Taxation Report: Taxation Analysis for Mr. Desai's Antique Business

VerifiedAdded on 2020/12/09

|10

|2744

|350

Report

AI Summary

This report analyzes the tax liabilities of Mr. Desai, an antique collector in the UK, acting as a case study. It begins with an introduction to taxation, followed by an examination of whether Mr. Desai's activities constitute trading, making him liable to pay tax. The report differentiates between tax evasion and tax avoidance, discussing HMRC's measures against abusive tax arrangements. It outlines the general rules for allowable expenditure when calculating trading profits and presents an income and expenditure statement, calculating Mr. Desai's adjusted trading profit. The report further addresses VAT registration requirements, including the registration date, submission of quarterly VAT liability, the benefits of the flat-rate scheme, and advice for handling customer payment defaults. The analysis is based on the Income Tax (Trading and Other Income) Act 2005 and Value Added Tax Act 1994, providing specific advice to Mr. Desai to comply with UK tax regulations.

Taxation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Advice to Mr. Desai....................................................................................................................1

QUESTION 2...................................................................................................................................2

a) Difference between tax evasion and tax avoidance................................................................2

b) Measures taken by HMRC to counteract any abusive arrangement.......................................3

QUESTION 3...................................................................................................................................4

a) General rule that governs whether or not expenditure is allowed when computing trading

profits..........................................................................................................................................4

b) Items of income and expenditure statement along with their explanation.............................4

c) Calculating adjusted trading profit for Mr Desai....................................................................5

QUESTION 4...................................................................................................................................6

a) Date for registering for VAT..................................................................................................6

b) How and when Desai will have to submit its quarterly VAT liability...................................6

c) Benefit of Flat – scheme for business....................................................................................6

d) Advice for customer default in their payment........................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

Advice to Mr. Desai....................................................................................................................1

QUESTION 2...................................................................................................................................2

a) Difference between tax evasion and tax avoidance................................................................2

b) Measures taken by HMRC to counteract any abusive arrangement.......................................3

QUESTION 3...................................................................................................................................4

a) General rule that governs whether or not expenditure is allowed when computing trading

profits..........................................................................................................................................4

b) Items of income and expenditure statement along with their explanation.............................4

c) Calculating adjusted trading profit for Mr Desai....................................................................5

QUESTION 4...................................................................................................................................6

a) Date for registering for VAT..................................................................................................6

b) How and when Desai will have to submit its quarterly VAT liability...................................6

c) Benefit of Flat – scheme for business....................................................................................6

d) Advice for customer default in their payment........................................................................6

CONCLUSION................................................................................................................................7

REFERENCES................................................................................................................................8

INTRODUCTION

Taxation is a charge which is imposed by government on citizens and corporate entities.

Taxation is described as a system which governmental authorities finance their expenditures by

charging money from people and spent it on various things such as education, health, public

welfare, defence and many more. Main aim of this project report is to build an understanding

about the concept of taxation in United Kingdom. In this project report, case study of Mr Desai is

evaluated who is an antique collector. As a trainee tax manager of chartered accountant firm,

situation of Mr. Desai is analysed in order to advice him about his tax liabilities. HMRC is

considered as the relevant tax authority for this case and British Taxation law is followed.

Difference between tax avoidance and tax evasion is discussed in this report along with various

measures taken by HMRC. Tax expenditures are calculated in this report for various situations

(Meade, 2013).

QUESTION 1

Advice to Mr. Desai

Mr. Desai has a vocation of collecting antiques and restoring them before selling for a

small amount of profit. Mr Desai does this activity on a regular basis and sometimes even buys

antiques in a large quantity. Neighbour of Mr. Desai informed him that HRMC can term his

activity as trading and can declare his earning an act of tax evasion.

According to Section 5 of Income tax (Trading and Other Income) Act 2005, trading is

trade that enables a user to earn any income from a profession or vocation. Taxable income from

trade under this act is defined as the profits of a trade, profession or vocation. There are various

badges mentioned in this act and six of them are discussed below:

Profit seeking motive – Badges of trade are the number of tests which are developed by

court. Motive behind conducting a trade activity is required to be identified in order to determine

whether profit motive is involved or not. In this case, Mr. Desai has a profit seeking motive

(Badges of trade, 2018).

Frequency of similar transactions – In this test, frequency of business activity

transactions are examined in order to identify whether these activities are continuous or not. In

the case of Mr. Desai, he is conducting a continuous business.

1

Taxation is a charge which is imposed by government on citizens and corporate entities.

