Answer - 1 Capital gains tax a. in respect of family home

VerifiedAdded on 2022/10/17

|8

|2195

|300

AI Summary

Capital gain in respect of family home The residents of Australia can claim tax exemption on capital gain earned from the sale of the family home if only they have the ownership of that property (Yardney, 2019). Jasmine acquired and has been residing in this residential property since 1981, and as per the law, any property that is bought before 1985 will not fall under the ambit of CGT. Hence, all these details suggest that Jasmine is eligible to claim full CGT exemption on the capital gain earned from

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation

Answer – 1 Capital gains tax

a. Capital gain in respect of family home

The residents of Australia can claim tax exemption on capital gain earned from

the sale of the family home if only they have the ownership of that property

(Camp, 2019). In the given case, it can be seen that Jasmine is the owner of the

property and she has solely used the same for residential purposes only. Jasmine

has citizenship of United Kingdom and she moved to Australia long back. The

property was registered in her name and all her emails were received at this

particular address. Therefore, Jasmine qualifies all the requirements for availing

tax exemption on capital gain earned from the sale of her family home. The

residential property was purchased by Jasmine for $40,000 and the same was

sold at $650,000. This means that the residential property was sold at a capital

gain of $610,000 ($650,000-$40,000). The earnings from this residential property

cannot be taxed as Jasmine does not fall under the purview of CGT (capital gains

tax). Jasmine acquired and has been residing in this residential property since

1981, and as per the law, any property that is bought before 1985 will not fall

under the ambit of CGT.

CGT is levied in multiple countries. Even in Australia, the citizens have to pay

CGT on the capital gains earned by them from the disposal of an asset. Any asset

that has a worth of ten thousand dollars will fall under the ambit of CGT (Orem,

2019). Jasmine who is a resident of Australia is the owner of her property that

was purchased in 1981 has used this property solely for residential purposes.

Hence, all these details suggest that Jasmine is eligible to claim full CGT

exemption on the capital gain earned from the sale of her property used for

dwelling purposes (Manto, 2019).

b. The capital gain or loss made by the sale of the car

Assets like four-wheelers, motorbikes, residential property, machinery, etc that

are bought on or before September 20, 1985, is exempted from CGT. Jasmine

earned a capital loss amounting to $21,000 from the sale of her car. Jasmine will

not be liable to pay capital gains tax as there have not been any capital gains

2

Answer – 1 Capital gains tax

a. Capital gain in respect of family home

The residents of Australia can claim tax exemption on capital gain earned from

the sale of the family home if only they have the ownership of that property

(Camp, 2019). In the given case, it can be seen that Jasmine is the owner of the

property and she has solely used the same for residential purposes only. Jasmine

has citizenship of United Kingdom and she moved to Australia long back. The

property was registered in her name and all her emails were received at this

particular address. Therefore, Jasmine qualifies all the requirements for availing

tax exemption on capital gain earned from the sale of her family home. The

residential property was purchased by Jasmine for $40,000 and the same was

sold at $650,000. This means that the residential property was sold at a capital

gain of $610,000 ($650,000-$40,000). The earnings from this residential property

cannot be taxed as Jasmine does not fall under the purview of CGT (capital gains

tax). Jasmine acquired and has been residing in this residential property since

1981, and as per the law, any property that is bought before 1985 will not fall

under the ambit of CGT.

CGT is levied in multiple countries. Even in Australia, the citizens have to pay

CGT on the capital gains earned by them from the disposal of an asset. Any asset

that has a worth of ten thousand dollars will fall under the ambit of CGT (Orem,

2019). Jasmine who is a resident of Australia is the owner of her property that

was purchased in 1981 has used this property solely for residential purposes.

Hence, all these details suggest that Jasmine is eligible to claim full CGT

exemption on the capital gain earned from the sale of her property used for

dwelling purposes (Manto, 2019).

b. The capital gain or loss made by the sale of the car

Assets like four-wheelers, motorbikes, residential property, machinery, etc that

are bought on or before September 20, 1985, is exempted from CGT. Jasmine

earned a capital loss amounting to $21,000 from the sale of her car. Jasmine will

not be liable to pay capital gains tax as there have not been any capital gains

2

Taxation

earned from the sale of the car. Jasmine might have been liable to pay CGT if

there would have been any capital gains earned from the disposal of the car. It is

a known fact that capital loss can be absorbed by capital gains (Patnia, 2011).

