Taxation Law Question Answer 2022

VerifiedAdded on 2022/10/11

|11

|2029

|34

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................4

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to Part A:...................................................................................................................6

Part B:.....................................................................................................................................6

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Article 1: Call to scrap not reform the tax on luxury car:......................................................7

Relevant facts in the article:...................................................................................................7

Concise explanation of tax concepts:.....................................................................................7

Connection between concepts discussed and good tax policy indicators:.............................8

Article 2: Policy nudge could swap stamp duty for land tax:................................................8

Relevant facts in the article:...................................................................................................8

Concise explanation of tax concepts:.....................................................................................8

Connection between concepts discussed and good tax policy indicators:.............................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Issues:.....................................................................................................................................2

Rule:.......................................................................................................................................2

Application:............................................................................................................................3

Conclusion:............................................................................................................................4

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................6

Answer to Part A:...................................................................................................................6

Part B:.....................................................................................................................................6

Answer to question 4:.................................................................................................................6

Answer to question 5:.................................................................................................................7

Article 1: Call to scrap not reform the tax on luxury car:......................................................7

Relevant facts in the article:...................................................................................................7

Concise explanation of tax concepts:.....................................................................................7

Connection between concepts discussed and good tax policy indicators:.............................8

Article 2: Policy nudge could swap stamp duty for land tax:................................................8

Relevant facts in the article:...................................................................................................8

Concise explanation of tax concepts:.....................................................................................8

Connection between concepts discussed and good tax policy indicators:.............................8

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

Will the taxpayer be treated as Australian dweller under the provision of

“6(1), ITAA 1936”?

Rule:

As per

“section 6 (1), ITAA 1936” an individual who lives in Australia and covers

those people that has their home in Australia except when the tax official is satisfied that a

person’s fixed house is out of Australia (Kenny et al., 2018). There are four test that are

applied on the individuals namely;

1. Resides Test in Australia

2. Person’s Domicile in Australia

3. 183-Day Test

4. Commonwealth Superannuation Test

Resides Test:

This test defines the person’s behaviour at the time of living in Australia. This consist

of the intention of taxpayer to live in Australia. It also includes business or occupation ties

and social or living preparations (Krever, 2014). In

“Joachim v FCT (2002)” the taxpayer

was held as Australian resident since the taxpayer kept his family home in Australia and often

retuned home during his employment contracts.

Domicile Test:

A person under this test is Australian occupant if one has abode in Australia,

excluding the officer understands that the person has the fixed place of residence out of

Australia. As said in

“FCT v Applegate (1979)” the law court explained that fixed does not

implies everlasting and the objectivity is assessed every year (Morgan et al., 2013).

Answer to question 1:

Issues:

Will the taxpayer be treated as Australian dweller under the provision of

“6(1), ITAA 1936”?

Rule:

As per

“section 6 (1), ITAA 1936” an individual who lives in Australia and covers

those people that has their home in Australia except when the tax official is satisfied that a

person’s fixed house is out of Australia (Kenny et al., 2018). There are four test that are

applied on the individuals namely;

1. Resides Test in Australia

2. Person’s Domicile in Australia

3. 183-Day Test

4. Commonwealth Superannuation Test

Resides Test:

This test defines the person’s behaviour at the time of living in Australia. This consist

of the intention of taxpayer to live in Australia. It also includes business or occupation ties

and social or living preparations (Krever, 2014). In

“Joachim v FCT (2002)” the taxpayer

was held as Australian resident since the taxpayer kept his family home in Australia and often

retuned home during his employment contracts.

Domicile Test:

A person under this test is Australian occupant if one has abode in Australia,

excluding the officer understands that the person has the fixed place of residence out of

Australia. As said in

“FCT v Applegate (1979)” the law court explained that fixed does not

implies everlasting and the objectivity is assessed every year (Morgan et al., 2013).

3TAXATION LAW

183-Days Test:

A taxpayer is treated as Australian occupant if they have really been present in

Australia either regularly or in breaks for more than six months except when the

commissioner understands that the person has set up his usual place in overseas.

Superannuation Test:

Where a taxpayer is the member of commonwealth superannuation fund, then they

will be treated Australian dweller for tax purpose.

