TAXATION LAW AND MANAGEMENT l ASSIGNMENT

VerifiedAdded on 2022/09/22

|15

|2416

|19

Assignment

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Executive summary:

The current note is aimed at giving summary of tax related information to the taxpayer for the

applicable income year of 2019. The letter of recommendation will be covering the

substances of small business entity concession that are obtainable to the taxpayer. The letter

of advice will consist of facts whether the taxpayer will be instantaneously capable of writing

off each asset acquired by him recently. The letter of advice will also lay down the advice

relating to depreciation and will converse the most suitable technique that is appropriate for

the taxpayer.

Executive summary:

The current note is aimed at giving summary of tax related information to the taxpayer for the

applicable income year of 2019. The letter of recommendation will be covering the

substances of small business entity concession that are obtainable to the taxpayer. The letter

of advice will consist of facts whether the taxpayer will be instantaneously capable of writing

off each asset acquired by him recently. The letter of advice will also lay down the advice

relating to depreciation and will converse the most suitable technique that is appropriate for

the taxpayer.

2TAXATION LAW

Private and Confidential

Roma Tax Advice & CO

18 Pollock Street

Smithville VIC 3207

Mr Herbie

65 Smith Street

Smithville VIC 3207

Dear Herbie,

To proceed further with our most current discussion, we would request you to please

find below our letter of advice that contains valuable advice relating to the matters as

requested by you.

Scope:

The scope of this letter is to advice you on the matters relating to “Small Business

Entity” and its concession.

Note: Please note that the current letter simply excludes the tax consequences that will follow

if the asset is surplus in the organization either on the basis of loan, distribution or payment.

Facts:

The current advice is based on the relevant taxation laws, cases and guidelines that are

issued by the ATO as we understand its application in your situation.

Summary of Advice:

Private and Confidential

Roma Tax Advice & CO

18 Pollock Street

Smithville VIC 3207

Mr Herbie

65 Smith Street

Smithville VIC 3207

Dear Herbie,

To proceed further with our most current discussion, we would request you to please

find below our letter of advice that contains valuable advice relating to the matters as

requested by you.

Scope:

The scope of this letter is to advice you on the matters relating to “Small Business

Entity” and its concession.

Note: Please note that the current letter simply excludes the tax consequences that will follow

if the asset is surplus in the organization either on the basis of loan, distribution or payment.

Facts:

The current advice is based on the relevant taxation laws, cases and guidelines that are

issued by the ATO as we understand its application in your situation.

Summary of Advice:

3TAXATION LAW

The necessary facts and assumptions on the basis of which our advice was based

along with the summary of your brief has been outlined in the Appendix A. In case you

notice that any of our facts or assumptions do not meet your understanding then please

contact us immediately because this will carry an effect on the advice that is given. In

summary our advice are as follows:

Issues:

1. Is Herbie is regarded as small business entity within the purpose of “ITAA 1997”?

2. Is Herbie eligible for claiming any available concession that are allowed to small

business entity?

3. Is Herbie allowed to claim an immediate deduction or write off of assets that is

purchased by her recently?

4. Is Herbie eligible for obtaining deduction in respect of the decline in value of asset or

any available method of claiming depreciation?

Rule:

Small Business Entity

As explained by the ATO a business may be classified as small business entity if it is a

partnership, company, individual or trust that is;

a. Doing or carrying any business

b. Has the total or aggregate turnover of lower than $10 million.

The aggregate turnover represents the yearly turnover along with the yearly turnover

of any other businesses a taxpayer is having connection with or have influence over it1. The

1 "Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-

detail/Depreciating-assets/Simplified-depreciation---rules-and-calculations/>

The necessary facts and assumptions on the basis of which our advice was based

along with the summary of your brief has been outlined in the Appendix A. In case you

notice that any of our facts or assumptions do not meet your understanding then please

contact us immediately because this will carry an effect on the advice that is given. In

summary our advice are as follows:

Issues:

1. Is Herbie is regarded as small business entity within the purpose of “ITAA 1997”?

2. Is Herbie eligible for claiming any available concession that are allowed to small

business entity?

