Understanding Taxation Law: Analysis of Taxable Income, Capital Gain and Loss, Tax Avoidance and Evasion

VerifiedAdded on 2023/06/04

|12

|3071

|264

AI Summary

This report provides an in-depth analysis of taxation law, including taxable income, capital gain and loss, tax avoidance and evasion. It discusses the relationship between capital gain and loss in rental property and the annual payment in respect of lotteries. It also explains the principles of tax evasion and tax avoidance. The subject is Taxation Law, with no specific course code or name, and no college or university mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Law 1

Taxation Law

Taxation Law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Law 2

Table of Contents

Introduction......................................................................................................................................2

Question 1........................................................................................................................................3

Question2.........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Table of Contents

Introduction......................................................................................................................................2

Question 1........................................................................................................................................3

Question2.........................................................................................................................................4

Question 3........................................................................................................................................6

Question 4........................................................................................................................................8

Conclusion.....................................................................................................................................10

References......................................................................................................................................11

Taxation Law 3

Introduction

This report helps to understand the concept of taxation law and analyse the different aspects of

taxation. It also provides the data and information related to the taxable income and lays down

the different principles. It also provides the relationship between the capital gain and capital

losses in relation to the rental property. It also accesses the information regarding the annual

payment in respect of lotteries. It also discusses the principle of tax evasion and tax avoidance.

This report will explain the value and importance of taxable earning and various alternate

methods to realise and treat capital losses relatively to rental property. It will help the reader to

access and understand the facts and of tax avoidance & evasion. It will reveal the value and

importance of such evasion principles in management of businesses and companies of Australia.

Introduction

This report helps to understand the concept of taxation law and analyse the different aspects of

taxation. It also provides the data and information related to the taxable income and lays down

the different principles. It also provides the relationship between the capital gain and capital

losses in relation to the rental property. It also accesses the information regarding the annual

payment in respect of lotteries. It also discusses the principle of tax evasion and tax avoidance.

This report will explain the value and importance of taxable earning and various alternate

methods to realise and treat capital losses relatively to rental property. It will help the reader to

access and understand the facts and of tax avoidance & evasion. It will reveal the value and

importance of such evasion principles in management of businesses and companies of Australia.

Taxation Law 4

Question 1

Solution

Gross annual income can be known as the Annual payment income that can be earned by the

entities on the yearly basis. It can be stated that from the lottery an individual can earn a lump

sum and that can be received annually. The act of lottery is recognised as the gambling that

consist of receivables by drawing the number of prizes. There are different regulations that can

be established by the government in respect of lottery to protect the interest of the public in

general. It can be noted that if the winner receives the sum of the lottery then he/she is liable for

paying the amount of capital gain tax on that lottery. In the situation of annuity pay-outs, the

winner has an opportunity to earn the jackpots. It also consists of interest that can be

accumulated from the investment over the time period of annuity (Cai, et. al., 2017).

It can be asserted that rather than the payment of annuity income, the sum received by the winner

can be fixed every year with the amount of $50,000 and that can be restricted to the nature of

payout in a situation of family emergency and financial emergency. It can also be stated that the

winner has no capability to pay the more amount of investments as a result into the generation of

cash and that can be compared to the sum of interest that can be earned on annuities. Apart from

this, the payment of annuity income the tax can be levied on the $50000as they receive the

revenue of $50000 from the lottery.

The other reason recognising the revenue that can be earned from lottery as the income of annual

payment is that the individual has received the inflow of cash from the lottery for next 20 years.

It can also note that the number of estates of deceased after the death of an individual can be

Question 1

Solution

Gross annual income can be known as the Annual payment income that can be earned by the

entities on the yearly basis. It can be stated that from the lottery an individual can earn a lump

sum and that can be received annually. The act of lottery is recognised as the gambling that

consist of receivables by drawing the number of prizes. There are different regulations that can

be established by the government in respect of lottery to protect the interest of the public in

general. It can be noted that if the winner receives the sum of the lottery then he/she is liable for

paying the amount of capital gain tax on that lottery. In the situation of annuity pay-outs, the

winner has an opportunity to earn the jackpots. It also consists of interest that can be

accumulated from the investment over the time period of annuity (Cai, et. al., 2017).

