Enhancing the Integrity and Functionality of Division 7A of the ITAA 1997

VerifiedAdded on 2019/11/29

|13

|2969

|150

Report

AI Summary

The assignment content discusses the amendments made to Division 7A of the Income Tax Assessment Act (ITAA) 1997, which aims to simplify the process and management of tax payers by providing guidelines for maintaining compliance with policy intentions. The division ensures that profits are not circulated to all owners of a corporation, and violations can result in payments of dividends from earned profits on which taxes are charged. The amendments aim to make it simpler and easier for taxpayers to fix inadvertent liabilities under Division 7A.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Taxation Law

Name of the Student

Name of the University

Authors Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2TAXATION LAW

Table of Contents

Category 1: Assessable Earnings...............................................................................................2

Solution to Question 2:...............................................................................................................2

Solution to Question 4:...............................................................................................................4

Category 2:.................................................................................................................................5

Solution to Question 3:...............................................................................................................5

Detailed Discussion:...................................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

Table of Contents

Category 1: Assessable Earnings...............................................................................................2

Solution to Question 2:...............................................................................................................2

Solution to Question 4:...............................................................................................................4

Category 2:.................................................................................................................................5

Solution to Question 3:...............................................................................................................5

Detailed Discussion:...................................................................................................................6

Conclusion..................................................................................................................................7

References..................................................................................................................................8

3TAXATION LAW

Category 1: Assessable Earnings

Solution to Question 2:

Issue

In particular, this particular issue deals with specific outcomes of income tax along with

capital gains mentioned specifically under the stipulation under sub section 160 M (6) as well

as 160M (7) (Ato.gov.au 2017). The guidelines mentioned under the 160 M (6) talks about

the defensive agreements as well as business relationships appropriately pointed out in the

ITAA 1936 (Anderson et al. 2016).

Specific legislation:

Application:

The taxation ruling of TR 95/3 defines about different outcomes of both income tax as well as

capital gain that are pertinent specifically within the purview of subsections 160 M (6) and

160 M (7) (Bauer 2016). This explains about diverse restrictive covenants along employment

ties that are illustrated under the guidelines stipulated under ITAA of 1936 (Barkoczy 2016).

Particularly, nature as well as features of employment is linked to the agreements and

compensations that is explained under the service contract case of FC of T v. Woite 82 ATC

4578; (1982. According to this particular verdict explicated by this case, it can be hereby

Category 1: Assessable Earnings

Solution to Question 2:

Issue

In particular, this particular issue deals with specific outcomes of income tax along with

capital gains mentioned specifically under the stipulation under sub section 160 M (6) as well

as 160M (7) (Ato.gov.au 2017). The guidelines mentioned under the 160 M (6) talks about

the defensive agreements as well as business relationships appropriately pointed out in the

ITAA 1936 (Anderson et al. 2016).

Specific legislation:

Application:

The taxation ruling of TR 95/3 defines about different outcomes of both income tax as well as

capital gain that are pertinent specifically within the purview of subsections 160 M (6) and

160 M (7) (Bauer 2016). This explains about diverse restrictive covenants along employment

ties that are illustrated under the guidelines stipulated under ITAA of 1936 (Barkoczy 2016).

Particularly, nature as well as features of employment is linked to the agreements and

compensations that is explained under the service contract case of FC of T v. Woite 82 ATC

4578; (1982. According to this particular verdict explicated by this case, it can be hereby

4TAXATION LAW

mentioned the sum for restricting the player from gaining the opportunity to play that else

wise could have been available to the player. Essentially, this advances the query regarding

the amount of receipt for one of the defensive contracts or else for any other form of

disconnected or else positive covenants in which the least amount for payment that is

accepted is regarded as an assessable earning (Braithwaite 2017).

