ACCG 924 Taxation Law: Computing Taxable Income - A Case Study

VerifiedAdded on 2023/06/03

|12

|2247

|352

Case Study

AI Summary

This case study provides a detailed analysis of Technology Computer Pty Ltd's taxable income and tax payable for the year ended June 30, 2018. It includes adjustments to the accounting profit based on various items such as trading stock, service revenue, depreciation, sale of a machine, repair and maintenance expenditures, borrowing costs, sale of land, entertainment expenses, and provisions for employee benefits. The solution calculates the taxable income to be $1,380,650.00 and the tax payable on this income to be $379,678.75. Additionally, it addresses a capital gain of $100,000 with a corresponding tax of $30,000, resulting in a net tax payable of $409,678.75 for the year. Desklib provides access to similar solved assignments and resources for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

TAXATION LAW

Contents

Introduction:....................................................................................................................................2

Part a:...............................................................................................................................................2

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

TAXATION LAW

Contents

Introduction:....................................................................................................................................2

Part a:...............................................................................................................................................2

Conclusion:......................................................................................................................................9

References:....................................................................................................................................10

2

TAXATION LAW

Introduction:

Taking into consideration the rules and regulations governing the tax related matters of the

corporates in the country, a detailed explanation of the items of income and expenditures to be

included and excluded for calculation of taxable profit of Technology Computer Pty Ltd

(Technology) is provided below for the appraisal of the Chief Financial Officer of the company.

Part a:

The explanations as to treatments of the different items mentioned in the notes in relation to the

adjustments for calculation of taxable income of business of Technology are enumerated below:

1. Trading stock at the close of the year: As on 30th June, 2018, stock valuing $40,000 purchased

from a Singapore based company is yet to be received as the goods are still on a ship. However,

Technology Computer Pty Ltd (Technology) has included the value of these stock in calculating

the closing stock. Thus, the profit of the company is overvalued by the amount of stock.

Accordingly, to be deducted in computing the taxable profit of the company (Nisha, 2015).

2. Service revenue of $50,000 should not be recorded as revenue until unless the required terms and

conditions of such revenue is fulfilled. Since, the client in this case has the right to ask for refund

in case the service is not completed by technology by the end of the year. Hence, there is still

uncertainty attached with the item of revenue. Hence, it should not be considered while

calculating the taxable income of the company. Thus, excluded from accounting profit before tax

to calculate the taxable profit (Jiang et. al. 2016).

3. Amount of depreciation provided in the books of accounts, i.e. $300,000 is added back to the

accounting profit and the allowable depreciation of $375,000 is deducted for calculating taxable

income of Technology. In Tax Reconciliation Statement of the company, a net deduction of

TAXATION LAW

Introduction:

Taking into consideration the rules and regulations governing the tax related matters of the

corporates in the country, a detailed explanation of the items of income and expenditures to be

included and excluded for calculation of taxable profit of Technology Computer Pty Ltd

(Technology) is provided below for the appraisal of the Chief Financial Officer of the company.

Part a:

The explanations as to treatments of the different items mentioned in the notes in relation to the

adjustments for calculation of taxable income of business of Technology are enumerated below:

1. Trading stock at the close of the year: As on 30th June, 2018, stock valuing $40,000 purchased

from a Singapore based company is yet to be received as the goods are still on a ship. However,

Technology Computer Pty Ltd (Technology) has included the value of these stock in calculating

the closing stock. Thus, the profit of the company is overvalued by the amount of stock.

Accordingly, to be deducted in computing the taxable profit of the company (Nisha, 2015).

2. Service revenue of $50,000 should not be recorded as revenue until unless the required terms and

conditions of such revenue is fulfilled. Since, the client in this case has the right to ask for refund

in case the service is not completed by technology by the end of the year. Hence, there is still

uncertainty attached with the item of revenue. Hence, it should not be considered while

calculating the taxable income of the company. Thus, excluded from accounting profit before tax

to calculate the taxable profit (Jiang et. al. 2016).

3. Amount of depreciation provided in the books of accounts, i.e. $300,000 is added back to the

accounting profit and the allowable depreciation of $375,000 is deducted for calculating taxable

income of Technology. In Tax Reconciliation Statement of the company, a net deduction of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

TAXATION LAW

$75,000 ($375000 - $300,000) could have also been shown to calculate the taxable income of the

company. Thus, in both circumstances the net effect to the profit is reduction of $75,000 for

calculation of taxable profit (Smith et. al. 2016).

