Comprehensive Income Tax Case Study: TAX305 Taxation Law, 2018

VerifiedAdded on 2023/06/08

|12

|2910

|181

Case Study

AI Summary

This case study provides a detailed analysis of Bruce's tax liability for the year ended 2018, based on Australian Taxation Law. It examines various income sources, including business receipts, military service income, rental income, part-time lecturing income, dividends, and bank deposit interest, determining their assessability under the Income Tax Assessment Act 1997 (ITAA 1997). The study also assesses the deductibility of various expenses, such as office rent, employee salary, cleaning contractor fees, business tool purchases, client entertainment, travel costs, and home-related expenses, applying relevant sections of the ITAA 1997 and case law to justify the conclusions. Furthermore, it discusses specific deductions related to tax agent fees and rental property expenses, including interest on loans and repairs, while also addressing non-deductible expenses like initial repairs and capital improvements to the investment property. The document concludes with a computation of Bruce's overall tax liability.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

References:.................................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

References:.................................................................................................................................9

2TAXATION LAW

Answer to question 1:

According to the explanation of “section 6-5 of the ITAA 1997” an individual

taxpayer earning income from the business is termed as ordinary income (Barkoczy 2014).

To categorize the receipts from business in the form of ordinary income it is necessary to

understand whether a business activity is conducted by an individual taxpayer or whether the

business receipts are treated as normal earnings obtained from carrying on of business. As

explained under “section 995-1 of the ITAA 1997” the definition of business includes

conducting an act of profession or trade but not include an occupation in capacity of

employee.

Case facts obtained from Bruce scenario is based on determining tax liability of

receipts and deductibility of expenditure for the year ended 2018. To categorize the business

receipts as the ordinary income it is essential the receipts has nexus with the business

activities. Categorizing the receipts in the form of ordinary income from the business

involves two process (Coleman and Sadiq 2013). This includes determining whether the

taxpayer is performing the business or whether the considerations for the receipts that is

received originated from the normal proceeds of the business activity. Any form of receipts

obtained through the normal proceeds is regarded as income from ordinary concepts under

“section 6-5”.

As stated under the “section 6-1” an individual taxpayer that obtains receipts from the

employment and personal services would be treated for the income tax purpose (Grange,

Jover-Ledesma and Maydew 2014). As understood from the case facts of Bruce, he obtained

business receipts amounting to $340,000. The amount represents ordinary income from the

business activities and would be considered as the assessable income. “Section 6-20 of the

ITAA 1997” is associated with the exempted income. As obvious Bruce reports income from

Answer to question 1:

According to the explanation of “section 6-5 of the ITAA 1997” an individual

taxpayer earning income from the business is termed as ordinary income (Barkoczy 2014).

To categorize the receipts from business in the form of ordinary income it is necessary to

understand whether a business activity is conducted by an individual taxpayer or whether the

business receipts are treated as normal earnings obtained from carrying on of business. As

explained under “section 995-1 of the ITAA 1997” the definition of business includes

conducting an act of profession or trade but not include an occupation in capacity of

employee.

Case facts obtained from Bruce scenario is based on determining tax liability of

receipts and deductibility of expenditure for the year ended 2018. To categorize the business

receipts as the ordinary income it is essential the receipts has nexus with the business

activities. Categorizing the receipts in the form of ordinary income from the business

involves two process (Coleman and Sadiq 2013). This includes determining whether the

taxpayer is performing the business or whether the considerations for the receipts that is

received originated from the normal proceeds of the business activity. Any form of receipts

obtained through the normal proceeds is regarded as income from ordinary concepts under

“section 6-5”.

As stated under the “section 6-1” an individual taxpayer that obtains receipts from the

employment and personal services would be treated for the income tax purpose (Grange,

Jover-Ledesma and Maydew 2014). As understood from the case facts of Bruce, he obtained

business receipts amounting to $340,000. The amount represents ordinary income from the

business activities and would be considered as the assessable income. “Section 6-20 of the

ITAA 1997” is associated with the exempted income. As obvious Bruce reports income from

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

the military service. The amount will be treated as the exempted income under “section 6-20

of the ITAA 1997”.