It can be asserted that rather than the payment of annuity income, the sum received by the winner

can be fixed every year with the amount of $50,000 and that can be restricted to the nature of

payout in a situation of family emergency and financial emergency. It can also be stated that the

winner has no capability to pay the more amount of investments as a result into the generation of

cash and that can be compared to the sum of interest that can be earned on annuities. Apart from

this, the payment of annuity income the tax can be levied on the $50000as they receive the

revenue of $50000 from the lottery.

The other reason recognising the revenue that can be earned from lottery as the income of annual

payment is that the individual has received the inflow of cash from the lottery for next 20 years.

It can also note that the number of estates of deceased after the death of an individual can be

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Law 5

recognised as the income of deceased. In this context, the winner can receive the amount of

$50,000 on which he receives the sum of money for the first time in the next 20 years.

Question 2

Solution

It can be determined that under the system of accrual basis. The expenses and revenues are

recorded when they are realized. Along with that income should be matched with the

expenditure. It can be noted that expenses are recorded at the time of occurrence and when the

cash is paid. Taxable income can be defined as the sum of income that helps to calculate the tax

which can be paid by the corporation and individuals in every year. The gross income can be

adjusted against the exemptions and reductions that can be allowed in the taxation year. It

consists of salary, bonus, investment income in respect of individuals.

Apart from this, in respect of a company, the taxable income consists the income that can be

generated by selling the services and products. It also consists the subsidies that can be provided

to their clients. It does not include the expenditure that can be made by the corporations from the

income to calculate the taxable income.

recognised as the income of deceased. In this context, the winner can receive the amount of

$50,000 on which he receives the sum of money for the first time in the next 20 years.

Question 2

Solution

It can be determined that under the system of accrual basis. The expenses and revenues are

recorded when they are realized. Along with that income should be matched with the

expenditure. It can be noted that expenses are recorded at the time of occurrence and when the

cash is paid. Taxable income can be defined as the sum of income that helps to calculate the tax

which can be paid by the corporation and individuals in every year. The gross income can be

adjusted against the exemptions and reductions that can be allowed in the taxation year. It

consists of salary, bonus, investment income in respect of individuals.

Apart from this, in respect of a company, the taxable income consists the income that can be

generated by selling the services and products. It also consists the subsidies that can be provided

to their clients. It does not include the expenditure that can be made by the corporations from the

income to calculate the taxable income.