3. Is Herbie allowed to claim an immediate deduction or write off of assets that is

purchased by her recently?

4. Is Herbie eligible for obtaining deduction in respect of the decline in value of asset or

any available method of claiming depreciation?

Rule:

Small Business Entity

As explained by the ATO a business may be classified as small business entity if it is a

partnership, company, individual or trust that is;

a. Doing or carrying any business

b. Has the total or aggregate turnover of lower than $10 million.

The aggregate turnover represents the yearly turnover along with the yearly turnover

of any other businesses a taxpayer is having connection with or have influence over it1. The

1 "Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-

detail/Depreciating-assets/Simplified-depreciation---rules-and-calculations/>

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

rule of aggregation ascertain when a person is required to include the yearly turnover of

another business when they are computing their aggregate turnover. An individual will be

classified as small business if they are not related with any other business and their business

turnover is lower than $10 million.

The small business Eligibility Test:

The small business eligibility test requires a business to meet one of the below stated

criteria;

a. It is a small business entity as explained in

“Div 328 ITAA 1997”, widely that is

executing its business activities and has the aggregate turnover of lower than $10

million during the income year; or

b. It is a partner in the partnership that is considered as the small business entity; or

c. The overall net “value of assets” of a taxpayer and its related entities do not surpass

$6 million2.

Active asset Test:

The asset that is disposed by the small business is used by the taxpayer in conducting

or doing business activities.

Concessional stakeholder test:

This test is only applied if the asset which is sold by the taxpayer in the company or

an interest in a trust.

Small Business CGT Concessions:

2 Barkoczy, Stephen, Foundations Of Taxation Law 2018

rule of aggregation ascertain when a person is required to include the yearly turnover of

another business when they are computing their aggregate turnover. An individual will be

classified as small business if they are not related with any other business and their business

turnover is lower than $10 million.

The small business Eligibility Test:

The small business eligibility test requires a business to meet one of the below stated

criteria;

a. It is a small business entity as explained in

“Div 328 ITAA 1997”, widely that is

executing its business activities and has the aggregate turnover of lower than $10

million during the income year; or

b. It is a partner in the partnership that is considered as the small business entity; or

c. The overall net “value of assets” of a taxpayer and its related entities do not surpass

$6 million2.

Active asset Test:

The asset that is disposed by the small business is used by the taxpayer in conducting

or doing business activities.

Concessional stakeholder test:

This test is only applied if the asset which is sold by the taxpayer in the company or

an interest in a trust.

Small Business CGT Concessions:

2 Barkoczy, Stephen, Foundations Of Taxation Law 2018

5TAXATION LAW

On satisfying the above stated small business eligibility test the small business are

given four CGT concessions when they sell their business assets3.

15-Year Exemption: Under “sec 152-105 ITAA 1997” a small business is given with 15-

year exemption from CGT is given upon retirement4. This requires the taxpayer to completely

ignore the capital gains if the taxpayer has used the asset for a minimum of 15 years in the

business.

50% Reduction in CGT: Under the “sec 152-205 ITAA 1997” another 50% reduction in

capital gains is given on top of the usual CGT discount.

Retirement Exemption: Under the “sec 152-305 ITAA 1997” a retirement concession is

allowed to the taxpayer to disregard the capital gains for a maximum of $500,000.

Replacement asset roll-over: Under “sec 152-405 ITAA 1997” a capital gain is deferred

until an event occurs to the “replacement asset”5.

Immediate writing off asset:

Within the instant asset write-off eligible business is allowed to claim;

a. Under the instant write-off the cost of every asset which has the cost of lower than the

threshold limit.

3 Deutsch, Robert Et Al, Australian Tax Handbook 2018 (Thomson Reuters Australia, 2018)

4 "Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/in-

detail/depreciating-assets/simplified-depreciation---rules-and-calculations/?page=4>

5 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

On satisfying the above stated small business eligibility test the small business are

given four CGT concessions when they sell their business assets3.

15-Year Exemption: Under “sec 152-105 ITAA 1997” a small business is given with 15-

year exemption from CGT is given upon retirement4. This requires the taxpayer to completely

ignore the capital gains if the taxpayer has used the asset for a minimum of 15 years in the

business.