An individual taxpayer that derives income with the help of personal service will be

accounted as ordinary income under the ordinary concepts of “section 6-5”. The taxation

commissioner in “FCT v Kelly (1985)” held that nexus is not impacted for any one-off or

lump sum receipts and also not relevant for those that pays (James 2014). As defined under

“section 6-5” taxpayer obtaining income from the investment property is regarded as the

ordinary income.

Quoting the judgement in “Black v FCT (1984)” periodic or regular receipts is

categorized as ordinary income. Gains that are periodic or regular will be treated as the

income under ordinary concepts (Jover-Ledesma 2014). In the later part of the case, Bruce

reports rental receipts obtained during the income year from the investment property. The

amount of $10,000 would be treated as taxable rental receipts obtained from investment

property. The sum constitute income under the ordinary concepts of “section 6-5”.

The Australian Taxation Office explains that irrelevant of the fact whether a person is

employed in one or greater than occupation or working either full or part-time, any income

from such employment would attract tax liability. As held in “Smith v FCT (1997)” where an

individual taxpayer obtains income for completing the tertiary services would be treated as

ordinary income under “section 15-2 of the ITAA 1997” (Kenny 2013). Similarly, in the case

of Bruce, he reports a receipts of 34,000 from the part-time lecturing in University. The

receipt is an income from employment and would be treated as ordinary income under

“section 15-2”.

According to the “section 44 (1)” income obtained from the dividend should be

included in the tax return. Dividends derived by the taxpayer from the public listed

the military service. The amount will be treated as the exempted income under “section 6-20

of the ITAA 1997”.

An individual taxpayer that derives income with the help of personal service will be

accounted as ordinary income under the ordinary concepts of “section 6-5”. The taxation

commissioner in “FCT v Kelly (1985)” held that nexus is not impacted for any one-off or

lump sum receipts and also not relevant for those that pays (James 2014). As defined under

“section 6-5” taxpayer obtaining income from the investment property is regarded as the

ordinary income.

Quoting the judgement in “Black v FCT (1984)” periodic or regular receipts is

categorized as ordinary income. Gains that are periodic or regular will be treated as the

income under ordinary concepts (Jover-Ledesma 2014). In the later part of the case, Bruce

reports rental receipts obtained during the income year from the investment property. The

amount of $10,000 would be treated as taxable rental receipts obtained from investment

property. The sum constitute income under the ordinary concepts of “section 6-5”.

The Australian Taxation Office explains that irrelevant of the fact whether a person is

employed in one or greater than occupation or working either full or part-time, any income

from such employment would attract tax liability. As held in “Smith v FCT (1997)” where an

individual taxpayer obtains income for completing the tertiary services would be treated as

ordinary income under “section 15-2 of the ITAA 1997” (Kenny 2013). Similarly, in the case

of Bruce, he reports a receipts of 34,000 from the part-time lecturing in University. The

receipt is an income from employment and would be treated as ordinary income under

“section 15-2”.

According to the “section 44 (1)” income obtained from the dividend should be

included in the tax return. Dividends derived by the taxpayer from the public listed

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

companies for the shares that are publicly traded should be included in the taxable income

(Krever 2013). Certain dividends carry franking credits for which a tax offset is available to a

taxpayer at the time of filing tax return. With reference to “section 44 (1)” receipts of

dividend by Bruce is a constituent of taxable incomes while the franking the credits can be

used for claiming the tax offset by Bruce as it would help in lowering the tax payable amount.

Income earned by the Australian resident in the form of bank deposit interest must be

accounted as the taxable income (Morgan, Mortimer and Pinto 2013). A taxpayer is required

to declare such income in his taxable return. Bruce during the income year earned income

from Bank deposit that amounted to $5,000. The amount has the character of income and

constitute taxable income under the ordinary concepts of “section 6-5”.

The main provision of “section 8-1” enables the taxpayer with the general deduction

for the expenditure that are incurred in gaining the assessable. “Section 8-1” general

deduction has the potential to implement on any taxpayer (Sadiq 2014). A taxpayer is

allowed to claim specific deductions under the “section 8-5 of the ITAA 1997”. The

provision of “section 8-1” explains that a taxpayer is prohibited from claiming deductions if

the expenses are private or domestic in nature and fails meet the eligibility conditions of

“section 8-1 (2)(b)”.