Application:

Taite arrived in Australia on 1st August 2017 and during his visit he did not stayed in

one place. The following test are applied to determine Taite residency status;

Resides Test:

Taite has the residential home in Europe and his family lives there. He intended to

return to Europe following his short stay in Australia and these factors cannot be considered

significant. Mentioning the case of

“Joachim v FCT (2002)” Taite did not show any

intention of living in Australia. Therefore, Taite is not a occupant under this test.

Domicile Test:

Trait has not conclusively explained conclusively that his choice of home is in

Australia. Referring to

“FCT v Applegate (1979)” the circumstances gathered portray that

he has the permanent residence in Europe (Nethercott, 2018). He did not establish any home

in Australia and his stay did not reflect any permanency with a certain place in Australia. So

he is not a resident under this test.

183-Days Test:

A taxpayer is treated as Australian occupant if they have really been present in

Australia either regularly or in breaks for more than six months except when the

commissioner understands that the person has set up his usual place in overseas.

Superannuation Test:

Where a taxpayer is the member of commonwealth superannuation fund, then they

will be treated Australian dweller for tax purpose.

Application:

Taite arrived in Australia on 1st August 2017 and during his visit he did not stayed in

one place. The following test are applied to determine Taite residency status;

Resides Test:

Taite has the residential home in Europe and his family lives there. He intended to

return to Europe following his short stay in Australia and these factors cannot be considered

significant. Mentioning the case of

“Joachim v FCT (2002)” Taite did not show any

intention of living in Australia. Therefore, Taite is not a occupant under this test.

Domicile Test:

Trait has not conclusively explained conclusively that his choice of home is in

Australia. Referring to

“FCT v Applegate (1979)” the circumstances gathered portray that

he has the permanent residence in Europe (Nethercott, 2018). He did not establish any home

in Australia and his stay did not reflect any permanency with a certain place in Australia. So

he is not a resident under this test.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

183-Days Test:

Trait under this cannot be treated as Australia resident because his actual place of

residence is out of Australia in Europe and he does not proposes to take up the residency in

Australia. So he is not the Australian occupant under this test.

Commonwealth Superannuation Test:

This is not applicable on Taite as he is not the member of superannuation fund.

Conclusion:

Conclusively, Taite cannot be treated as Australian resident under the provision of

“6

(1), ITAA 1936” as he did not any above test since his stay is temporary in nature.

Answer to question 2:

The main provision which gives the taxpayer with the deduction for an outgoing that

are general deduction provision of

“section 8-1, ITAA 1997”. A deduction is allowed is to

taxpayer under

“section 8-1, ITAA 1997” from his or her taxable earnings if the outgoings

are occurred in deriving the assessable income (Sadiq, 2018). While specific deduction

originates under

“section 8-5, ITAA 1997” when a specific provision of the income tax

legislation allows the taxpayer with the deduction. While under

“section 25-5” deduction is

not available in certain situations such as for capital expenditure. Additionally,

“section 8-1

(2)” explains that deduction is not provided under general limbs for expenditures that are

capital or capital in nature.

During the year Derek installed a new internal wall during August 2017. He also

repainted the current walls and laid down new carpet all through the year. Referring to

“section 25-10(3), ITAA 1997” the installation of new internal wall, repainting of current

wall and laying down of carpet is not permitted for deduction since it is a capital expenditure

183-Days Test:

Trait under this cannot be treated as Australia resident because his actual place of

residence is out of Australia in Europe and he does not proposes to take up the residency in

Australia. So he is not the Australian occupant under this test.

Commonwealth Superannuation Test:

This is not applicable on Taite as he is not the member of superannuation fund.

Conclusion:

Conclusively, Taite cannot be treated as Australian resident under the provision of

“6

(1), ITAA 1936” as he did not any above test since his stay is temporary in nature.

Answer to question 2:

The main provision which gives the taxpayer with the deduction for an outgoing that

are general deduction provision of

“section 8-1, ITAA 1997”. A deduction is allowed is to

taxpayer under

“section 8-1, ITAA 1997” from his or her taxable earnings if the outgoings

are occurred in deriving the assessable income (Sadiq, 2018). While specific deduction

originates under

“section 8-5, ITAA 1997” when a specific provision of the income tax

legislation allows the taxpayer with the deduction. While under

“section 25-5” deduction is

not available in certain situations such as for capital expenditure. Additionally,

“section 8-1

(2)” explains that deduction is not provided under general limbs for expenditures that are

capital or capital in nature.

