Taxation Law: Assessable Income and Capital Gains Analysis Assignment

VerifiedAdded on 2022/08/26

|11

|2883

|16

Homework Assignment

AI Summary

This taxation law assignment provides a comprehensive analysis of assessable income and capital gains, referencing relevant legislation and case law. The assignment addresses two key questions. Question 1 examines Emmi's assessable income, including tips, employment income, gifts, and fringe benefits, determining the tax implications of each. Question 2 delves into capital gains tax (CGT), analyzing the tax treatment of assets sold by Liu, including her main residence (pre-CGT asset), a personal use car, assets related to a small business enterprise, furniture, and collectables. The assignment applies relevant sections of the Income Tax Assessment Act 1997 (ITAA 1997) and the Fringe Benefits Tax Assessment Act 1986 (FBTAA 1986), providing detailed explanations and calculations to determine the tax liabilities and exemptions for both Emmi and Liu. The analysis includes discussions on ordinary income, CGT events, personal use assets, small business CGT concessions, and the specific rules governing collectables.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer A:..................................................................................................................................5

Answer B:...................................................................................................................................6

Answer C:...................................................................................................................................6

Answer D:..................................................................................................................................7

Answer E:...................................................................................................................................8

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................5

Answer A:..................................................................................................................................5

Answer B:...................................................................................................................................6

Answer C:...................................................................................................................................6

Answer D:..................................................................................................................................7

Answer E:...................................................................................................................................8

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

Issues:

The case study will take into the consideration the issues arising from the receipt that

is derived by the taxpayer from employment amounts to income under the ordinary concepts

of “section 6-5 ITA Act 97”.

Rule:

Ordinary income is regarded as income in agreement with the ordinary concepts and it

is considered taxable under “sec 6-5 ITA Act 97”. Gains usually needs the characterization

by courts in order to be held as income (Bankman et al. 2017). On noticing that the taxpayer

gets the voluntary payment as the reward for service are held as ordinary income since it

constitute benefit from employment. The decision made in “Penn v Speirs & Pond Ltd

(1908)” tips is viewed as third party gift and it is a voluntary payment because it is earned

from the extent of service that is rendered by a taxpayer (Schenk 2017). It establishes a

required relation among the service rendered and making it as a taxable ordinary earnings.

When a person earns wages, salaries, commissions, bonuses, fees for the services and

other types of payment which is considered incidental to the employment are held as reward

for service and amounts ordinary income (Schmalbeck, Zelenak and Lawsky 2015). The

court in “British Columbia v Ostrum (1904)” explained that a receipt that is generated from

employment or the service given is regarded as income.

Personal gifts, opposite to other forms of voluntary payment that are viewed

incidental to service or employment rendered are not regarded as income. It is necessary that

a difference should be made among the gratuitous payment and voluntary payment given to

someone on personal groups and one that is incidental to a specific income producing activity

Answer to question 1:

Issues:

The case study will take into the consideration the issues arising from the receipt that

is derived by the taxpayer from employment amounts to income under the ordinary concepts

of “section 6-5 ITA Act 97”.

Rule:

Ordinary income is regarded as income in agreement with the ordinary concepts and it

is considered taxable under “sec 6-5 ITA Act 97”. Gains usually needs the characterization

by courts in order to be held as income (Bankman et al. 2017). On noticing that the taxpayer

gets the voluntary payment as the reward for service are held as ordinary income since it

constitute benefit from employment. The decision made in “Penn v Speirs & Pond Ltd

(1908)” tips is viewed as third party gift and it is a voluntary payment because it is earned

from the extent of service that is rendered by a taxpayer (Schenk 2017). It establishes a

required relation among the service rendered and making it as a taxable ordinary earnings.

When a person earns wages, salaries, commissions, bonuses, fees for the services and

other types of payment which is considered incidental to the employment are held as reward

for service and amounts ordinary income (Schmalbeck, Zelenak and Lawsky 2015). The

court in “British Columbia v Ostrum (1904)” explained that a receipt that is generated from

employment or the service given is regarded as income.

