Taxation Law | Questions and Answers

VerifiedAdded on 2022/08/30

|12

|2757

|15

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................8

Answer to E:...........................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer A:..............................................................................................................................6

Answer B:...............................................................................................................................6

Answer C:...............................................................................................................................7

Answer D:..............................................................................................................................8

Answer to E:...........................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Is the taxpayer in the current situation will be considered taxable for the numerous

receipt that is made during the year from the part-time employment?

Rule:

The ordinary income is regarded as the notable part of assessable earnings. An

individual taxpayer’s assessable income contain income that are in agreement with the

ordinary concepts. Under “sec 6-5 ITAA 1997” this is known as ordinary income. Where a

taxpayer gets unanticipated or voluntary payments which is recovered as the part of reward of

service amounts to income under ordinary concepts because the benefits represents the

incidence of employment (Sharkey 2016). As noted in “Calvert v Wainwright (1947)” tips

that are given to a third party as gift and signifies a voluntary payment because they are made

to an individual for their services rendered establishes a nexus among the services provided.

Tips are usually regarded as an ordinary income.

As there is no particular definition of the word “income” under the legislation, the

provision of “sec 6 (1) ITAA 1936” defines income from personal exertion as something that

is received in the form of salary, wages, bonus, commission, etc. by an individual taxpayer

for rendering any personal services (Pert et al. 2017). The law court in “Brown v FCT

(2002)” explains that receipts which is associated to carrying out of service is treated as

product or incidence of employment or reward for activity. Such receipts amounts to taxable

ordinary income.

Personal gifts are normally treated as taxable earnings under “sec 6-5 ITAA 1997”.

Where the personal gifts, opposite to other type of voluntary payments that are related to

Answer to question 1:

Issues:

Is the taxpayer in the current situation will be considered taxable for the numerous

receipt that is made during the year from the part-time employment?

Rule:

The ordinary income is regarded as the notable part of assessable earnings. An

individual taxpayer’s assessable income contain income that are in agreement with the

ordinary concepts. Under “sec 6-5 ITAA 1997” this is known as ordinary income. Where a

taxpayer gets unanticipated or voluntary payments which is recovered as the part of reward of

service amounts to income under ordinary concepts because the benefits represents the

incidence of employment (Sharkey 2016). As noted in “Calvert v Wainwright (1947)” tips

that are given to a third party as gift and signifies a voluntary payment because they are made

to an individual for their services rendered establishes a nexus among the services provided.

Tips are usually regarded as an ordinary income.

As there is no particular definition of the word “income” under the legislation, the

provision of “sec 6 (1) ITAA 1936” defines income from personal exertion as something that

is received in the form of salary, wages, bonus, commission, etc. by an individual taxpayer

for rendering any personal services (Pert et al. 2017). The law court in “Brown v FCT

(2002)” explains that receipts which is associated to carrying out of service is treated as

product or incidence of employment or reward for activity. Such receipts amounts to taxable

ordinary income.

Personal gifts are normally treated as taxable earnings under “sec 6-5 ITAA 1997”.

Where the personal gifts, opposite to other type of voluntary payments that are related to

3TAXATION LAW

employment or services provided, are not viewed as taxable ordinary income. In the case of

“Scott v FCT (1966)” the solicitor was paid a huge amount of (10,000 pound) simply

because the solicitor acted for the widowed wife in regard of this estate and as the gesture of

friendship (Lam and Whitney 2016). The federal court held the amount non-taxable under

“sec 25 (1) of ITAA 1936”.

Under “sec 66 (1) FBTAA 1986”, FBT is normally imposed on the employer. The

taxes are normally imposed on the basis of fringe benefits and not on the receiver of benefit.

Under “sec 136 (1) FBTAA 1986” fringe benefit refers to rights, privilege, services of

facility that is given for carrying out work in respect of employment (Sadiq 2016). While

“sec 137 FBTAA 1986” assures that FBT is applicable when there is evident employment

relationship however the employee is provided with non-cash benefits rather than salary or

wages. Under “sec 23L” the employer is held liable for tax on the worth of fringe benefit

provided to employee. In “Essenboourne Pty Ltd v FCT (2002)” the benefit should be

related to employee only.