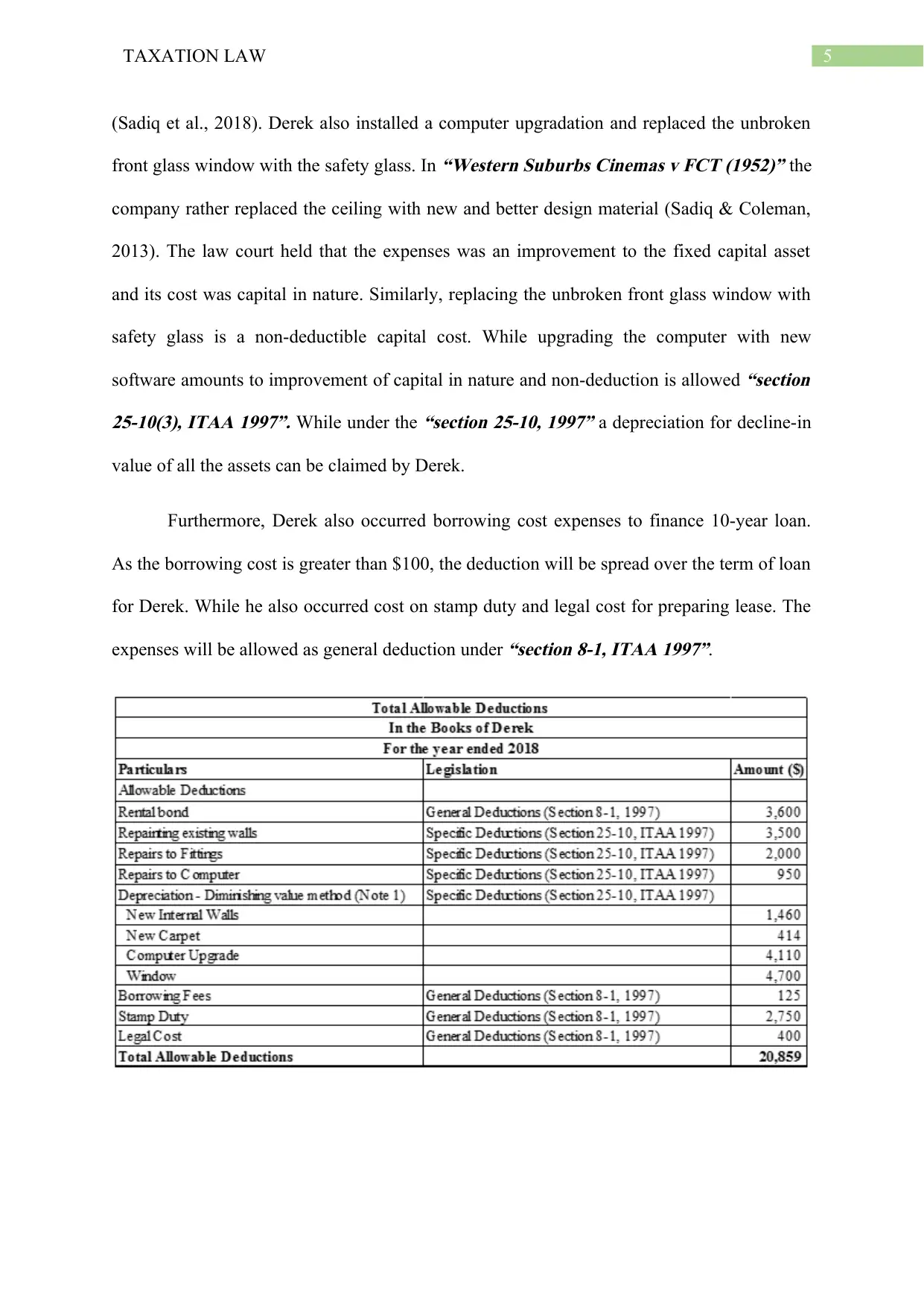

During the year Derek installed a new internal wall during August 2017. He also

repainted the current walls and laid down new carpet all through the year. Referring to

“section 25-10(3), ITAA 1997” the installation of new internal wall, repainting of current

wall and laying down of carpet is not permitted for deduction since it is a capital expenditure

5TAXATION LAW

(Sadiq et al., 2018). Derek also installed a computer upgradation and replaced the unbroken

front glass window with the safety glass. In

“Western Suburbs Cinemas v FCT (1952)” the

company rather replaced the ceiling with new and better design material (Sadiq & Coleman,

2013). The law court held that the expenses was an improvement to the fixed capital asset

and its cost was capital in nature. Similarly, replacing the unbroken front glass window with

safety glass is a non-deductible capital cost. While upgrading the computer with new

software amounts to improvement of capital in nature and non-deduction is allowed

“section

25-10(3), ITAA 1997”. While under the

“section 25-10, 1997” a depreciation for decline-in

value of all the assets can be claimed by Derek.