Taxation Law 6

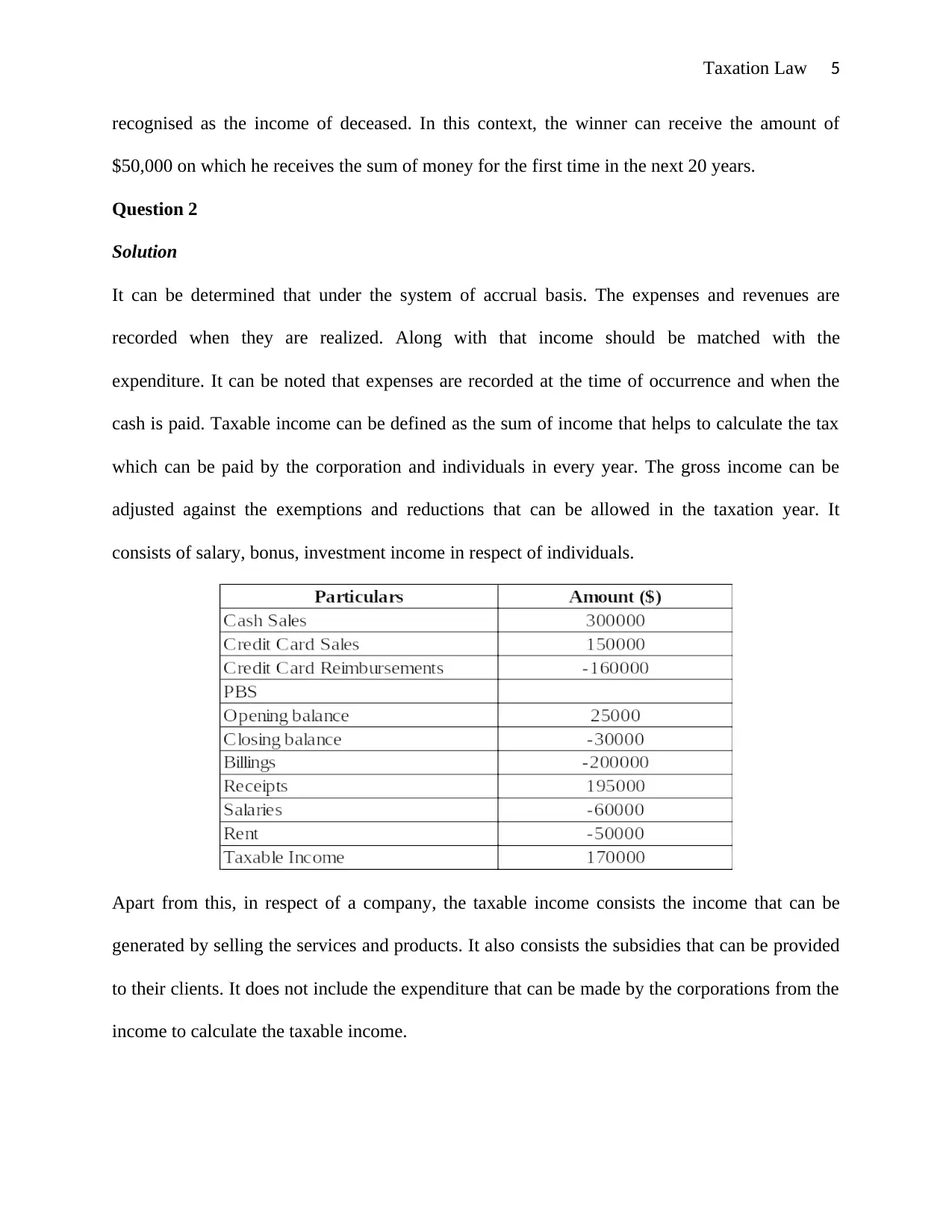

Additionally, it refers to the Pharmaceutical Benefits Scheme (PBS) that can be conducted by the

government of Australia and also it provides the subsidized drugs to their residents along with

the foreigners and that comes under the Reciprocal Health Care agreement. This type of scheme

enhances the residents and able to access the affordable an consistent range of drugs and

medicines. They also face the scrutiny that leads to the increase in cost. Corner pharmacy

calculated the taxable income as: It can be noted that corner pharmacy has followed the system

of accrual basis and that helps them to calculate the taxable income and the expenditure and the

cost of sales can be allowed as the deductions for tax purposes due to this the corner pharmacy

has the taxable income of amount of $170000.

Question 3

Solution

It can be stated that IRC V Duke of Westminister [1936] lays down the principle in which court

provided an opportunity to an individual to maintain and manage their statement of affairs in that

manner so that they can pay less tax. They have the ability to carry out this type of creative tax

planning that helps in future. In the case of Duke of Westminster they provide an opportunity in

which they hire a gardener and also make them payment of income from the income of post-tax,

but to reduce the amount of tax the Duke stops the payment of gardener rather than the covenant

and also agreed to pay the amount at the specified period. This case denotes the concept of tax

avoidance (Oishi, et. al, 2018).

It can be stated that the case tax avoidance is the condition in which the company needs to make

some arrangements to manage and control the financial statements of affairs that help to facilitate

the tax reduction of tax liability within the system of law. It can be defined as the usage or

process for the modification of the accounts of financial statements of an individual that helps to

Additionally, it refers to the Pharmaceutical Benefits Scheme (PBS) that can be conducted by the

government of Australia and also it provides the subsidized drugs to their residents along with

the foreigners and that comes under the Reciprocal Health Care agreement. This type of scheme

enhances the residents and able to access the affordable an consistent range of drugs and

medicines. They also face the scrutiny that leads to the increase in cost. Corner pharmacy

calculated the taxable income as: It can be noted that corner pharmacy has followed the system

of accrual basis and that helps them to calculate the taxable income and the expenditure and the

cost of sales can be allowed as the deductions for tax purposes due to this the corner pharmacy

has the taxable income of amount of $170000.