Taxation is described as a system which governmental authorities finance their expenditures by

charging money from people and spent it on various things such as education, health, public

welfare, defence and many more. Main aim of this project report is to build an understanding

about the concept of taxation in United Kingdom. In this project report, case study of Mr Desai is

evaluated who is an antique collector. As a trainee tax manager of chartered accountant firm,

situation of Mr. Desai is analysed in order to advice him about his tax liabilities. HMRC is

considered as the relevant tax authority for this case and British Taxation law is followed.

Difference between tax avoidance and tax evasion is discussed in this report along with various

measures taken by HMRC. Tax expenditures are calculated in this report for various situations

(Meade, 2013).

QUESTION 1

Advice to Mr. Desai

Mr. Desai has a vocation of collecting antiques and restoring them before selling for a

small amount of profit. Mr Desai does this activity on a regular basis and sometimes even buys

antiques in a large quantity. Neighbour of Mr. Desai informed him that HRMC can term his

activity as trading and can declare his earning an act of tax evasion.

According to Section 5 of Income tax (Trading and Other Income) Act 2005, trading is

trade that enables a user to earn any income from a profession or vocation. Taxable income from

trade under this act is defined as the profits of a trade, profession or vocation. There are various

badges mentioned in this act and six of them are discussed below:

Profit seeking motive – Badges of trade are the number of tests which are developed by

court. Motive behind conducting a trade activity is required to be identified in order to determine

whether profit motive is involved or not. In this case, Mr. Desai has a profit seeking motive

(Badges of trade, 2018).

Frequency of similar transactions – In this test, frequency of business activity

transactions are examined in order to identify whether these activities are continuous or not. In

the case of Mr. Desai, he is conducting a continuous business.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Modification of asset – In this test, it is identified whether any assets is modified in

order to make it resalable or not. In the case of Mr. Desai, modifies antiques in order to make

little profit from re-selling them.

Nature of asset – In this test, nature of assets is identified in order to ascertain whether

the asset is for personal use or not. In the case of Mr Desai, nature of the assets are resalable.

Connection with existing trade – Under this test, asset is examined in order to ascertain

whether this asset has any connecting with individual's existing trade or not.

Financing arrangements – In this test, term for which asset is purchased is identified. It

is determined whether the asset is purchased for short term or long term. In the case of Mr.

Desai, antiques are purchased for short time period with the purpose of resale them (Kim and

et.al., 2013).

By analysing above case of Mr Desai and badges mentioned under relevant act, it has

been evaluated that Mr. Desai is involved in trade for which he is liable to pay tax. This activity

can also be termed as tax evasion.

In order to provide evidence to above statement, an example of similar case is provided

as follows: According to Salt V Chamberlain, the court of law stated that badges should be used

as a defined checklist. Motive and behaviour of activity must be analysed if any individual has

continuous profit motive then it should be considered as trade or business operation (Salt V

Chamberlain, 2018).

QUESTION 2

a) Difference between tax evasion and tax avoidance

According to Surbhi S, tax avoidance is an activity in which an individuals legally tries to

basic intention of the law by taking advantage of loop holes and shortcomings of the legal

statute. On the other hand, tax evasion is an exercise in which an assessee reduces tax liability

through illegal practices such as increasing expenses or suppressing income. Both of these

concepts are not advised to be practised as it reduces income of government (Difference between

tax evasion and tax avoidance, 2015).

Difference between these two concepts is mentioned below in order to ascertain their

legal consequence’s to Mr Desai:

Basis of difference Tax Avoidance Tax Evasion

2

order to make it resalable or not. In the case of Mr. Desai, modifies antiques in order to make

little profit from re-selling them.

Nature of asset – In this test, nature of assets is identified in order to ascertain whether

the asset is for personal use or not. In the case of Mr Desai, nature of the assets are resalable.

Connection with existing trade – Under this test, asset is examined in order to ascertain

whether this asset has any connecting with individual's existing trade or not.

Financing arrangements – In this test, term for which asset is purchased is identified. It

is determined whether the asset is purchased for short term or long term. In the case of Mr.

Desai, antiques are purchased for short time period with the purpose of resale them (Kim and

et.al., 2013).

By analysing above case of Mr Desai and badges mentioned under relevant act, it has

been evaluated that Mr. Desai is involved in trade for which he is liable to pay tax. This activity

can also be termed as tax evasion.

In order to provide evidence to above statement, an example of similar case is provided

as follows: According to Salt V Chamberlain, the court of law stated that badges should be used

as a defined checklist. Motive and behaviour of activity must be analysed if any individual has

continuous profit motive then it should be considered as trade or business operation (Salt V

Chamberlain, 2018).