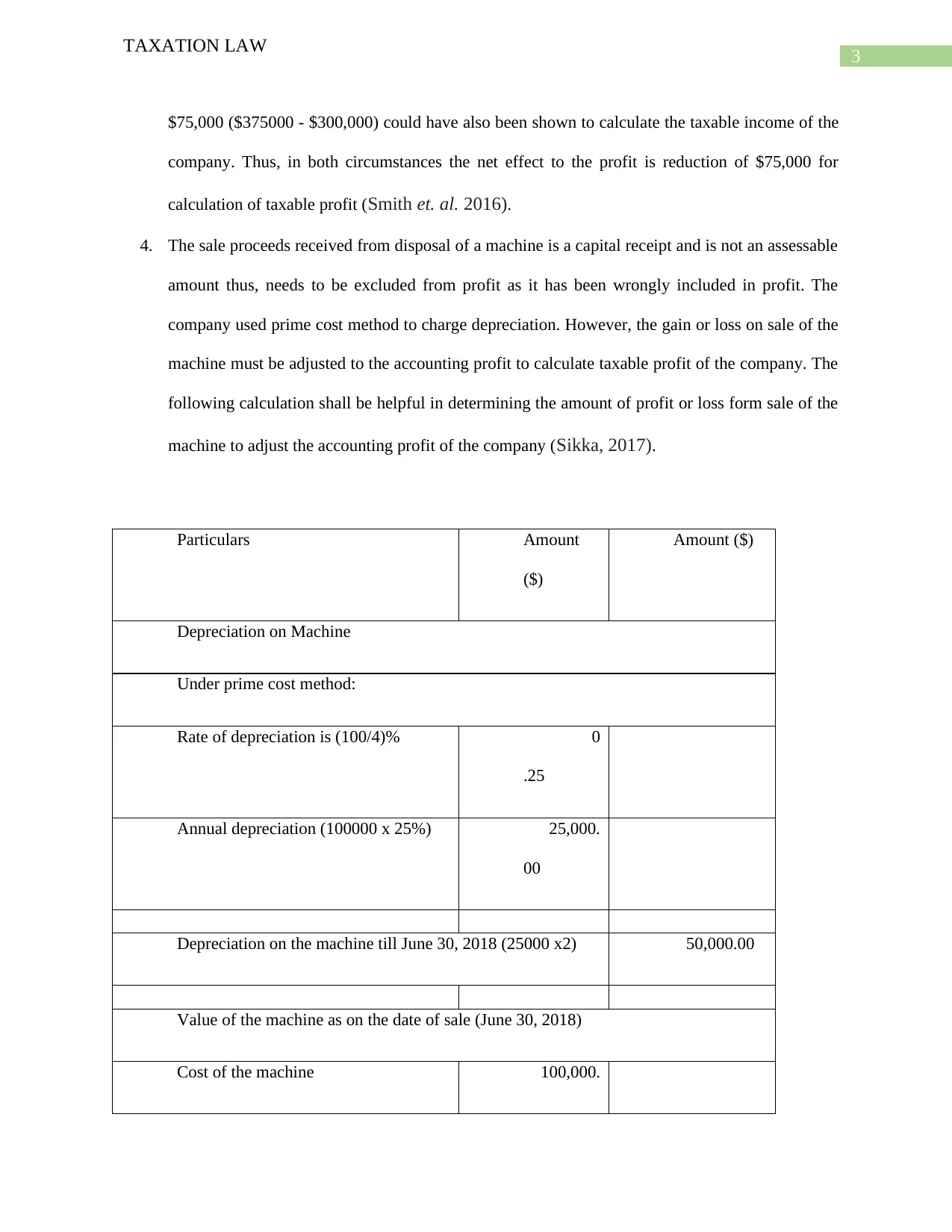

4. The sale proceeds received from disposal of a machine is a capital receipt and is not an assessable

amount thus, needs to be excluded from profit as it has been wrongly included in profit. The

company used prime cost method to charge depreciation. However, the gain or loss on sale of the

machine must be adjusted to the accounting profit to calculate taxable profit of the company. The

following calculation shall be helpful in determining the amount of profit or loss form sale of the

machine to adjust the accounting profit of the company (Sikka, 2017).

Particulars Amount

($)

Amount ($)

Depreciation on Machine

Under prime cost method:

Rate of depreciation is (100/4)% 0

.25

Annual depreciation (100000 x 25%) 25,000.

00

Depreciation on the machine till June 30, 2018 (25000 x2) 50,000.00

Value of the machine as on the date of sale (June 30, 2018)