As stated by ATO cash gifts given during birthday present or special occasion are not

held as taxable income for the recipient. For example, present given from father to son is

considered as non-taxable income. As noted in “Hayes v FCT (1956)” gift of parcel of shares

in conjunction with payments do not have the taxable income character.

Application:

The current case study involves Emmi who is studying accounting in Holmes Institute

and works for part-time basis in Crown Melbourne restaurant. In the present income year

Emmi got $335 cash as tips from its customers. The cash tips of $335 should be viewed as

voluntary payments which is recovered as the part of reward for service. The cash amount is

an income under ordinary concepts because the benefits represents an incidence of Emmi’s

employment or services provided, are not viewed as taxable ordinary income. In the case of

“Scott v FCT (1966)” the solicitor was paid a huge amount of (10,000 pound) simply

because the solicitor acted for the widowed wife in regard of this estate and as the gesture of

friendship (Lam and Whitney 2016). The federal court held the amount non-taxable under

“sec 25 (1) of ITAA 1936”.

Under “sec 66 (1) FBTAA 1986”, FBT is normally imposed on the employer. The

taxes are normally imposed on the basis of fringe benefits and not on the receiver of benefit.

Under “sec 136 (1) FBTAA 1986” fringe benefit refers to rights, privilege, services of

facility that is given for carrying out work in respect of employment (Sadiq 2016). While

“sec 137 FBTAA 1986” assures that FBT is applicable when there is evident employment

relationship however the employee is provided with non-cash benefits rather than salary or

wages. Under “sec 23L” the employer is held liable for tax on the worth of fringe benefit

provided to employee. In “Essenboourne Pty Ltd v FCT (2002)” the benefit should be

related to employee only.

As stated by ATO cash gifts given during birthday present or special occasion are not

held as taxable income for the recipient. For example, present given from father to son is

considered as non-taxable income. As noted in “Hayes v FCT (1956)” gift of parcel of shares

in conjunction with payments do not have the taxable income character.

Application:

The current case study involves Emmi who is studying accounting in Holmes Institute

and works for part-time basis in Crown Melbourne restaurant. In the present income year

Emmi got $335 cash as tips from its customers. The cash tips of $335 should be viewed as

voluntary payments which is recovered as the part of reward for service. The cash amount is

an income under ordinary concepts because the benefits represents an incidence of Emmi’s

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

employment. Mentioning the judgement of “Calvert v Wainwright (1947)” tips that is given

to Emmi signifies a voluntary payment because it is given to her for her services rendered

(Kenny, Blissenden and Villios 2016). The amount establishes a nexus among the services

provided and taxable as ordinary income under “sec 6-5 ITAA 1997”.

She received $25,000 as income from her employment during the year. The sum of

$25,000 under “sec 6 (1) ITAA 1936” is an income from personal exertion. Mentioning the

judgement of “Brown v FCT (2002)” the amount received by Emmi is associated to carrying

out of employment service (Sadiq and Hreal 2017). It should be treated as product of

employment and amounts to taxable ordinary income under “sec 6-5 ITAA 1997”.

Emmi reports an event where one of her regular customer gifted her with a perfume

that has worth of $250 during Christmas time. The perfume is a personal gift which is

opposite to other type of voluntary payments that are related to employment or services

provided and are not viewed as taxable ordinary income. Referring to “Scott v FCT (1966)”

the perfume received by Emmi is non-taxable income under “sec 25 (1) of ITAA 1936”.

Furthermore, the perfume cannot be converted into money or money’s worth and fails to

meet the characteristics of ordinary income.

All through the year Emmi was paid a monthly entertainment event by the employer.