Bruce incurs expenses on office rent, employee salary and cleaning contractor. The

law court in “Ronpibon Tin NL v FCT (1949)” held that for an expense to be allowed for

deductions must be an outgoing that is incurred in gaining or generating the assessable

income (Woellner et al. 2014). The expenses should be relevant and incidental to that end.

The expenses on office rent, employee salary and cleaning contractor are incurred by Bruce is

an outgoing which is incurred in gaining or producing the taxable income. Bruce can claim an

allowable deduction under the positive limbs of “section 8-1 of the ITAA 1997” as these are

companies for the shares that are publicly traded should be included in the taxable income

(Krever 2013). Certain dividends carry franking credits for which a tax offset is available to a

taxpayer at the time of filing tax return. With reference to “section 44 (1)” receipts of

dividend by Bruce is a constituent of taxable incomes while the franking the credits can be

used for claiming the tax offset by Bruce as it would help in lowering the tax payable amount.

Income earned by the Australian resident in the form of bank deposit interest must be

accounted as the taxable income (Morgan, Mortimer and Pinto 2013). A taxpayer is required

to declare such income in his taxable return. Bruce during the income year earned income

from Bank deposit that amounted to $5,000. The amount has the character of income and

constitute taxable income under the ordinary concepts of “section 6-5”.

The main provision of “section 8-1” enables the taxpayer with the general deduction

for the expenditure that are incurred in gaining the assessable. “Section 8-1” general

deduction has the potential to implement on any taxpayer (Sadiq 2014). A taxpayer is

allowed to claim specific deductions under the “section 8-5 of the ITAA 1997”. The

provision of “section 8-1” explains that a taxpayer is prohibited from claiming deductions if

the expenses are private or domestic in nature and fails meet the eligibility conditions of

“section 8-1 (2)(b)”.

Bruce incurs expenses on office rent, employee salary and cleaning contractor. The

law court in “Ronpibon Tin NL v FCT (1949)” held that for an expense to be allowed for

deductions must be an outgoing that is incurred in gaining or generating the assessable

income (Woellner et al. 2014). The expenses should be relevant and incidental to that end.

The expenses on office rent, employee salary and cleaning contractor are incurred by Bruce is

an outgoing which is incurred in gaining or producing the taxable income. Bruce can claim an

allowable deduction under the positive limbs of “section 8-1 of the ITAA 1997” as these are

5TAXATION LAW

incurred inside the initial part of subsection which is sufficient as well as necessary in

producing the taxable income.

As defined by the Australian Taxation Office, a taxpayer that incurs expenses in

purchase of business tools or equipment or any form of assets which has sufficient nexus in

generating assessable income, then the expenses would be allowed as deductions (Pinto

2013). Furthermore, the explanation of Australian Taxation Office includes that a business

item or equipment having a cost base of $300 or less can be immediately claimed for

deductions. Bruce reports a purchase of calculator for business use. The cost base of

calculator was less than $300 and the same can be immediately claimed for deductions since

the has sufficient nexus in generating assessable income.

The Australian Taxation Office explains that meals and entertainment to clients are

considered as entertainment expenditure for business purpose (Braithwaite 2017). Equivalent

to such explanation Bruce incurs meal and entertainment on his client. The meal and

entertainment cost incurred on client by Bruce would be allowed as business entertainment

deductions. Conversely Bruce also report the meal and entertainment expenses on himself. A

part of the meal and entertainment expenses will not be allowed for deductions since it is

personal expenses and non-deductible under the positive limbs of “section 8-1”.

As stated under second negative limb of “section 8-1 (2)(b)” any outgoings of

domestic or private type is not deductible since it fails to meet the criteria of positive limbs

and non-deductible under second negative limbs (Robin 2017). The court in “Lunney v FCT

(1958)” explains that it is necessary to look into the essential character of losses or outgoings

whether it forms the vital prerequisite in derivation of taxable income. Expenses incurred on

travel between home and individual place of work is non-deductible. The court in “Payne v

FCT (2001)” denied the taxpayer from obtaining deductions for the cost occurred in

incurred inside the initial part of subsection which is sufficient as well as necessary in

producing the taxable income.

As defined by the Australian Taxation Office, a taxpayer that incurs expenses in

purchase of business tools or equipment or any form of assets which has sufficient nexus in

generating assessable income, then the expenses would be allowed as deductions (Pinto

2013). Furthermore, the explanation of Australian Taxation Office includes that a business

item or equipment having a cost base of $300 or less can be immediately claimed for

deductions. Bruce reports a purchase of calculator for business use. The cost base of

calculator was less than $300 and the same can be immediately claimed for deductions since

the has sufficient nexus in generating assessable income.