This means that capital gains can only be used to set-off capital loss. Capital loss

earned from the disposal of long term capital assets can be set-off using long-

term capital gains. Capital loss earned from the disposal of short-term capital

assets can be set-off using both long-term capital gains and short-term capital

gains. This provision applies to all types of capital assets excluding shares.

c. The capital gain on the sale of the business

Capital gain earned from the sale of the business is partially exempted from

capital gains tax. A discount of 50 percent can be availed on the capital gain

earned from the sale of a business. Only organizations can claim this discount

and not individuals. Any individual who wishes to claim this discount shall be

over and above 55 years of age. Jasmine can claim this discount since she is 65

years old which is way higher than the required ceiling to qualify for the 50

percent exemption on capital gains that are earned from the sale of the business

(Brown, Ferguson & Sherry, 2010). As per all the calculation, it can be understood

that her business was started at least fifteen years ago as the same was

established soon after she shifted to Australia and when she shifted she was

almost nearing her retirement. The overall value of intangible and tangible assets

owned by Jasmine stands at $ 125,000. The capital gain earned by her amounts to

$50,000 and as she can claim 50% exemption on the same, therefore, her CGT is

$25,000.

d. The capital gain on selling the furniture

Assets used for personal purposes are called personal assets. Personal assets

that are worth $1,000 or anything lesser shall not be charged for CGT (Yardney,

2019). This means that the furniture owned by Jasmine shall be exempted from

the purview of capital gains tax. She can claim an exemption only on the value at

which the furniture is acquired. The furniture was purchased for $2,000 and the

same was sold at $5,000. This means that the furniture shall not fall under the

3

earned from the sale of the car. Jasmine might have been liable to pay CGT if

there would have been any capital gains earned from the disposal of the car. It is

a known fact that capital loss can be absorbed by capital gains (Patnia, 2011).

This means that capital gains can only be used to set-off capital loss. Capital loss

earned from the disposal of long term capital assets can be set-off using long-

term capital gains. Capital loss earned from the disposal of short-term capital

assets can be set-off using both long-term capital gains and short-term capital

gains. This provision applies to all types of capital assets excluding shares.

c. The capital gain on the sale of the business

Capital gain earned from the sale of the business is partially exempted from

capital gains tax. A discount of 50 percent can be availed on the capital gain

earned from the sale of a business. Only organizations can claim this discount

and not individuals. Any individual who wishes to claim this discount shall be

over and above 55 years of age. Jasmine can claim this discount since she is 65

years old which is way higher than the required ceiling to qualify for the 50

percent exemption on capital gains that are earned from the sale of the business

(Brown, Ferguson & Sherry, 2010). As per all the calculation, it can be understood

that her business was started at least fifteen years ago as the same was

established soon after she shifted to Australia and when she shifted she was

almost nearing her retirement. The overall value of intangible and tangible assets

owned by Jasmine stands at $ 125,000. The capital gain earned by her amounts to

$50,000 and as she can claim 50% exemption on the same, therefore, her CGT is

$25,000.

d. The capital gain on selling the furniture

Assets used for personal purposes are called personal assets. Personal assets

that are worth $1,000 or anything lesser shall not be charged for CGT (Yardney,

2019). This means that the furniture owned by Jasmine shall be exempted from

the purview of capital gains tax. She can claim an exemption only on the value at

which the furniture is acquired. The furniture was purchased for $2,000 and the

same was sold at $5,000. This means that the furniture shall not fall under the

3

Taxation

purview of CGT. Hence, CGT not applicable in the case of capital gain earned

from the sale of the furniture.

e. The capital gain about selling the paintings

Capital gain earned from the sale of paintings can be claimed if in any case, the

cost at which the painting was purchased is within or $500 (Sadiq et. al, 2014).