Personal gifts, opposite to other forms of voluntary payment that are viewed

incidental to service or employment rendered are not regarded as income. It is necessary that

a difference should be made among the gratuitous payment and voluntary payment given to

someone on personal groups and one that is incidental to a specific income producing activity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

(Elliott 2015). As eminent in the event of “Hayes v FCT (1947)” a gift on the basis of

personal qualities cannot be viewed as ordinary earnings and such gift is not commonly held

taxable to recipient.

Employer should denote under “sec 66 (1) FBTAA 1986”, that fringe benefit tax is

paid by the employer and not by the employees. This type of tax is normally implemented on

provision of fringe benefit and not on the receipt of benefit (Hildreth 2019). The word fringe

benefit is explained in “sec 136 (1) FBTAA 1986” says that it is a benefit that is given by the

employer to employee during the year of taxation in relation to employment of an employee.

While “sec 137 FBTAA 1986” makes sure that FBT legislation is applicable in those

situations where there is an evident relation of employment is noticed however the employee

is remunerated with cash benefits rather than paying the salary (Woellner et al. 2016). In

“FCT v Indooroopily Children’s Services (2007)” a fringe benefit only happens when the

benefit that is given is related to employee.

A taxpayer should denote that when they receive any cash birthday gift or any sort of

identical amounts that is received from their family members then such amount is not

included in to the taxable income (Ausness 2017). Amounts might be held as taxable if they

receive them as the portion of business activity or in regard to the income generating activity

as employee.

Application:

During the year it is noticed that Emmi being the student of accounting is found to be

working a Melbourne restaurant on a part-time basis. As the part of her employment Emmi

has received a tips of $335 from her customers. Referring to decision made in “Penn v

Speirs & Pond Ltd (1908)” tips got be Emmi should be viewed as third party gift and it is a

voluntary payment because it is earned from the extent of service that is rendered by her

(Elliott 2015). As eminent in the event of “Hayes v FCT (1947)” a gift on the basis of

personal qualities cannot be viewed as ordinary earnings and such gift is not commonly held

taxable to recipient.

Employer should denote under “sec 66 (1) FBTAA 1986”, that fringe benefit tax is

paid by the employer and not by the employees. This type of tax is normally implemented on

provision of fringe benefit and not on the receipt of benefit (Hildreth 2019). The word fringe

benefit is explained in “sec 136 (1) FBTAA 1986” says that it is a benefit that is given by the

employer to employee during the year of taxation in relation to employment of an employee.

While “sec 137 FBTAA 1986” makes sure that FBT legislation is applicable in those

situations where there is an evident relation of employment is noticed however the employee

is remunerated with cash benefits rather than paying the salary (Woellner et al. 2016). In

“FCT v Indooroopily Children’s Services (2007)” a fringe benefit only happens when the

benefit that is given is related to employee.

A taxpayer should denote that when they receive any cash birthday gift or any sort of

identical amounts that is received from their family members then such amount is not

included in to the taxable income (Ausness 2017). Amounts might be held as taxable if they

receive them as the portion of business activity or in regard to the income generating activity

as employee.

Application:

During the year it is noticed that Emmi being the student of accounting is found to be

working a Melbourne restaurant on a part-time basis. As the part of her employment Emmi

has received a tips of $335 from her customers. Referring to decision made in “Penn v

Speirs & Pond Ltd (1908)” tips got be Emmi should be viewed as third party gift and it is a

voluntary payment because it is earned from the extent of service that is rendered by her

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

(Miller and Oats 2016). It establishes a required relation among the service rendered and

making it as a taxable ordinary earnings for Emmi under “sec 6-5 ITA Act 97”.

