Taxation Law 3 Assignment: Income Tax, GST, and Partnership Analysis

VerifiedAdded on 2020/04/01

|14

|2488

|60

Homework Assignment

AI Summary

This taxation law assignment provides detailed answers to several questions. Question 1.1 examines allowable deductions for moving machinery, referencing the ITAA 1997 and relevant rulings, concluding that such costs are not deductible. Question 1.2 discusses asset revaluation based on insurance, again referencing ITAA 1997. Question 1.3 addresses legal expenditure related to business shutdown, distinguishing between deductible and non-deductible expenses. Question 2 analyzes GST and input tax credits for a bank, applying the GST Act 1999 and relevant rulings to determine the eligibility of advertising costs for input tax credits. Question 3 calculates an individual's taxable income, including foreign income and tax offsets. Finally, Question 4 computes net income from a partnership, detailing revenue, deductible expenses, and the resulting partnership income. The assignment provides a comprehensive analysis of key taxation concepts and their application.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Rule:...........................................................................................................................................5

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 2:.................................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

Table of Contents

Answer to Question 1.1:.............................................................................................................3

Issue:..........................................................................................................................................3

Rule:...........................................................................................................................................3

Application:................................................................................................................................3

Conclusion:................................................................................................................................3

Answer to question 1.2:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................4

Application:................................................................................................................................4

Answer to question 1.3:..............................................................................................................4

Issue:..........................................................................................................................................4

Rule:...........................................................................................................................................5

Application:................................................................................................................................5

Rule:...........................................................................................................................................5

Applications:..............................................................................................................................6

Conclusion:................................................................................................................................6

Answer to question 2:.................................................................................................................6

Issue:..........................................................................................................................................6

Rule:...........................................................................................................................................6

Applications:..............................................................................................................................6

2TAXATION LAW

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to question 4:...............................................................................................................10

References................................................................................................................................13

Conclusion:................................................................................................................................8

Answer to question 3:.................................................................................................................9

Answer to question 4:...............................................................................................................10

References................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to Question 1.1:

Issue:

With reference to “Section 8-1 of the ITAA”, is allowable deduction applicable for

placing machinery from one location to another.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “British Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

On applying the rulings of “Section 8-1 of the ITAA”, it has been discerned that

moving of machinery involves inflated asset value. As the activity of shifting the machinery

has taken place based on the assessable income it cannot be held liable for deductions as this

has led to increased cost of asset.

As per the findings of the case “British Insulated & Helsby Cables”, it has been

discerned that previously companies have taken advantage of moving a depreciable asset. As

per the rulings of “Taxation ruling of TD 92/126” the cost of assembling a new machinery

can be considered as a part of the revenue under cost of capital which cannot be held for

allowable deductions (Barkoczy 2016).

Conclusion:

It can be rightly said that the cost of moving the depreciable asset/machinery cannot

be taken into account for the purpose of deductions which are allowable as they are a division

of the capital.

Answer to Question 1.1:

Issue:

With reference to “Section 8-1 of the ITAA”, is allowable deduction applicable for

placing machinery from one location to another.

Rule:

I. “Section 8-1 of the ITAA 1997”

II. “British Insulated & Helsby Cables”

III. “Taxation ruling of TD 92/126”

Application:

On applying the rulings of “Section 8-1 of the ITAA”, it has been discerned that

moving of machinery involves inflated asset value. As the activity of shifting the machinery

has taken place based on the assessable income it cannot be held liable for deductions as this

has led to increased cost of asset.

As per the findings of the case “British Insulated & Helsby Cables”, it has been

discerned that previously companies have taken advantage of moving a depreciable asset. As

per the rulings of “Taxation ruling of TD 92/126” the cost of assembling a new machinery

can be considered as a part of the revenue under cost of capital which cannot be held for

allowable deductions (Barkoczy 2016).

Conclusion:

It can be rightly said that the cost of moving the depreciable asset/machinery cannot

be taken into account for the purpose of deductions which are allowable as they are a division

of the capital.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

Answer to question 1.2:

Issue:

The issue has been recognised for the consideration of asset revaluation based on the

insurance cover with reference to “Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

As per the applicability aspect of “Section 8-1 of the ITAA 1997”, it has been

discerned that any cost which is recurring in nature needs to be entitled for the allowable

nature of deductions. As for the given case the cost of the expenditure is seen to be repeating

and moreover the outer cost incurred for the fixed asset is seen to be considered as per

straight-line basis such costs depict impertinent advantages. Therefore it is important to take

into consideration the cost of asset revaluation as per “Section 8-1 of the ITAA 1997”

(Millar 2014).

Conclusion:

The given rulings under “Section 8-1 of the ITAA 1997”, shows that it is important

to consider the asset revaluation as an outcome of insurance cover.

Answer to question 1.3:

Issue:

The basic question has highlighted on the important aspect of legal expenditure

incurred in opposition to a shutting down of business activity and the same is to be

considered under permissible amount of deductions.