50% Reduction in CGT: Under the “sec 152-205 ITAA 1997” another 50% reduction in

capital gains is given on top of the usual CGT discount.

Retirement Exemption: Under the “sec 152-305 ITAA 1997” a retirement concession is

allowed to the taxpayer to disregard the capital gains for a maximum of $500,000.

Replacement asset roll-over: Under “sec 152-405 ITAA 1997” a capital gain is deferred

until an event occurs to the “replacement asset”5.

Immediate writing off asset:

Within the instant asset write-off eligible business is allowed to claim;

a. Under the instant write-off the cost of every asset which has the cost of lower than the

threshold limit.

3 Deutsch, Robert Et Al, Australian Tax Handbook 2018 (Thomson Reuters Australia, 2018)

4 "Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/in-

detail/depreciating-assets/simplified-depreciation---rules-and-calculations/?page=4>

5 Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

6TAXATION LAW

b. Obtain a tax deduction for business part of the purchase cost during the year in which

the asset is first used or installed as ready for use.

The instant asset write-off can be used for the new and second hand assets. The

$30,000 instant asset write-off provides the small business with the asset write-off. The asset

should have the cost of lower than instant asset write-off threshold and should be purchased

as well as used in the year when the write-off is claimed. In order to be eligible for claiming

an instant asset write-off a business should be recognized as small business by the ATO.

Depreciation:

Under the

“Div 40 ITAA 1997” uniform capital allowance is given to the taxpayer.

Under the

“sec 40-25 (1)” an entity is given the permission of claiming a deduction for the

decline in value for the income year relating to a depreciating asset that is held by the

taxpayer all through the year6. To compute the depreciation for majority of asset an individual

is permitted to implement the general depreciation rules unless a taxpayer is considered

eligible for using the install asset write off or the simplified depreciation for the small

business. The general rules of depreciation set down that the amount which can be claimed on

the basis of effective life of the asset.

To compute the depreciation, a taxpayer is allowed to claim depreciation either by

using the prime cost method or the diminishing value method. In majority of the cases, a

taxpayer is permitted to choose either of the two alternative methods for computing the

depreciation. This involves the

“prime cost method” and the

“diminishing value method”.

Under the prime cost method depreciation for decline in value of asset is computed by

6 Nethercott, Les, Australian Taxation Study Manual 2018 (Oxford University Press, 2018)

b. Obtain a tax deduction for business part of the purchase cost during the year in which

the asset is first used or installed as ready for use.

The instant asset write-off can be used for the new and second hand assets. The

$30,000 instant asset write-off provides the small business with the asset write-off. The asset

should have the cost of lower than instant asset write-off threshold and should be purchased

as well as used in the year when the write-off is claimed. In order to be eligible for claiming

an instant asset write-off a business should be recognized as small business by the ATO.

Depreciation:

Under the

“Div 40 ITAA 1997” uniform capital allowance is given to the taxpayer.

Under the

“sec 40-25 (1)” an entity is given the permission of claiming a deduction for the

decline in value for the income year relating to a depreciating asset that is held by the

taxpayer all through the year6. To compute the depreciation for majority of asset an individual

is permitted to implement the general depreciation rules unless a taxpayer is considered

eligible for using the install asset write off or the simplified depreciation for the small

business. The general rules of depreciation set down that the amount which can be claimed on

the basis of effective life of the asset.

To compute the depreciation, a taxpayer is allowed to claim depreciation either by

using the prime cost method or the diminishing value method. In majority of the cases, a

taxpayer is permitted to choose either of the two alternative methods for computing the

depreciation. This involves the

“prime cost method” and the

“diminishing value method”.

Under the prime cost method depreciation for decline in value of asset is computed by

6 Nethercott, Les, Australian Taxation Study Manual 2018 (Oxford University Press, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

uniformly decreasing the asset over its effective life7. While the diminishing value method

presumes that the value of

“depreciating asset” decreases more during the yearly years of its

effective life.