Question 3

Solution

It can be stated that IRC V Duke of Westminister [1936] lays down the principle in which court

provided an opportunity to an individual to maintain and manage their statement of affairs in that

manner so that they can pay less tax. They have the ability to carry out this type of creative tax

planning that helps in future. In the case of Duke of Westminster they provide an opportunity in

which they hire a gardener and also make them payment of income from the income of post-tax,

but to reduce the amount of tax the Duke stops the payment of gardener rather than the covenant

and also agreed to pay the amount at the specified period. This case denotes the concept of tax

avoidance (Oishi, et. al, 2018).

It can be stated that the case tax avoidance is the condition in which the company needs to make

some arrangements to manage and control the financial statements of affairs that help to facilitate

the tax reduction of tax liability within the system of law. It can be defined as the usage or

process for the modification of the accounts of financial statements of an individual that helps to

Taxation Law 7

deduct the value of tax and that can be paid by the taxpayer on the income that can be earned by

the individuals. They also adopt the practice in which the taxpayer less their liability of tax

which means tax evasion that lays down the illegal activities to deduct the liability of taxpayer.

In today modern era, this principle is irrelevant and substituted by the Ramsay principle. Under

this principle, the corporations made the capital gains by entering to the number of transactions

to generate the illusion in respect of capital losses that helps to avoid the capital gains than in that

case the authority has the power to charge tax on all the transactions. The reason behind this is

that the corporations manage the stages in a pre-decided manner to save the value of tax and did

not serve any saleable purpose (La Torre, et. al., 2018).

It can also be evaluated that this principle does not influence the amount of capital gain but it

consists of all different kinds of taxation and also put the condition on the taxpayer to involve in

the method of creative tax planning. There is another method in which the taxpayer has the

capability to avoid the imposition by the provision of anti-avoidance and that helps in the

execution of an equitable tax system. This provision helps in the complexities of the legislation

and there is a method of compliance cost in which the taxpayer can be self-accessed (Miles,

2017).

There is the establishment of regulation and legislation under the part IV A that can be used to

avoid the tax arrangements and that does not involve any saleable substance. This system can’t

be applied before the end of financial year to create the fear in banks and tax payers to frame the

arrangements in respect of repayment of money that can be borrowed for the saleable purpose. It

can be defined as the usage or process for the modification of the accounts of financial

statements of an individual that helps to deduct the value of tax and that can be paid by the

taxpayer on the income that can be earned by the individuals. They also adopt the practice in

deduct the value of tax and that can be paid by the taxpayer on the income that can be earned by

the individuals. They also adopt the practice in which the taxpayer less their liability of tax

which means tax evasion that lays down the illegal activities to deduct the liability of taxpayer.

In today modern era, this principle is irrelevant and substituted by the Ramsay principle. Under

this principle, the corporations made the capital gains by entering to the number of transactions

to generate the illusion in respect of capital losses that helps to avoid the capital gains than in that

case the authority has the power to charge tax on all the transactions. The reason behind this is

that the corporations manage the stages in a pre-decided manner to save the value of tax and did

not serve any saleable purpose (La Torre, et. al., 2018).

It can also be evaluated that this principle does not influence the amount of capital gain but it

consists of all different kinds of taxation and also put the condition on the taxpayer to involve in

the method of creative tax planning. There is another method in which the taxpayer has the

capability to avoid the imposition by the provision of anti-avoidance and that helps in the

execution of an equitable tax system. This provision helps in the complexities of the legislation

and there is a method of compliance cost in which the taxpayer can be self-accessed (Miles,

2017).