Also, these paintings must not be taken into use for revenue generation

purposes. Jasmine had two paintings that were purchased for $500 and $1000

respectively. The second painting shall be charged for CGT. CGT on paintings

must be based on the capital gain earned from the resale of the same (Black,

2019). Jasmine earned a profit of $4000 from the sale of the second painting.

Jasmine is liable to pay 50% tax on capital gain earned from the resale of

painting, therefore, her tax liability amounts to $2,000.

4

purview of CGT. Hence, CGT not applicable in the case of capital gain earned

from the sale of the furniture.

e. The capital gain about selling the paintings

Capital gain earned from the sale of paintings can be claimed if in any case, the

cost at which the painting was purchased is within or $500 (Sadiq et. al, 2014).

Also, these paintings must not be taken into use for revenue generation

purposes. Jasmine had two paintings that were purchased for $500 and $1000

respectively. The second painting shall be charged for CGT. CGT on paintings

must be based on the capital gain earned from the resale of the same (Black,

2019). Jasmine earned a profit of $4000 from the sale of the second painting.

Jasmine is liable to pay 50% tax on capital gain earned from the resale of

painting, therefore, her tax liability amounts to $2,000.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Taxation

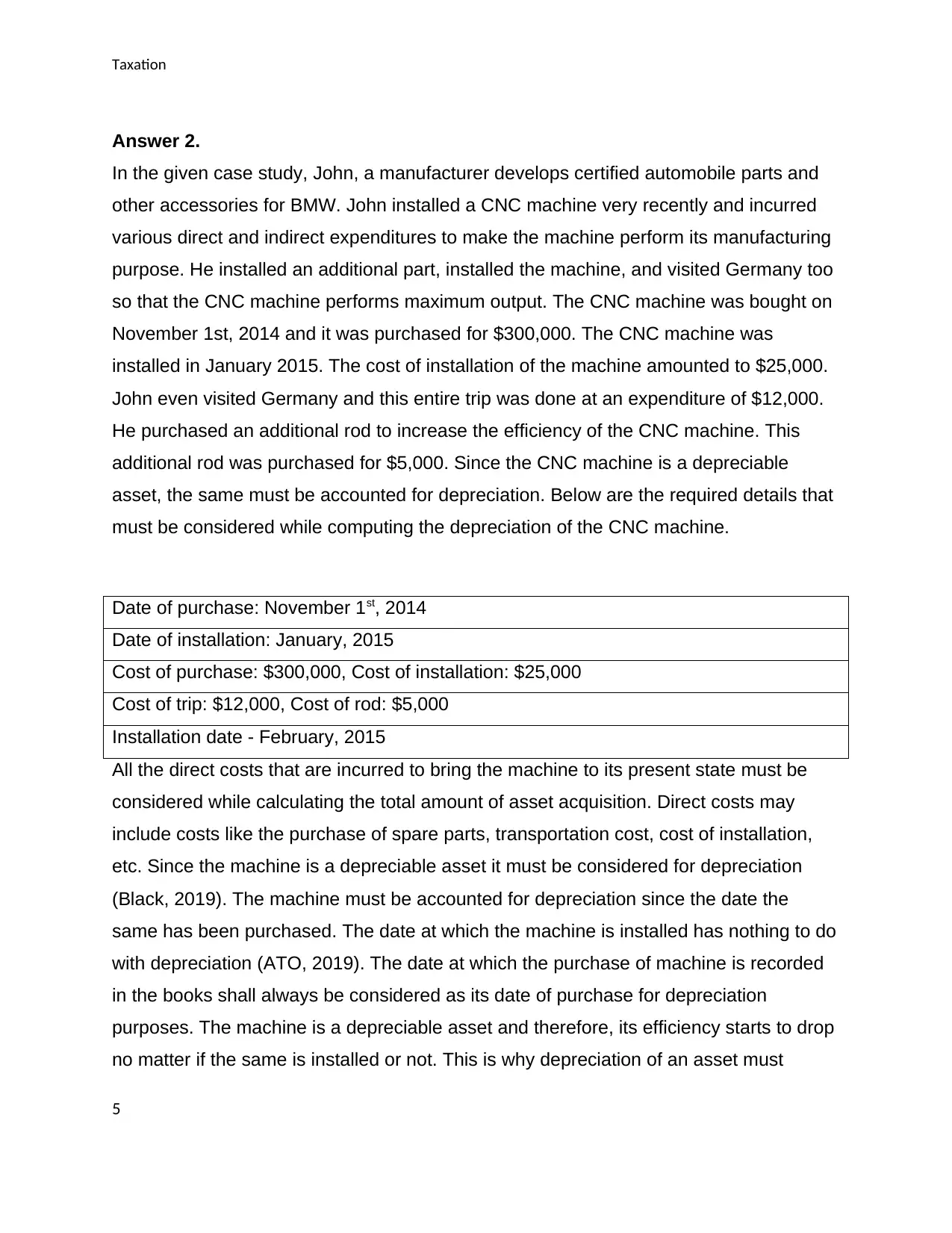

Answer 2.

In the given case study, John, a manufacturer develops certified automobile parts and

other accessories for BMW. John installed a CNC machine very recently and incurred

various direct and indirect expenditures to make the machine perform its manufacturing

purpose. He installed an additional part, installed the machine, and visited Germany too

so that the CNC machine performs maximum output. The CNC machine was bought on

November 1st, 2014 and it was purchased for $300,000. The CNC machine was

installed in January 2015. The cost of installation of the machine amounted to $25,000.

John even visited Germany and this entire trip was done at an expenditure of $12,000.

He purchased an additional rod to increase the efficiency of the CNC machine. This

additional rod was purchased for $5,000. Since the CNC machine is a depreciable

asset, the same must be accounted for depreciation. Below are the required details that

must be considered while computing the depreciation of the CNC machine.

Date of purchase: November 1st, 2014

Date of installation: January, 2015

Cost of purchase: $300,000, Cost of installation: $25,000

Cost of trip: $12,000, Cost of rod: $5,000

Installation date - February, 2015

All the direct costs that are incurred to bring the machine to its present state must be

considered while calculating the total amount of asset acquisition. Direct costs may