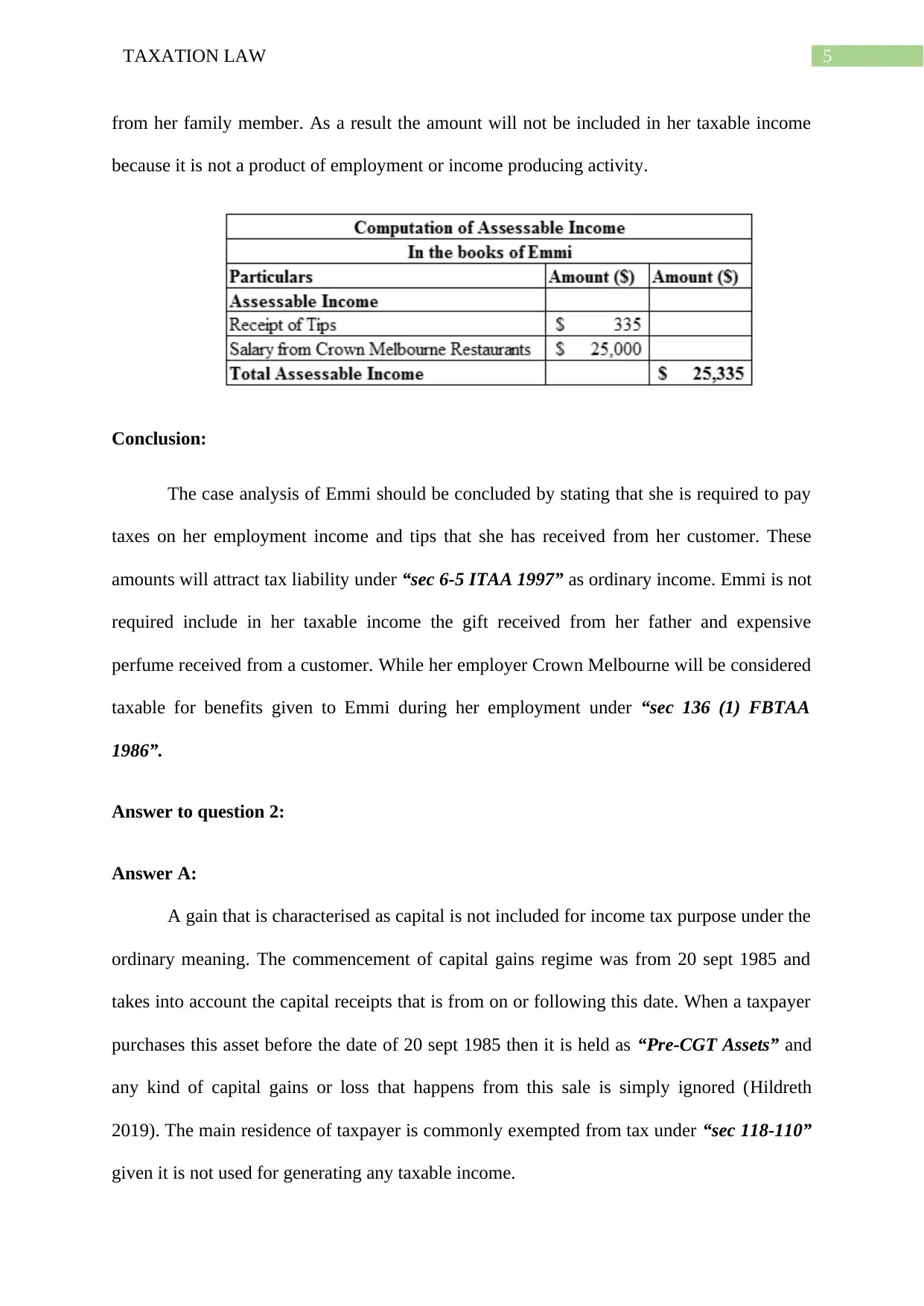

All through the year Emmi also made an income that amounted to $25,000 from her

part-time employment with Crown Melbourne Restaurant. Denoting the verdict made in

“British Columbia v Ostrum (1904)” the receipt of $25,000 that is generated from

employment or the service given is regarded as income for Emmi (Kiprotich 2016). The

amount is an income from personal exertion and it will be included in Emmi’s tax return

under “sec 6-5 ITA Act 97”.

