the capital loss suffered from disposing the car needs to be ignored by Liu as it is not

allowed for offset.

Answer to C:

Under the “Division 152”, small business is given with the concession from CGT

events that takes place on or following the 21/9/1999 (Burman 2016). Under the “sec 152-35

& sec 152-40” when a CGT asset which meets the “active asset test”, they are provided with

four concessions. In order to access the concession, there are eligibility criteria which needs

to be met to avail concession are;

a. A business should be a small business entity within “sec 152-10”;

b. Any business taxpayer that has the net value of CGT asset and its associated entities is

not greater than $6 million under “sec 152-10 & sec 152-15”.

After meeting the eligibility criteria given above, there are four small business

concessions which are as follows;

a. Under “Subdivision 152-B”, a taxpayer is given 15-year asset ownership exemption

from capital gains. The minimum age to qualify for this exemption is 55 years or

more.

b. Under “Subdivision 152-C”, a taxpayer is provided with 50% capital gain reduction.

c. Under “Subdivision 152-D”, the taxpayer of small business entity is given a

retirement exemption from capital gains (Evans, Minas and Lim 2015).

the “subdivision 108-C”. The disposal of car resulted in “CGT event A1” within “sec 104-

10”. In the event of selling the car, Liu has suffered a capital loss. Under the “sec 108-20

(1)”, the capital loss suffered from disposing the car needs to be ignored by Liu as it is not

allowed for offset.

Answer to C:

Under the “Division 152”, small business is given with the concession from CGT

events that takes place on or following the 21/9/1999 (Burman 2016). Under the “sec 152-35

& sec 152-40” when a CGT asset which meets the “active asset test”, they are provided with

four concessions. In order to access the concession, there are eligibility criteria which needs

to be met to avail concession are;

a. A business should be a small business entity within “sec 152-10”;

b. Any business taxpayer that has the net value of CGT asset and its associated entities is

not greater than $6 million under “sec 152-10 & sec 152-15”.

After meeting the eligibility criteria given above, there are four small business

concessions which are as follows;

a. Under “Subdivision 152-B”, a taxpayer is given 15-year asset ownership exemption

from capital gains. The minimum age to qualify for this exemption is 55 years or

more.

b. Under “Subdivision 152-C”, a taxpayer is provided with 50% capital gain reduction.

c. Under “Subdivision 152-D”, the taxpayer of small business entity is given a

retirement exemption from capital gains (Evans, Minas and Lim 2015).

8TAXATION LAW

d. Under “Subdivision 152-E”, the taxpayer is given with rollover relief after

purchasing replacement asset.

The case study provides that Liu had the small business which she disposed in the present

tax year for $125,000. The assets included the photography equipment of $53,000 and the

goodwill was sold for $50,000. As evident the business of Liu will be viewed as small

business because under “sec 152-10” the net value of the CGT assets that was owned by the

taxpayer is not greater than $6 million (Lally and Van Zijl 2014). Liu can obtain a retirement

exemption under “subdivision 152-D” because she is retiring from the business and the net

proceeds from the assets is not more than $500,000.

Answer to D:

As per the special rules given in “sec 118-10 (3)” relating to personal use asset states

that any amount of capital gains is required to be ignored where the value of asset is not

greater than $10,000 or less (Freebairn 2018). Evidently, Liu reports the sale of furniture for

$4,800. The cost base of the furniture is $2,000. Furniture is classified as personal use asset

under “sec 108-20 (2)”. As a result, the capital gains made from selling the furniture will be

ignored under “sec 118-10 (3)” since it fails to meet first element cost base of less than

$10,000.

Answer to E:

A collectable under “sec 118-10 (2)” refers to assets such as artwork, rare folio,

stamp, manuscript, painting, jewellery etc. that is kept by taxpayer for private usage.

Collectables which the taxpayer purchases for less than $500 is exempted from CGT

provision under “sec 118-10 (1)” (Woellner et al. 2015). Liu has acquired numerous

paintings for $500 that she sold for $28,000. The paintings are classified as collectables under

“sec 118-10 (2)”. The capital gains derived from selling the painting will be ignored under

d. Under “Subdivision 152-E”, the taxpayer is given with rollover relief after

purchasing replacement asset.