include costs like the purchase of spare parts, transportation cost, cost of installation,

etc. Since the machine is a depreciable asset it must be considered for depreciation

(Black, 2019). The machine must be accounted for depreciation since the date the

same has been purchased. The date at which the machine is installed has nothing to do

with depreciation (ATO, 2019). The date at which the purchase of machine is recorded

in the books shall always be considered as its date of purchase for depreciation

purposes. The machine is a depreciable asset and therefore, its efficiency starts to drop

no matter if the same is installed or not. This is why depreciation of an asset must

5

Answer 2.

In the given case study, John, a manufacturer develops certified automobile parts and

other accessories for BMW. John installed a CNC machine very recently and incurred

various direct and indirect expenditures to make the machine perform its manufacturing

purpose. He installed an additional part, installed the machine, and visited Germany too

so that the CNC machine performs maximum output. The CNC machine was bought on

November 1st, 2014 and it was purchased for $300,000. The CNC machine was

installed in January 2015. The cost of installation of the machine amounted to $25,000.

John even visited Germany and this entire trip was done at an expenditure of $12,000.

He purchased an additional rod to increase the efficiency of the CNC machine. This

additional rod was purchased for $5,000. Since the CNC machine is a depreciable

asset, the same must be accounted for depreciation. Below are the required details that

must be considered while computing the depreciation of the CNC machine.

Date of purchase: November 1st, 2014

Date of installation: January, 2015

Cost of purchase: $300,000, Cost of installation: $25,000

Cost of trip: $12,000, Cost of rod: $5,000

Installation date - February, 2015

All the direct costs that are incurred to bring the machine to its present state must be

considered while calculating the total amount of asset acquisition. Direct costs may

include costs like the purchase of spare parts, transportation cost, cost of installation,

etc. Since the machine is a depreciable asset it must be considered for depreciation

(Black, 2019). The machine must be accounted for depreciation since the date the

same has been purchased. The date at which the machine is installed has nothing to do

with depreciation (ATO, 2019). The date at which the purchase of machine is recorded

in the books shall always be considered as its date of purchase for depreciation

purposes. The machine is a depreciable asset and therefore, its efficiency starts to drop

no matter if the same is installed or not. This is why depreciation of an asset must

5

Taxation

always be accounted from the date the same has been acquired and not from its date of

installation.