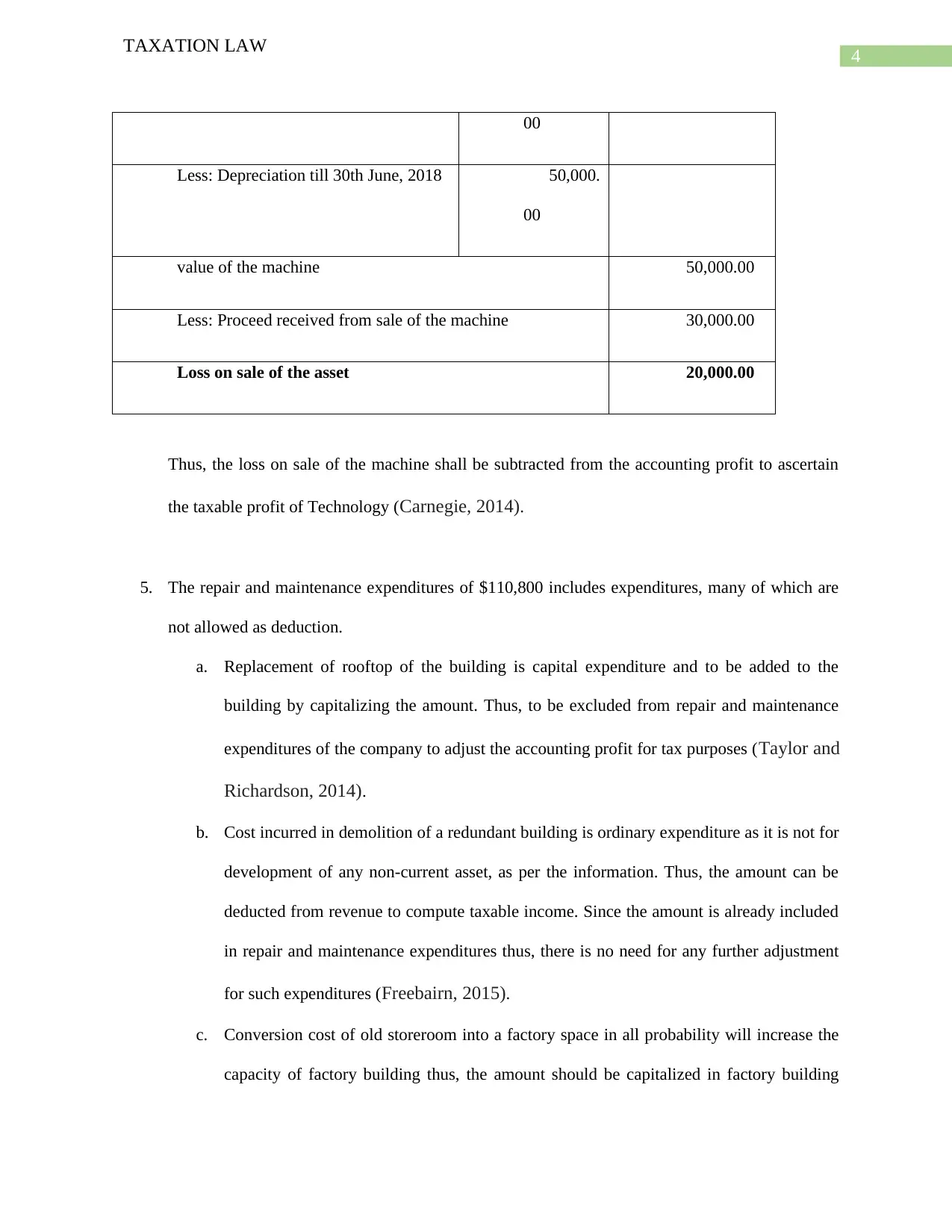

Cost of the machine 100,000.

TAXATION LAW

$75,000 ($375000 - $300,000) could have also been shown to calculate the taxable income of the

company. Thus, in both circumstances the net effect to the profit is reduction of $75,000 for

calculation of taxable profit (Smith et. al. 2016).

4. The sale proceeds received from disposal of a machine is a capital receipt and is not an assessable

amount thus, needs to be excluded from profit as it has been wrongly included in profit. The

company used prime cost method to charge depreciation. However, the gain or loss on sale of the

machine must be adjusted to the accounting profit to calculate taxable profit of the company. The

following calculation shall be helpful in determining the amount of profit or loss form sale of the

machine to adjust the accounting profit of the company (Sikka, 2017).

Particulars Amount

($)

Amount ($)

Depreciation on Machine

Under prime cost method:

Rate of depreciation is (100/4)% 0

.25

Annual depreciation (100000 x 25%) 25,000.

00

Depreciation on the machine till June 30, 2018 (25000 x2) 50,000.00

Value of the machine as on the date of sale (June 30, 2018)

Cost of the machine 100,000.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

TAXATION LAW

00

Less: Depreciation till 30th June, 2018 50,000.

00

value of the machine 50,000.00

Less: Proceed received from sale of the machine 30,000.00

Loss on sale of the asset 20,000.00

Thus, the loss on sale of the machine shall be subtracted from the accounting profit to ascertain

the taxable profit of Technology (Carnegie, 2014).

5. The repair and maintenance expenditures of $110,800 includes expenditures, many of which are

not allowed as deduction.

a. Replacement of rooftop of the building is capital expenditure and to be added to the

building by capitalizing the amount. Thus, to be excluded from repair and maintenance

expenditures of the company to adjust the accounting profit for tax purposes (Taylor and

Richardson, 2014).

b. Cost incurred in demolition of a redundant building is ordinary expenditure as it is not for

development of any non-current asset, as per the information. Thus, the amount can be

deducted from revenue to compute taxable income. Since the amount is already included

in repair and maintenance expenditures thus, there is no need for any further adjustment

for such expenditures (Freebairn, 2015).

c. Conversion cost of old storeroom into a factory space in all probability will increase the

capacity of factory building thus, the amount should be capitalized in factory building

TAXATION LAW

00

Less: Depreciation till 30th June, 2018 50,000.

00

value of the machine 50,000.00

Less: Proceed received from sale of the machine 30,000.00

Loss on sale of the asset 20,000.00

Thus, the loss on sale of the machine shall be subtracted from the accounting profit to ascertain

the taxable profit of Technology (Carnegie, 2014).

5. The repair and maintenance expenditures of $110,800 includes expenditures, many of which are

not allowed as deduction.

a. Replacement of rooftop of the building is capital expenditure and to be added to the

building by capitalizing the amount. Thus, to be excluded from repair and maintenance

expenditures of the company to adjust the accounting profit for tax purposes (Taylor and

Richardson, 2014).

b. Cost incurred in demolition of a redundant building is ordinary expenditure as it is not for

development of any non-current asset, as per the information. Thus, the amount can be

deducted from revenue to compute taxable income. Since the amount is already included

in repair and maintenance expenditures thus, there is no need for any further adjustment

for such expenditures (Freebairn, 2015).

c. Conversion cost of old storeroom into a factory space in all probability will increase the

capacity of factory building thus, the amount should be capitalized in factory building

5

TAXATION LAW

account. However, the company has considered it as repair and maintenance expenditure

thus, the amount of $14,800 must be added back to the accounting profit to adjust the

profit for tax purpose (Li and Tran, 2016).