There is the establishment of regulation and legislation under the part IV A that can be used to

avoid the tax arrangements and that does not involve any saleable substance. This system can’t

be applied before the end of financial year to create the fear in banks and tax payers to frame the

arrangements in respect of repayment of money that can be borrowed for the saleable purpose. It

can be defined as the usage or process for the modification of the accounts of financial

statements of an individual that helps to deduct the value of tax and that can be paid by the

taxpayer on the income that can be earned by the individuals. They also adopt the practice in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation Law 8

which the taxpayer less their liability of tax which means tax evasion that lays down the illegal

activities to deduct the liability of taxpayer. In the today’s era, income tax and practice can be

adjusted and handled as per companies’ needs and individual requirements. Practice should be

adopted and applied as per deduction of tax could be done in order to pay tax by the taxpayer on

the value he earned as taxable income. In today’s time, the taxation office of Australia

scrutinizes the avoidance of tax and also inspects the affairs of tax that can be paid by the public

and private companies that are operating in Australia. They also enhance the corporation that

they are paying the right value of tax or not (La Torre, et. al., 2018).

Question 4

Solution

Capital gain can be defined as the number of capital assets that gives the high amount than the

value of purchase price. It has unrealised value until the sale of that particular assets. On the

other side, the capital loss can be defined as the value that can be obtained by the seller and that

has less value against the price of purchase. It can also be noted that the loss incurred by the

parties can be termed as the capital loss and that can be set off against the capital gain on the

rental property for the time period of 8 years. As per the case, the capital assets can be

recognised as the rental property and it can be observed that the individuals purchased the rental

property in a joint manner (Bankman, et. al, 2017). The Joseph has right to receive the 20% of

the profit from the property and wife is entitled to 80% of profit that can be gained from the

profit. Capital gain has unrealised value till the sales of that asset. On the other hand the capital

loss can be taken as the price of obtaining value that is entitled to seller and it creates less value

over purchase price. Such losses are incurred by individual parties and companies who can be set

off by capital gain over rental property. So Joseph has a right to receive 20% of amount as a

which the taxpayer less their liability of tax which means tax evasion that lays down the illegal

activities to deduct the liability of taxpayer. In the today’s era, income tax and practice can be

adjusted and handled as per companies’ needs and individual requirements. Practice should be

adopted and applied as per deduction of tax could be done in order to pay tax by the taxpayer on

the value he earned as taxable income. In today’s time, the taxation office of Australia

scrutinizes the avoidance of tax and also inspects the affairs of tax that can be paid by the public

and private companies that are operating in Australia. They also enhance the corporation that

they are paying the right value of tax or not (La Torre, et. al., 2018).

Question 4

Solution

Capital gain can be defined as the number of capital assets that gives the high amount than the

value of purchase price. It has unrealised value until the sale of that particular assets. On the

other side, the capital loss can be defined as the value that can be obtained by the seller and that

has less value against the price of purchase. It can also be noted that the loss incurred by the

parties can be termed as the capital loss and that can be set off against the capital gain on the

rental property for the time period of 8 years. As per the case, the capital assets can be

recognised as the rental property and it can be observed that the individuals purchased the rental

property in a joint manner (Bankman, et. al, 2017). The Joseph has right to receive the 20% of

the profit from the property and wife is entitled to 80% of profit that can be gained from the

profit. Capital gain has unrealised value till the sales of that asset. On the other hand the capital

loss can be taken as the price of obtaining value that is entitled to seller and it creates less value

over purchase price. Such losses are incurred by individual parties and companies who can be set

off by capital gain over rental property. So Joseph has a right to receive 20% of amount as a

Taxation Law 9

profit and his wife was entitled to 80% of profit. It should be described that loss incurred by

individual or parties.

Apart from this, if there is a loss then, in that case, Joseph has entitled to bear all the loss. In the

provide case, if the parties enter into contract and according to that, they contribute 20:80 ratio.

But later on, it can be analysed that party has loss of $40000 and that can be bear by the Joseph.

Although in this respect, a rule was framed that capital loss or capital gain is carried to next

coming years and if they occur then, in that case, it depicts the capital loss and capital gains then

this amount can be realised for the tax purposes (Artsand Fleming, 2018).