The owner also spent $380 for Emmi’s meal. Under “sec 136 (1) FBTAA 1986” the monthly

entertainment event and meal expenses paid by employer is a fringe benefit that is given to

Emmi for carrying out work in respect of her employment (Kenny 2015). Citing

“Essenboourne Pty Ltd v FCT (2002)” a fringe benefit tax will be applicable under “sec 137

FBTAA 1986” since there is an evident employee and employer relationship. Under “sec

23L” the Crown Melbourne restaurant should be held liable for tax on the worth of fringe

benefit provided to Emmi.

employment. Mentioning the judgement of “Calvert v Wainwright (1947)” tips that is given

to Emmi signifies a voluntary payment because it is given to her for her services rendered

(Kenny, Blissenden and Villios 2016). The amount establishes a nexus among the services

provided and taxable as ordinary income under “sec 6-5 ITAA 1997”.

She received $25,000 as income from her employment during the year. The sum of

$25,000 under “sec 6 (1) ITAA 1936” is an income from personal exertion. Mentioning the

judgement of “Brown v FCT (2002)” the amount received by Emmi is associated to carrying

out of employment service (Sadiq and Hreal 2017). It should be treated as product of

employment and amounts to taxable ordinary income under “sec 6-5 ITAA 1997”.

Emmi reports an event where one of her regular customer gifted her with a perfume

that has worth of $250 during Christmas time. The perfume is a personal gift which is

opposite to other type of voluntary payments that are related to employment or services

provided and are not viewed as taxable ordinary income. Referring to “Scott v FCT (1966)”

the perfume received by Emmi is non-taxable income under “sec 25 (1) of ITAA 1936”.

Furthermore, the perfume cannot be converted into money or money’s worth and fails to

meet the characteristics of ordinary income.

All through the year Emmi was paid a monthly entertainment event by the employer.

The owner also spent $380 for Emmi’s meal. Under “sec 136 (1) FBTAA 1986” the monthly

entertainment event and meal expenses paid by employer is a fringe benefit that is given to

Emmi for carrying out work in respect of her employment (Kenny 2015). Citing

“Essenboourne Pty Ltd v FCT (2002)” a fringe benefit tax will be applicable under “sec 137

FBTAA 1986” since there is an evident employee and employer relationship. Under “sec

23L” the Crown Melbourne restaurant should be held liable for tax on the worth of fringe

benefit provided to Emmi.

