Taxation Law: Analysis of Income Tax, Avoidance, and Joint Ownership

VerifiedAdded on 2023/06/04

|13

|3373

|251

Report

AI Summary

This report delves into various aspects of taxation law, beginning with an analysis of whether annual lottery payments constitute assessable income under Section 6-5 of the ITAA 1997, concluding that they do due to their regularity and periodicity. It further examines the principle of tax avoidance as illustrated by the IRC v Duke of Westminster case, contrasting it with tax evasion and discussing the evolution of anti-avoidance measures in Australia. Finally, the report addresses the deductibility of losses incurred by joint owners of an investment property, referencing Taxation Ruling TR 93/32 to determine the allocation of income and losses based on legal interests, highlighting that Desklib provides students access to similar solved assignments and resources.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................5

Answer to question 4:.................................................................................................................7

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Issue:

Will the assessable income of the taxpayer would include the annual payments that is

received form the lotteries each year?

Rule:

The taxable income comprises of the income in accordance with the ordinary concepts

which is known as the ordinary income. For the federal commissioner of taxation to

determine the tax of the taxpayer it is vital to recognize the relevant taxpaying entity. The

impression of income is referred as the fundamental in determining whether the receipt would

be treated as the taxable income (Buenker 2018). Under the “section 6-5, ITAA 1997” the

Australian resident taxable income comprises of the ordinary income that is obtained from all

the sources whether the income is derived indirectly or directly from every sources.

Under the “ITA Act 1997 section 6-5 (4)” the doctrine of constructive receipt is

defined as soon as the individual is taken to have received the amount as and when it is

implemented or dealt in the manner when a taxpayer provides direction on their behalf

(Pomerleau 2016). As per the role of the tax legislation it is necessary to include in the

taxable income of the taxpayer the amount that necessarily meets the eligibility criteria of

case laws principles. The amount will be treated as the taxable income under “ITAA 1997 of

section 6-5”.

As per the “section 6-5, ITA Act 1997” the taxable income of the taxpayer includes

the ordinary income. On the basis of the special provision of the Act, there are certain taxable

income of the taxpayer that does not include the ordinary income. “Section 6-5, ITAA 1997”

places emphasis on the general concepts of the ordinary income that are subjected to income

Answer to question 1:

Issue:

Will the assessable income of the taxpayer would include the annual payments that is

received form the lotteries each year?

Rule:

The taxable income comprises of the income in accordance with the ordinary concepts

which is known as the ordinary income. For the federal commissioner of taxation to

determine the tax of the taxpayer it is vital to recognize the relevant taxpaying entity. The

impression of income is referred as the fundamental in determining whether the receipt would

be treated as the taxable income (Buenker 2018). Under the “section 6-5, ITAA 1997” the

Australian resident taxable income comprises of the ordinary income that is obtained from all

the sources whether the income is derived indirectly or directly from every sources.

Under the “ITA Act 1997 section 6-5 (4)” the doctrine of constructive receipt is

defined as soon as the individual is taken to have received the amount as and when it is

implemented or dealt in the manner when a taxpayer provides direction on their behalf

(Pomerleau 2016). As per the role of the tax legislation it is necessary to include in the

taxable income of the taxpayer the amount that necessarily meets the eligibility criteria of

case laws principles. The amount will be treated as the taxable income under “ITAA 1997 of

section 6-5”.

As per the “section 6-5, ITA Act 1997” the taxable income of the taxpayer includes

the ordinary income. On the basis of the special provision of the Act, there are certain taxable

income of the taxpayer that does not include the ordinary income. “Section 6-5, ITAA 1997”

places emphasis on the general concepts of the ordinary income that are subjected to income

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

tax and the same is added into the taxable income (Black 2018). There are certain

prerequisites of ordinary income that needs to be fulfilled. The ordinary income should be

cash or gains to the taxpayer that receives it. Provided that the prerequisites of the ordinary

income are met, then the gains will be an ordinary income if income is regular or periodical

receipts or has the concept of flow. The concept of periodical receipts has been defined in the

federal court example of “Dixon v FCT (1952)”. The periodical payments carry the nature of

income stream (Grubert and Altshuler 2016). This represents the money that is payable

periodically or at least annually to the taxpayer. In another example of the court in “Blake v

FC of T (1984)” held that gains that are having the characteristics of regular or periodic will

be held as ordinary income rather than those which is paid in lump sum.