The purchase of an additional spare part for the CNC machine must be regarded as a

direct cost. This is because an additional rod is purchased with an intent to increase the

output of the CNC machine. This item can be treated either as a separate line item or

cost (Hans, 2012). The additional rod is separately purchased to enhance the

productivity of the machine. Since the expenditure incurred in the purchase of an

additional rod is recognized as a direct cost, therefore, the same will be considered

while computing the total cost of the asset.

The Germany trip is completely disregarded from qualifying as a direct cost since the

same has nothing to do with enhancing the performance of the CNC machine. The

expenditure incurred on this trip is not related to increasing the productivity of the CNC

machine and therefore, it is an indirect expenditure (Yardney, 2019). The trip to

Germany was for inspecting the installation of the CNC machine only. This cost must be

entirely ignored while computing the overall cost of asset acquisition.

The cost of machine installation must be considered while computing the total cost of

the machine. Installation cost is a necessary expenditure and therefore, it will be

regarded as a direct cost. On November 1st, 2014 the CNC machine was purchased

and the same was installed in January 2015. The machine was installed for $25,000.

The CNC machine will be charged for depreciation from the date at which the same is

purchased or recorded in the books irrespective of when the same is taken into use.

Installing an additional rod is surely a direct expenditure since it aided in enhancing the

efficiency and productivity of the CNC machine. The rod installed will also be accounted

for depreciation. The trip to Germany is an indirect expenditure since it had nothing to

do with enhancing the productivity and functioning of the CNC machine. The installation

cost incurred is a necessary expenditure because if the machine is not installed then

how the same can fulfill the purpose for which it is bought (Yardney, 2019). The total

cost of asset acquisition can be calculated by adding the purchase cost of the machine,

6

always be accounted from the date the same has been acquired and not from its date of

installation.

The purchase of an additional spare part for the CNC machine must be regarded as a

direct cost. This is because an additional rod is purchased with an intent to increase the

output of the CNC machine. This item can be treated either as a separate line item or

cost (Hans, 2012). The additional rod is separately purchased to enhance the

productivity of the machine. Since the expenditure incurred in the purchase of an

additional rod is recognized as a direct cost, therefore, the same will be considered

while computing the total cost of the asset.

The Germany trip is completely disregarded from qualifying as a direct cost since the

same has nothing to do with enhancing the performance of the CNC machine. The

expenditure incurred on this trip is not related to increasing the productivity of the CNC

machine and therefore, it is an indirect expenditure (Yardney, 2019). The trip to

Germany was for inspecting the installation of the CNC machine only. This cost must be

entirely ignored while computing the overall cost of asset acquisition.

The cost of machine installation must be considered while computing the total cost of

the machine. Installation cost is a necessary expenditure and therefore, it will be

regarded as a direct cost. On November 1st, 2014 the CNC machine was purchased

and the same was installed in January 2015. The machine was installed for $25,000.

The CNC machine will be charged for depreciation from the date at which the same is

purchased or recorded in the books irrespective of when the same is taken into use.

Installing an additional rod is surely a direct expenditure since it aided in enhancing the

efficiency and productivity of the CNC machine. The rod installed will also be accounted

for depreciation. The trip to Germany is an indirect expenditure since it had nothing to

do with enhancing the productivity and functioning of the CNC machine. The installation

cost incurred is a necessary expenditure because if the machine is not installed then

how the same can fulfill the purpose for which it is bought (Yardney, 2019). The total

cost of asset acquisition can be calculated by adding the purchase cost of the machine,

6

Taxation

its installation cost and the cost of additional rod. Hence, the overall cost of machine

amounts to $330,000 ($300,000+$25,000+$5,000). The machine will be charged for the

depreciation that amounts to $12,000. The amount of depreciation shall be reported to

the Profit/Loss Account.