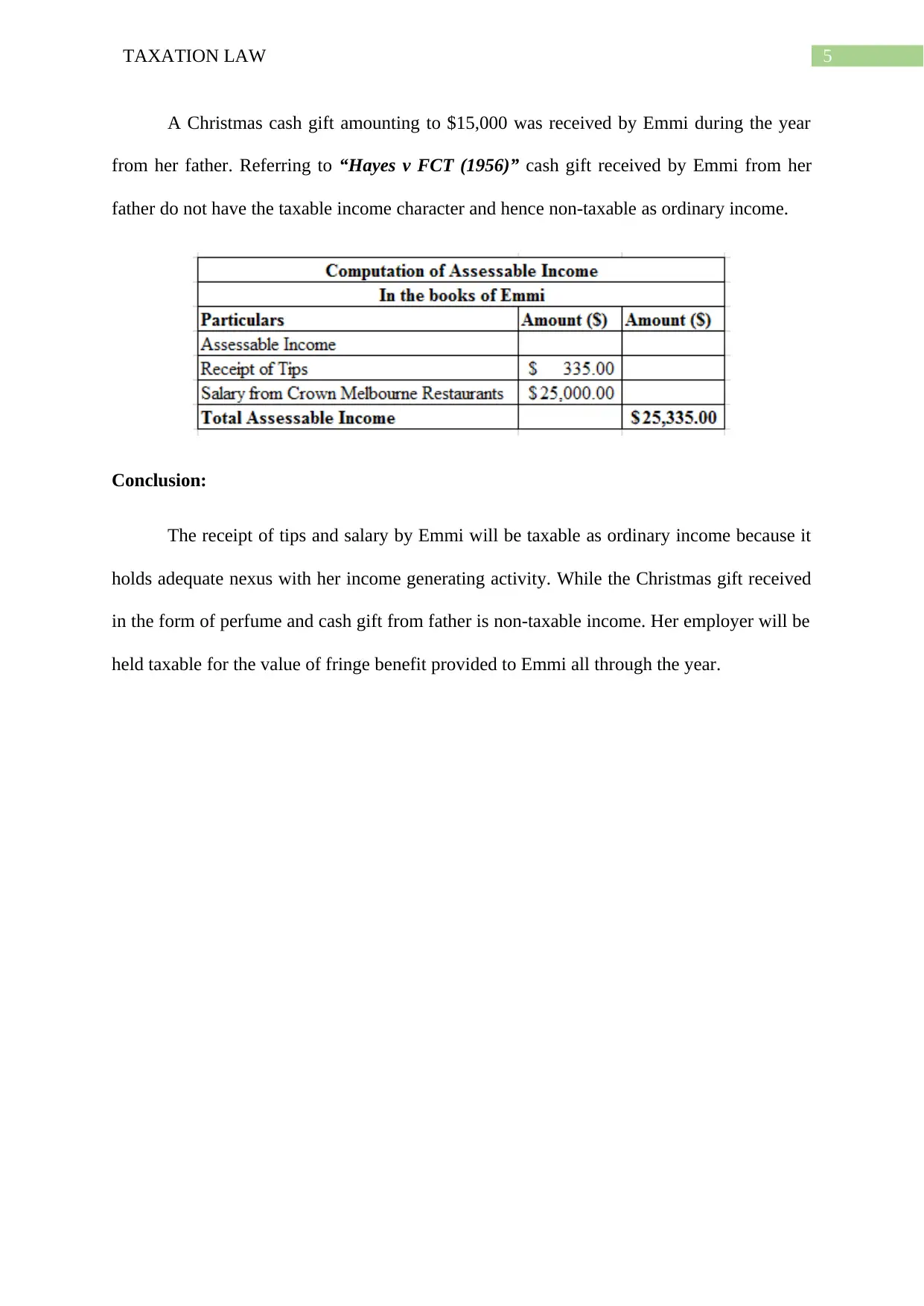

5TAXATION LAW

A Christmas cash gift amounting to $15,000 was received by Emmi during the year

from her father. Referring to “Hayes v FCT (1956)” cash gift received by Emmi from her

father do not have the taxable income character and hence non-taxable as ordinary income.

Conclusion:

The receipt of tips and salary by Emmi will be taxable as ordinary income because it

holds adequate nexus with her income generating activity. While the Christmas gift received

in the form of perfume and cash gift from father is non-taxable income. Her employer will be

held taxable for the value of fringe benefit provided to Emmi all through the year.

A Christmas cash gift amounting to $15,000 was received by Emmi during the year

from her father. Referring to “Hayes v FCT (1956)” cash gift received by Emmi from her

father do not have the taxable income character and hence non-taxable as ordinary income.

Conclusion:

The receipt of tips and salary by Emmi will be taxable as ordinary income because it

holds adequate nexus with her income generating activity. While the Christmas gift received

in the form of perfume and cash gift from father is non-taxable income. Her employer will be

held taxable for the value of fringe benefit provided to Emmi all through the year.

6TAXATION LAW

Answer to question 2:

Answer A:

The legislation of CGT was introduced with the only objective of imposing tax on the

capital gains. The provision of taxing capital gains arises when the CGT assets are purchased

after 20 Sept 1985. These assets are known as “post-CGT assets” and should be subsequently

sold or disposed (Jogarajan 2016). In the meantime, assets that is purchased before the date of

20 Sept 1985 are termed as “Pre-CGT” assets. Capital gains or loss that happens from selling

these type of assets are ignored.

The case facts of Liu suggest that she has decided to sell the house that she had

purchased in 1981 for a cost of $55,000. The house was ultimately disposed for $630,000 in

the present tax year. As the house was bought before the 20 Sept 1985, it must be termed as

“Pre-CGT Assets”. The capital gains which Liu has earned from disposing her main

residence will be simply disregarded from the regimes of CGT.

Answer B:

As noted in “sect 108-5 ITAA 1997” CGT asset is a form of property or legal rights

which cannot be held as property. When the CGT asset is sold then a “CGT event A1” under

“sec 104-10 ITA Act 1997” happens. As noted in subdivision 108-C assets which a taxpayer

holds for their own use (Schurgott 2016). Under “sect 108-20 (2) & (3) ITAA 1997” the

examples of personal use asset are boats, furniture, motor vehicles, electrical items etc. A

taxpayer under the “sec 108-20 (1)” is needed to disregard the capital loss that is suffered

from disposing the personal use asset.