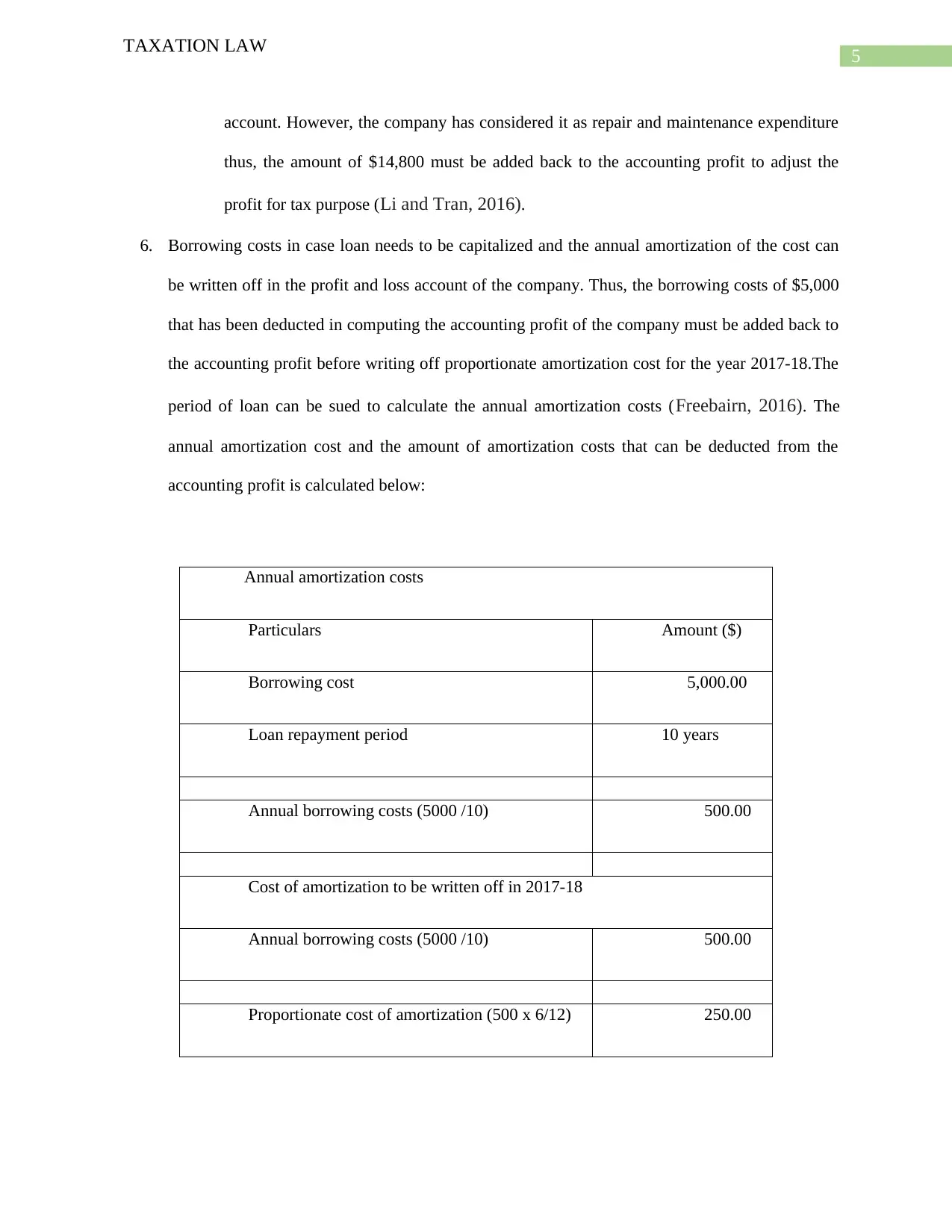

6. Borrowing costs in case loan needs to be capitalized and the annual amortization of the cost can

be written off in the profit and loss account of the company. Thus, the borrowing costs of $5,000

that has been deducted in computing the accounting profit of the company must be added back to

the accounting profit before writing off proportionate amortization cost for the year 2017-18.The

period of loan can be sued to calculate the annual amortization costs (Freebairn, 2016). The

annual amortization cost and the amount of amortization costs that can be deducted from the

accounting profit is calculated below:

Annual amortization costs

Particulars Amount ($)

Borrowing cost 5,000.00

Loan repayment period 10 years

Annual borrowing costs (5000 /10) 500.00

Cost of amortization to be written off in 2017-18

Annual borrowing costs (5000 /10) 500.00

Proportionate cost of amortization (500 x 6/12) 250.00

TAXATION LAW

account. However, the company has considered it as repair and maintenance expenditure

thus, the amount of $14,800 must be added back to the accounting profit to adjust the

profit for tax purpose (Li and Tran, 2016).

6. Borrowing costs in case loan needs to be capitalized and the annual amortization of the cost can

be written off in the profit and loss account of the company. Thus, the borrowing costs of $5,000

that has been deducted in computing the accounting profit of the company must be added back to

the accounting profit before writing off proportionate amortization cost for the year 2017-18.The

period of loan can be sued to calculate the annual amortization costs (Freebairn, 2016). The

annual amortization cost and the amount of amortization costs that can be deducted from the

accounting profit is calculated below:

Annual amortization costs

Particulars Amount ($)

Borrowing cost 5,000.00

Loan repayment period 10 years

Annual borrowing costs (5000 /10) 500.00

Cost of amortization to be written off in 2017-18

Annual borrowing costs (5000 /10) 500.00

Proportionate cost of amortization (500 x 6/12) 250.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

TAXATION LAW

Hence, after adding back the borrowing cost of $5,000 the accounting profit should be

reduced by $250 for amortization expenses.