Applications:

The principal issue in this case is understanding whether the annual payment of

lottery receipts every year will be an income under ordinary concepts of “section 6-5”. The

occurrences from the case unfolded where the winner of lottery is rewarded with a sum of

$50,000. Additionally, the winner would be receiving the sum of $50,000 for every year

regularly for a period of 20 years. further events that unfolded from the case states that if the

winner dies, the commission of lottery may pay the outstanding amount to the estate of

deceased nominated by the winner.

The issue in the question clearly defines that the annual payment will be treated as

income because the amount necessarily meets the eligibility criteria of “section 6-5” of the

ordinary concepts. Referring to “Dixon v FCT (1952)” the annual payment can be easily

classified as the income since it holds the characteristics of periodicity, recurrence and

regularity (Yagan 2015). The issue of annual payment in the question fulfils the perquisites of

tax and the same is added into the taxable income (Black 2018). There are certain

prerequisites of ordinary income that needs to be fulfilled. The ordinary income should be

cash or gains to the taxpayer that receives it. Provided that the prerequisites of the ordinary

income are met, then the gains will be an ordinary income if income is regular or periodical

receipts or has the concept of flow. The concept of periodical receipts has been defined in the

federal court example of “Dixon v FCT (1952)”. The periodical payments carry the nature of

income stream (Grubert and Altshuler 2016). This represents the money that is payable

periodically or at least annually to the taxpayer. In another example of the court in “Blake v

FC of T (1984)” held that gains that are having the characteristics of regular or periodic will

be held as ordinary income rather than those which is paid in lump sum.

Applications:

The principal issue in this case is understanding whether the annual payment of

lottery receipts every year will be an income under ordinary concepts of “section 6-5”. The

occurrences from the case unfolded where the winner of lottery is rewarded with a sum of

$50,000. Additionally, the winner would be receiving the sum of $50,000 for every year

regularly for a period of 20 years. further events that unfolded from the case states that if the

winner dies, the commission of lottery may pay the outstanding amount to the estate of

deceased nominated by the winner.

The issue in the question clearly defines that the annual payment will be treated as

income because the amount necessarily meets the eligibility criteria of “section 6-5” of the

ordinary concepts. Referring to “Dixon v FCT (1952)” the annual payment can be easily

classified as the income since it holds the characteristics of periodicity, recurrence and

regularity (Yagan 2015). The issue of annual payment in the question fulfils the perquisites of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

real gain for the taxpayer that is receiving it and itself sufficient for the annual payment to be

classified as the ordinary income.

The yearly payment represents the characteristics of regular and periodical as well as

the flow concept. In accordance with the judgement that was made under “Blake v FC of T

(1984)” the annual payment will be treated as the income with respect to the case laws

principles (Keightley and Sherlock 2014). The annual payment of $50,000 will be assessed

under the ordinary concepts of “ITAA 1997 of section 6-5”.

Conclusion:

The $50,000 yearly payment meets the prerequisites of income. The annual payment

is the gain because it is holding the characteristics of regular or periodical receipts. The

amount will be treated as the taxable income under “ITAA 1997 of section 6-5”.