As Liu is selling all her Australian assets and moving to China, she reports the

disposal of car that she had purchased in 2011 for an acquisition cost of $37,000. The sale

price of car fetched Liu approximately $8,000. The car is treated as personal use CGT asset

Answer to question 2:

Answer A:

The legislation of CGT was introduced with the only objective of imposing tax on the

capital gains. The provision of taxing capital gains arises when the CGT assets are purchased

after 20 Sept 1985. These assets are known as “post-CGT assets” and should be subsequently

sold or disposed (Jogarajan 2016). In the meantime, assets that is purchased before the date of

20 Sept 1985 are termed as “Pre-CGT” assets. Capital gains or loss that happens from selling

these type of assets are ignored.

The case facts of Liu suggest that she has decided to sell the house that she had

purchased in 1981 for a cost of $55,000. The house was ultimately disposed for $630,000 in

the present tax year. As the house was bought before the 20 Sept 1985, it must be termed as

“Pre-CGT Assets”. The capital gains which Liu has earned from disposing her main

residence will be simply disregarded from the regimes of CGT.

Answer B:

As noted in “sect 108-5 ITAA 1997” CGT asset is a form of property or legal rights

which cannot be held as property. When the CGT asset is sold then a “CGT event A1” under

“sec 104-10 ITA Act 1997” happens. As noted in subdivision 108-C assets which a taxpayer

holds for their own use (Schurgott 2016). Under “sect 108-20 (2) & (3) ITAA 1997” the

examples of personal use asset are boats, furniture, motor vehicles, electrical items etc. A

taxpayer under the “sec 108-20 (1)” is needed to disregard the capital loss that is suffered

from disposing the personal use asset.

As Liu is selling all her Australian assets and moving to China, she reports the

disposal of car that she had purchased in 2011 for an acquisition cost of $37,000. The sale

price of car fetched Liu approximately $8,000. The car is treated as personal use CGT asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

under “sect 108-20 (2) & (3)”. The sale of car has given rise to “CGT event A1” under “sec

104-10”. With respect to the special rules given in “sec 108-20 (1)” Liu is needed to

disregard the capital loss that is suffered from disposing the car.

Answer C:

“Div 152 of ITAA 1997” deals with small business concession for the CGT events that

happens on or following the 21/9/1999. When a CGT asset meets the “active asset test” there

are four types of concessions which is available to the taxpayer of small business that has the

net value of CGT asset is not greater than $6 million under “sec 152-10 of ITAA 1997” (Lee

2017). The concessions available to small business are

1. 15-year ownership of asset capital gains exemption under “Subdivision 152-B”.

2. 50% reduction from capital gains under “subdivision 152-C”

3. Retirement capital gains exemption up to a sum of $500,000 under “subdivision 152-

D”

4. Roll-over relief asset replacement under “subdivision 152-E”.

A “CGT event C1” comes into the act when the goodwill of a business is destroyed.

When a business is ceased permanently whether it is out of voluntary or involuntary act, the

ruling explains that there is a “loss” or “destruction of goodwill” relating to business.

In the current situation of Liu, she has decided to retire from her business. The

business was permanently ceased and taken over by a purchaser for a sum of $125,000. Liu

will be considered eligible for small business CGT concession under “sec 152-10 ITAA

1997”. The value of her CGT asset is not greater than $6 million. Liu can obtain a 15-year

exemption from the capital gains earned from disposal of her photography equipment as it is

assumed that she has held the asset for a minimum of 15 years. While for her business

goodwill a “CGT event C1” happened when it was disposed by Liu. As a result, under

under “sect 108-20 (2) & (3)”. The sale of car has given rise to “CGT event A1” under “sec

104-10”. With respect to the special rules given in “sec 108-20 (1)” Liu is needed to

disregard the capital loss that is suffered from disposing the car.