Answer to question 1.2:

Issue:

The issue has been recognised for the consideration of asset revaluation based on the

insurance cover with reference to “Section 8-1 of the ITAA 1997”.

Rule:

I. “Section 8-1 of ITAA 1997”

Application:

As per the applicability aspect of “Section 8-1 of the ITAA 1997”, it has been

discerned that any cost which is recurring in nature needs to be entitled for the allowable

nature of deductions. As for the given case the cost of the expenditure is seen to be repeating

and moreover the outer cost incurred for the fixed asset is seen to be considered as per

straight-line basis such costs depict impertinent advantages. Therefore it is important to take

into consideration the cost of asset revaluation as per “Section 8-1 of the ITAA 1997”

(Millar 2014).

Conclusion:

The given rulings under “Section 8-1 of the ITAA 1997”, shows that it is important

to consider the asset revaluation as an outcome of insurance cover.

Answer to question 1.3:

Issue:

The basic question has highlighted on the important aspect of legal expenditure

incurred in opposition to a shutting down of business activity and the same is to be

considered under permissible amount of deductions.

5TAXATION LAW

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

As per the inference made from “Section 8-1 of the ITAA 1997”, the legal

expenditure which has been identified with shutting down of business cannot be held under

permissible nature of deductions. As per “Taxation ruling of ID 2004/367” the legal

expenditure cost which is proposed to carry out any business operation then only can be held

for permissible deductions. However, as the expense is a result of ordinary course of business

it cannot be treated under permissible deductions (Australian Trade Commission 2015).

In a similar case of “FC of T v Snowden and Wilson Pty Ltd (1958)”, the

expenses are borne as a result from ordinary course of business which prevented it from

consideration from allowable deductions (Australian Government 2015).

Based on the given situation shutdown of business may be qualifying under the

positive limbs but as the expenses are aligned with business structure it is having

characteristics nature of capital henceforth cannot be considered for deductions.

Conclusion:

The study shows how the expenses which are depicting capital characteristics of

business activities cannot be considered for deductions as per “Section 8-1 of the ITAA

1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

Rule:

I. “FC of T v Snowden and Wilson Pty Ltd (1958)”

II. “Section 8-1 of the ITAA 1997”

Application:

As per the inference made from “Section 8-1 of the ITAA 1997”, the legal

expenditure which has been identified with shutting down of business cannot be held under

permissible nature of deductions. As per “Taxation ruling of ID 2004/367” the legal

expenditure cost which is proposed to carry out any business operation then only can be held

for permissible deductions. However, as the expense is a result of ordinary course of business

it cannot be treated under permissible deductions (Australian Trade Commission 2015).

In a similar case of “FC of T v Snowden and Wilson Pty Ltd (1958)”, the

expenses are borne as a result from ordinary course of business which prevented it from

consideration from allowable deductions (Australian Government 2015).

Based on the given situation shutdown of business may be qualifying under the

positive limbs but as the expenses are aligned with business structure it is having

characteristics nature of capital henceforth cannot be considered for deductions.

Conclusion:

The study shows how the expenses which are depicting capital characteristics of

business activities cannot be considered for deductions as per “Section 8-1 of the ITAA

1997”.

Rule:

I. “Section 8-1 of the ITAA 1997”

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Applications:

The depiction is made from “Section 8-1 of the ITAA 1997”, has been able to

demonstrate that legal outlay with characteristic features of capital cannot be held under non-

deductible income. The trading activities should be taken into consideration based on the

parameter of allowable deduction as it should be noted that the legal expenditure is directly

associated to the revenue producing aspect. By consideration of the given situation, it needs

to be noted that the cost born for solicitor services are duly considered for deductions as per

“Section 8-1 of the ITAA 1997” (Australian Taxation Office 2015).

Conclusion:

The different types of legal expenditure as a result of revenue generating criteria

allow for the deductions with the rulings of “Section 8-1 of the ITAA 1997”.

Answer to question 2:

Issue:

The important concern is related to “GST Act 1999” and to discern that the taxpayer needs to

determine the “Input Tax Credit (ITC)” for the GST supplies.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