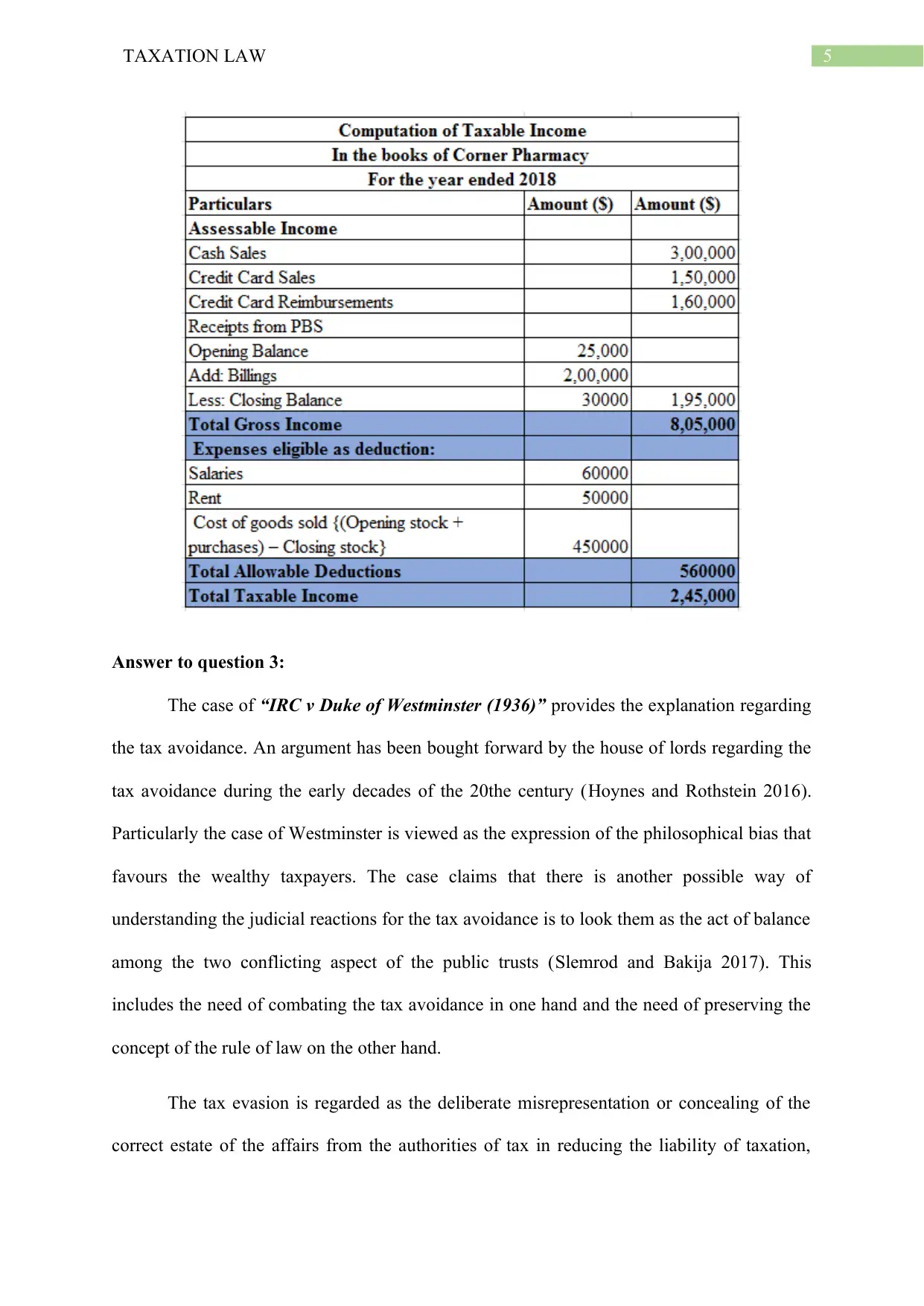

Answer to question 2:

On assuming that the accrual basis is applicable, the taxable income of Pharmacy’s is

calculated below;

real gain for the taxpayer that is receiving it and itself sufficient for the annual payment to be

classified as the ordinary income.