7. Land is non-current and non-depreciable asset thus, sale of such asset would result in either

capital gain or capital loss to a person. Such capital gain and capital loss must not be included in

business income and expenditures for calculating taxable profit of business. Hence, the same is

deducted from accounting profit (Chardon, Freudenberg and Brimble, 2016).

8. Entertainment expenses of 20,000 incurred on the employee even if GST is paid on such

entertainment expenses is not allowed as deduction. However, entertainment expense of clients

assuming it is necessary to earn revenue from business is allowed as deduction.

9. The relationship between the directors and an entity is based on the Agency theory. The directors

are expected run the affairs of the business effectively. Increasing the provision of long service

pay and holiday pay is not an allowable expense. Hence, the increase of $60,000 has to be

reversed by adding back the same to the profit of the company (Dixon and Nassios, 2016).

10. Expenditures incurred on research is allowed as deduction since it is still not feasible to capitalize

the expenditure assuming future benefits as the feasibility study has just been conducted. Since

the research expenses have been deducted to calculate accounting profit hence, not adjustment is

necessary.

11. The bad debt of $5,500 is in relation with the debtors of the entity acquired thus, it should have

been adjusted with the net assets acquired by the company at the time of acquisition. Thus,

$5,500 is to be added to the accounting profit to calculate the taxable profit from business.

Part b:

TAXATION LAW

Hence, after adding back the borrowing cost of $5,000 the accounting profit should be

reduced by $250 for amortization expenses.

7. Land is non-current and non-depreciable asset thus, sale of such asset would result in either

capital gain or capital loss to a person. Such capital gain and capital loss must not be included in

business income and expenditures for calculating taxable profit of business. Hence, the same is

deducted from accounting profit (Chardon, Freudenberg and Brimble, 2016).

8. Entertainment expenses of 20,000 incurred on the employee even if GST is paid on such

entertainment expenses is not allowed as deduction. However, entertainment expense of clients

assuming it is necessary to earn revenue from business is allowed as deduction.

9. The relationship between the directors and an entity is based on the Agency theory. The directors

are expected run the affairs of the business effectively. Increasing the provision of long service

pay and holiday pay is not an allowable expense. Hence, the increase of $60,000 has to be

reversed by adding back the same to the profit of the company (Dixon and Nassios, 2016).

10. Expenditures incurred on research is allowed as deduction since it is still not feasible to capitalize

the expenditure assuming future benefits as the feasibility study has just been conducted. Since

the research expenses have been deducted to calculate accounting profit hence, not adjustment is

necessary.

11. The bad debt of $5,500 is in relation with the debtors of the entity acquired thus, it should have

been adjusted with the net assets acquired by the company at the time of acquisition. Thus,

$5,500 is to be added to the accounting profit to calculate the taxable profit from business.