As per the fact of the case, there is a loss of around $400000 that can bear by the husband that is

Joseph and that balance can be carry forward in the present year(Meidner, et. al,. 2017). If there

is any capital gain then it could be adjusted in respect of losses and the remaining amount can be

recognised as the tax. In respect of the case, the entire amount is not the loss that is $40,000

some amount can be recognised for the purpose of the tax. For example, if the Jane and Joseph

have the revenue of $100000 then that value can be adjusted for the loss that can be occurred in

the last year. They adjusted the amount in a respective manner such as $2000 and that can be

reduced from the $40,000 and $38, 0000 can be recognised as for the purpose of tax (Huizinga,

et. al,. 2018). If capital gain is incurred and it could be adjusted in any terms of loss and

remaining value would be identified as a tax then Jane and Joseph has chance to occur in a

previous and they could adjust their profit and loss into 280:30 ratio. In all cases, capital gain can

be reduced in the purpose to adjust and value the loss occurred in previous year. In the respective

amount of taxable income, around $2000 value of reduced value would be identified as mean of

taxable income (Meidner, et. al., 2017).

profit and his wife was entitled to 80% of profit. It should be described that loss incurred by

individual or parties.

Apart from this, if there is a loss then, in that case, Joseph has entitled to bear all the loss. In the

provide case, if the parties enter into contract and according to that, they contribute 20:80 ratio.

But later on, it can be analysed that party has loss of $40000 and that can be bear by the Joseph.

Although in this respect, a rule was framed that capital loss or capital gain is carried to next

coming years and if they occur then, in that case, it depicts the capital loss and capital gains then

this amount can be realised for the tax purposes (Artsand Fleming, 2018).

As per the fact of the case, there is a loss of around $400000 that can bear by the husband that is

Joseph and that balance can be carry forward in the present year(Meidner, et. al,. 2017). If there

is any capital gain then it could be adjusted in respect of losses and the remaining amount can be

recognised as the tax. In respect of the case, the entire amount is not the loss that is $40,000

some amount can be recognised for the purpose of the tax. For example, if the Jane and Joseph

have the revenue of $100000 then that value can be adjusted for the loss that can be occurred in

the last year. They adjusted the amount in a respective manner such as $2000 and that can be

reduced from the $40,000 and $38, 0000 can be recognised as for the purpose of tax (Huizinga,

et. al,. 2018). If capital gain is incurred and it could be adjusted in any terms of loss and

remaining value would be identified as a tax then Jane and Joseph has chance to occur in a

previous and they could adjust their profit and loss into 280:30 ratio. In all cases, capital gain can

be reduced in the purpose to adjust and value the loss occurred in previous year. In the respective

amount of taxable income, around $2000 value of reduced value would be identified as mean of

taxable income (Meidner, et. al., 2017).

Taxation Law 10

Along with this share, the amount of profit that is $8000 of Jane can be recognised for the

purpose of the tax. In the given scenario, it can be stated that Joseph can set off the amount of

$40000 as the loss and that can be for the next 8 years and it was against the capital gain that can

be earned in the next coming future. By this analysis, it can be asserted that the amount of $5000

can be set off against the capital loss and that can be extended for the period f 8 years. When the

parties decide to sell the properties then it can be stated that capital gain can be realised and the

Joseph has the right of 20% of the profits. In this respect there is loss and that can be allocated

for the purpose of tax and they can incur the capital loss and capital gain. As per the fact of the

case, there is a loss of around $400000 that can bear by the husband that is Joseph and that

balance can be carry forward in the present year. If there is any capital gain then it could be

adjusted in respect of losses and the remaining amount can be recognised as the tax.

Along with this share, the amount of profit that is $8000 of Jane can be recognised for the

purpose of the tax. In the given scenario, it can be stated that Joseph can set off the amount of

$40000 as the loss and that can be for the next 8 years and it was against the capital gain that can

be earned in the next coming future. By this analysis, it can be asserted that the amount of $5000

can be set off against the capital loss and that can be extended for the period f 8 years. When the

parties decide to sell the properties then it can be stated that capital gain can be realised and the

Joseph has the right of 20% of the profits. In this respect there is loss and that can be allocated

for the purpose of tax and they can incur the capital loss and capital gain. As per the fact of the

case, there is a loss of around $400000 that can bear by the husband that is Joseph and that

balance can be carry forward in the present year. If there is any capital gain then it could be

adjusted in respect of losses and the remaining amount can be recognised as the tax.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation Law 11

Conclusion

From the above report, it can be determined that taxation plays a crucial role in the organisations.