The yearly payment represents the characteristics of regular and periodical as well as

the flow concept. In accordance with the judgement that was made under “Blake v FC of T

(1984)” the annual payment will be treated as the income with respect to the case laws

principles (Keightley and Sherlock 2014). The annual payment of $50,000 will be assessed

under the ordinary concepts of “ITAA 1997 of section 6-5”.

Conclusion:

The $50,000 yearly payment meets the prerequisites of income. The annual payment

is the gain because it is holding the characteristics of regular or periodical receipts. The

amount will be treated as the taxable income under “ITAA 1997 of section 6-5”.

Answer to question 2:

On assuming that the accrual basis is applicable, the taxable income of Pharmacy’s is

calculated below;

5TAXATION LAW

Answer to question 3:

The case of “IRC v Duke of Westminster (1936)” provides the explanation regarding

the tax avoidance. An argument has been bought forward by the house of lords regarding the

tax avoidance during the early decades of the 20the century (Hoynes and Rothstein 2016).

Particularly the case of Westminster is viewed as the expression of the philosophical bias that

favours the wealthy taxpayers. The case claims that there is another possible way of

understanding the judicial reactions for the tax avoidance is to look them as the act of balance

among the two conflicting aspect of the public trusts (Slemrod and Bakija 2017). This

includes the need of combating the tax avoidance in one hand and the need of preserving the

concept of the rule of law on the other hand.

The tax evasion is regarded as the deliberate misrepresentation or concealing of the

correct estate of the affairs from the authorities of tax in reducing the liability of taxation,

Answer to question 3:

The case of “IRC v Duke of Westminster (1936)” provides the explanation regarding

the tax avoidance. An argument has been bought forward by the house of lords regarding the

tax avoidance during the early decades of the 20the century (Hoynes and Rothstein 2016).

Particularly the case of Westminster is viewed as the expression of the philosophical bias that

favours the wealthy taxpayers. The case claims that there is another possible way of

understanding the judicial reactions for the tax avoidance is to look them as the act of balance

among the two conflicting aspect of the public trusts (Slemrod and Bakija 2017). This

includes the need of combating the tax avoidance in one hand and the need of preserving the

concept of the rule of law on the other hand.

The tax evasion is regarded as the deliberate misrepresentation or concealing of the

correct estate of the affairs from the authorities of tax in reducing the liability of taxation,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

through dishonest reporting of understated profits and overstating of deductions (Braithwaite

2017). Tax avoidance is regarded as the lawful concept which comprises of exploiting the

rules of reducing the tax liability. In the current case of “IRC v Duke of Westminster

(1936)” the term tax avoidance is regarded as the legal concept (Sikka 2014). The scenario

that is obtained from the case suggest that Westminster Duke paid his gardener a weekly sum

of wages.

The Duke further entered into the contract where he stopped paying the wages and

rather drawing up the covenant where he agreed to pay the sum till the equivalent amount.

The gardener still received the similar amount however as per the ruling the taxpayer was

able to claim the income tax deductions because of the covenant (Dyreng, Hanlon and

Maydew 2018). The duke of Westminster ultimately won the case. When the case was

presented before the house of lords and stated judgement stated that every taxpayer is eligible

for arranging their tax agreement within the boundary of the law.

The ruling can be considered as the attractive principle for those that seek to avoid

paying tax legally by establishing a complex structure. The ruling has now been discouraged

by the subsequent cases where the court of law have considered the wide ranging impact. The

court of law in the further case adopted the principle of Ramsay by undertaking more

constructive approach (Blaufus et al. 2017). The revenue issued a document that contained

the title relating to the disclosure of tax avoidance that needed making disclosure relating to

the schemes of tax planning to the tax authorities shortly when they are marketed or

implemented. The overall intention was to help to the users in working out the difference

amid the artificial schemes of avoidance and the ordinary sensible planning of tax.