Application:

Herbie in the current case be classified as small business entity since it is an

individual sole trader because he is carrying on the business and has the overall turnover of

less than $10 million. The business of Herbie is a small business entity under

“Div 328

ITAA 1997”, because it is executing its business activities and has the aggregate turnover of

lower than $10 million during the income year8. Furthermore it is assumed that the overall net

“value of assets” do not surpass $6 million.

As Herbie has met the eligibility test, he can obtain four CGT concessions when he

sell their business assets. Herbie can obtain a 15-year exemption under “sec 152-105 ITAA

1997” from the CGT when he retires from the business given that the assets are used by him

for a minimum of 15-years. Besides this Herbie is also eligible for a 50% reduction in CGT

within “sec 152-205 ITAA 1997” apart from the 50% reduction in capital gains is given on

7 "Prime Cost (Straight Line) And Diminishing Value Methods", Ato.Gov.Au (Webpage,

2020) <https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/

general-depreciation-rules---capital-allowances/prime-cost-(straight-line)-and-diminishing-

value-methods/>

8 Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

uniformly decreasing the asset over its effective life7. While the diminishing value method

presumes that the value of

“depreciating asset” decreases more during the yearly years of its

effective life.

Application:

Herbie in the current case be classified as small business entity since it is an

individual sole trader because he is carrying on the business and has the overall turnover of

less than $10 million. The business of Herbie is a small business entity under

“Div 328

ITAA 1997”, because it is executing its business activities and has the aggregate turnover of

lower than $10 million during the income year8. Furthermore it is assumed that the overall net

“value of assets” do not surpass $6 million.

As Herbie has met the eligibility test, he can obtain four CGT concessions when he

sell their business assets. Herbie can obtain a 15-year exemption under “sec 152-105 ITAA

1997” from the CGT when he retires from the business given that the assets are used by him

for a minimum of 15-years. Besides this Herbie is also eligible for a 50% reduction in CGT

within “sec 152-205 ITAA 1997” apart from the 50% reduction in capital gains is given on

7 "Prime Cost (Straight Line) And Diminishing Value Methods", Ato.Gov.Au (Webpage,

2020) <https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/

general-depreciation-rules---capital-allowances/prime-cost-(straight-line)-and-diminishing-

value-methods/>

8 Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

8TAXATION LAW

top of the usual CGT discount9. Furthermore a retirement exemption and a replacement asset

rollover is also available to Herbie.

Herbie during the year has purchased three new VW Beetle. Under division 40 capital

allowance can be claimed by Herbie. To compute the depreciation for majority of asset

Herbie is permitted to implement the general depreciation rules10. With respect to the

“sec

40-25 (1) ITAA 1997” Herbie can claim decline in value of the red VW Beetle is more than

$33,000 because the value of asset is more than the instant asset write-off limit. The instant

asset write-off can be used for the new VW Beetles. As Herbie is a small business it is

qualified for an instant asset it can immediately write off the VW Beetle and yellow VW

Beetle because the value of its asset is lower than $30,000 threshold limit. While the VW red

Beetle asset is depreciated on the basis of prime cost method. The prime cost method is

considered as the most appropriate method of depreciating the asset as this will allow Herbie

to claim deduction on the constant basis11. The asset is purchased as well as used in the year

when the write-off is claimed by Herbie. It is assumed that the asset has the effective life of

five years.

Taxable Income and Tax Liability

The case study further provides that Herbie has reported a total taxable income of

$420,334 following the deduction of all the expenses incurred by the business. The total

9 Taylor, C. J et al, Understanding Taxation Law 2018

10 "Deductions For Prepaid Expenses 2019", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Forms/Deductions-for-prepaid-expenses-2019/?page=5>

11 Woellner, R. H, Australian Taxation Law 2018

top of the usual CGT discount9. Furthermore a retirement exemption and a replacement asset

rollover is also available to Herbie.