Furthermore, Derek also occurred borrowing cost expenses to finance 10-year loan.

As the borrowing cost is greater than $100, the deduction will be spread over the term of loan

for Derek. While he also occurred cost on stamp duty and legal cost for preparing lease. The

expenses will be allowed as general deduction under

“section 8-1, ITAA 1997”.

(Sadiq et al., 2018). Derek also installed a computer upgradation and replaced the unbroken

front glass window with the safety glass. In

“Western Suburbs Cinemas v FCT (1952)” the

company rather replaced the ceiling with new and better design material (Sadiq & Coleman,

2013). The law court held that the expenses was an improvement to the fixed capital asset

and its cost was capital in nature. Similarly, replacing the unbroken front glass window with

safety glass is a non-deductible capital cost. While upgrading the computer with new

software amounts to improvement of capital in nature and non-deduction is allowed

“section

25-10(3), ITAA 1997”. While under the

“section 25-10, 1997” a depreciation for decline-in

value of all the assets can be claimed by Derek.

Furthermore, Derek also occurred borrowing cost expenses to finance 10-year loan.

As the borrowing cost is greater than $100, the deduction will be spread over the term of loan

for Derek. While he also occurred cost on stamp duty and legal cost for preparing lease. The

expenses will be allowed as general deduction under

“section 8-1, ITAA 1997”.