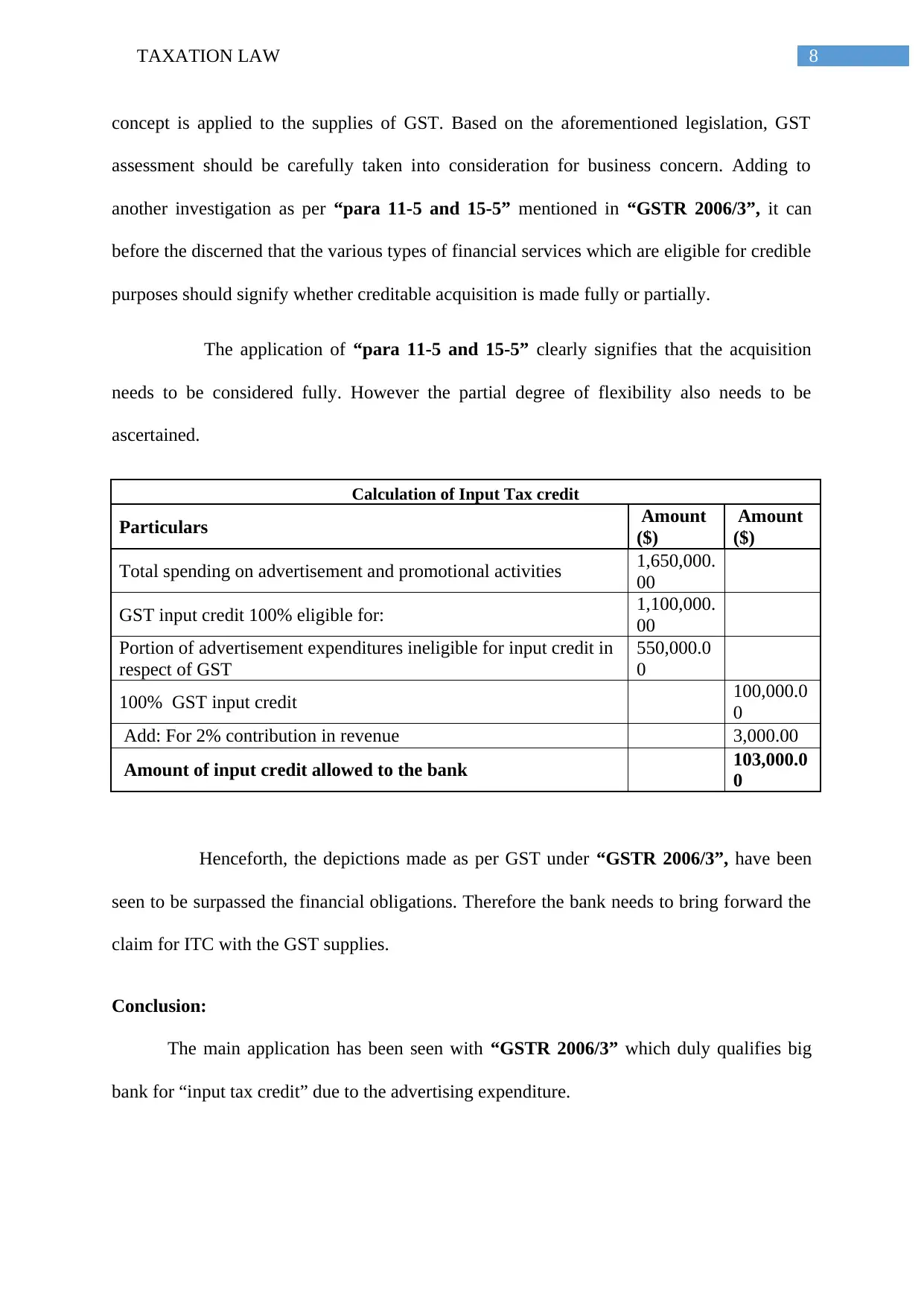

Applications:

The main form of the GST supplies for the Big Bank has been duly noted with the

advertising cost. The consideration of ITC as per “Chapter 2 of the GST Act 1999”, shows

that any expense which has been incurred the normal business function should be inclusive of

Applications:

The depiction is made from “Section 8-1 of the ITAA 1997”, has been able to

demonstrate that legal outlay with characteristic features of capital cannot be held under non-

deductible income. The trading activities should be taken into consideration based on the

parameter of allowable deduction as it should be noted that the legal expenditure is directly

associated to the revenue producing aspect. By consideration of the given situation, it needs

to be noted that the cost born for solicitor services are duly considered for deductions as per

“Section 8-1 of the ITAA 1997” (Australian Taxation Office 2015).

Conclusion:

The different types of legal expenditure as a result of revenue generating criteria

allow for the deductions with the rulings of “Section 8-1 of the ITAA 1997”.

Answer to question 2:

Issue:

The important concern is related to “GST Act 1999” and to discern that the taxpayer needs to

determine the “Input Tax Credit (ITC)” for the GST supplies.

Rule:

I. “Ronpibon Tin NL v FC of T”

II. “Goods and Service Taxation Ruling of GSTR 2006/3”

III. “GST Act 1999”

Applications:

The main form of the GST supplies for the Big Bank has been duly noted with the

advertising cost. The consideration of ITC as per “Chapter 2 of the GST Act 1999”, shows

that any expense which has been incurred the normal business function should be inclusive of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

ITC. However, the claim for a city needs to be added up with the GST amount. The bank has

been recognised to provide its financial services in more than 50 branches throughout the

country. There have been several programs for insurance and home content apart from the

credit facilities. Henceforth, the various types of ITC have been considered under the rulings

of “Taxation Ruling of GSTR 2006/3”.