Herbie during the year has purchased three new VW Beetle. Under division 40 capital

allowance can be claimed by Herbie. To compute the depreciation for majority of asset

Herbie is permitted to implement the general depreciation rules10. With respect to the

“sec

40-25 (1) ITAA 1997” Herbie can claim decline in value of the red VW Beetle is more than

$33,000 because the value of asset is more than the instant asset write-off limit. The instant

asset write-off can be used for the new VW Beetles. As Herbie is a small business it is

qualified for an instant asset it can immediately write off the VW Beetle and yellow VW

Beetle because the value of its asset is lower than $30,000 threshold limit. While the VW red

Beetle asset is depreciated on the basis of prime cost method. The prime cost method is

considered as the most appropriate method of depreciating the asset as this will allow Herbie

to claim deduction on the constant basis11. The asset is purchased as well as used in the year

when the write-off is claimed by Herbie. It is assumed that the asset has the effective life of

five years.

Taxable Income and Tax Liability

The case study further provides that Herbie has reported a total taxable income of

$420,334 following the deduction of all the expenses incurred by the business. The total

9 Taylor, C. J et al, Understanding Taxation Law 2018

10 "Deductions For Prepaid Expenses 2019", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Forms/Deductions-for-prepaid-expenses-2019/?page=5>

11 Woellner, R. H, Australian Taxation Law 2018

9TAXATION LAW

assessable income for the business stands $11,660,150. On the other hand the total allowable

expenses for Herbie for the year ended 30th June 2020 is $11,239,818. The total amount of

Medicare levy is imposed on the taxable income for Herbie is $8,406.6812. The information

furnished also provides that a PAYG has been withheld that amounted to $5,000. The PAYG

that has been withheld has been considered as a permissible tax offset and same is deducted

from the overall tax liability that is payable by Herbie. On the basis of the information that

has been furnished it can be stated that the overall tax liability for the Herbie stands

$165,653.68.

Conclusion:

Preceding from the above given explanation the advice can be concluded by stating

that Herbie business activities will be categorised as small business entity because the

business being carried on as a sole trader. The business is eligible for small business entity

concession under

“Div 328 ITAA 1997”. This is because the aggregate turnover for the

business during the year do not exceeds the threshold limit of $10 million during the income

year and overall net “value of assets” of the taxpayer and its related entities do not surpass $6

million threshold limit. Herbie will be allowed to claim instant asset write off for blue VW

Beetle and yellow VW Beetle that is purchased by him on 15th February and 6th June

respectively. While for the red VW Beetle depreciation for the decline in value can be

claimed as the cost of asset is beyond the threshold limit of $30,000.

As it has been stated earlier once you have accordingly reviewed our advice given and

you find it appropriate then please let us know as this will have an impact on your tax return.

If you are looking forward to discuss with us for any of the above given matters in more

12 Woellner, R. H, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

assessable income for the business stands $11,660,150. On the other hand the total allowable

expenses for Herbie for the year ended 30th June 2020 is $11,239,818. The total amount of

Medicare levy is imposed on the taxable income for Herbie is $8,406.6812. The information

furnished also provides that a PAYG has been withheld that amounted to $5,000. The PAYG

that has been withheld has been considered as a permissible tax offset and same is deducted

from the overall tax liability that is payable by Herbie. On the basis of the information that

has been furnished it can be stated that the overall tax liability for the Herbie stands

$165,653.68.

Conclusion:

Preceding from the above given explanation the advice can be concluded by stating

that Herbie business activities will be categorised as small business entity because the

business being carried on as a sole trader. The business is eligible for small business entity

concession under

“Div 328 ITAA 1997”. This is because the aggregate turnover for the

business during the year do not exceeds the threshold limit of $10 million during the income

year and overall net “value of assets” of the taxpayer and its related entities do not surpass $6

million threshold limit. Herbie will be allowed to claim instant asset write off for blue VW

Beetle and yellow VW Beetle that is purchased by him on 15th February and 6th June

respectively. While for the red VW Beetle depreciation for the decline in value can be

claimed as the cost of asset is beyond the threshold limit of $30,000.

As it has been stated earlier once you have accordingly reviewed our advice given and

you find it appropriate then please let us know as this will have an impact on your tax return.

If you are looking forward to discuss with us for any of the above given matters in more

12 Woellner, R. H, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

detail then we will request you to please not hesitate and you can contact or reach our

registered office at any point of time during our office hours.