QUESTION 2

a) Difference between tax evasion and tax avoidance

According to Surbhi S, tax avoidance is an activity in which an individuals legally tries to

basic intention of the law by taking advantage of loop holes and shortcomings of the legal

statute. On the other hand, tax evasion is an exercise in which an assessee reduces tax liability

through illegal practices such as increasing expenses or suppressing income. Both of these

concepts are not advised to be practised as it reduces income of government (Difference between

tax evasion and tax avoidance, 2015).

Difference between these two concepts is mentioned below in order to ascertain their

legal consequence’s to Mr Desai:

Basis of difference Tax Avoidance Tax Evasion

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

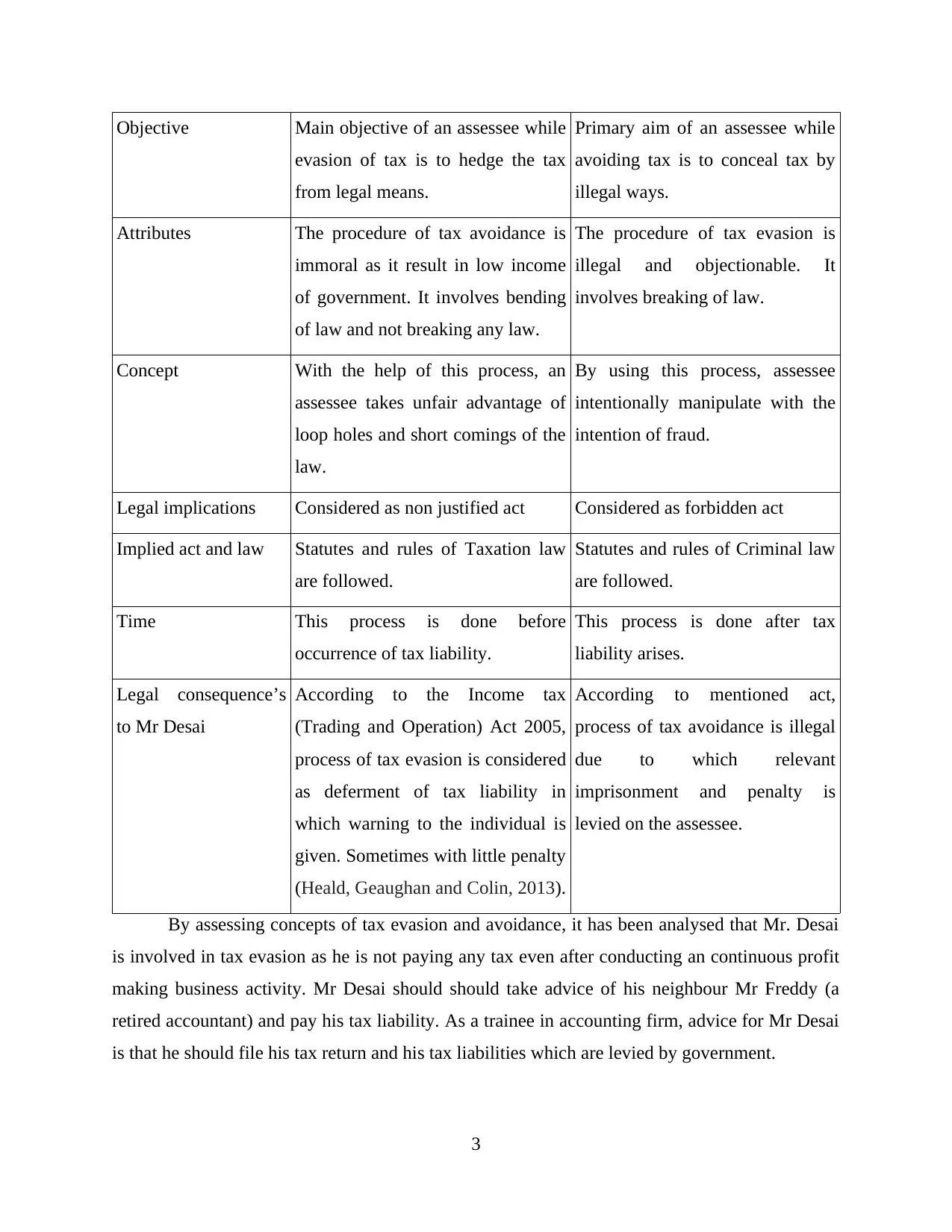

Objective Main objective of an assessee while

evasion of tax is to hedge the tax

from legal means.