Part b:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

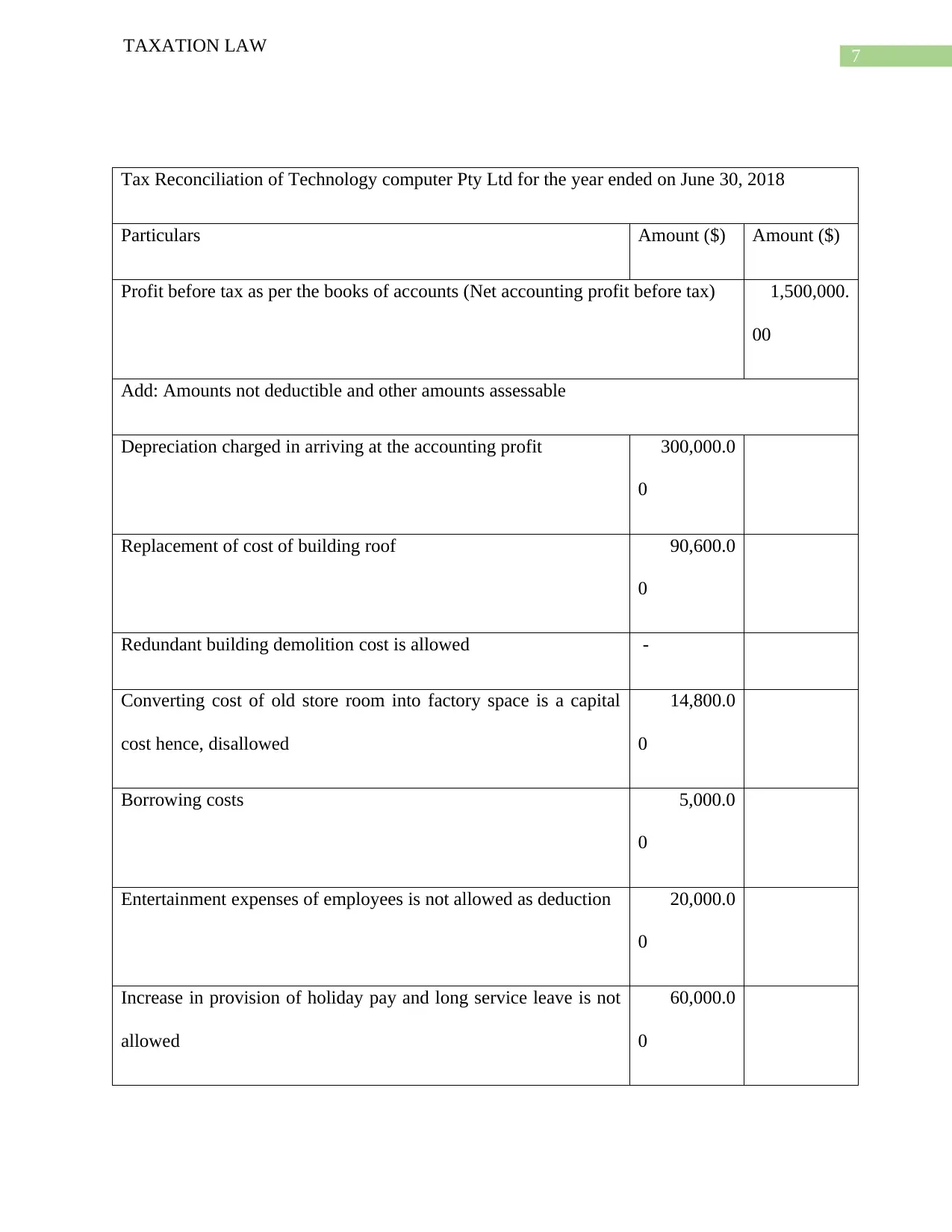

Tax Reconciliation of Technology computer Pty Ltd for the year ended on June 30, 2018

Particulars Amount ($) Amount ($)

Profit before tax as per the books of accounts (Net accounting profit before tax) 1,500,000.

00

Add: Amounts not deductible and other amounts assessable

Depreciation charged in arriving at the accounting profit 300,000.0

0

Replacement of cost of building roof 90,600.0

0

Redundant building demolition cost is allowed -

Converting cost of old store room into factory space is a capital

cost hence, disallowed

14,800.0

0

Borrowing costs 5,000.0

0

Entertainment expenses of employees is not allowed as deduction 20,000.0

0

Increase in provision of holiday pay and long service leave is not

allowed

60,000.0

0

TAXATION LAW

Tax Reconciliation of Technology computer Pty Ltd for the year ended on June 30, 2018

Particulars Amount ($) Amount ($)

Profit before tax as per the books of accounts (Net accounting profit before tax) 1,500,000.

00

Add: Amounts not deductible and other amounts assessable

Depreciation charged in arriving at the accounting profit 300,000.0

0

Replacement of cost of building roof 90,600.0

0

Redundant building demolition cost is allowed -

Converting cost of old store room into factory space is a capital

cost hence, disallowed

14,800.0

0

Borrowing costs 5,000.0

0

Entertainment expenses of employees is not allowed as deduction 20,000.0

0

Increase in provision of holiday pay and long service leave is not

allowed

60,000.0

0

8

TAXATION LAW

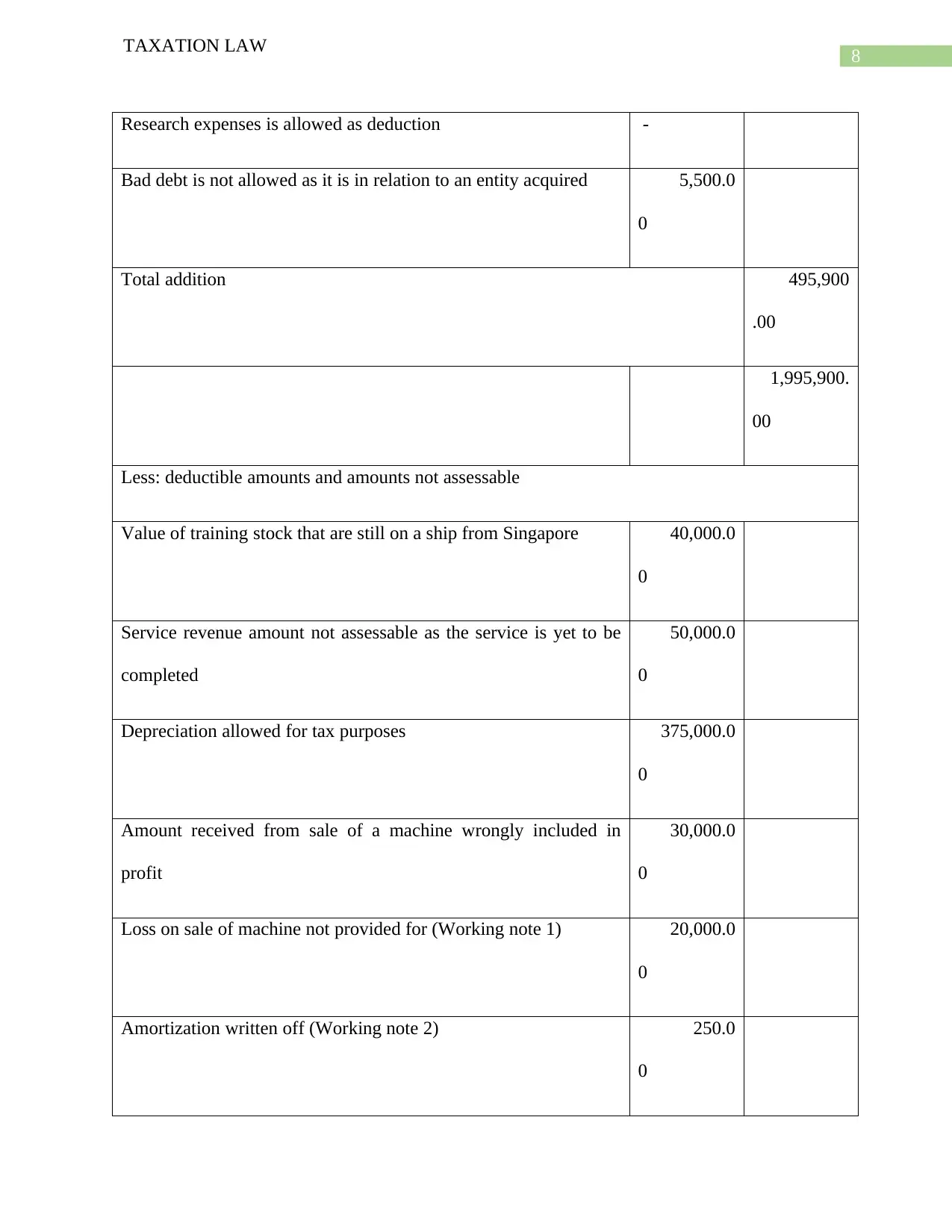

Research expenses is allowed as deduction -

Bad debt is not allowed as it is in relation to an entity acquired 5,500.0

0

Total addition 495,900

.00

1,995,900.