A perfume of $250 was received by one of her customer as Christmas gift. Emmi did

not used the perfume and gave it to her mother. Citing “Hayes v FCT (1947)” the expensive

perfume received by Emmi is a personal gift on the basis of her personal qualities (Du Preez

2016). and it is opposite to other forms of voluntary payment that are viewed incidental to

service or employment. It cannot be viewed as ordinary earnings and such gift should not be

held taxable to her.

All through the year a monthly entertainment event was paid by Emmi’s employer to

Emmi. It also included meals that Emmi consumed. Denoting the event of “FCT v

Indooroopily Children’s Services (2007)” the entertainment event and food is a benefit under

“sec 136 (1) FBTAA 1986” that is given by the employer to Emmi during the year of

taxation in relation to her employment as an employee (Fleurbaey and Maniquet 2018). The

employer here Crown Melbourne restaurant will be liable for taxation under “sec 66 (1)

FBTAA 1986” relating to the value of entertainment event and food benefit that is given to

Emmi during the year of tax.

Lastly, Emmi also revived a gift that amounted to $15,000 from her father as a

Christmas gift. It can be stated that the gift amount of $15,000 is a non-taxable gift received

(Miller and Oats 2016). It establishes a required relation among the service rendered and

making it as a taxable ordinary earnings for Emmi under “sec 6-5 ITA Act 97”.

All through the year Emmi also made an income that amounted to $25,000 from her

part-time employment with Crown Melbourne Restaurant. Denoting the verdict made in

“British Columbia v Ostrum (1904)” the receipt of $25,000 that is generated from

employment or the service given is regarded as income for Emmi (Kiprotich 2016). The

amount is an income from personal exertion and it will be included in Emmi’s tax return

under “sec 6-5 ITA Act 97”.

A perfume of $250 was received by one of her customer as Christmas gift. Emmi did

not used the perfume and gave it to her mother. Citing “Hayes v FCT (1947)” the expensive

perfume received by Emmi is a personal gift on the basis of her personal qualities (Du Preez

2016). and it is opposite to other forms of voluntary payment that are viewed incidental to

service or employment. It cannot be viewed as ordinary earnings and such gift should not be

held taxable to her.

All through the year a monthly entertainment event was paid by Emmi’s employer to

Emmi. It also included meals that Emmi consumed. Denoting the event of “FCT v

Indooroopily Children’s Services (2007)” the entertainment event and food is a benefit under

“sec 136 (1) FBTAA 1986” that is given by the employer to Emmi during the year of

taxation in relation to her employment as an employee (Fleurbaey and Maniquet 2018). The

employer here Crown Melbourne restaurant will be liable for taxation under “sec 66 (1)

FBTAA 1986” relating to the value of entertainment event and food benefit that is given to

Emmi during the year of tax.

Lastly, Emmi also revived a gift that amounted to $15,000 from her father as a

Christmas gift. It can be stated that the gift amount of $15,000 is a non-taxable gift received

5TAXATION LAW

from her family member. As a result the amount will not be included in her taxable income

because it is not a product of employment or income producing activity.

Conclusion:

The case analysis of Emmi should be concluded by stating that she is required to pay

taxes on her employment income and tips that she has received from her customer. These

amounts will attract tax liability under “sec 6-5 ITAA 1997” as ordinary income. Emmi is not

required include in her taxable income the gift received from her father and expensive

perfume received from a customer. While her employer Crown Melbourne will be considered

taxable for benefits given to Emmi during her employment under “sec 136 (1) FBTAA

1986”.

Answer to question 2:

Answer A:

A gain that is characterised as capital is not included for income tax purpose under the

ordinary meaning. The commencement of capital gains regime was from 20 sept 1985 and

takes into account the capital receipts that is from on or following this date. When a taxpayer

purchases this asset before the date of 20 sept 1985 then it is held as “Pre-CGT Assets” and

any kind of capital gains or loss that happens from this sale is simply ignored (Hildreth

2019). The main residence of taxpayer is commonly exempted from tax under “sec 118-110”

given it is not used for generating any taxable income.

from her family member. As a result the amount will not be included in her taxable income

because it is not a product of employment or income producing activity.