The Australian Taxation Office explains that meals and entertainment to clients are

considered as entertainment expenditure for business purpose (Braithwaite 2017). Equivalent

to such explanation Bruce incurs meal and entertainment on his client. The meal and

entertainment cost incurred on client by Bruce would be allowed as business entertainment

deductions. Conversely Bruce also report the meal and entertainment expenses on himself. A

part of the meal and entertainment expenses will not be allowed for deductions since it is

personal expenses and non-deductible under the positive limbs of “section 8-1”.

As stated under second negative limb of “section 8-1 (2)(b)” any outgoings of

domestic or private type is not deductible since it fails to meet the criteria of positive limbs

and non-deductible under second negative limbs (Robin 2017). The court in “Lunney v FCT

(1958)” explains that it is necessary to look into the essential character of losses or outgoings

whether it forms the vital prerequisite in derivation of taxable income. Expenses incurred on

travel between home and individual place of work is non-deductible. The court in “Payne v

FCT (2001)” denied the taxpayer from obtaining deductions for the cost occurred in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

travelling amid his home and usual workplace. Bruce incurs cost on traveling to and from

work. The expenses will not be allowed for deductions under “section 8-1” since it constitute

travel between two unrelated place of work.

Expenses that are domestic or capital in nature is prohibited from deduction under

negative limbs of “section 8-1 (2)” as there is no nexus in the derivation of assessable

income. Bruce has occurred expenses on rates and electricity for family home (Burton 2017).

The expenses on rates and electricity for family home is not allowable for deductions since

the expenses are domestic in nature which is prohibited from deduction under negative limbs

of “section 8-1 (2)” as there is no nexus in the derivation of assessable income.

As per the “section 8-5 of the ITAA 1997” a taxpayer is permitted to claim an

allowable specific deduction. As defined in “section 25-5 of the ITAA 1997” expenses that

are related to tax is allowed for deductions (White and Townsend 2018). Certain costs such as

managing tax affairs, payments to general interest are allowed for specific deductions under

the “section 25-5”. An expense of $1,000 was incurred by Bruce on the tax agent fees for

preparing the tax returns of 2016/17. The expenses qualify specific deductions under

“section 25-5”.

A taxpayer is allowed to claim deductions for the expenses that is incurred on the

rental property till the period when the property is rented out or open for rent. Bruce reports

expenses an expense of $2000 on investment property. Bruce additionally reported an

expense of $15,000 as the interest on loan for acquiring the property. Denoting the reference

in “Amalgamated Zinc Ltd v FCT (1935)” a taxpayer is allowed to claim an immediate

deduction for expenses such as interest on loan because they are incurred in gaining or

producing the assessable income (Swan 2018). Similarly, Bruce is allowed to claim

travelling amid his home and usual workplace. Bruce incurs cost on traveling to and from

work. The expenses will not be allowed for deductions under “section 8-1” since it constitute

travel between two unrelated place of work.

Expenses that are domestic or capital in nature is prohibited from deduction under

negative limbs of “section 8-1 (2)” as there is no nexus in the derivation of assessable

income. Bruce has occurred expenses on rates and electricity for family home (Burton 2017).

The expenses on rates and electricity for family home is not allowable for deductions since

the expenses are domestic in nature which is prohibited from deduction under negative limbs

of “section 8-1 (2)” as there is no nexus in the derivation of assessable income.

As per the “section 8-5 of the ITAA 1997” a taxpayer is permitted to claim an

allowable specific deduction. As defined in “section 25-5 of the ITAA 1997” expenses that

are related to tax is allowed for deductions (White and Townsend 2018). Certain costs such as

managing tax affairs, payments to general interest are allowed for specific deductions under

the “section 25-5”. An expense of $1,000 was incurred by Bruce on the tax agent fees for

preparing the tax returns of 2016/17. The expenses qualify specific deductions under

“section 25-5”.