00

Less: deductible amounts and amounts not assessable

Value of training stock that are still on a ship from Singapore 40,000.0

0

Service revenue amount not assessable as the service is yet to be

completed

50,000.0

0

Depreciation allowed for tax purposes 375,000.0

0

Amount received from sale of a machine wrongly included in

profit

30,000.0

0

Loss on sale of machine not provided for (Working note 1) 20,000.0

0

Amortization written off (Working note 2) 250.0

0

TAXATION LAW

Research expenses is allowed as deduction -

Bad debt is not allowed as it is in relation to an entity acquired 5,500.0

0

Total addition 495,900

.00

1,995,900.

00

Less: deductible amounts and amounts not assessable

Value of training stock that are still on a ship from Singapore 40,000.0

0

Service revenue amount not assessable as the service is yet to be

completed

50,000.0

0

Depreciation allowed for tax purposes 375,000.0

0

Amount received from sale of a machine wrongly included in

profit

30,000.0

0

Loss on sale of machine not provided for (Working note 1) 20,000.0

0

Amortization written off (Working note 2) 250.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

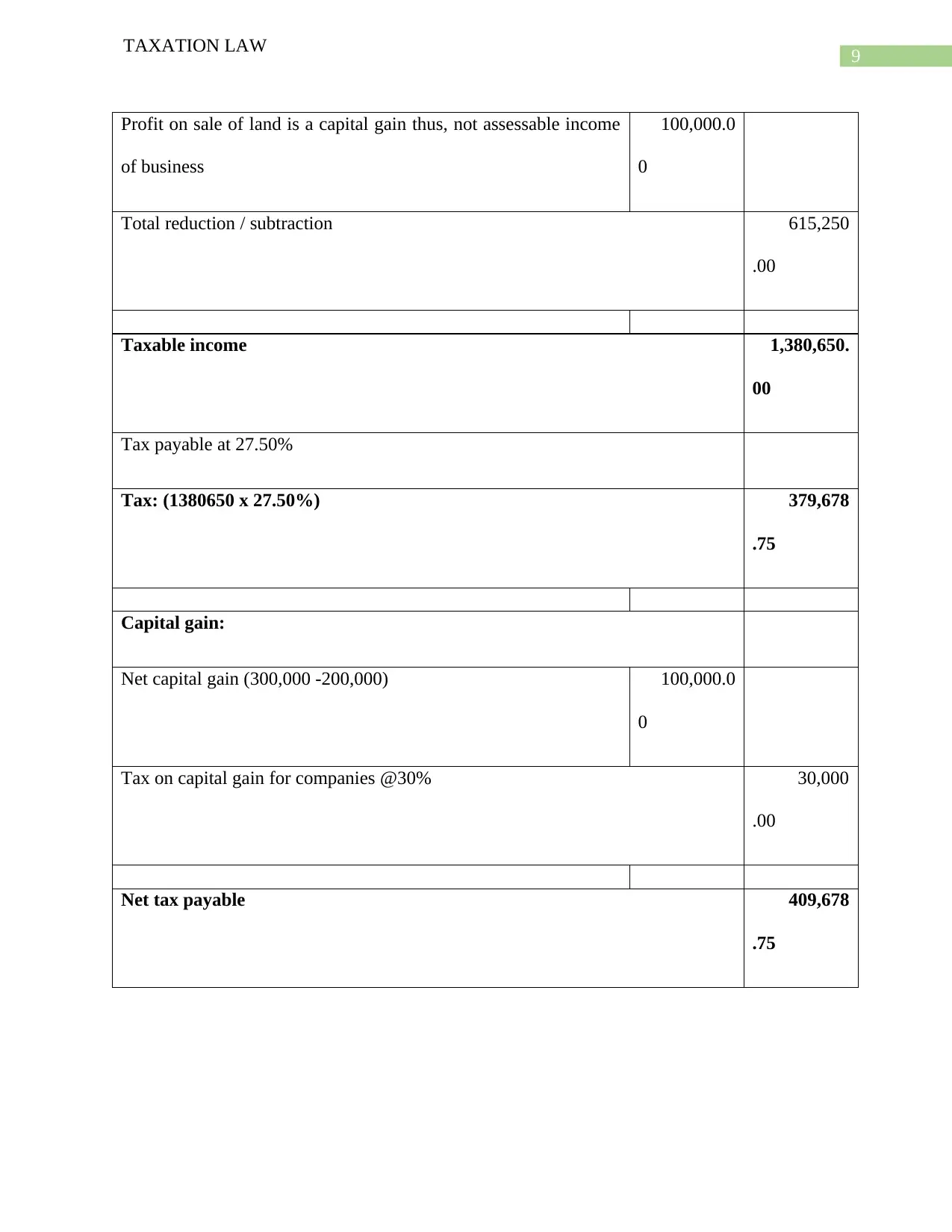

TAXATION LAW

Profit on sale of land is a capital gain thus, not assessable income

of business

100,000.0

0

Total reduction / subtraction 615,250

.00

Taxable income 1,380,650.