The consideration is made from “division 11-15 and 129 of the GST Act

1999”, has been further able to highlight on the acquisitions as per previous rulings. The

important applications of taxation ruling have been recognised with “GSTR 2006/3” which

depicts the benchmark on the acquisition limit associated to the acquisitions of ITC or “lower

input tax credit”.

In the given situation of the bank, it can be stated that the expenses has been

mainly incurred as a result of advertising cost and that has been already clubbed with GST

amount. Therefore, the present question needs to ensure whether the issue is able to comply

with “GSTR 2006/3”. By the rulings of “GSTR 2006/3”, it has been discerned that Big

Bank has duly met the criteria for ITC. As per the various types of depictions from “GSTR

2006/3”, it has been inferred that any registration of having commercial significance needs to

be recognised under “GST Act 1999”, for the payment of GST amount based on the financial

requirements (Besley and PerssonT 2013).

It has been for the discerned from the “GSTR 2006/3”, that the commercial activity

can be directly claimed for ITC as it has been associated to the GST amount for financial

supplies. On the other hand, commercial entity is seen to be related to claimable amount of

ITC. However, only a certain portion of the entity is claimable (ATO 2015).

As for the application of the case “Ronpibon Tin NL v FC of T”, significant criteria

as per the rulings of “GSTR 2006/3” for the GST depicts that “extent” and “to the extent”

ITC. However, the claim for a city needs to be added up with the GST amount. The bank has

been recognised to provide its financial services in more than 50 branches throughout the

country. There have been several programs for insurance and home content apart from the

credit facilities. Henceforth, the various types of ITC have been considered under the rulings

of “Taxation Ruling of GSTR 2006/3”.

The consideration is made from “division 11-15 and 129 of the GST Act

1999”, has been further able to highlight on the acquisitions as per previous rulings. The

important applications of taxation ruling have been recognised with “GSTR 2006/3” which

depicts the benchmark on the acquisition limit associated to the acquisitions of ITC or “lower

input tax credit”.

In the given situation of the bank, it can be stated that the expenses has been

mainly incurred as a result of advertising cost and that has been already clubbed with GST

amount. Therefore, the present question needs to ensure whether the issue is able to comply

with “GSTR 2006/3”. By the rulings of “GSTR 2006/3”, it has been discerned that Big

Bank has duly met the criteria for ITC. As per the various types of depictions from “GSTR

2006/3”, it has been inferred that any registration of having commercial significance needs to

be recognised under “GST Act 1999”, for the payment of GST amount based on the financial

requirements (Besley and PerssonT 2013).

It has been for the discerned from the “GSTR 2006/3”, that the commercial activity

can be directly claimed for ITC as it has been associated to the GST amount for financial

supplies. On the other hand, commercial entity is seen to be related to claimable amount of

ITC. However, only a certain portion of the entity is claimable (ATO 2015).

As for the application of the case “Ronpibon Tin NL v FC of T”, significant criteria

as per the rulings of “GSTR 2006/3” for the GST depicts that “extent” and “to the extent”

8TAXATION LAW

concept is applied to the supplies of GST. Based on the aforementioned legislation, GST

assessment should be carefully taken into consideration for business concern. Adding to

another investigation as per “para 11-5 and 15-5” mentioned in “GSTR 2006/3”, it can

before the discerned that the various types of financial services which are eligible for credible

purposes should signify whether creditable acquisition is made fully or partially.

The application of “para 11-5 and 15-5” clearly signifies that the acquisition

needs to be considered fully. However the partial degree of flexibility also needs to be

ascertained.

Calculation of Input Tax credit

Particulars Amount

($)

Amount

($)

Total spending on advertisement and promotional activities 1,650,000.

00

GST input credit 100% eligible for: 1,100,000.

00

Portion of advertisement expenditures ineligible for input credit in

respect of GST

550,000.0

0

100% GST input credit 100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.0

0

Henceforth, the depictions made as per GST under “GSTR 2006/3”, have been

seen to be surpassed the financial obligations. Therefore the bank needs to bring forward the

claim for ITC with the GST supplies.

Conclusion:

The main application has been seen with “GSTR 2006/3” which duly qualifies big

bank for “input tax credit” due to the advertising expenditure.

concept is applied to the supplies of GST. Based on the aforementioned legislation, GST

assessment should be carefully taken into consideration for business concern. Adding to

another investigation as per “para 11-5 and 15-5” mentioned in “GSTR 2006/3”, it can

before the discerned that the various types of financial services which are eligible for credible

purposes should signify whether creditable acquisition is made fully or partially.

The application of “para 11-5 and 15-5” clearly signifies that the acquisition

needs to be considered fully. However the partial degree of flexibility also needs to be

ascertained.