It is hereby apparent from the above mentioned fact that defensive agreement is related to the

present time period of employment together with the closing period of employment. In this

case, the fraction of the specific consideration that is accepted for the employment period can

be considered as taxable earning directed under the guidelines stipulated under the sub

section legislation 25 (1) or paragraph 26 (e) (Law.ato.gov.au 2017)

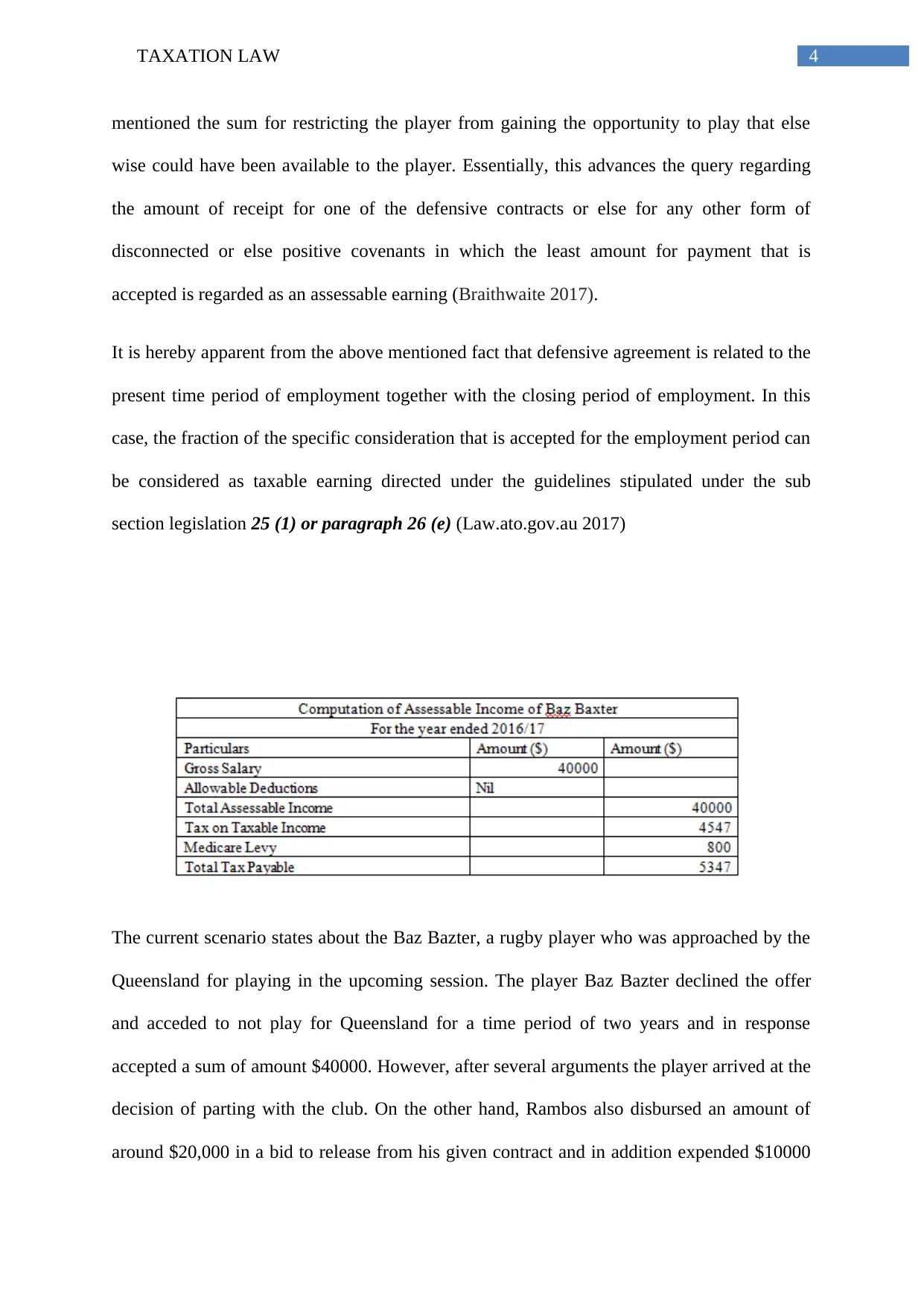

The current scenario states about the Baz Bazter, a rugby player who was approached by the