Yours Sincerely

Associate Taxation

Roma Tax Advice & CO

detail then we will request you to please not hesitate and you can contact or reach our

registered office at any point of time during our office hours.

Yours Sincerely

Associate Taxation

Roma Tax Advice & CO

11TAXATION LAW

References:

"Deductions For Prepaid Expenses 2019", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Forms/Deductions-for-prepaid-expenses-2019/?page=5>

"Prime Cost (Straight Line) And Diminishing Value Methods", Ato.Gov.Au (Webpage,

2020) <https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/

general-depreciation-rules---capital-allowances/prime-cost-(straight-line)-and-diminishing-

value-methods/>

"Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/in-

detail/depreciating-assets/simplified-depreciation---rules-and-calculations/?page=4>

"Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-

detail/Depreciating-assets/Simplified-depreciation---rules-and-calculations/>

Barkoczy, Stephen, Foundations Of Taxation Law 2018

Deutsch, Robert Et Al, Australian Tax Handbook 2018 (Thomson Reuters Australia, 2018)

Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

Nethercott, Les, Australian Taxation Study Manual 2018 (Oxford University Press, 2018)

Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

Taylor, C. J et al, Understanding Taxation Law 2018

Woellner, R. H, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

Woellner, R. H, Australian Taxation Law 2018

References:

"Deductions For Prepaid Expenses 2019", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Forms/Deductions-for-prepaid-expenses-2019/?page=5>

"Prime Cost (Straight Line) And Diminishing Value Methods", Ato.Gov.Au (Webpage,

2020) <https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/

general-depreciation-rules---capital-allowances/prime-cost-(straight-line)-and-diminishing-

value-methods/>

"Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-allowances/in-

detail/depreciating-assets/simplified-depreciation---rules-and-calculations/?page=4>

"Simplified Depreciation - Rules And Calculations", Ato.Gov.Au (Webpage, 2020)

<https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-

detail/Depreciating-assets/Simplified-depreciation---rules-and-calculations/>

Barkoczy, Stephen, Foundations Of Taxation Law 2018

Deutsch, Robert Et Al, Australian Tax Handbook 2018 (Thomson Reuters Australia, 2018)

Kenny, Paul, Michael Blissenden and Sylvia Villios, Australian Tax 2018

Nethercott, Les, Australian Taxation Study Manual 2018 (Oxford University Press, 2018)

Sadiq, Kerrie, Australian Taxation Law Cases 2018 (Thomson Reuters, 2018)

Taylor, C. J et al, Understanding Taxation Law 2018

Woellner, R. H, Stephen Barkoczy and Shirley Murphy, Australian Taxation Law 2019