Calculation of Input Tax credit

Particulars Amount

($)

Amount

($)

Total spending on advertisement and promotional activities 1,650,000.

00

GST input credit 100% eligible for: 1,100,000.

00

Portion of advertisement expenditures ineligible for input credit in

respect of GST

550,000.0

0

100% GST input credit 100,000.0

0

Add: For 2% contribution in revenue 3,000.00

Amount of input credit allowed to the bank 103,000.0

0

Henceforth, the depictions made as per GST under “GSTR 2006/3”, have been

seen to be surpassed the financial obligations. Therefore the bank needs to bring forward the

claim for ITC with the GST supplies.

Conclusion:

The main application has been seen with “GSTR 2006/3” which duly qualifies big

bank for “input tax credit” due to the advertising expenditure.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

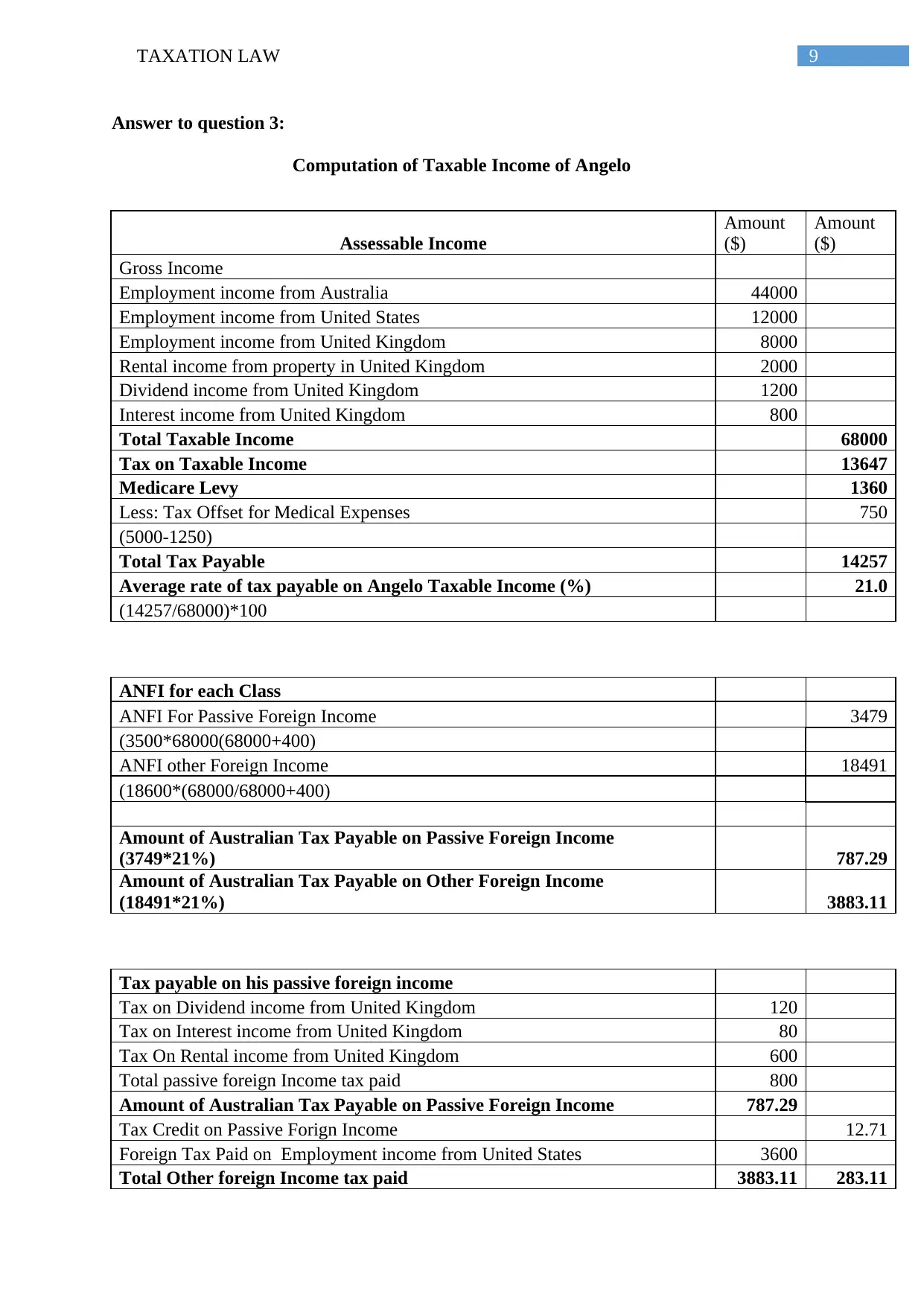

Answer to question 3:

Computation of Taxable Income of Angelo

Assessable Income

Amount

($)

Amount

($)