Queensland for playing in the upcoming session. The player Baz Bazter declined the offer

and acceded to not play for Queensland for a time period of two years and in response

accepted a sum of amount $40000. However, after several arguments the player arrived at the

decision of parting with the club. On the other hand, Rambos also disbursed an amount of

around $20,000 in a bid to release from his given contract and in addition expended $10000

mentioned the sum for restricting the player from gaining the opportunity to play that else

wise could have been available to the player. Essentially, this advances the query regarding

the amount of receipt for one of the defensive contracts or else for any other form of

disconnected or else positive covenants in which the least amount for payment that is

accepted is regarded as an assessable earning (Braithwaite 2017).

It is hereby apparent from the above mentioned fact that defensive agreement is related to the

present time period of employment together with the closing period of employment. In this

case, the fraction of the specific consideration that is accepted for the employment period can

be considered as taxable earning directed under the guidelines stipulated under the sub

section legislation 25 (1) or paragraph 26 (e) (Law.ato.gov.au 2017)

The current scenario states about the Baz Bazter, a rugby player who was approached by the

Queensland for playing in the upcoming session. The player Baz Bazter declined the offer

and acceded to not play for Queensland for a time period of two years and in response

accepted a sum of amount $40000. However, after several arguments the player arrived at the

decision of parting with the club. On the other hand, Rambos also disbursed an amount of

around $20,000 in a bid to release from his given contract and in addition expended $10000

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

5TAXATION LAW

to release Baz for wrapping up the expenditure incurred for moving from a specific club to

another one. Thus, as per the sub section mentioned under the sub section 160 M (6)

acceptance receipt of a fraction of consideration that is in any way related to the employment

phase after the closing of the service can be regarded as an assessable earning

(Law.ato.gov.au 2017).

In this regard, the reference to the situation of Baz can be considered that helps in explaining

the taxation ruling mentioned under the directives of Taxation Ruling of TR 95/3 (Miller and

Oats 2016). This ruling helps in explaining the outcomes of the consequences of the decision

declared by the high court in the legal case of (“Hepples v. FC of T (1991) 173 CLR 492”)

for the purpose of treating the taxable earning of the receipt of considerations in association

to specific restrictive covenants. The acceptance of the payment for different restrictive

covenants is related to the present employment period and after the employment period for

particularly the considerations accepted can be considered for evaluation under the rulings

mentioned under the sub-section 25(1) (Mitchell et al. 2016). This is so because it is

connected to the employment phase.

Concluding statement:

The acceptance of restrictive compensation by the rugby player Baz can be related to the

present employment period. In addition to this, the payment or the fraction of consideration

received subsequent to the period of service can also be related to the employment period

and can be regarded as taxable earning under the ruling mentioned under sub-section 25(1).

Solution to Question 4:

Identified Issue:

to release Baz for wrapping up the expenditure incurred for moving from a specific club to

another one. Thus, as per the sub section mentioned under the sub section 160 M (6)

acceptance receipt of a fraction of consideration that is in any way related to the employment

phase after the closing of the service can be regarded as an assessable earning

(Law.ato.gov.au 2017).

In this regard, the reference to the situation of Baz can be considered that helps in explaining

the taxation ruling mentioned under the directives of Taxation Ruling of TR 95/3 (Miller and

Oats 2016). This ruling helps in explaining the outcomes of the consequences of the decision

declared by the high court in the legal case of (“Hepples v. FC of T (1991) 173 CLR 492”)

for the purpose of treating the taxable earning of the receipt of considerations in association

to specific restrictive covenants. The acceptance of the payment for different restrictive

covenants is related to the present employment period and after the employment period for

particularly the considerations accepted can be considered for evaluation under the rulings

mentioned under the sub-section 25(1) (Mitchell et al. 2016). This is so because it is

connected to the employment phase.