A taxpayer is allowed to claim deductions for the expenses that is incurred on the

rental property till the period when the property is rented out or open for rent. Bruce reports

expenses an expense of $2000 on investment property. Bruce additionally reported an

expense of $15,000 as the interest on loan for acquiring the property. Denoting the reference

in “Amalgamated Zinc Ltd v FCT (1935)” a taxpayer is allowed to claim an immediate

deduction for expenses such as interest on loan because they are incurred in gaining or

producing the assessable income (Swan 2018). Similarly, Bruce is allowed to claim

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

deductions under “section 8-1” for the above stated expenses on rental property as they are

occurred in producing the rental income.

Denoting the explanation in “Section 25-10 of the ITAA 1997” costs that are

occurred for notional repair is non-allowable as deductions. Citing the judgement in “Inland

Revenue Commissioners v Shipping Co Ltd (1923)” a deductions was non-allowable to the

taxpayer for the cost incurred on initial repair of the investment property because these

expenses are treated as capital expenses which is not allowed for deductions (Woellner et al.,

2014). Evidences from the case suggest that Bruce reports costs on repainting the investment

property which is initially bought by him. The cost of repainting the investment property

amounts to initial repair of capital nature. The expenses are initial repair that is occurred in

remedying the defects or in other words, it is a deterioration that was present in the property

on the date when Bruce acquired the investment property. The repainting expenses are non-

deductible under “Section 25-10 of the ITAA 1997”.

As stated in “Section 25-10” a taxpayer is permitted to claim deductions for the

expenses that is incurred in replacing a portion of property which is damaged by storm

(Morgan, Mortimer and Pinto 2013). A sum of $1,000 was incurred by Bruce for replacing

the tiles on the roof of the investment property since it was damaged by storm. Under

“section 25-10” the taxpayer can claim permissible deductions for expenses that is incurred

in replacing the tiles of roof since the rental property was held in derivation of the taxable

income.

Under “section 25-10 (3) of the ITAA 1997” a taxpayer is denied deductions for

expenses that are capital in nature (Coleman and Sadiq 2013). The section prohibits the

taxpayer from claiming deductions for repairs that involves improvement of substantial

nature. Expenses incurred in addition or alteration in the property cannot be allowed for

deductions under “section 8-1” for the above stated expenses on rental property as they are

occurred in producing the rental income.

Denoting the explanation in “Section 25-10 of the ITAA 1997” costs that are

occurred for notional repair is non-allowable as deductions. Citing the judgement in “Inland

Revenue Commissioners v Shipping Co Ltd (1923)” a deductions was non-allowable to the

taxpayer for the cost incurred on initial repair of the investment property because these

expenses are treated as capital expenses which is not allowed for deductions (Woellner et al.,

2014). Evidences from the case suggest that Bruce reports costs on repainting the investment

property which is initially bought by him. The cost of repainting the investment property

amounts to initial repair of capital nature. The expenses are initial repair that is occurred in

remedying the defects or in other words, it is a deterioration that was present in the property

on the date when Bruce acquired the investment property. The repainting expenses are non-

deductible under “Section 25-10 of the ITAA 1997”.

As stated in “Section 25-10” a taxpayer is permitted to claim deductions for the

expenses that is incurred in replacing a portion of property which is damaged by storm

(Morgan, Mortimer and Pinto 2013). A sum of $1,000 was incurred by Bruce for replacing

the tiles on the roof of the investment property since it was damaged by storm. Under

“section 25-10” the taxpayer can claim permissible deductions for expenses that is incurred

in replacing the tiles of roof since the rental property was held in derivation of the taxable

income.

Under “section 25-10 (3) of the ITAA 1997” a taxpayer is denied deductions for

expenses that are capital in nature (Coleman and Sadiq 2013). The section prohibits the

taxpayer from claiming deductions for repairs that involves improvement of substantial

nature. Expenses incurred in addition or alteration in the property cannot be allowed for

8TAXATION LAW

deductions under “section 25-10 (3) of the ITAA 1997”. Bruce incurs an expense of $15,000

for extending the bathroom in the investment property. The costs that is incurred in extending

the bathroom of the investment property is characterised as significant improvement. No

deduction for cost of extending the bathroom will be allowed under “section 25-10 (3)” to

Bruce.