Gross Income

Employment income from Australia 44000

Employment income from United States 12000

Employment income from United Kingdom 8000

Rental income from property in United Kingdom 2000

Dividend income from United Kingdom 1200

Interest income from United Kingdom 800

Total Taxable Income 68000

Tax on Taxable Income 13647

Medicare Levy 1360

Less: Tax Offset for Medical Expenses 750

(5000-1250)

Total Tax Payable 14257

Average rate of tax payable on Angelo Taxable Income (%) 21.0

(14257/68000)*100

ANFI for each Class

ANFI For Passive Foreign Income 3479

(3500*68000(68000+400)

ANFI other Foreign Income 18491

(18600*(68000/68000+400)

Amount of Australian Tax Payable on Passive Foreign Income

(3749*21%) 787.29

Amount of Australian Tax Payable on Other Foreign Income

(18491*21%) 3883.11

Tax payable on his passive foreign income

Tax on Dividend income from United Kingdom 120

Tax on Interest income from United Kingdom 80

Tax On Rental income from United Kingdom 600

Total passive foreign Income tax paid 800

Amount of Australian Tax Payable on Passive Foreign Income 787.29

Tax Credit on Passive Forign Income 12.71

Foreign Tax Paid on Employment income from United States 3600

Total Other foreign Income tax paid 3883.11 283.11

Answer to question 3:

Computation of Taxable Income of Angelo

Assessable Income

Amount

($)

Amount

($)

Gross Income

Employment income from Australia 44000

Employment income from United States 12000

Employment income from United Kingdom 8000

Rental income from property in United Kingdom 2000

Dividend income from United Kingdom 1200

Interest income from United Kingdom 800

Total Taxable Income 68000

Tax on Taxable Income 13647

Medicare Levy 1360

Less: Tax Offset for Medical Expenses 750

(5000-1250)

Total Tax Payable 14257

Average rate of tax payable on Angelo Taxable Income (%) 21.0

(14257/68000)*100

ANFI for each Class

ANFI For Passive Foreign Income 3479

(3500*68000(68000+400)

ANFI other Foreign Income 18491

(18600*(68000/68000+400)

Amount of Australian Tax Payable on Passive Foreign Income

(3749*21%) 787.29

Amount of Australian Tax Payable on Other Foreign Income

(18491*21%) 3883.11

Tax payable on his passive foreign income

Tax on Dividend income from United Kingdom 120

Tax on Interest income from United Kingdom 80

Tax On Rental income from United Kingdom 600

Total passive foreign Income tax paid 800

Amount of Australian Tax Payable on Passive Foreign Income 787.29

Tax Credit on Passive Forign Income 12.71

Foreign Tax Paid on Employment income from United States 3600

Total Other foreign Income tax paid 3883.11 283.11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