The case study provides that Liu had the small business which she disposed in the present

tax year for $125,000. The assets included the photography equipment of $53,000 and the

goodwill was sold for $50,000. As evident the business of Liu will be viewed as small

business because under “sec 152-10” the net value of the CGT assets that was owned by the

taxpayer is not greater than $6 million (Lally and Van Zijl 2014). Liu can obtain a retirement

exemption under “subdivision 152-D” because she is retiring from the business and the net

proceeds from the assets is not more than $500,000.

Answer to D:

As per the special rules given in “sec 118-10 (3)” relating to personal use asset states

that any amount of capital gains is required to be ignored where the value of asset is not

greater than $10,000 or less (Freebairn 2018). Evidently, Liu reports the sale of furniture for

$4,800. The cost base of the furniture is $2,000. Furniture is classified as personal use asset

under “sec 108-20 (2)”. As a result, the capital gains made from selling the furniture will be

ignored under “sec 118-10 (3)” since it fails to meet first element cost base of less than

$10,000.

Answer to E:

A collectable under “sec 118-10 (2)” refers to assets such as artwork, rare folio,

stamp, manuscript, painting, jewellery etc. that is kept by taxpayer for private usage.

Collectables which the taxpayer purchases for less than $500 is exempted from CGT

provision under “sec 118-10 (1)” (Woellner et al. 2015). Liu has acquired numerous

paintings for $500 that she sold for $28,000. The paintings are classified as collectables under

“sec 118-10 (2)”. The capital gains derived from selling the painting will be ignored under