Conclusion:

The case analysis of Emmi should be concluded by stating that she is required to pay

taxes on her employment income and tips that she has received from her customer. These

amounts will attract tax liability under “sec 6-5 ITAA 1997” as ordinary income. Emmi is not

required include in her taxable income the gift received from her father and expensive

perfume received from a customer. While her employer Crown Melbourne will be considered

taxable for benefits given to Emmi during her employment under “sec 136 (1) FBTAA

1986”.

Answer to question 2:

Answer A:

A gain that is characterised as capital is not included for income tax purpose under the

ordinary meaning. The commencement of capital gains regime was from 20 sept 1985 and

takes into account the capital receipts that is from on or following this date. When a taxpayer

purchases this asset before the date of 20 sept 1985 then it is held as “Pre-CGT Assets” and

any kind of capital gains or loss that happens from this sale is simply ignored (Hildreth

2019). The main residence of taxpayer is commonly exempted from tax under “sec 118-110”

given it is not used for generating any taxable income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

The taxpayer here Liu is found be a 65-year old Australian resident who has decided

to move china by selling all her Australian assets. As evident she sells her main residence that

she has purchased in 1981 for $55,000. The sells proceeds derived from sale stood $630,000.

As a result, the asset or her main residence should be classified as “Pre-CGT Asset” because

the house of Liu was bought before the start of CGT regime (Jones and Rhoades-Catanach

2015). Therefore, the capital gains made is simply required to be ignored by Liu.

Answer B:

“CGT event A1” is associated with sale of CGT asset under “sec 104-10 ITAA

1997”. “Personal use asset” (PUA’s) under the “sec 108-20 (2)” consist of the CGT asset

that is used by taxpayer for own usage. The type of asset under this category include

racehorse, furniture, electrical goods, motor vehicles and household goods. Most importantly,

under the “sec 108-20 (1)” capital loss that happens from sale of PUA’s is to be ignored

(Sikka 2017).

Liu sells her private car for $8,000. She purchased the car in 2001 for $37,000. When

the car was disposed by Liu a “CGT event A1” under “sec 104-10” happened. The car of Liu

is classified as PUA’s under “sec 108-20 (2)” because she used the car for her private

purpose. However, she suffered a capital loss when the car was sold (Burman et al. 2016).

Under “sec 108-20 (1)”, Liu should disregard her capital loss suffered from selling her car.

Answer C:

In order to assist the small business, there is a basic conditions that is aimed at

providing relief to small business from any capital gains which happens from selling the

business can be lowered by numerous concessions available under “Div 152 ITAA 1997”.

These exemptions are

The taxpayer here Liu is found be a 65-year old Australian resident who has decided

to move china by selling all her Australian assets. As evident she sells her main residence that

she has purchased in 1981 for $55,000. The sells proceeds derived from sale stood $630,000.

As a result, the asset or her main residence should be classified as “Pre-CGT Asset” because

the house of Liu was bought before the start of CGT regime (Jones and Rhoades-Catanach

2015). Therefore, the capital gains made is simply required to be ignored by Liu.

Answer B:

“CGT event A1” is associated with sale of CGT asset under “sec 104-10 ITAA

1997”. “Personal use asset” (PUA’s) under the “sec 108-20 (2)” consist of the CGT asset

that is used by taxpayer for own usage. The type of asset under this category include

racehorse, furniture, electrical goods, motor vehicles and household goods. Most importantly,

under the “sec 108-20 (1)” capital loss that happens from sale of PUA’s is to be ignored

(Sikka 2017).

Liu sells her private car for $8,000. She purchased the car in 2001 for $37,000. When

the car was disposed by Liu a “CGT event A1” under “sec 104-10” happened. The car of Liu

is classified as PUA’s under “sec 108-20 (2)” because she used the car for her private

purpose. However, she suffered a capital loss when the car was sold (Burman et al. 2016).

Under “sec 108-20 (1)”, Liu should disregard her capital loss suffered from selling her car.