Answer C:

“Div 152 of ITAA 1997” deals with small business concession for the CGT events that

happens on or following the 21/9/1999. When a CGT asset meets the “active asset test” there

are four types of concessions which is available to the taxpayer of small business that has the

net value of CGT asset is not greater than $6 million under “sec 152-10 of ITAA 1997” (Lee

2017). The concessions available to small business are

1. 15-year ownership of asset capital gains exemption under “Subdivision 152-B”.

2. 50% reduction from capital gains under “subdivision 152-C”

3. Retirement capital gains exemption up to a sum of $500,000 under “subdivision 152-

D”

4. Roll-over relief asset replacement under “subdivision 152-E”.

A “CGT event C1” comes into the act when the goodwill of a business is destroyed.

When a business is ceased permanently whether it is out of voluntary or involuntary act, the

ruling explains that there is a “loss” or “destruction of goodwill” relating to business.

In the current situation of Liu, she has decided to retire from her business. The

business was permanently ceased and taken over by a purchaser for a sum of $125,000. Liu

will be considered eligible for small business CGT concession under “sec 152-10 ITAA

1997”. The value of her CGT asset is not greater than $6 million. Liu can obtain a 15-year

exemption from the capital gains earned from disposal of her photography equipment as it is

assumed that she has held the asset for a minimum of 15 years. While for her business

goodwill a “CGT event C1” happened when it was disposed by Liu. As a result, under

8TAXATION LAW

“Subdivision 152-D”, Liu can obtain a retirement concession because the value of capital

gains does not goes past $500,000 limit.

Answer D:

The special rules that is given for personal use asset under “sec 118-10 ITAA 1997”

states that capital gains that arises from the disposal must be ignored if the taxpayer has

purchased the asset for an acquisition cost of less than $10,000 (Spence 2016). As apparent,

Liu during the year sold furniture for $4,800. The cost of furniture when Liu purchased it

stood not greater than $2,000.

The furniture here is categorized as personal use asset under “sec 108-20 (2) & (3)

ITAA 1997”. When Liu sold the furniture a capital gain occurred. However, Liu must

disregard the capital gains from furniture under “sec 118-10 ITA Act 1997” because the cost

base is less than $10,000.

Answer to E:

As denoted within “subdivision 108-B” collectables are regarded as a form of CGT

asset that the taxpayer holds in their possession for private enjoyment and use purpose.

Importantly under “sec 108-10 (2) & (3) ITAA 1997” examples of collectables are paintings,

jewellery, stamps, coins and antiques (Lee 2017). The special rules say that capital gains and

loss should necessarily be ignored under “sec 118-10 (1)” when the cost base of asset is $500

or less.

Liu bought a large number of paintings from a second hand shops for $500 each. In

the current tax year, she sold the paintings for $28,000. The paintings must be treated as

collectable under “sec 108-10 (2) & (3) ITAA 1997” because Liu purchased it for her private

enjoyment. The capital gains derived from painting is to be ignored by Liu under “sec 118-10

(1)” since the cost base of asset is $500 only and fails to meet the first element of cost base.

“Subdivision 152-D”, Liu can obtain a retirement concession because the value of capital

gains does not goes past $500,000 limit.

Answer D:

The special rules that is given for personal use asset under “sec 118-10 ITAA 1997”

states that capital gains that arises from the disposal must be ignored if the taxpayer has

purchased the asset for an acquisition cost of less than $10,000 (Spence 2016). As apparent,

Liu during the year sold furniture for $4,800. The cost of furniture when Liu purchased it

stood not greater than $2,000.

The furniture here is categorized as personal use asset under “sec 108-20 (2) & (3)

ITAA 1997”. When Liu sold the furniture a capital gain occurred. However, Liu must

disregard the capital gains from furniture under “sec 118-10 ITA Act 1997” because the cost

base is less than $10,000.

Answer to E:

As denoted within “subdivision 108-B” collectables are regarded as a form of CGT

asset that the taxpayer holds in their possession for private enjoyment and use purpose.

Importantly under “sec 108-10 (2) & (3) ITAA 1997” examples of collectables are paintings,

jewellery, stamps, coins and antiques (Lee 2017). The special rules say that capital gains and

loss should necessarily be ignored under “sec 118-10 (1)” when the cost base of asset is $500

or less.