Responding the current situation in Australia there was the constant struggle between

the legislator and the ingenious taxpayer and his advisors. The authorities of tax have

through dishonest reporting of understated profits and overstating of deductions (Braithwaite

2017). Tax avoidance is regarded as the lawful concept which comprises of exploiting the

rules of reducing the tax liability. In the current case of “IRC v Duke of Westminster

(1936)” the term tax avoidance is regarded as the legal concept (Sikka 2014). The scenario

that is obtained from the case suggest that Westminster Duke paid his gardener a weekly sum

of wages.

The Duke further entered into the contract where he stopped paying the wages and

rather drawing up the covenant where he agreed to pay the sum till the equivalent amount.

The gardener still received the similar amount however as per the ruling the taxpayer was

able to claim the income tax deductions because of the covenant (Dyreng, Hanlon and

Maydew 2018). The duke of Westminster ultimately won the case. When the case was

presented before the house of lords and stated judgement stated that every taxpayer is eligible

for arranging their tax agreement within the boundary of the law.

The ruling can be considered as the attractive principle for those that seek to avoid

paying tax legally by establishing a complex structure. The ruling has now been discouraged

by the subsequent cases where the court of law have considered the wide ranging impact. The

court of law in the further case adopted the principle of Ramsay by undertaking more

constructive approach (Blaufus et al. 2017). The revenue issued a document that contained

the title relating to the disclosure of tax avoidance that needed making disclosure relating to

the schemes of tax planning to the tax authorities shortly when they are marketed or

implemented. The overall intention was to help to the users in working out the difference

amid the artificial schemes of avoidance and the ordinary sensible planning of tax.

Responding the current situation in Australia there was the constant struggle between

the legislator and the ingenious taxpayer and his advisors. The authorities of tax have

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

undertaken provision in both the legislation as well as the subsidiary legislation in making

sure that there is an effective blockage of potential loopholes are covered (Rablen 2017). The

tools that is employed by the legislator comprises of both the specific and the general anti-

avoidance provision. Referring to the current situation in Australia the tax authorities have

catered to the specific abuse and have made contribution to implement control in the specific

areas. The current income tax provision comprises of the specific provisions which is inserted

in the articles all through the act. The principle that was established in the case of Duke is not

any more relevant because the statutory provision of the anti-avoidance rules is regularly

imposed and expressed the intention of imposing the general overlay in either whole or

specified parts of tax legislation.

The general anti-avoidance rules act as the carte blanche in denying the tax

advantages that is obtained from the transactions that are actuated by the prescribed tax

avoidance would eventually give an effect to the legislative policy and intention. In the recent

years the Australian taxation authorities have implemented the special clause in the general

anti-avoidance that provides the commissioner with the authority of disregarding artificial

and fictitious transactions or schemes that aims to lower down the sum of tax payable by any

person even though the schemes are not completely effective or implemented (Alldridge

2015). Arguably, the current tax regimes in Australia have been designed in the manner that

no taxpayer can avoid the payment of tax on excess profits by entering into the artificial or

fictitious operations.

Answer to question 4:

Issues:

Can the taxpayer claim 100% deductions for the loss that is occurred by the joint

owners of the investment property that is jointly held by the owners?

undertaken provision in both the legislation as well as the subsidiary legislation in making

sure that there is an effective blockage of potential loopholes are covered (Rablen 2017). The

tools that is employed by the legislator comprises of both the specific and the general anti-

avoidance provision. Referring to the current situation in Australia the tax authorities have

catered to the specific abuse and have made contribution to implement control in the specific

areas. The current income tax provision comprises of the specific provisions which is inserted

in the articles all through the act. The principle that was established in the case of Duke is not

any more relevant because the statutory provision of the anti-avoidance rules is regularly

imposed and expressed the intention of imposing the general overlay in either whole or

specified parts of tax legislation.