6TAXATION LAW

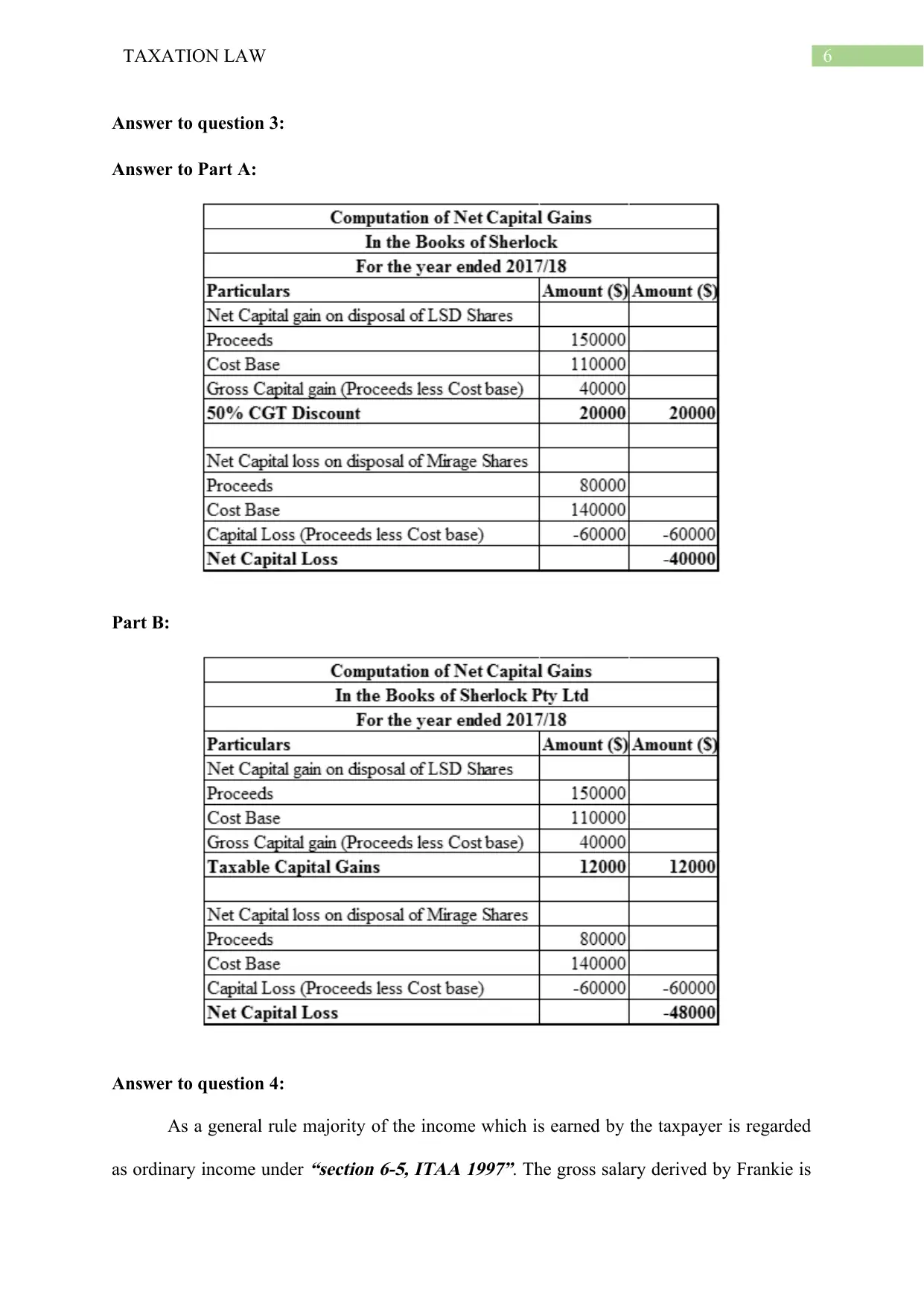

Answer to question 3:

Answer to Part A:

Part B:

Answer to question 4:

As a general rule majority of the income which is earned by the taxpayer is regarded

as ordinary income under

“section 6-5, ITAA 1997”. The gross salary derived by Frankie is

Answer to question 3:

Answer to Part A:

Part B:

Answer to question 4:

As a general rule majority of the income which is earned by the taxpayer is regarded

as ordinary income under

“section 6-5, ITAA 1997”. The gross salary derived by Frankie is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

held as ordinary income under

“section 6-5, ITAA 1997”. A simple windfall gains cannot be

treated as having the character of income. Frankie also reported receipts of $1,200,000 and

amateur prize from baseball team of $500. The amount represents windfall gain and it is not

an income. Dividends are considered taxable under

“section 44 (1), ITAA 1936”. The

dividend received by Frankie from shares are considered as statutory income while the

franking credit attached with the dividends is taxable as statutory income under

“section

207-20(1), ITAA 1997”.

Frankie also reported income from sole trader business. The court in

“Henderson v

FCT (1970)” held that only one method is appropriate for any one of income (Woellner et

al., 2018). Cash basis is appropriate for business income that is derived from provision of

knowledge while for trading or manufacturing business the accrual basis is generally

considered appropriate. For Frankie the cash basis method has been followed.

Answer to question 5:

Article 1: Call to scrap not reform the tax on luxury car:

Relevant facts in the article:

The Morrison government is currently facing renewal calls of abolishing the tax hit on

the luxury cars since it employs its effort to expand the refunds for the tourism business and

farmers.

Concise explanation of tax concepts:

The treasury is planning to extend the scheme for refund for the primary producers

and the operators of tourism business in order to save $10,000 in purchase of luxury car

(Australian Financial Review, 2019). The policy would only be applicable on all wheel drive

vehicles that are purchased following July 1 by the GST registered operators.

held as ordinary income under

“section 6-5, ITAA 1997”. A simple windfall gains cannot be

treated as having the character of income. Frankie also reported receipts of $1,200,000 and

amateur prize from baseball team of $500. The amount represents windfall gain and it is not

an income. Dividends are considered taxable under

“section 44 (1), ITAA 1936”. The

dividend received by Frankie from shares are considered as statutory income while the

franking credit attached with the dividends is taxable as statutory income under

“section

207-20(1), ITAA 1997”.

Frankie also reported income from sole trader business. The court in

“Henderson v

FCT (1970)” held that only one method is appropriate for any one of income (Woellner et

al., 2018). Cash basis is appropriate for business income that is derived from provision of

knowledge while for trading or manufacturing business the accrual basis is generally

considered appropriate. For Frankie the cash basis method has been followed.

Answer to question 5:

Article 1: Call to scrap not reform the tax on luxury car:

Relevant facts in the article:

The Morrison government is currently facing renewal calls of abolishing the tax hit on

the luxury cars since it employs its effort to expand the refunds for the tourism business and

farmers.

Concise explanation of tax concepts:

The treasury is planning to extend the scheme for refund for the primary producers

and the operators of tourism business in order to save $10,000 in purchase of luxury car

(Australian Financial Review, 2019). The policy would only be applicable on all wheel drive

vehicles that are purchased following July 1 by the GST registered operators.