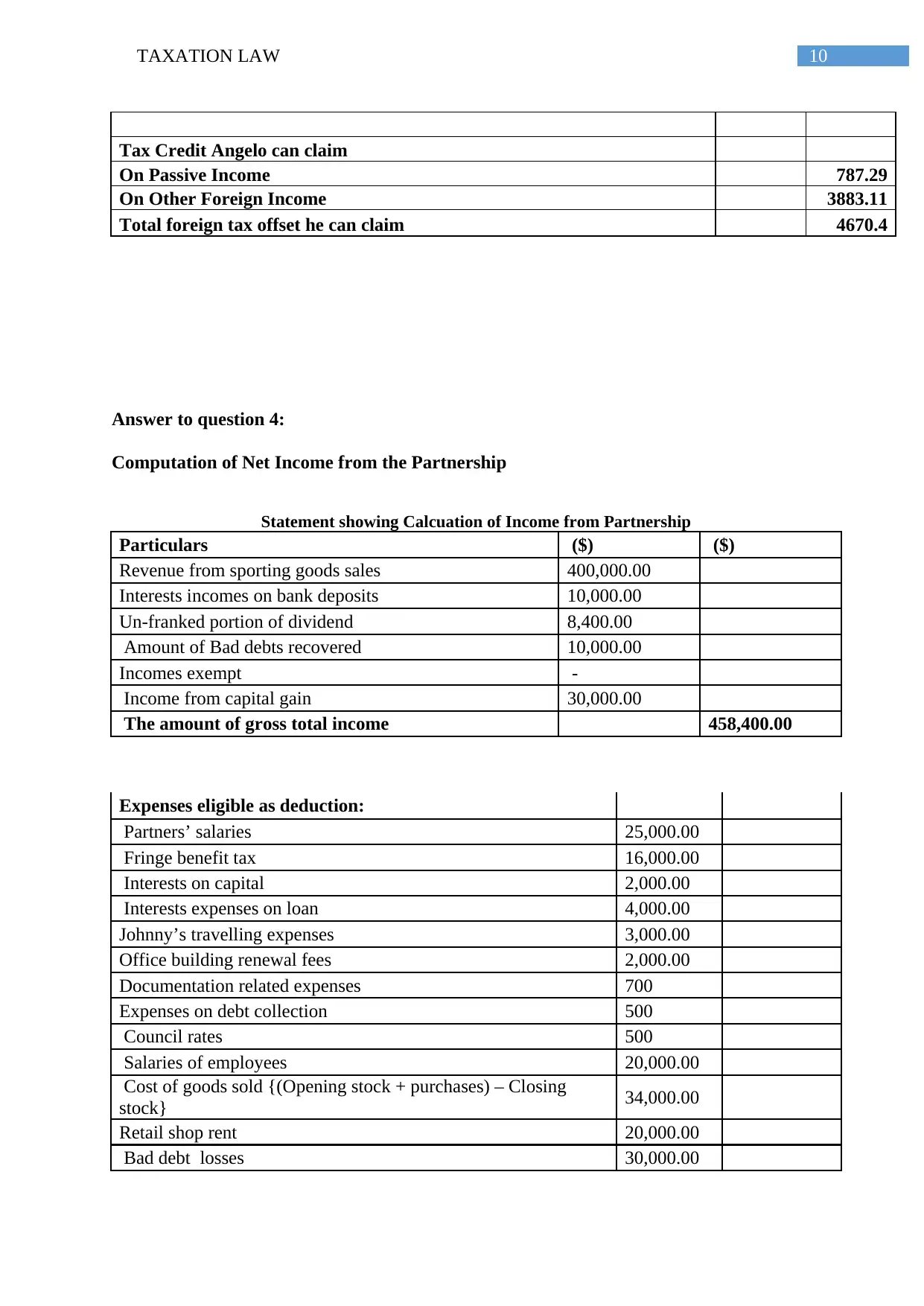

Tax Credit Angelo can claim

On Passive Income 787.29

On Other Foreign Income 3883.11

Total foreign tax offset he can claim 4670.4

Answer to question 4:

Computation of Net Income from the Partnership

Statement showing Calcuation of Income from Partnership

Particulars ($) ($)

Revenue from sporting goods sales 400,000.00

Interests incomes on bank deposits 10,000.00

Un-franked portion of dividend 8,400.00

Amount of Bad debts recovered 10,000.00

Incomes exempt -

Income from capital gain 30,000.00

The amount of gross total income 458,400.00

Expenses eligible as deduction:

Partners’ salaries 25,000.00

Fringe benefit tax 16,000.00

Interests on capital 2,000.00

Interests expenses on loan 4,000.00

Johnny’s travelling expenses 3,000.00

Office building renewal fees 2,000.00

Documentation related expenses 700

Expenses on debt collection 500

Council rates 500

Salaries of employees 20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock} 34,000.00

Retail shop rent 20,000.00

Bad debt losses 30,000.00

Tax Credit Angelo can claim

On Passive Income 787.29

On Other Foreign Income 3883.11

Total foreign tax offset he can claim 4670.4

Answer to question 4:

Computation of Net Income from the Partnership

Statement showing Calcuation of Income from Partnership

Particulars ($) ($)

Revenue from sporting goods sales 400,000.00

Interests incomes on bank deposits 10,000.00

Un-franked portion of dividend 8,400.00

Amount of Bad debts recovered 10,000.00

Incomes exempt -

Income from capital gain 30,000.00

The amount of gross total income 458,400.00

Expenses eligible as deduction:

Partners’ salaries 25,000.00

Fringe benefit tax 16,000.00

Interests on capital 2,000.00

Interests expenses on loan 4,000.00

Johnny’s travelling expenses 3,000.00

Office building renewal fees 2,000.00

Documentation related expenses 700

Expenses on debt collection 500

Council rates 500

Salaries of employees 20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock} 34,000.00