The general anti-avoidance rules act as the carte blanche in denying the tax

advantages that is obtained from the transactions that are actuated by the prescribed tax

avoidance would eventually give an effect to the legislative policy and intention. In the recent

years the Australian taxation authorities have implemented the special clause in the general

anti-avoidance that provides the commissioner with the authority of disregarding artificial

and fictitious transactions or schemes that aims to lower down the sum of tax payable by any

person even though the schemes are not completely effective or implemented (Alldridge

2015). Arguably, the current tax regimes in Australia have been designed in the manner that

no taxpayer can avoid the payment of tax on excess profits by entering into the artificial or

fictitious operations.

Answer to question 4:

Issues:

Can the taxpayer claim 100% deductions for the loss that is occurred by the joint

owners of the investment property that is jointly held by the owners?

8TAXATION LAW

Laws:

A division of net income and loss between the joint owners of the rental property is

considered under the “taxation ruling of TR 93/32”. The “taxation ruling of TR 93/32”

provides that the net income for the purpose of taxation of the rental property should be

shared as per the legal interest of the owners, except in the situations where there is a

sufficient evidence to establish that the equal rights is different from the lawful title (Bently

and Sherman 2014). The legal interest of the property holders is ascertained by the legal title

of the property. It is having been rightly stated the equitable interest do not follow the legal

title as there are certain basis for distributing the profit and loss based on the equitable terms

and not in terms of the legal basis.

As per the paragraph 8 of the “taxation ruling of TR 93/32” the joint-ownership

bears entitlement of exerting the maximum amount of allowable rights over what is owned by

the property holders (Honey, Mugambwa and Webb 2017). Usually the legal interest in the

land is attained by the owner when the title of the land is registered in the name of the title

holder. As per the general rule of the “taxation ruling of TR 93/32” the joint owners of the

rental property would usually be holding the property as the joint tenants or the tenants in

common.

One of the essential features of the joint tenants and the tenants in common is the

tenants legal interest in the property. It represents the legal interest that should be in the

similar extent, nature and the duration (Byrne 2018). The owners of the rental property each

owning the 50% share in the property and must share the income or loss on equal grounds.

Referring to the paragraph 3 of the “taxation ruling of TR 93/32” the joint ownership of the

rental property is regarded as the owners under the income tax purpose rather than classifying

them as the partners under the general law. When it is noticed that the joint owners of the

Laws:

A division of net income and loss between the joint owners of the rental property is

considered under the “taxation ruling of TR 93/32”. The “taxation ruling of TR 93/32”

provides that the net income for the purpose of taxation of the rental property should be

shared as per the legal interest of the owners, except in the situations where there is a

sufficient evidence to establish that the equal rights is different from the lawful title (Bently

and Sherman 2014). The legal interest of the property holders is ascertained by the legal title

of the property. It is having been rightly stated the equitable interest do not follow the legal

title as there are certain basis for distributing the profit and loss based on the equitable terms

and not in terms of the legal basis.

As per the paragraph 8 of the “taxation ruling of TR 93/32” the joint-ownership

bears entitlement of exerting the maximum amount of allowable rights over what is owned by

the property holders (Honey, Mugambwa and Webb 2017). Usually the legal interest in the

land is attained by the owner when the title of the land is registered in the name of the title

holder. As per the general rule of the “taxation ruling of TR 93/32” the joint owners of the

rental property would usually be holding the property as the joint tenants or the tenants in

common.

One of the essential features of the joint tenants and the tenants in common is the

tenants legal interest in the property. It represents the legal interest that should be in the

similar extent, nature and the duration (Byrne 2018). The owners of the rental property each

owning the 50% share in the property and must share the income or loss on equal grounds.

Referring to the paragraph 3 of the “taxation ruling of TR 93/32” the joint ownership of the

rental property is regarded as the owners under the income tax purpose rather than classifying

them as the partners under the general law. When it is noticed that the joint owners of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

rental property amounts to income tax purpose instead of the partnership under the general

definition of law then the profit and loss should be shared in the equal basis with private

engage of sharing profit and loss is in effective.