00

Tax payable at 27.50%

Tax: (1380650 x 27.50%) 379,678

.75

Capital gain:

Net capital gain (300,000 -200,000) 100,000.0

0

Tax on capital gain for companies @30% 30,000

.00

Net tax payable 409,678

.75

TAXATION LAW

Profit on sale of land is a capital gain thus, not assessable income

of business

100,000.0

0

Total reduction / subtraction 615,250

.00

Taxable income 1,380,650.

00

Tax payable at 27.50%

Tax: (1380650 x 27.50%) 379,678

.75

Capital gain:

Net capital gain (300,000 -200,000) 100,000.0

0

Tax on capital gain for companies @30% 30,000

.00

Net tax payable 409,678

.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

TAXATION LAW

Conclusion:

The taxable income from business of Technology for the year 2017-18 is $1,380,650.00 and tax

payable on such taxable business income is $379,678.75. In addition to that capital gain of the

company is $100,000 with tax payable on such gain at the rate 30%. Thus, net tax payable by

the company is $409,678.75 for the year 2017-18.

References:

Carnegie, G., 2014. Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321. [Online] Available from:

https://heinonline.org/HOL/LandingPage?handle=hein.journals/austraxrum31&div=16&id=&pa

ge= [Accessed 01 October 2018]

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre for Policy Studies, Victoria University. [Online] Available from:

https://www.copsmodels.com/ftp/workpapr/g-260.pdf [Accessed 01 October 2018]

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review, 48(4), pp.357-368.

Freebairn, J., 2016. Design alternatives for an Australian allowance for corporate equity. Austl.

Tax F., 31, p.555.

Jiang, W., Lu, M., Shan, Y. and Zhu, T., 2016. Evidence of avoiding working capital deficits in

Australia. Australian Accounting Review, 26(1), pp.107-118.

TAXATION LAW

Conclusion:

The taxable income from business of Technology for the year 2017-18 is $1,380,650.00 and tax

payable on such taxable business income is $379,678.75. In addition to that capital gain of the

company is $100,000 with tax payable on such gain at the rate 30%. Thus, net tax payable by

the company is $409,678.75 for the year 2017-18.

References:

Carnegie, G., 2014. Pastoral accounting in colonial Australia: a case study of unregulated

accounting. Routledge.

Chardon, T., Freudenberg, B. and Brimble, M., 2016. Tax literacy in Australia: not knowing

your deduction from your offset. Austl. Tax F., 31, p.321. [Online] Available from:

https://heinonline.org/HOL/LandingPage?handle=hein.journals/austraxrum31&div=16&id=&pa

ge= [Accessed 01 October 2018]

Dixon, J.M. and Nassios, J., 2016. Modelling the impacts of a cut to company tax in Australia.

Centre for Policy Studies, Victoria University. [Online] Available from:

https://www.copsmodels.com/ftp/workpapr/g-260.pdf [Accessed 01 October 2018]

Freebairn, J., 2015. Who Pays the Australian Corporate Income Tax?. Australian Economic

Review, 48(4), pp.357-368.

Freebairn, J., 2016. Design alternatives for an Australian allowance for corporate equity. Austl.

Tax F., 31, p.555.

Jiang, W., Lu, M., Shan, Y. and Zhu, T., 2016. Evidence of avoiding working capital deficits in

Australia. Australian Accounting Review, 26(1), pp.107-118.

11

TAXATION LAW

Li, E.X. and Tran, A.V., 2016. An Empirical Analysis of the Tax Burden of Mining Firms versus

Non-Mining Firms in Australia. Austl. Tax F., 31, p.167.

Nisha, N., 2015. Inventory valuation practices: A developing country perspective. International

Journal of Information Research and Review, 2(7), pp.867-874. [Online] Available from:

http://www.ijirr.com/sites/default/files/issues-files/0431.pdf [Accessed 01 October 2018]

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Smith, F., Smillie, K., Fitzsimons, J., Lindsay, B., Wells, G., Marles, V., Hutchinson, J., Hara,

B.O., Perrigo, T. and Atkinson, I., 2016. Reforms required to the Australian tax system to

improve biodiversity conservation on private land. Environmental and Planning Law

Journal, 33, pp.443-450.

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

TAXATION LAW

Li, E.X. and Tran, A.V., 2016. An Empirical Analysis of the Tax Burden of Mining Firms versus

Non-Mining Firms in Australia. Austl. Tax F., 31, p.167.

Nisha, N., 2015. Inventory valuation practices: A developing country perspective. International

Journal of Information Research and Review, 2(7), pp.867-874. [Online] Available from:

http://www.ijirr.com/sites/default/files/issues-files/0431.pdf [Accessed 01 October 2018]

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Smith, F., Smillie, K., Fitzsimons, J., Lindsay, B., Wells, G., Marles, V., Hutchinson, J., Hara,

B.O., Perrigo, T. and Atkinson, I., 2016. Reforms required to the Australian tax system to

improve biodiversity conservation on private land. Environmental and Planning Law

Journal, 33, pp.443-450.

Taylor, G. and Richardson, G., 2014. Incentives for corporate tax planning and reporting:

Empirical evidence from Australia. Journal of Contemporary Accounting & Economics, 10(1),

pp.1-15.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.