Concluding statement:

The acceptance of restrictive compensation by the rugby player Baz can be related to the

present employment period. In addition to this, the payment or the fraction of consideration

received subsequent to the period of service can also be related to the employment period

and can be regarded as taxable earning under the ruling mentioned under sub-section 25(1).

Solution to Question 4:

Identified Issue:

6TAXATION LAW

This present issue can be associated to the deduction of expends that has happened after the

conclusion of the business. The identified issue introduces the specific question mark

regarding whether the payer of tax can be allowed or provided deductions in line with the

regulations mentioned under the sub-section 8-1 of the Income Tax Assessment Act 1997

for different legal expends that are essentially incurred after the conclusion of the business

(Parker 2015).

Relevant legislations:

Specific Application:

The decision mentioned under the ID 2003/210 takes into consideration the overall

entitlement to different allowable deductions mentioned under the directives of section 8-1 of

the Income Tax Assessment Act 1997 as regards specific legal disbursements after the

conclusion of business actions (Pearce and Pinto 2015). The directives mentioned therein

refers to the fact that taxpayers can consider certain expends for permissible deductions

mentioned under the section of the ruling 8-1 of the ITAA 1997 as has occurred after the

termination of the actions of business and that is particularly incurred in the past business

actions.

It is apparent from the present case that the tax payer undertook the activities of the trade of

ship building. After the onset of period of recession, the tax payer stopped the business

activities shortly before the Christmas. Immediately after the disposal of the assets/resources

of the business concern Waterside Investment Pty Ltd was incepted. The business entitiy

This present issue can be associated to the deduction of expends that has happened after the

conclusion of the business. The identified issue introduces the specific question mark

regarding whether the payer of tax can be allowed or provided deductions in line with the

regulations mentioned under the sub-section 8-1 of the Income Tax Assessment Act 1997

for different legal expends that are essentially incurred after the conclusion of the business

(Parker 2015).

Relevant legislations:

Specific Application:

The decision mentioned under the ID 2003/210 takes into consideration the overall

entitlement to different allowable deductions mentioned under the directives of section 8-1 of

the Income Tax Assessment Act 1997 as regards specific legal disbursements after the

conclusion of business actions (Pearce and Pinto 2015). The directives mentioned therein

refers to the fact that taxpayers can consider certain expends for permissible deductions

mentioned under the section of the ruling 8-1 of the ITAA 1997 as has occurred after the

termination of the actions of business and that is particularly incurred in the past business

actions.

It is apparent from the present case that the tax payer undertook the activities of the trade of

ship building. After the onset of period of recession, the tax payer stopped the business

activities shortly before the Christmas. Immediately after the disposal of the assets/resources

of the business concern Waterside Investment Pty Ltd was incepted. The business entitiy

7TAXATION LAW

Waterside Investment Pty Ltd made payments to the workers as per the agreed amount of

compensation for the purpose of settlement after the wind up of the parent concern (Pearson

2017).

However, the legal case Placer Pacific Management Pty Ltd v. FC of T 95 ATC 4459;

(1995) 31 ATR 253 mentions that the payer of tax is a manufacturer of conveyer belt

(ROBIN 2017). The decision of selling off the business to another concern was undertaken.

In accordance to the contract sales agreement, the corporation was held accountable for

different repairs that essentially originated from the establishment of the system prior to the

period of sale. The consideration for allowable deductions for expends carried out, the verdict

of the case passed by the Federal court for AGC (Advances) Ltd v. Federal Commissioner of

Taxation (1975) can be hereby referred to (Wu 2015). The circumstances under which the

disbursements took place during the latter half of the year might have ended and would

necessarily not be considered as a particular of deductibility. However, in the present case,

the claim for the compensation was made in the shape of outgoing right after the winding up

of the business. As per the rulings mentioned under the sub-section 8-1 of the guideline ITAA

of the year 1997 the business entity Waterside Investment Pty Ltd can claim for the

deductions for the specific compensation that particularly stemmed for the settlement of

Payment Company already liquidated.