Answer C:

In order to assist the small business, there is a basic conditions that is aimed at

providing relief to small business from any capital gains which happens from selling the

business can be lowered by numerous concessions available under “Div 152 ITAA 1997”.

These exemptions are

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

1. “15-year asset ownership” exemption from CGT under “subdiv 152-B” when the

asset owned by taxpayer is owned for 15 years or more and the minimum age of tax

payer is 55 years or more to access this concession.

2. “50% reduction” in capital gains under “Subdiv 152-C”. This concession is available

after making the general 50% CGT discount (Hildreth 2019).

3. Under the “Sub-152-D” a “retirement exemption” is given to the taxpayer from

capital gains tax. The exemption available to taxpayer is not more than $500,000 from

total CGT proceeds.

4. “Roll-over exemption relief” is given to taxpayer under subdiv 152-E when the

proceeds derived from taxpayer is used for purchasing the replacement assets.

The basic conditions for availing the CGT relief is that the entity should be a small

business and the value of net asset should not go beyond $6 million. Furthermore, the CGT

asset is ought to be an active asset.

Liu here reports the sale of her small business enterprise for a sales proceeds of

$125,000. It can be stated that Liu is eligible for claiming small business CGT concession

from CGT under “Div 152 ITAA 1997” because her business satisfies the given definition.

Furthermore, all her assets are active assets and the value of asset is not more than $6 million

(Miller and Oats 2016). As a result, under “SubDiv 152-D” Liu is eligible for claiming

retirement exemption relating to proceeds derived from sale of CGT asset. She is also retiring

from her business and the CGT proceeds is under the limit of $500,000.

Answer D:

Special rules are implemented on the gains or loss made from the personal use assets.

Under “sec 118-10(3)” capital gains or loss that happens should be ignored if the first

element of PUA’s cost base is lower than $10k (Kiprotich 2016). Accordingly, it has been

1. “15-year asset ownership” exemption from CGT under “subdiv 152-B” when the

asset owned by taxpayer is owned for 15 years or more and the minimum age of tax

payer is 55 years or more to access this concession.

2. “50% reduction” in capital gains under “Subdiv 152-C”. This concession is available

after making the general 50% CGT discount (Hildreth 2019).

3. Under the “Sub-152-D” a “retirement exemption” is given to the taxpayer from

capital gains tax. The exemption available to taxpayer is not more than $500,000 from

total CGT proceeds.

4. “Roll-over exemption relief” is given to taxpayer under subdiv 152-E when the

proceeds derived from taxpayer is used for purchasing the replacement assets.

The basic conditions for availing the CGT relief is that the entity should be a small

business and the value of net asset should not go beyond $6 million. Furthermore, the CGT

asset is ought to be an active asset.

Liu here reports the sale of her small business enterprise for a sales proceeds of

$125,000. It can be stated that Liu is eligible for claiming small business CGT concession

from CGT under “Div 152 ITAA 1997” because her business satisfies the given definition.

Furthermore, all her assets are active assets and the value of asset is not more than $6 million

(Miller and Oats 2016). As a result, under “SubDiv 152-D” Liu is eligible for claiming

retirement exemption relating to proceeds derived from sale of CGT asset. She is also retiring

from her business and the CGT proceeds is under the limit of $500,000.

Answer D:

Special rules are implemented on the gains or loss made from the personal use assets.

Under “sec 118-10(3)” capital gains or loss that happens should be ignored if the first

element of PUA’s cost base is lower than $10k (Kiprotich 2016). Accordingly, it has been

8TAXATION LAW

found in the case that Liu has sold the furniture and derived a sales proceeds of $4,800. There

are no single item that has been disposed by Liu for a purchase price of greater than $2,000.

The furniture is classified as personal use asset under “sec 108-20”.

In agreement with the special rules of PUA’s given in “sec 118-10(3)” the furniture

here fails to satisfy the first element cost base of $10k since it was purchased by Liu for less

than $10. The capital gains made here needs to be ignored by Liu.