The above stated principles can be further supported by the case of “McDonald v FC

of T (1987)” where the taxpayer and his spouse have rented out the two units of their strata

plots (Townsend 2018). The records that were obtained from the case was that the net profits

shall be distributed to Mrs McDonald wife at 75% while her husband Mr McDonald would

be getting only 25% of the profit and the husband would be bearing the full amount of the

loss. A claim of partnership under the general law was ruled out by the commissioner and the

only relevant relation that was applicable between the parties were the co-ownership. As Mr

and Mrs McDonald are the joint tenants under the equity and law the loss that is occurred in

letting the rental plot must be shared equally.

Application:

Events that unfolded from the case provides that an amount was borrowed by Joseph

and his wife to purchase the rental plot under the title of joint owners. The husband and the

wife formed the agreement where they decided to share the profits on basis of 20:80 per cent.

The couple eventually incurred $40,000 as the loss from the property. Referring to the

paragraph 8 of the “taxation ruling of TR 93/32” the joint-ownership of Joseph and Jane

bears the entitlement of exerting the maximum amount of allowable rights on the property

(Jones 2016). One of the essential features of the joint tenancy between the husband and wife

is the legal interest in the property. With respect to their equal rights the owners of the rental

property Joseph and Jane each owned the 50% share in the property.

Discussing explanation of the paragraph 3 of the “taxation ruling of TR 93/32” the

joint ownership of the rental property between Joseph and his wife will be regarded as the

rental property amounts to income tax purpose instead of the partnership under the general

definition of law then the profit and loss should be shared in the equal basis with private

engage of sharing profit and loss is in effective.

The above stated principles can be further supported by the case of “McDonald v FC

of T (1987)” where the taxpayer and his spouse have rented out the two units of their strata

plots (Townsend 2018). The records that were obtained from the case was that the net profits

shall be distributed to Mrs McDonald wife at 75% while her husband Mr McDonald would

be getting only 25% of the profit and the husband would be bearing the full amount of the

loss. A claim of partnership under the general law was ruled out by the commissioner and the

only relevant relation that was applicable between the parties were the co-ownership. As Mr

and Mrs McDonald are the joint tenants under the equity and law the loss that is occurred in

letting the rental plot must be shared equally.

Application:

Events that unfolded from the case provides that an amount was borrowed by Joseph

and his wife to purchase the rental plot under the title of joint owners. The husband and the

wife formed the agreement where they decided to share the profits on basis of 20:80 per cent.

The couple eventually incurred $40,000 as the loss from the property. Referring to the

paragraph 8 of the “taxation ruling of TR 93/32” the joint-ownership of Joseph and Jane

bears the entitlement of exerting the maximum amount of allowable rights on the property

(Jones 2016). One of the essential features of the joint tenancy between the husband and wife

is the legal interest in the property. With respect to their equal rights the owners of the rental

property Joseph and Jane each owned the 50% share in the property.

Discussing explanation of the paragraph 3 of the “taxation ruling of TR 93/32” the

joint ownership of the rental property between Joseph and his wife will be regarded as the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

owners under the income tax purpose rather than classifying them as the partners under the

general law (Wu 2018). As it is noticed that the joint owners of the rental property between

the couple amounted to co-ownership for income tax purpose rather than the partnership

under the general law the profit and loss should be shared in the equal basis with private

engage of sharing profit and loss is in effective.

Supporting the decision of court in “McDonald v FC of T (1987)” the couple are the

joint tenants under the equity and law (Townsend 2018). The $40,000 loss that is occurred in

letting the rental plot must be shared equally as their private engagement distributing the

profit and loss cannot override their respective entitlements for the purpose of taxation.

If the furthers events are unfolded where the couple decides selling the rental property

that they bought and any capital gains or loss arising thereof must be shared in respect to their

legal equitable interest. In other words, the capital gains or the capital loss that they may

obtained from selling the rental property must be shared in equal proportion. The capital

gains and the capital loss cannot be divided under the partnership agreement.