Conclusion

In conclusion it can be said that the legal expends that is taken into consideration in the

present business case of Waterside Investment Pty Ltd can be considered as permissible

deduction as it was incurred for the purpose of settlement of fee after the liquidation of the

business.

Waterside Investment Pty Ltd made payments to the workers as per the agreed amount of

compensation for the purpose of settlement after the wind up of the parent concern (Pearson

2017).

However, the legal case Placer Pacific Management Pty Ltd v. FC of T 95 ATC 4459;

(1995) 31 ATR 253 mentions that the payer of tax is a manufacturer of conveyer belt

(ROBIN 2017). The decision of selling off the business to another concern was undertaken.

In accordance to the contract sales agreement, the corporation was held accountable for

different repairs that essentially originated from the establishment of the system prior to the

period of sale. The consideration for allowable deductions for expends carried out, the verdict

of the case passed by the Federal court for AGC (Advances) Ltd v. Federal Commissioner of

Taxation (1975) can be hereby referred to (Wu 2015). The circumstances under which the

disbursements took place during the latter half of the year might have ended and would

necessarily not be considered as a particular of deductibility. However, in the present case,

the claim for the compensation was made in the shape of outgoing right after the winding up

of the business. As per the rulings mentioned under the sub-section 8-1 of the guideline ITAA

of the year 1997 the business entity Waterside Investment Pty Ltd can claim for the

deductions for the specific compensation that particularly stemmed for the settlement of

Payment Company already liquidated.

Conclusion

In conclusion it can be said that the legal expends that is taken into consideration in the

present business case of Waterside Investment Pty Ltd can be considered as permissible

deduction as it was incurred for the purpose of settlement of fee after the liquidation of the

business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8TAXATION LAW

Category 2:

Solution to Question 3:

During the year 2016-2017, the government made announcement regarding certain

amendments that will be carried out for enhancement of operations as well as proper

administration of the Division 7A of the Income Tax Assessment Act of the year 1936

(Anderson et al. 2016). Essentially, these amendments or in other words the modifications

shall be considered for the purpose of application on and from the period July 1 of the year

2018. As such, the modifications are supposed to introduce different mechanisms for self

corrections for the helping tax payers to rectify different unintentional breaches of the rulings

of the Division 7A.

The amendments mentioned therein under the Division 7A intends to deliver safe regulations

by implementation of certainty along with the ease of adherence to rules for the tax payers.

Fundamentally, the primary aim of the amendments is to simplify the regulations as

mentioned under Division 7A that talks about loans, span of loans along with the least

amount of interest that can be paid for the loans (Barkoczy 2016). In addition to this, the

amendments also refer to different minimum amounts of modifications that can help in

enhancing the overall integrity as well as the functionalities of the rulings mentioned under

Division 7A for the purpose of delivering better assurance to the payers of tax.

Detailed Discussion:

It can be hereby stated that the government has stressed the importance of improving the

process as well as proper management of the particularly Division 7A of the ITAA 1997. The

intended alterations are expected to present guidelines to all the payers of tax that in turn can

ensure simplification of the burden of maintenance of compliance by proper maintenance of

Category 2:

Solution to Question 3:

During the year 2016-2017, the government made announcement regarding certain

amendments that will be carried out for enhancement of operations as well as proper

administration of the Division 7A of the Income Tax Assessment Act of the year 1936

(Anderson et al. 2016). Essentially, these amendments or in other words the modifications

shall be considered for the purpose of application on and from the period July 1 of the year

2018. As such, the modifications are supposed to introduce different mechanisms for self

corrections for the helping tax payers to rectify different unintentional breaches of the rulings

of the Division 7A.

The amendments mentioned therein under the Division 7A intends to deliver safe regulations

by implementation of certainty along with the ease of adherence to rules for the tax payers.