7

its installation cost and the cost of additional rod. Hence, the overall cost of machine

amounts to $330,000 ($300,000+$25,000+$5,000). The machine will be charged for the

depreciation that amounts to $12,000. The amount of depreciation shall be reported to

the Profit/Loss Account.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Taxation

References

ATO 2019, Capital gains Tax 2019, viewed on 20 September 2019 <

https://www.ato.gov.au/General/Capital-gains-tax/

Black, E 2019, What is Capital Gains Tax and how do I calculate it?, viewed on 24

September 2019, https://www.realestate.com.au/advice/what-is-capital-gains-tax/

Brown, P., Ferguson, A., & Sherry, S 2010, Investor behaviour in response to

Australia's capital gains tax, Accounting and Finance, vol. 50, no. 4, pp. 783, viewed 20

September 2019 <https://search.proquest.com/docview/762714715?accountid=30552

Camp, A 2019, How to avoid capital gains tax when selling property, viewed 23

September 2019, https://www.finder.com/avoid-capital-gains-tax-when-selling-property

Hans, P.P 2012, Ensuring a Softer Grip, viewed 24 September 2019

https://www.businesstoday.in/moneytoday/tax/property-selling-profit-lowering-

tax-liability/story/189407.html

Manto, A 2019, How you can avoid paying Capital Gain Tax on your investment

property, viewed 24 September 2019

https://www.nowtolove.com.au/lifestyle/money/how-to-avoid paying-capital-gains-

tax-investment-property-33505

Orem, T 2019, Selling a House? Avoid Taxes on Capital Gains on Real Estate in 2018

and 2019, viewed 24 September 2019

https://www.nerdwallet.com/blog/taxes/selling-home-capital-gains-tax/

Patnia, A 2011, No Capital gain tax or income tax on profit on sale of a car or other

personal effect, viewed 20 September 2019, https://taxmantra.com/capital-gain-tax-

income-tax-profit-sale-car-personal-effect/

Sadiq,K., Coleman, C., Hanegbi, R., Jogarajan,S., Krever, R.,Obst, W., & Ting, A 2014,

Principles of Taxation Law, Sydney.

Yardney, M 2019, A Complete Guide to Capital Gains Tax, viewed on 24 September

2019, https://propertyupdate.com.au/a-complete-guide-to-capital-gains-tax/>

8

References

ATO 2019, Capital gains Tax 2019, viewed on 20 September 2019 <

https://www.ato.gov.au/General/Capital-gains-tax/

Black, E 2019, What is Capital Gains Tax and how do I calculate it?, viewed on 24

September 2019, https://www.realestate.com.au/advice/what-is-capital-gains-tax/

Brown, P., Ferguson, A., & Sherry, S 2010, Investor behaviour in response to

Australia's capital gains tax, Accounting and Finance, vol. 50, no. 4, pp. 783, viewed 20

September 2019 <https://search.proquest.com/docview/762714715?accountid=30552

Camp, A 2019, How to avoid capital gains tax when selling property, viewed 23

September 2019, https://www.finder.com/avoid-capital-gains-tax-when-selling-property

Hans, P.P 2012, Ensuring a Softer Grip, viewed 24 September 2019

https://www.businesstoday.in/moneytoday/tax/property-selling-profit-lowering-

tax-liability/story/189407.html

Manto, A 2019, How you can avoid paying Capital Gain Tax on your investment

property, viewed 24 September 2019

https://www.nowtolove.com.au/lifestyle/money/how-to-avoid paying-capital-gains-

tax-investment-property-33505

Orem, T 2019, Selling a House? Avoid Taxes on Capital Gains on Real Estate in 2018

and 2019, viewed 24 September 2019

https://www.nerdwallet.com/blog/taxes/selling-home-capital-gains-tax/

Patnia, A 2011, No Capital gain tax or income tax on profit on sale of a car or other

personal effect, viewed 20 September 2019, https://taxmantra.com/capital-gain-tax-

income-tax-profit-sale-car-personal-effect/

Sadiq,K., Coleman, C., Hanegbi, R., Jogarajan,S., Krever, R.,Obst, W., & Ting, A 2014,

Principles of Taxation Law, Sydney.

Yardney, M 2019, A Complete Guide to Capital Gains Tax, viewed on 24 September

2019, https://propertyupdate.com.au/a-complete-guide-to-capital-gains-tax/>

8

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.