Conclusion:

A decisive opinion is formed from the case analysis that no partnership in terms of the

general law subsisted between the couple. The relationship between the husband and wife

was of the co-ownership and even though they were deemed to be partners by the reason of

the “subsection 6 (1) of the Act”, the circumstances here will be immaterial under the general

law.

owners under the income tax purpose rather than classifying them as the partners under the

general law (Wu 2018). As it is noticed that the joint owners of the rental property between

the couple amounted to co-ownership for income tax purpose rather than the partnership

under the general law the profit and loss should be shared in the equal basis with private

engage of sharing profit and loss is in effective.

Supporting the decision of court in “McDonald v FC of T (1987)” the couple are the

joint tenants under the equity and law (Townsend 2018). The $40,000 loss that is occurred in

letting the rental plot must be shared equally as their private engagement distributing the

profit and loss cannot override their respective entitlements for the purpose of taxation.

If the furthers events are unfolded where the couple decides selling the rental property

that they bought and any capital gains or loss arising thereof must be shared in respect to their

legal equitable interest. In other words, the capital gains or the capital loss that they may

obtained from selling the rental property must be shared in equal proportion. The capital

gains and the capital loss cannot be divided under the partnership agreement.

Conclusion:

A decisive opinion is formed from the case analysis that no partnership in terms of the

general law subsisted between the couple. The relationship between the husband and wife

was of the co-ownership and even though they were deemed to be partners by the reason of

the “subsection 6 (1) of the Act”, the circumstances here will be immaterial under the general

law.

11TAXATION LAW

References:

Alldridge, P., 2015. 13. Tax avoidance, tax evasion, money laundering and the problem of

‘offshore’. Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Bently, L. and Sherman, B., 2014. Intellectual property law. Oxford University Press,

Australia.

Black, D., 2018. The incidence of income taxes. Routledge.

Blaufus, K., Hundsdoerfer, J., Jacob, M. and Sünwoldt, M., 2016. Does legality matter? The

case of tax avoidance and evasion. Journal of Economic Behavior & Organization, 127,

pp.182-206.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Byrne, S., 2018. Intellectual property in Australia [Book Review]. Ethos: Official Publication

of the Law Society of the Australian Capital Territory, (248), p.58.

Dyreng, S.D., Hanlon, M. and Maydew, E.L., 2018. When does tax avoidance result in tax

uncertainty?. The Accounting Review.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Honey, R., Mugambwa, J. and Webb, E., 2017. Real Property Law in Western Australia.

Hoynes, H. and Rothstein, J., 2016. Tax policy toward low-income families (No. w22080).

National Bureau of Economic Research.

References:

Alldridge, P., 2015. 13. Tax avoidance, tax evasion, money laundering and the problem of

‘offshore’. Greed, Corruption, and the Modern State: Essays in Political Economy, p.317.

Bently, L. and Sherman, B., 2014. Intellectual property law. Oxford University Press,

Australia.

Black, D., 2018. The incidence of income taxes. Routledge.

Blaufus, K., Hundsdoerfer, J., Jacob, M. and Sünwoldt, M., 2016. Does legality matter? The

case of tax avoidance and evasion. Journal of Economic Behavior & Organization, 127,

pp.182-206.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Buenker, J.D., 2018. The Income Tax and the Progressive Era. Routledge.

Byrne, S., 2018. Intellectual property in Australia [Book Review]. Ethos: Official Publication

of the Law Society of the Australian Capital Territory, (248), p.58.

Dyreng, S.D., Hanlon, M. and Maydew, E.L., 2018. When does tax avoidance result in tax

uncertainty?. The Accounting Review.

Grubert, H. and Altshuler, R., 2016. Shifting the burden of taxation from the corporate to the

personal level and getting the corporate tax rate down to 15 percent.

Honey, R., Mugambwa, J. and Webb, E., 2017. Real Property Law in Western Australia.

Hoynes, H. and Rothstein, J., 2016. Tax policy toward low-income families (No. w22080).

National Bureau of Economic Research.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.