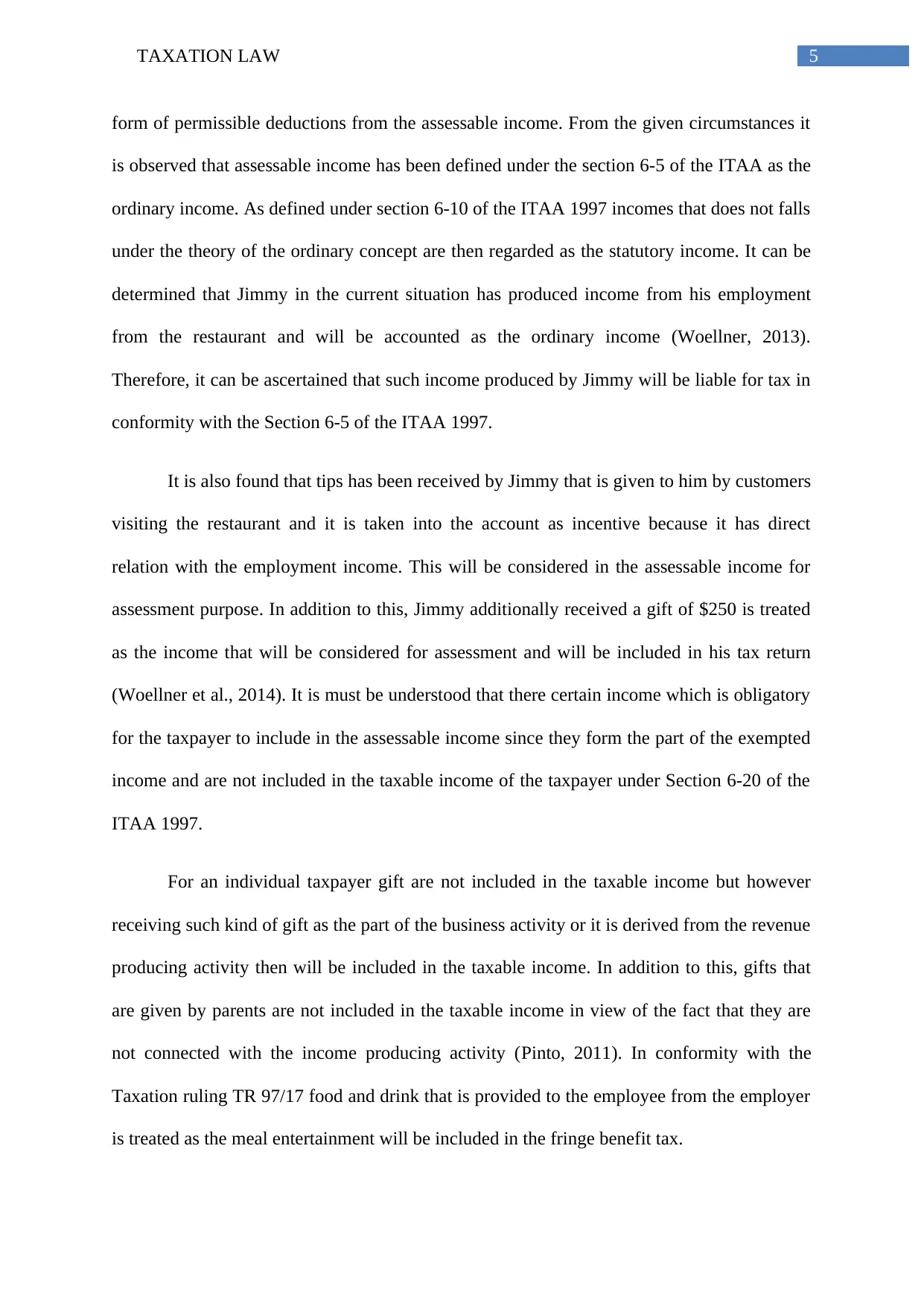

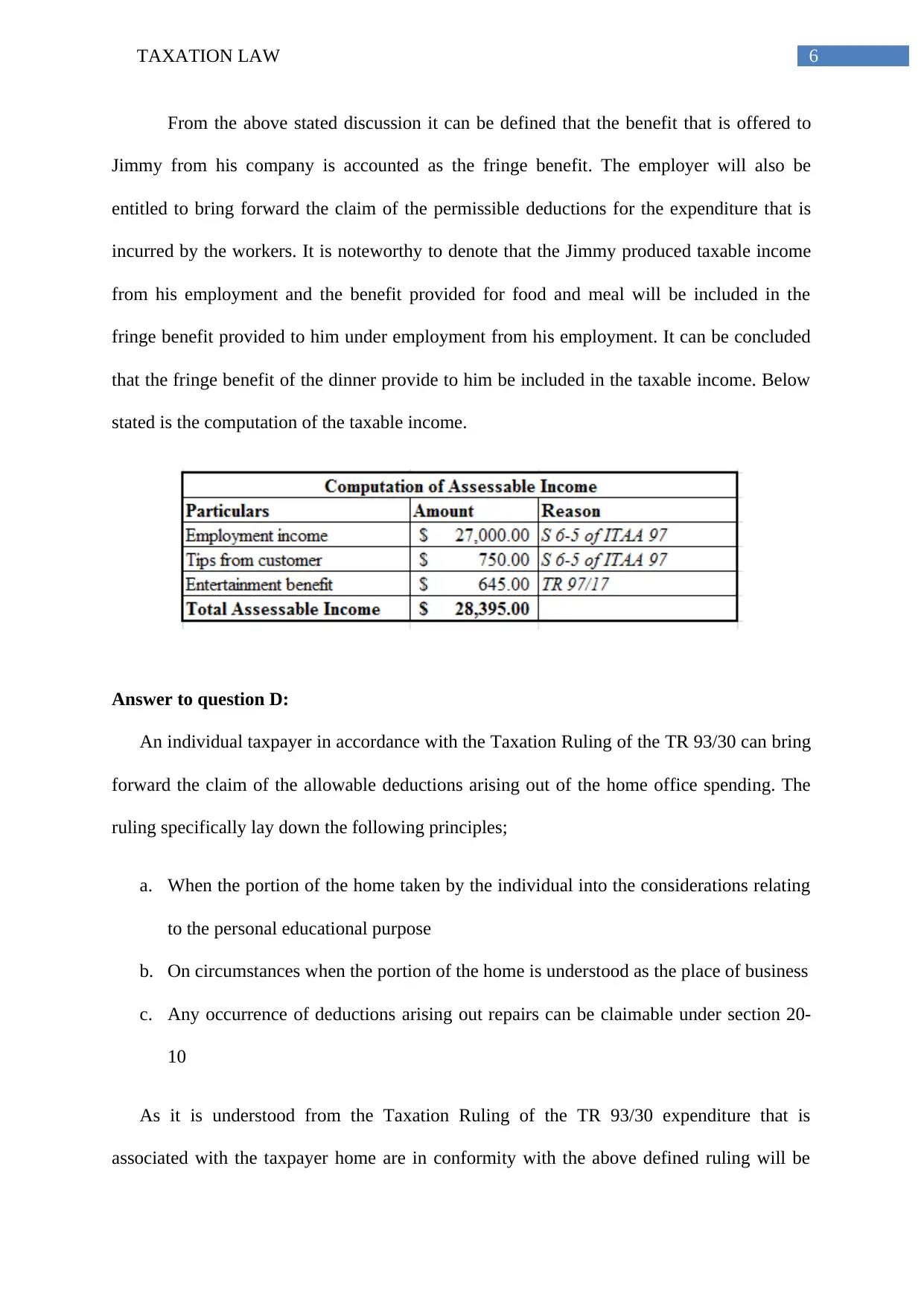

The Australian Taxation Act (1997) defines an individual as a resident of Australia if they have been present in the country for at least 183 days, or if they are enrolled in an Australian university for a course that lasts more than six months. Additionally, superannuation tests can also determine residency status. In the case of Tina, it is concluded that she will be treated as a resident of Australia under section 995-1 of the ITAA 1997. For Jimmy, his assessable income from his employment at the restaurant is considered ordinary income and will be subject to taxation. Tips received by Jimmy are also considered incentive payments and will be included in his assessable income. Jimmy's gift of $250 is treated as an income that must be included in his tax return. The assignment also discusses fringe benefits, including meals provided to employees, which can be claimed as deductions by the employer.

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)