They also identify that the taxable income of Corner pharmacy is $170000 that can be obtained

by reducing the expenditures from the revenue that can be earned by the corporations. Long with

this, there is a case of IRC V Duke of Westminster [1936] in which they establish the principle

of tax avoidance but now this concept is not relevant in today’s world. It can also be noted that

they replaced the principle of tax evasion and that is the principle of Ramsay principle. They also

set off the rental property against the capital gain and that can be for the time of 8 years and due

to that the Joseph can set the amount of $5000 and that can recover the loss of $40000 for tax. In

the overall conclusion, it is observed that tax avoidance would be replaced the facts and

principles of tax avoidance which covers real bodies of tax evasion and principle Ramsay

becomes irrelevant. This report has covered all principle and adjustments related to capital gain,

arrangements of taxable income and reduced the value of expenses from the revenue in any

company.

Conclusion

From the above report, it can be determined that taxation plays a crucial role in the organisations.

They also identify that the taxable income of Corner pharmacy is $170000 that can be obtained

by reducing the expenditures from the revenue that can be earned by the corporations. Long with

this, there is a case of IRC V Duke of Westminster [1936] in which they establish the principle

of tax avoidance but now this concept is not relevant in today’s world. It can also be noted that

they replaced the principle of tax evasion and that is the principle of Ramsay principle. They also

set off the rental property against the capital gain and that can be for the time of 8 years and due

to that the Joseph can set the amount of $5000 and that can recover the loss of $40000 for tax. In

the overall conclusion, it is observed that tax avoidance would be replaced the facts and

principles of tax avoidance which covers real bodies of tax evasion and principle Ramsay

becomes irrelevant. This report has covered all principle and adjustments related to capital gain,

arrangements of taxable income and reduced the value of expenses from the revenue in any

company.

Taxation Law 12

References

Arts, S. and Fleming, L., (2018) Paradise of Novelty—Or Loss of Human Capital? Exploring

New Fields and Inventive Output. Organization Science.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., (2017) Federal Income Taxation.

Netherlands: Wolters Kluwer Law & Business.

Cai, J., Chen, X. and Dai, M., (2017) Portfolio selection with capital gains tax, recursive utility,

and regime switching. Management Science, 64(5), pp.2308-2324.

Huizinga, H., Voget, J. and Wagner, W., (2018) Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial Economics.

La Torre, M., Dumay, J. and Rea, M.A., (2018) Breaching intellectual capital: critical reflections

on Big Data security. Meditari Accountancy Research.

Meidner, R., Hedborg, A. and Fond, G., (2017) Employee investment funds: An approach to

collective capital formation. Germany: Routledge.

Miles, J.J., (2017) Solving the problem of capital loss distribution upon dissolution of a service

partnership.

Oishi, S., Kushlev, K. and Schimmack, U., (2018) Progressive taxation, income inequality, and

happiness. American Psychologist, 73(2), pp.157.

References

Arts, S. and Fleming, L., (2018) Paradise of Novelty—Or Loss of Human Capital? Exploring

New Fields and Inventive Output. Organization Science.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., (2017) Federal Income Taxation.

Netherlands: Wolters Kluwer Law & Business.

Cai, J., Chen, X. and Dai, M., (2017) Portfolio selection with capital gains tax, recursive utility,

and regime switching. Management Science, 64(5), pp.2308-2324.

Huizinga, H., Voget, J. and Wagner, W., (2018) Capital gains taxation and the cost of capital:

Evidence from unanticipated cross-border transfers of tax base. Journal of Financial Economics.

La Torre, M., Dumay, J. and Rea, M.A., (2018) Breaching intellectual capital: critical reflections

on Big Data security. Meditari Accountancy Research.

Meidner, R., Hedborg, A. and Fond, G., (2017) Employee investment funds: An approach to

collective capital formation. Germany: Routledge.

Miles, J.J., (2017) Solving the problem of capital loss distribution upon dissolution of a service

partnership.

Oishi, S., Kushlev, K. and Schimmack, U., (2018) Progressive taxation, income inequality, and

happiness. American Psychologist, 73(2), pp.157.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.