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

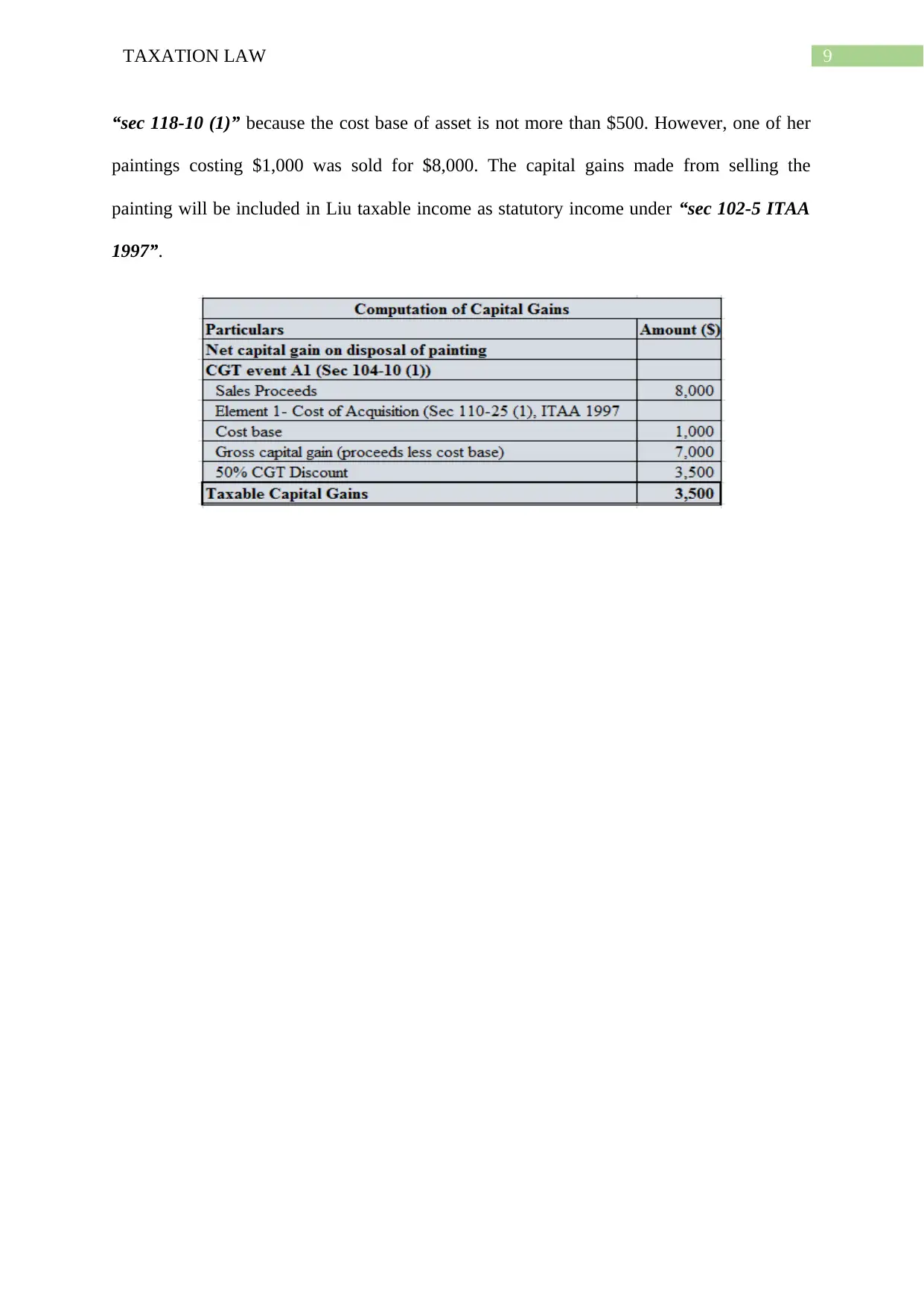

“sec 118-10 (1)” because the cost base of asset is not more than $500. However, one of her

paintings costing $1,000 was sold for $8,000. The capital gains made from selling the

painting will be included in Liu taxable income as statutory income under “sec 102-5 ITAA

1997”.

“sec 118-10 (1)” because the cost base of asset is not more than $500. However, one of her

paintings costing $1,000 was sold for $8,000. The capital gains made from selling the

painting will be included in Liu taxable income as statutory income under “sec 102-5 ITAA

1997”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Akhmadeev, R.G., Kosov, M.E., Bykanova, O.A., Ekimova, K.V., Frumina, S.V. and

Philippova, N.V., 2016. Impact of tax burden on the country‟ s

investments. Education, 54(3.5), pp.1-6.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Black, D., 2018. The incidence of income taxes. Routledge.

Burman, L., 2016. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal of

political philosophy, 22(2), pp.150-177.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Fane, G. and Richardson, M., 2015. Negative gearing and the taxation of capital gains in

Australia. Economic Record, 81(254), pp.249-261.

Freebairn, J.O.H.N., 2018. Indexation and Australian capital gains taxation. International

evidence on the effects of having no Capital Gains Taxes, pp.123-140.

Kaldor, N., 2014. Expenditure tax. Routledge.

Lally, M. and Van Zijl, T., 2014. Capital gains tax and the capital asset pricing

model. Accounting & Finance, 43(2), pp.187-210.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

References:

Akhmadeev, R.G., Kosov, M.E., Bykanova, O.A., Ekimova, K.V., Frumina, S.V. and

Philippova, N.V., 2016. Impact of tax burden on the country‟ s

investments. Education, 54(3.5), pp.1-6.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Black, D., 2018. The incidence of income taxes. Routledge.

Burman, L., 2016. Taxing Capital Gains in Australia: Assessment and

Recommendations'. Australian Business Tax Reform in Retrospect and Prospect.

Dietsch, P. and Rixen, T., 2014. Tax competition and global background justice. Journal of

political philosophy, 22(2), pp.150-177.

Evans, C., Minas, J. and Lim, Y., 2015. Taxing personal capital gains in Australia: An

alternative way forward. Austl. Tax F., 30, p.735.

Fane, G. and Richardson, M., 2015. Negative gearing and the taxation of capital gains in

Australia. Economic Record, 81(254), pp.249-261.

Freebairn, J.O.H.N., 2018. Indexation and Australian capital gains taxation. International

evidence on the effects of having no Capital Gains Taxes, pp.123-140.

Kaldor, N., 2014. Expenditure tax. Routledge.

Lally, M. and Van Zijl, T., 2014. Capital gains tax and the capital asset pricing

model. Accounting & Finance, 43(2), pp.187-210.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge.

11TAXATION LAW

Reynolds, A., 2017. Capital gains tax: Analysis of reform options for Australia. Australian

Stock Exchange.

Tuomala, M., 2016. Optimal redistributive taxation. Oxford University Press.

Twite, G., 2015. Capital structure choices and taxes: Evidence from the Australian dividend

imputation tax system. International Review of Finance, 2(4), pp.217-234.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2015. Australian taxation

law. CCH Australia.

Reynolds, A., 2017. Capital gains tax: Analysis of reform options for Australia. Australian

Stock Exchange.

Tuomala, M., 2016. Optimal redistributive taxation. Oxford University Press.

Twite, G., 2015. Capital structure choices and taxes: Evidence from the Australian dividend

imputation tax system. International Review of Finance, 2(4), pp.217-234.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2015. Australian taxation

law. CCH Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.