Retail shop rent 20,000.00

Bad debt losses 30,000.00

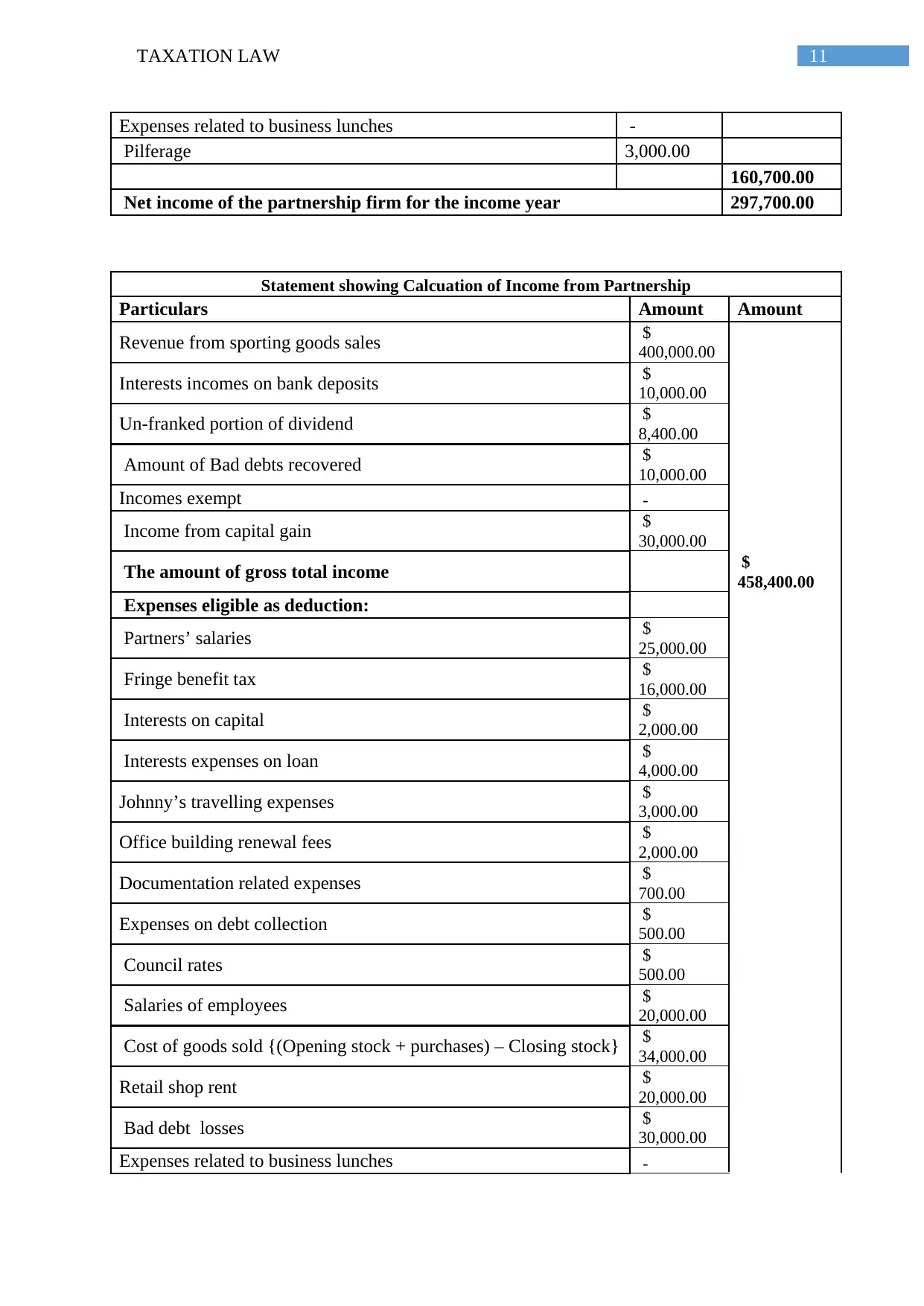

11TAXATION LAW

Expenses related to business lunches -

Pilferage 3,000.00

160,700.00

Net income of the partnership firm for the income year 297,700.00

Statement showing Calcuation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $

400,000.00

Interests incomes on bank deposits $

10,000.00

Un-franked portion of dividend $

8,400.00

Amount of Bad debts recovered $

10,000.00

Incomes exempt -

Income from capital gain $

30,000.00

The amount of gross total income $

458,400.00

Expenses eligible as deduction:

Partners’ salaries $

25,000.00

Fringe benefit tax $

16,000.00

Interests on capital $

2,000.00

Interests expenses on loan $

4,000.00

Johnny’s travelling expenses $

3,000.00

Office building renewal fees $

2,000.00

Documentation related expenses $

700.00

Expenses on debt collection $

500.00

Council rates $

500.00

Salaries of employees $

20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing stock} $

34,000.00

Retail shop rent $

20,000.00

Bad debt losses $

30,000.00

Expenses related to business lunches -

Expenses related to business lunches -

Pilferage 3,000.00

160,700.00

Net income of the partnership firm for the income year 297,700.00

Statement showing Calcuation of Income from Partnership

Particulars Amount Amount

Revenue from sporting goods sales $

400,000.00

Interests incomes on bank deposits $

10,000.00

Un-franked portion of dividend $

8,400.00

Amount of Bad debts recovered $

10,000.00

Incomes exempt -

Income from capital gain $

30,000.00

The amount of gross total income $

458,400.00

Expenses eligible as deduction:

Partners’ salaries $

25,000.00

Fringe benefit tax $

16,000.00

Interests on capital $

2,000.00

Interests expenses on loan $

4,000.00

Johnny’s travelling expenses $

3,000.00

Office building renewal fees $

2,000.00

Documentation related expenses $

700.00

Expenses on debt collection $

500.00

Council rates $

500.00

Salaries of employees $

20,000.00

Cost of goods sold {(Opening stock + purchases) – Closing stock} $

34,000.00

Retail shop rent $

20,000.00

Bad debt losses $

30,000.00

Expenses related to business lunches -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.