Liu bought a large number of paintings from a second hand shops for $500 each. In

the current tax year, she sold the paintings for $28,000. The paintings must be treated as

collectable under “sec 108-10 (2) & (3) ITAA 1997” because Liu purchased it for her private

enjoyment. The capital gains derived from painting is to be ignored by Liu under “sec 118-10

(1)” since the cost base of asset is $500 only and fails to meet the first element of cost base.

9TAXATION LAW

Liu however sold one of her paintings that she purchased it from an artist for $1,000. The

painting was sold for $8,000. The capital gains that is earned by Liu forms the part of her

assessable income and will be taxable as statutory income under “sec 102-5 ITAA 1997”.

Liu however sold one of her paintings that she purchased it from an artist for $1,000. The

painting was sold for $8,000. The capital gains that is earned by Liu forms the part of her

assessable income and will be taxable as statutory income under “sec 102-5 ITAA 1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

References:

Jogarajan, S., 2016. Regulating the regulator: assessing the effectiveness of the ATO's

external scrutiny arrangements. Journal of Australian Taxation, 18(1), p.23.

Kenny, P., 2015. LexisNexis concise tax legislation 2016,

Kenny, P., Blissenden, M. and Villios, S., 2016. Australian tax 2016,

Lam, D and Whitney, A, 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, 3(3), pp.84–85.

Lee, Y., 2017. Australian Practice in International Law 2016. Australian Yearbook of

International Law, 35, pp.373–508.

Pert, Alison, Chen, Helen and Carvosso, Rhys, 2017. 'Federal Commissioner of Taxation v

Jayasinghe' (2016) 247 FCR 40. Australian Year Book of International Law, 35, pp.260–262.

Sadiq, K C.C.and Hreal. et al., 2017. Principles of taxation law 2017 10th ed., Place of

publication not identified]: THOMSON LAWBOOK CO.

Sadiq, K. et al., 2016. Principles of taxation law 2016 Ninth., Sydney: Thomson Reuters.

Schurgott, K, 2016. Practical issues with trusts: Important updates. Tax Specialist, 20(1),

pp.2–9.

Sharkey, N, 2016. Reinventing administrative leadership in Australian taxation: Beware the

fine balance of social psychological and rule of law principles. AUSTRALIAN TAX

FORUM, 31(1), pp.63–97.

Spence, K, 2016. The evolution of corporate taxation - a work in progress. Australian Tax

Forum, 31(3), pp.481–508.

References:

Jogarajan, S., 2016. Regulating the regulator: assessing the effectiveness of the ATO's

external scrutiny arrangements. Journal of Australian Taxation, 18(1), p.23.

Kenny, P., 2015. LexisNexis concise tax legislation 2016,

Kenny, P., Blissenden, M. and Villios, S., 2016. Australian tax 2016,

Lam, D and Whitney, A, 2016. Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, 3(3), pp.84–85.

Lee, Y., 2017. Australian Practice in International Law 2016. Australian Yearbook of

International Law, 35, pp.373–508.

Pert, Alison, Chen, Helen and Carvosso, Rhys, 2017. 'Federal Commissioner of Taxation v

Jayasinghe' (2016) 247 FCR 40. Australian Year Book of International Law, 35, pp.260–262.

Sadiq, K C.C.and Hreal. et al., 2017. Principles of taxation law 2017 10th ed., Place of

publication not identified]: THOMSON LAWBOOK CO.

Sadiq, K. et al., 2016. Principles of taxation law 2016 Ninth., Sydney: Thomson Reuters.

Schurgott, K, 2016. Practical issues with trusts: Important updates. Tax Specialist, 20(1),

pp.2–9.

Sharkey, N, 2016. Reinventing administrative leadership in Australian taxation: Beware the

fine balance of social psychological and rule of law principles. AUSTRALIAN TAX

FORUM, 31(1), pp.63–97.

Spence, K, 2016. The evolution of corporate taxation - a work in progress. Australian Tax

Forum, 31(3), pp.481–508.

11TAXATION LAW

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.