8TAXATION LAW

Connection between concepts discussed and good tax policy indicators:

The plan should be considered as good tax policy because it would reduce the tax

revenue by around $11 million for the estimated period and the tax receipts for luxury car

would fall by 7.9%.

Article 2: Policy nudge could swap stamp duty for land tax:

Relevant facts in the article:

A proposal has been made to abolish the stamp duty by making use of credit for

recent property purchasers and bringing forward the land tax through the small tax holiday

period.

Concise explanation of tax concepts:

The change may be bought forward through a set of policy incentives and it may be

worth of $170 billion to the economy (Australian Financial Review, 2019). Replacing the

stamp duty with the land tax is a sensible reformation.

Connection between concepts discussed and good tax policy indicators:

This transition would have a limited option of opting-out by the new purchasers and

simultaneously the loss of revenue can be temporarily funded by the higher amount of land

tax rate.

Connection between concepts discussed and good tax policy indicators:

The plan should be considered as good tax policy because it would reduce the tax

revenue by around $11 million for the estimated period and the tax receipts for luxury car

would fall by 7.9%.

Article 2: Policy nudge could swap stamp duty for land tax:

Relevant facts in the article:

A proposal has been made to abolish the stamp duty by making use of credit for

recent property purchasers and bringing forward the land tax through the small tax holiday

period.

Concise explanation of tax concepts:

The change may be bought forward through a set of policy incentives and it may be

worth of $170 billion to the economy (Australian Financial Review, 2019). Replacing the

stamp duty with the land tax is a sensible reformation.

Connection between concepts discussed and good tax policy indicators:

This transition would have a limited option of opting-out by the new purchasers and

simultaneously the loss of revenue can be temporarily funded by the higher amount of land

tax rate.

9TAXATION LAW

References:

Australian Financial Review. (2019). Call to scrap not reform the luxury car tax. Retrieved 7

August 2019, from https://www.afr.com/policy/tax-and-super/call-to-scrap-not-

reform-the-luxury-car-tax-20190805-p52dzk

Australian Financial Review. (2019). Policy nudges could swap stamp duty for land tax.

Retrieved 7 August 2019, from https://www.afr.com/policy/tax-and-super/policy-

nudges-could-swap-stamp-duty-for-land-tax-20190801-p52cze

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax.

Krever, R. (2014). Australian taxation law cases.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Nethercott, L. (2018). Australian Taxation Study Manual 2018. Other: Oxford University

Press.

Sadiq, K. (2018). Australian taxation law cases 2018. Pyrmont, NSW: Thomson Reuters.

Sadiq, K., & Coleman, C. (2013). Principles of taxation law 2013. Sydney, N.S.W.: Lawbook

Co./Thomson Reuters.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al. (2018).

Principles of taxation law.

Woellner, R., Barkoczy, S., & Murphy, S. (2018). Australian Taxation Law 2018 ebook 28e.

Melbourne: OUPANZ.

References:

Australian Financial Review. (2019). Call to scrap not reform the luxury car tax. Retrieved 7

August 2019, from https://www.afr.com/policy/tax-and-super/call-to-scrap-not-

reform-the-luxury-car-tax-20190805-p52dzk

Australian Financial Review. (2019). Policy nudges could swap stamp duty for land tax.

Retrieved 7 August 2019, from https://www.afr.com/policy/tax-and-super/policy-

nudges-could-swap-stamp-duty-for-land-tax-20190801-p52cze

Kenny, P., Blissenden, M., & Villios, S. (2018). Australian Tax.

Krever, R. (2014). Australian taxation law cases.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Nethercott, L. (2018). Australian Taxation Study Manual 2018. Other: Oxford University

Press.

Sadiq, K. (2018). Australian taxation law cases 2018. Pyrmont, NSW: Thomson Reuters.

Sadiq, K., & Coleman, C. (2013). Principles of taxation law 2013. Sydney, N.S.W.: Lawbook

Co./Thomson Reuters.

Sadiq, K., Coleman, C., Hanegbi, R., Jogarajan, S., Krever, R., & Obst, W. et al. (2018).

Principles of taxation law.

Woellner, R., Barkoczy, S., & Murphy, S. (2018). Australian Taxation Law 2018 ebook 28e.

Melbourne: OUPANZ.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.