Fundamentally, the primary aim of the amendments is to simplify the regulations as

mentioned under Division 7A that talks about loans, span of loans along with the least

amount of interest that can be paid for the loans (Barkoczy 2016). In addition to this, the

amendments also refer to different minimum amounts of modifications that can help in

enhancing the overall integrity as well as the functionalities of the rulings mentioned under

Division 7A for the purpose of delivering better assurance to the payers of tax.

Detailed Discussion:

It can be hereby stated that the government has stressed the importance of improving the

process as well as proper management of the particularly Division 7A of the ITAA 1997. The

intended alterations are expected to present guidelines to all the payers of tax that in turn can

ensure simplification of the burden of maintenance of compliance by proper maintenance of

9TAXATION LAW

integrity as well as policy intention of the Division 7A of the ITAA 1997 (Barkoczy 2016).

Essentially Division 7A of the ITAA 1997 can be regarded as an effectual provision of

reliability that can help in ascertainment of the fact that profits are not circulated to all the

owners of the corporation.

It is discovered that in case if Division 7A is violated then the payers of the tax can be

observed to make payments of dividends from the earned profits on which taxes are charged.

However, it is exclusive of all the advantages of credits. As such, it can be mentioned that the

Division 7A are very complicated to understand as they are very lengthy. Particularly, a

specific individual can certainly commit a error for which corrective actions are obligatory

for averting the severity of the regulations. In this present scenario, in case if the payer of tax

is considered under the Division 7A, the substitutes of taking up corrective actions are very

much restricted (Law.ato.gov.au 2017). Essentially, these mainly consist of treatment of

amount that is withdrawn from the business concern as loan with a minimum principle and

terms of reimbursement of interest. Again, payers of tax can be delivered with the alternatives

of implementing to the representative for relief. This also consists of affecting the

commissioner in a bid to carry out the discretion to disregard the deemed dividend or permit

it to be franked under certain situations.

As rightly indicated by Barkoczy (2016), the commissioner power is essentially to carry out

in a discretionary and comprehensive manner and it is available to the payers of tax that have

candid fault or else an unintentional omission. Again, it also consists of different state of

affairs that is ahead of the control of the payers of tax. They might also suffer the hardships in

case if the loans are regarded as dividend. Essentially, the federal government referred to the

fact that it might also impose the alterations that might possibly make it uncomplicated and

simple to fix and bear inadvertent liability of the rulings of Division 7A.

integrity as well as policy intention of the Division 7A of the ITAA 1997 (Barkoczy 2016).

Essentially Division 7A of the ITAA 1997 can be regarded as an effectual provision of

reliability that can help in ascertainment of the fact that profits are not circulated to all the

owners of the corporation.

It is discovered that in case if Division 7A is violated then the payers of the tax can be

observed to make payments of dividends from the earned profits on which taxes are charged.

However, it is exclusive of all the advantages of credits. As such, it can be mentioned that the

Division 7A are very complicated to understand as they are very lengthy. Particularly, a

specific individual can certainly commit a error for which corrective actions are obligatory

for averting the severity of the regulations. In this present scenario, in case if the payer of tax

is considered under the Division 7A, the substitutes of taking up corrective actions are very

much restricted (Law.ato.gov.au 2017). Essentially, these mainly consist of treatment of

amount that is withdrawn from the business concern as loan with a minimum principle and

terms of reimbursement of interest. Again, payers of tax can be delivered with the alternatives

of implementing to the representative for relief. This also consists of affecting the

commissioner in a bid to carry out the discretion to disregard the deemed dividend or permit

it to be franked under certain situations.

As rightly indicated by Barkoczy (2016), the commissioner power is essentially to carry out

in a discretionary and comprehensive manner and it is available to the payers of tax that have

candid fault or else an unintentional omission. Again, it also consists of different state of

affairs that is ahead of the control of the payers of tax. They might also suffer the hardships in

case if the loans are regarded as dividend. Essentially, the federal government referred to the

fact that it might also impose the alterations that might possibly make it uncomplicated and

simple to fix and bear inadvertent liability of the rulings of Division 7A.