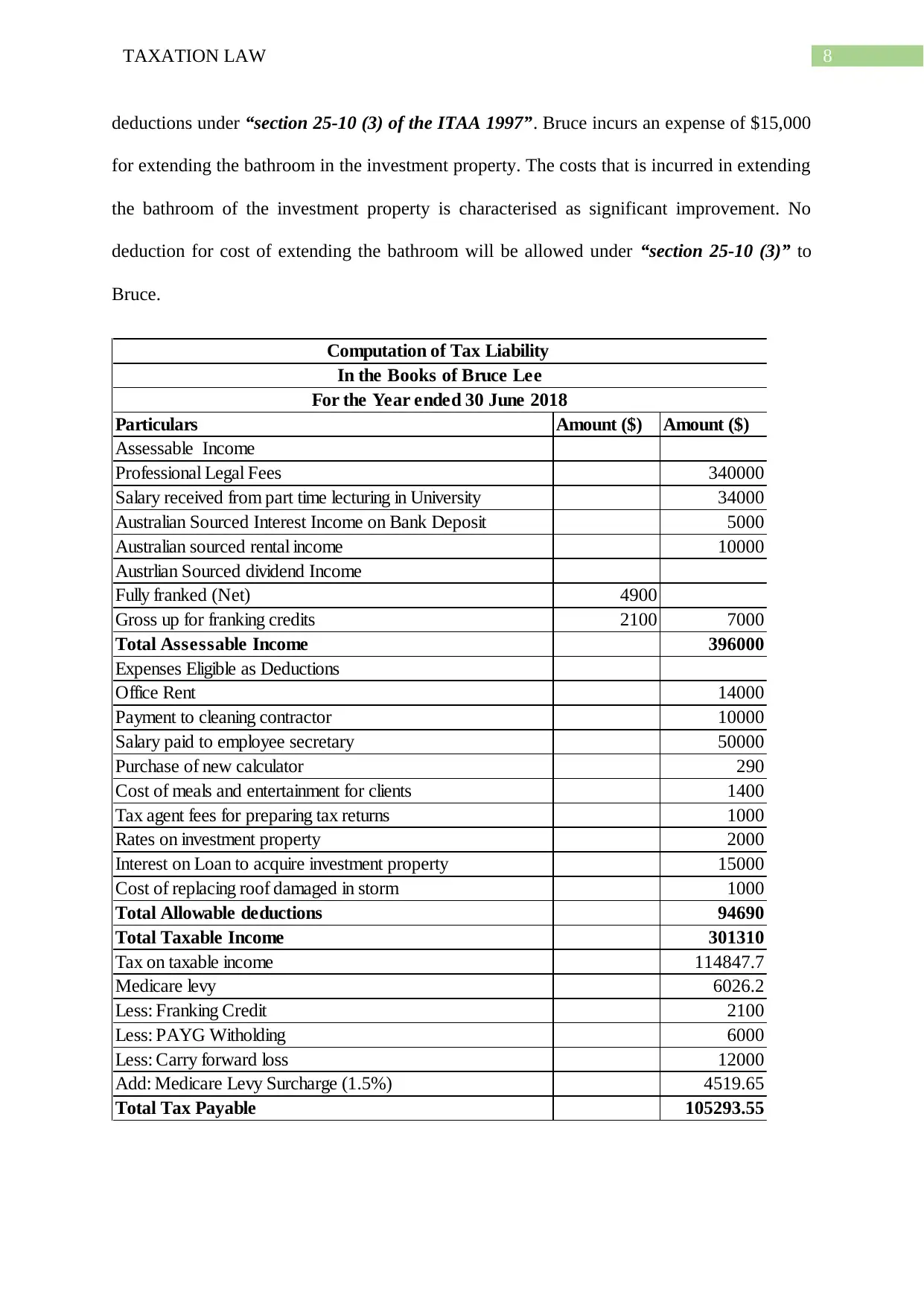

Particulars Amount ($) Amount ($)

Assessable Income

Professional Legal Fees 340000

Salary received from part time lecturing in University 34000

Australian Sourced Interest Income on Bank Deposit 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits 2100 7000

Total Assessable Income 396000

Expenses Eligible as Deductions

Office Rent 14000

Payment to cleaning contractor 10000

Salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Tax agent fees for preparing tax returns 1000

Rates on investment property 2000

Interest on Loan to acquire investment property 15000

Cost of replacing roof damaged in storm 1000

Total Allowable deductions 94690

Total Taxable Income 301310

Tax on taxable income 114847.7

Medicare levy 6026.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 4519.65

Total Tax Payable 105293.55

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

deductions under “section 25-10 (3) of the ITAA 1997”. Bruce incurs an expense of $15,000

for extending the bathroom in the investment property. The costs that is incurred in extending

the bathroom of the investment property is characterised as significant improvement. No

deduction for cost of extending the bathroom will be allowed under “section 25-10 (3)” to

Bruce.