Woellner, R. H, Australian Taxation Law 2018

12TAXATION LAW

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13TAXATION LAW

14TAXATION LAW

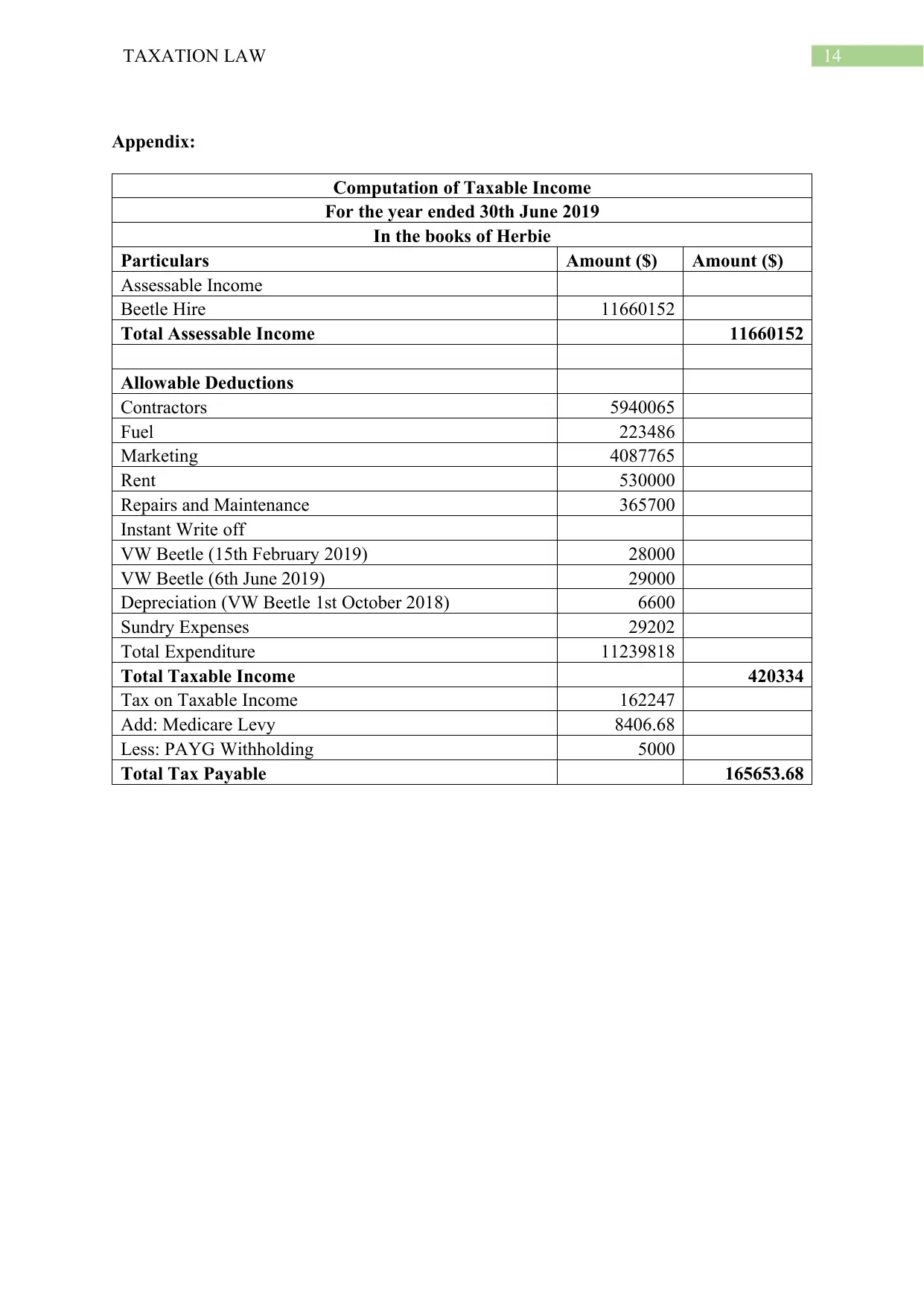

Appendix:

Computation of Taxable Income

For the year ended 30th June 2019

In the books of Herbie

Particulars Amount ($) Amount ($)

Assessable Income

Beetle Hire 11660152

Total Assessable Income 11660152

Allowable Deductions

Contractors 5940065

Fuel 223486

Marketing 4087765

Rent 530000

Repairs and Maintenance 365700

Instant Write off

VW Beetle (15th February 2019) 28000

VW Beetle (6th June 2019) 29000

Depreciation (VW Beetle 1st October 2018) 6600

Sundry Expenses 29202

Total Expenditure 11239818

Total Taxable Income 420334

Tax on Taxable Income 162247

Add: Medicare Levy 8406.68

Less: PAYG Withholding 5000

Total Tax Payable 165653.68

Appendix:

Computation of Taxable Income

For the year ended 30th June 2019

In the books of Herbie

Particulars Amount ($) Amount ($)

Assessable Income

Beetle Hire 11660152

Total Assessable Income 11660152

Allowable Deductions

Contractors 5940065

Fuel 223486

Marketing 4087765

Rent 530000

Repairs and Maintenance 365700

Instant Write off

VW Beetle (15th February 2019) 28000

VW Beetle (6th June 2019) 29000

Depreciation (VW Beetle 1st October 2018) 6600

Sundry Expenses 29202

Total Expenditure 11239818

Total Taxable Income 420334

Tax on Taxable Income 162247

Add: Medicare Levy 8406.68

Less: PAYG Withholding 5000

Total Tax Payable 165653.68

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.