10TAXATION LAW

As rightly put forward by Barkoczy (2016), measures assumed are necessarily in the direction

of improvement of the existing functions and management of specifically Division 7A that

can be accepted by corporations and advisors of tax. In particular, Division 7A can be

regarded as one of the many-sided and difficult areas for inadvertent violations and safe

harbours. In essence, this can be observed as an assistance to get relief from the possible

severity of the regulations of Division 7A.

According to the taxation board, it can be comprehended that there is a considerable amount

of scope for enhancement of divisions in a manner that can be complemented with the

assistance of restructuring. Basically, as mentioned in the stipulations mentioned under

rulings of Division 7A, the first step is to create a reasonable set of policy standards. Again,

this can prove to be beneficial for the investment that is financed by profits and the similar

thing can be taxed at a corporate rate over re-investment that is of the business revenues from

the dormant revenues from the business (Anderson et al. 2016).

As mentioned by Bauer (2016), the board believe that protecting the progressiveness of the

taxation arrangement that need not be at the cost of obstructing the capability of the business

in a bid to reinvest the earning as working capital. Reinvestment strategies aids in generating

augmented productivity and commercial growth. Contrarily the private use of different

business proceeds serves the purpose of accumulation of private wealth. Essentially, the

higher level of taxation policy necessarily helps in the process of generation of efficacy,

simplicity along with equity since the board has generated a structure of policy that is in

agreement with the classified business designed to present proper balance between different

competing firms. It is particularly developed to measure the current regime and developing

the models of restructuring. Bauer (2016) opined that the board regard superior level of tax

policy as a way of attainment of simplicity as well as equity.

As rightly put forward by Barkoczy (2016), measures assumed are necessarily in the direction

of improvement of the existing functions and management of specifically Division 7A that

can be accepted by corporations and advisors of tax. In particular, Division 7A can be

regarded as one of the many-sided and difficult areas for inadvertent violations and safe

harbours. In essence, this can be observed as an assistance to get relief from the possible

severity of the regulations of Division 7A.

According to the taxation board, it can be comprehended that there is a considerable amount

of scope for enhancement of divisions in a manner that can be complemented with the

assistance of restructuring. Basically, as mentioned in the stipulations mentioned under

rulings of Division 7A, the first step is to create a reasonable set of policy standards. Again,

this can prove to be beneficial for the investment that is financed by profits and the similar

thing can be taxed at a corporate rate over re-investment that is of the business revenues from

the dormant revenues from the business (Anderson et al. 2016).

As mentioned by Bauer (2016), the board believe that protecting the progressiveness of the

taxation arrangement that need not be at the cost of obstructing the capability of the business

in a bid to reinvest the earning as working capital. Reinvestment strategies aids in generating

augmented productivity and commercial growth. Contrarily the private use of different

business proceeds serves the purpose of accumulation of private wealth. Essentially, the

higher level of taxation policy necessarily helps in the process of generation of efficacy,

simplicity along with equity since the board has generated a structure of policy that is in

agreement with the classified business designed to present proper balance between different

competing firms. It is particularly developed to measure the current regime and developing

the models of restructuring. Bauer (2016) opined that the board regard superior level of tax

policy as a way of attainment of simplicity as well as equity.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

11TAXATION LAW

Conclusion

In conclusion, it can be said that the corporate structure of business acquires the advantages

of restricting taxation to rate of the company without allocating the gains out of the specific

units. In case if the business functions with the assistance of the open trust then it can become

difficult to attain the cap of corporate tax rate at a specific stage. In this case the distribution

of tax to diverse individuals can surpass the business rate. Thus, it can be concluded that

Division 7A assists in the process of inspiring the corporation in distributing the gains under

specific circumstances in which the shareholders can acquire the accessibility of the profits.

