Taxation Law Assignment | Income Determination

13 Pages1795 Words52 Views

Added on 2020-05-28

Taxation Law Assignment | Income Determination

Added on 2020-05-28

ShareRelated Documents

TAXATION LAW1Taxation LawName of the StudentName of the UniversityAuthors NoteCourse IDTABLE OF CONTENT

S1.workpapers..........................................................................................................................1Income Related to Work............................................................................................................1Capital Gains..........................................................................................................................1Rental Property.......................................................................................................................8Tax payable, offsets and Levies.............................................................................................9Depreciation Worksheet.........................................................................................................9Reference and bibiliography:...................................................................................................11

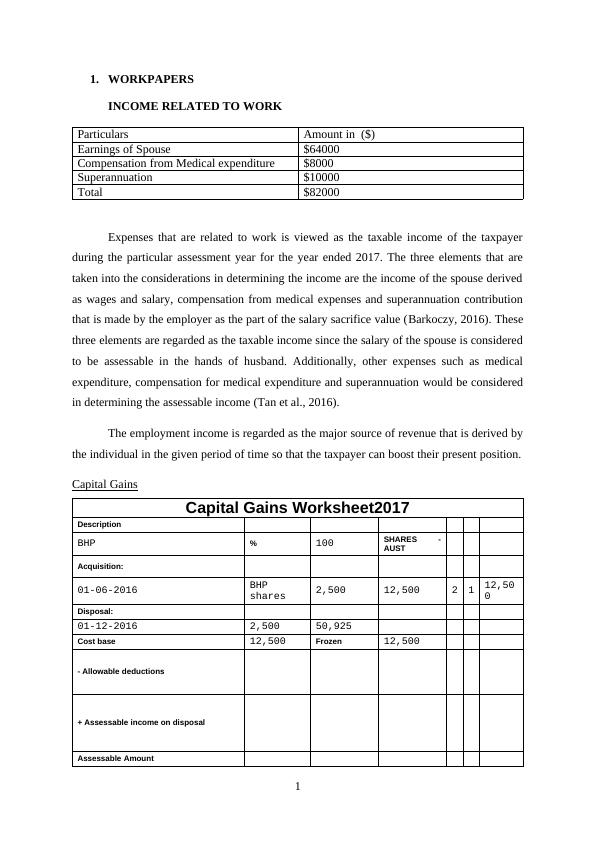

1.WORKPAPERSINCOME RELATED TO WORKParticularsAmount in ($)Earnings of Spouse$64000Compensation from Medical expenditure$8000Superannuation $10000Total$82000Expenses that are related to work is viewed as the taxable income of the taxpayerduring the particular assessment year for the year ended 2017. The three elements that aretaken into the considerations in determining the income are the income of the spouse derivedas wages and salary, compensation from medical expenses and superannuation contributionthat is made by the employer as the part of the salary sacrifice value (Barkoczy, 2016). Thesethree elements are regarded as the taxable income since the salary of the spouse is consideredto be assessable in the hands of husband. Additionally, other expenses such as medicalexpenditure, compensation for medical expenditure and superannuation would be consideredin determining the assessable income (Tan et al., 2016).The employment income is regarded as the major source of revenue that is derived bythe individual in the given period of time so that the taxpayer can boost their present position.Capital GainsCapital Gains Worksheet2017DescriptionBHP%100SHARES -AUSTAcquisition:01-06-2016BHPshares2,50012,5002112,500Disposal:01-12-20162,50050,925Cost base12,500Frozen12,500- Allowable deductions+ Assessable income on disposalAssessable Amount1

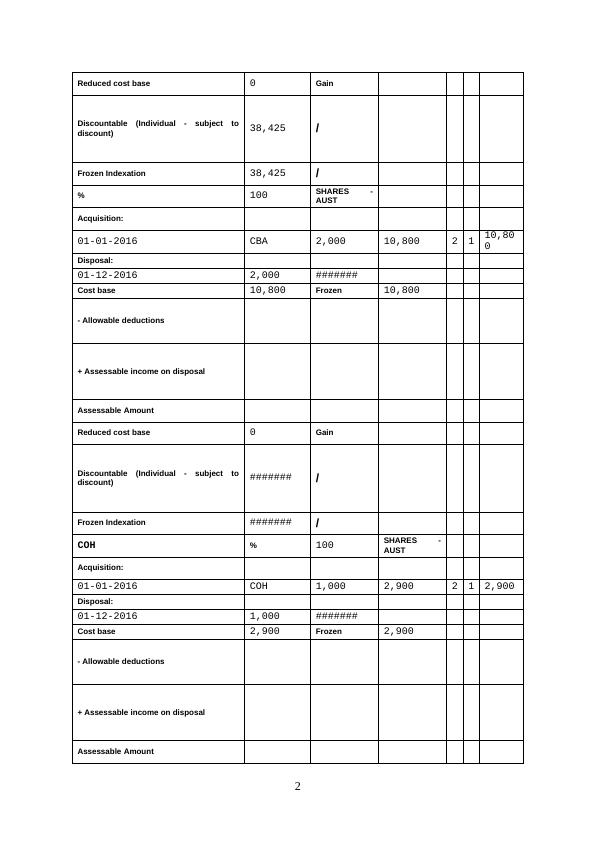

Reduced cost base0GainDiscountable (Individual - subject todiscount)38,425/Frozen Indexation38,425/%100SHARES -AUSTAcquisition:01-01-2016CBA2,00010,8002110,800Disposal:01-12-20162,000#######Cost base10,800Frozen10,800- Allowable deductions+ Assessable income on disposalAssessable AmountReduced cost base0GainDiscountable (Individual - subject todiscount)#######/Frozen Indexation#######/COH%100SHARES -AUSTAcquisition:01-01-2016COH1,0002,900212,900Disposal:01-12-20161,000#######Cost base2,900Frozen2,900- Allowable deductions+ Assessable income on disposalAssessable Amount2

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

TABL5551 Tax Law Assignmentlg...

|14

|1832

|78

Taxation Law Assignment- Assessable Incomelg...

|17

|1943

|86