Answer E:

Collectables, apart from “personal use asset” defined in “sec 108-10 (2)” includes

antiques, jewellery, artwork such as paintings, sculptures etc. bought or kept by taxpayer for

private usage and enjoyment. Under the special rule of “sec 118-10 (1) and (2)” capital gains

from collectables is to be ignored when the purchase price or first element cost base is $500

or lower than $500 (Schenk 2017).

In the current tax year, Liu has sold paintings for $28,000 with each paintings cost is

not greater than $500. The paintings bought by Liu meets the definition of collectable under

“sec 108-10 (2)” (Bankman et al. 2018). The paintings resulted in capital gains when sold by

Liu. However, the paintings fail to meet the first element cost base of $500 and capital gains

derived will be ignored by Liu under “sec 118-10 (1) and (2)”.

While there was one painting that had the cost of $1000 was sold by Liu for $8,000.

As a result, the capital gains made will be considered taxable as statutory income for Liu

under “sec 102-5 ITAA 1997”.

found in the case that Liu has sold the furniture and derived a sales proceeds of $4,800. There

are no single item that has been disposed by Liu for a purchase price of greater than $2,000.

The furniture is classified as personal use asset under “sec 108-20”.

In agreement with the special rules of PUA’s given in “sec 118-10(3)” the furniture

here fails to satisfy the first element cost base of $10k since it was purchased by Liu for less

than $10. The capital gains made here needs to be ignored by Liu.

Answer E:

Collectables, apart from “personal use asset” defined in “sec 108-10 (2)” includes

antiques, jewellery, artwork such as paintings, sculptures etc. bought or kept by taxpayer for

private usage and enjoyment. Under the special rule of “sec 118-10 (1) and (2)” capital gains

from collectables is to be ignored when the purchase price or first element cost base is $500

or lower than $500 (Schenk 2017).

In the current tax year, Liu has sold paintings for $28,000 with each paintings cost is

not greater than $500. The paintings bought by Liu meets the definition of collectable under

“sec 108-10 (2)” (Bankman et al. 2018). The paintings resulted in capital gains when sold by

Liu. However, the paintings fail to meet the first element cost base of $500 and capital gains

derived will be ignored by Liu under “sec 118-10 (1) and (2)”.

While there was one painting that had the cost of $1000 was sold by Liu for $8,000.

As a result, the capital gains made will be considered taxable as statutory income for Liu

under “sec 102-5 ITAA 1997”.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

References:

Ausness, R.C., 2017. Discretionary Trusts: An Update. ACTEC LJ, 43, p.231.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Du Preez, H., 2016. A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Elliott, W.D., 2015. Federal Taxation: 2014-2015. Tex. Tech L. Rev., 48, p.679.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of taxation for business and investment

planning. McGraw-Hill Higher Education.

Kiprotich, B.A., 2016. Principles of taxation. governance, 5(7), pp.341-352.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Noseda, F., 2017. Trusts and privacy: A new battle front. Trusts & Trustees, 23(3), pp.301-

310.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

References:

Ausness, R.C., 2017. Discretionary Trusts: An Update. ACTEC LJ, 43, p.231.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2018. Federal Income Taxation.

Aspen Publishers.

Burman, L.E., Gale, W.G., Gault, S., Kim, B., Nunns, J. and Rosenthal, S., 2016. Financial

transaction taxes in theory and practice. National Tax Journal, 69(1), pp.171-216.

Du Preez, H., 2016. A construction of the fundamental principles of taxation (Doctoral

dissertation, University of Pretoria).

Elliott, W.D., 2015. Federal Taxation: 2014-2015. Tex. Tech L. Rev., 48, p.679.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Hildreth, W.B. ed., 2019. Handbook on taxation. Routledge.

Jones, S. and Rhoades-Catanach, S., 2015. Principles of taxation for business and investment

planning. McGraw-Hill Higher Education.

Kiprotich, B.A., 2016. Principles of taxation. governance, 5(7), pp.341-352.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

Noseda, F., 2017. Trusts and privacy: A new battle front. Trusts & Trustees, 23(3), pp.301-

310.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum (Vol. 41, No. 4, pp. 390-405). Taylor & Francis.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.