Taxation Law Assignment for HI6028, T2 2019, Holmes Institute

VerifiedAdded on 2022/10/13

|10

|2114

|20

Homework Assignment

AI Summary

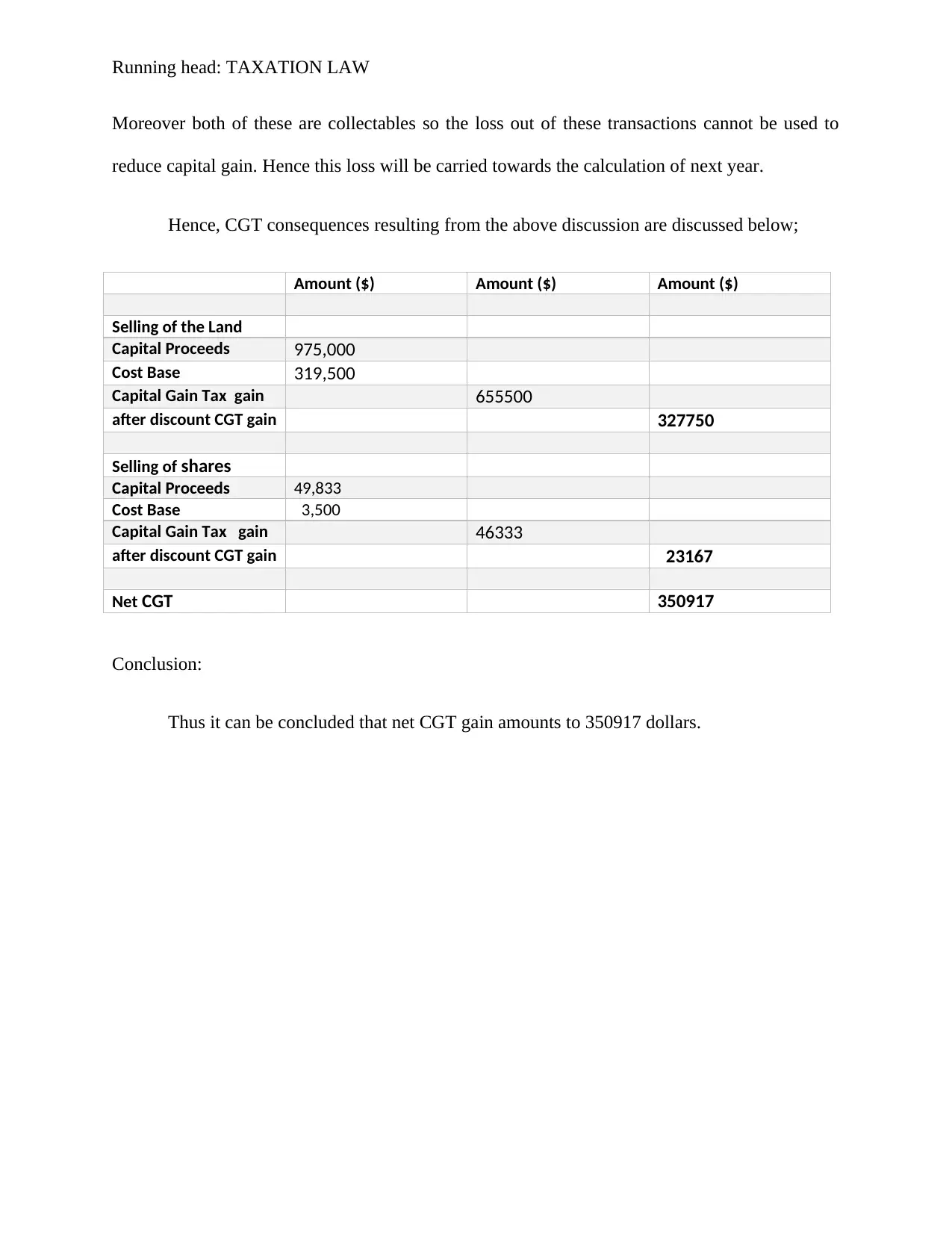

This assignment solution addresses two key taxation issues: the availability of Input Tax Credit (ITC) for a company and the Capital Gains Tax (CGT) consequences for an individual based on their transactions. The first part analyzes whether a company, City Sky Co., can claim ITC on legal services, applying the Goods and Services Tax Act 1999 (GSTA) and relevant sections on creditable acquisitions and taxable supplies. It calculates the ITC amount based on the legal service fees. The second part examines the CGT implications of various transactions made by Emma, including the sale of land, shares, a stamp collection, and a grand piano. It calculates the cost base, capital proceeds, and capital gains or losses for each transaction, applying the Income Tax Assessment Act 1997 (ITAA) and considering the 50% discount for assets held over 12 months. The conclusion summarizes the net CGT gain.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.