Particulars Amount ($) Amount ($)

Assessable Income

Professional Legal Fees 340000

Salary received from part time lecturing in University 34000

Australian Sourced Interest Income on Bank Deposit 5000

Australian sourced rental income 10000

Austrlian Sourced dividend Income

Fully franked (Net) 4900

Gross up for franking credits 2100 7000

Total Assessable Income 396000

Expenses Eligible as Deductions

Office Rent 14000

Payment to cleaning contractor 10000

Salary paid to employee secretary 50000

Purchase of new calculator 290

Cost of meals and entertainment for clients 1400

Tax agent fees for preparing tax returns 1000

Rates on investment property 2000

Interest on Loan to acquire investment property 15000

Cost of replacing roof damaged in storm 1000

Total Allowable deductions 94690

Total Taxable Income 301310

Tax on taxable income 114847.7

Medicare levy 6026.2

Less: Franking Credit 2100

Less: PAYG Witholding 6000

Less: Carry forward loss 12000

Add: Medicare Levy Surcharge (1.5%) 4519.65

Total Tax Payable 105293.55

Computation of Tax Liability

In the Books of Bruce Lee

For the Year ended 30 June 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

As understood from the above stated computation the total amount of taxable income

for Bruce during the year ended 30 June 2018 stands $301,310. Bruce reported that he does

not have private health insurance therefore a Medicare levy surcharge of 1.5% will be

applicable on his assessable income. He also bought forward a loss of $12,000 from the

previous year. The loss can be used for setoff purpose which can help in reducing the tax

liability. Hence, the total tax payable for Bruce stands $105,293.55 for the income year ended

30 June 2018.

As understood from the above stated computation the total amount of taxable income

for Bruce during the year ended 30 June 2018 stands $301,310. Bruce reported that he does

not have private health insurance therefore a Medicare levy surcharge of 1.5% will be

applicable on his assessable income. He also bought forward a loss of $12,000 from the

previous year. The loss can be used for setoff purpose which can help in reducing the tax

liability. Hence, the total tax payable for Bruce stands $105,293.55 for the income year ended

30 June 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Barkoczy, S. 2014. Foundations of taxation law.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

James, S. 2014. The economics of taxation.

Jover-Ledesma, G. 2014. Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. 2013. Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Pinto, D., 2013. State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Sadiq, K. 2014. Principles of taxation law.

Swan, P.L., 2018. Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

References:

Barkoczy, S. 2014. Foundations of taxation law.

Braithwaite, V., 2017. Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Burton, M., 2017. A Review of Judicial References to the Dictum of Jordan CJ, Expressed in

Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the Purposes

of the Australian Income Tax. J. Austl. Tax'n, 19, p.50.

Coleman, C. and Sadiq, K. 2013. Principles of taxation law.

Grange, J., Jover-Ledesma, G. and Maydew, G. 2014. principles of business taxation.

James, S. 2014. The economics of taxation.

Jover-Ledesma, G. 2014. Principles of business taxation 2015. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. 2013. Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. 2013. Australian taxation law cases. Pyrmont, N.S.W.: Thomson Reuters.

Morgan, A., Mortimer, C. and Pinto, D. 2013. A practical introduction to Australian taxation

law. North Ryde [N.S.W.]: CCH Australia.

Pinto, D., 2013. State taxes. In Australian Taxation Law (pp. 1763-1762). CCH Australia

Limited.

Robin, H., 2017. Australian taxation law 2017. Oxford University Press.

Sadiq, K. 2014. Principles of taxation law.

Swan, P.L., 2018. Investment, the Corporate Tax Rate, and the Pricing of Franking Credits.

11TAXATION LAW

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2014. Australian taxation

law select.

White, J. and Townsend, A., 2018. Deductibility of employee travel expenses: The ATO's

guidance. Taxation in Australia, 52(11), p.608.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D. 2014. Australian taxation

law select.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.