Conclusion

In conclusion, it can be said that the corporate structure of business acquires the advantages

of restricting taxation to rate of the company without allocating the gains out of the specific

units. In case if the business functions with the assistance of the open trust then it can become

difficult to attain the cap of corporate tax rate at a specific stage. In this case the distribution

of tax to diverse individuals can surpass the business rate. Thus, it can be concluded that

Division 7A assists in the process of inspiring the corporation in distributing the gains under

specific circumstances in which the shareholders can acquire the accessibility of the profits.

12TAXATION LAW

References

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Ato.gov.au. 2017. Legal Database. [online] Available at:

https://www.ato.gov.au/law/view/document?docid=PAC/19970038/8-1 [Accessed 7 Sep.

2017].

Barkoczy, S. 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bauer, A. M. 2016. Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Law.ato.gov.au. (2017). TR 95/3 - Income tax and capital gains: application of subsections

160M(6) and 160M(7) to restrictive covenants and trade ties (As at 29 October 2006).

[online] Available at:

http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR953/NAT/ATO%27 [Accessed 7

Sep. 2017].

Law.ato.gov.au. 2017. ATO ID 2003/210 (Withdrawn) - Deductibility of legal expenses

incurred after cessation of business. [online] Available at:

http://law.ato.gov.au/atolaw/view.htm?docid=AID/AID2003210/00001 [Accessed 7 Sep.

2017].

Miller, A., and Oats, L. 2016. Principles of international taxation. Bloomsbury Publishing.

References

Anderson, C., Dickfos, J. and Brown, C., 2016. The Australian Taxation Office-what role

does it play in anti-phoenix activity?. INSOLVENCY LAW JOURNAL, 24(2), pp.127-140.

Ato.gov.au. 2017. Legal Database. [online] Available at:

https://www.ato.gov.au/law/view/document?docid=PAC/19970038/8-1 [Accessed 7 Sep.

2017].

Barkoczy, S. 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Bauer, A. M. 2016. Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Law.ato.gov.au. (2017). TR 95/3 - Income tax and capital gains: application of subsections

160M(6) and 160M(7) to restrictive covenants and trade ties (As at 29 October 2006).

[online] Available at:

http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR953/NAT/ATO%27 [Accessed 7

Sep. 2017].

Law.ato.gov.au. 2017. ATO ID 2003/210 (Withdrawn) - Deductibility of legal expenses

incurred after cessation of business. [online] Available at:

http://law.ato.gov.au/atolaw/view.htm?docid=AID/AID2003210/00001 [Accessed 7 Sep.

2017].

Miller, A., and Oats, L. 2016. Principles of international taxation. Bloomsbury Publishing.

13TAXATION LAW

Mitchell, R., O'Donnell, A., Marshall, S., and Ramsay, I. 2016. Law, corporate governance

and partnerships at work: a study of australian regulatory style and business practice.

Routledge.

Parker, M., 2015. Division 7A and winding up structures. Taxation in Australia, 50(6), p.312.

Pearce, P., and Pinto, D. 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), 146-153.

Pearson, G. 2017. Further challenges for Australian consumer law. In Consumer Law and

Socioeconomic Development (pp. 287-305). Springer, Cham.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Wu, Y. 2015. Evasion of Interest Withholding Tax: Evidence from Trading Volumes in

Australian Government Bonds. J. Austl. Tax'n, 17, 251.

Mitchell, R., O'Donnell, A., Marshall, S., and Ramsay, I. 2016. Law, corporate governance

and partnerships at work: a study of australian regulatory style and business practice.

Routledge.

Parker, M., 2015. Division 7A and winding up structures. Taxation in Australia, 50(6), p.312.

Pearce, P., and Pinto, D. 2015. An evaluation of the case for a congestion tax in

Australia. The Tax Specialist, 18(4), 146-153.

Pearson, G. 2017. Further challenges for Australian consumer law. In Consumer Law and

Socioeconomic Development (pp. 287-305). Springer, Cham.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Wu, Y. 2015. Evasion of Interest Withholding Tax: Evidence from Trading Volumes in

Australian Government Bonds. J. Austl. Tax'n, 17, 251.

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.