Primary aim of an assessee while

avoiding tax is to conceal tax by

illegal ways.

Attributes The procedure of tax avoidance is

immoral as it result in low income

of government. It involves bending

of law and not breaking any law.

The procedure of tax evasion is

illegal and objectionable. It

involves breaking of law.

Concept With the help of this process, an

assessee takes unfair advantage of

loop holes and short comings of the

law.

By using this process, assessee

intentionally manipulate with the

intention of fraud.

Legal implications Considered as non justified act Considered as forbidden act

Implied act and law Statutes and rules of Taxation law

are followed.

Statutes and rules of Criminal law

are followed.

Time This process is done before

occurrence of tax liability.

This process is done after tax

liability arises.

Legal consequence’s

to Mr Desai

According to the Income tax

(Trading and Operation) Act 2005,

process of tax evasion is considered

as deferment of tax liability in

which warning to the individual is

given. Sometimes with little penalty

(Heald, Geaughan and Colin, 2013).

According to mentioned act,

process of tax avoidance is illegal

due to which relevant

imprisonment and penalty is

levied on the assessee.

By assessing concepts of tax evasion and avoidance, it has been analysed that Mr. Desai

is involved in tax evasion as he is not paying any tax even after conducting an continuous profit

making business activity. Mr Desai should should take advice of his neighbour Mr Freddy (a

retired accountant) and pay his tax liability. As a trainee in accounting firm, advice for Mr Desai

is that he should file his tax return and his tax liabilities which are levied by government.

3

evasion of tax is to hedge the tax

from legal means.

Primary aim of an assessee while

avoiding tax is to conceal tax by

illegal ways.

Attributes The procedure of tax avoidance is

immoral as it result in low income

of government. It involves bending

of law and not breaking any law.

The procedure of tax evasion is

illegal and objectionable. It

involves breaking of law.

Concept With the help of this process, an

assessee takes unfair advantage of

loop holes and short comings of the

law.

By using this process, assessee

intentionally manipulate with the

intention of fraud.

Legal implications Considered as non justified act Considered as forbidden act

Implied act and law Statutes and rules of Taxation law

are followed.

Statutes and rules of Criminal law

are followed.

Time This process is done before

occurrence of tax liability.

This process is done after tax

liability arises.

Legal consequence’s

to Mr Desai

According to the Income tax

(Trading and Operation) Act 2005,

process of tax evasion is considered

as deferment of tax liability in

which warning to the individual is

given. Sometimes with little penalty

(Heald, Geaughan and Colin, 2013).

According to mentioned act,

process of tax avoidance is illegal

due to which relevant

imprisonment and penalty is

levied on the assessee.

By assessing concepts of tax evasion and avoidance, it has been analysed that Mr. Desai

is involved in tax evasion as he is not paying any tax even after conducting an continuous profit

making business activity. Mr Desai should should take advice of his neighbour Mr Freddy (a

retired accountant) and pay his tax liability. As a trainee in accounting firm, advice for Mr Desai

is that he should file his tax return and his tax liabilities which are levied by government.

3

b) Measures taken by HMRC to counteract any abusive arrangement

Abusive tax arrangement is the scheme by which assessee tries to deliberately manipulate

taxation law in order to conduct tax evasion. In order to counteract these arrangements, HMRC

can few measures. HM Revenues and Customs is a department of UK Government which is

responsible for collection of taxes. HMRC measures, includes penalties which are levied on

individuals who are involved in abusive tax arrangements. The amount of these penalties are

calculated from the gross consideration which is earned by the assessee from tax evasion (Crook,

Henneberry and Whitehead, 2015).

QUESTION 3

a) General rule that governs whether or not expenditure is allowed when computing trading

profits

According to Section 3(c) of Income tax (Trading and Other Income) Act 2005, trading

profit is the difference between earned income and allowable expenses. General rule of this law

states that taxable profit should be deducted with expenditures which are governed by

governmental authorities. Main aim for developing these type of rules is to levy relevant tax

liabilities on corporate entities and prevent any abusive tax arrangements. While computing

trading profit for the year ending 31 December 2017, Mr. Desai should deduct only allowable

expenses from operational earnings. Allowance expenses includes operational expenses,

depreciation, gifts to employees, donations, legal charges and many more. Disallowed expenses

includes fines, penalties and many more.

b) Items of income and expenditure statement along with their explanation

In order to prepare an adjusted income statement for Mr. Desai's business, it is important

to deduct only those expenses which are allowed by taxation authority of United Kingdom.

Various items of income and expenditure statement along with their explanation is depicted

below:

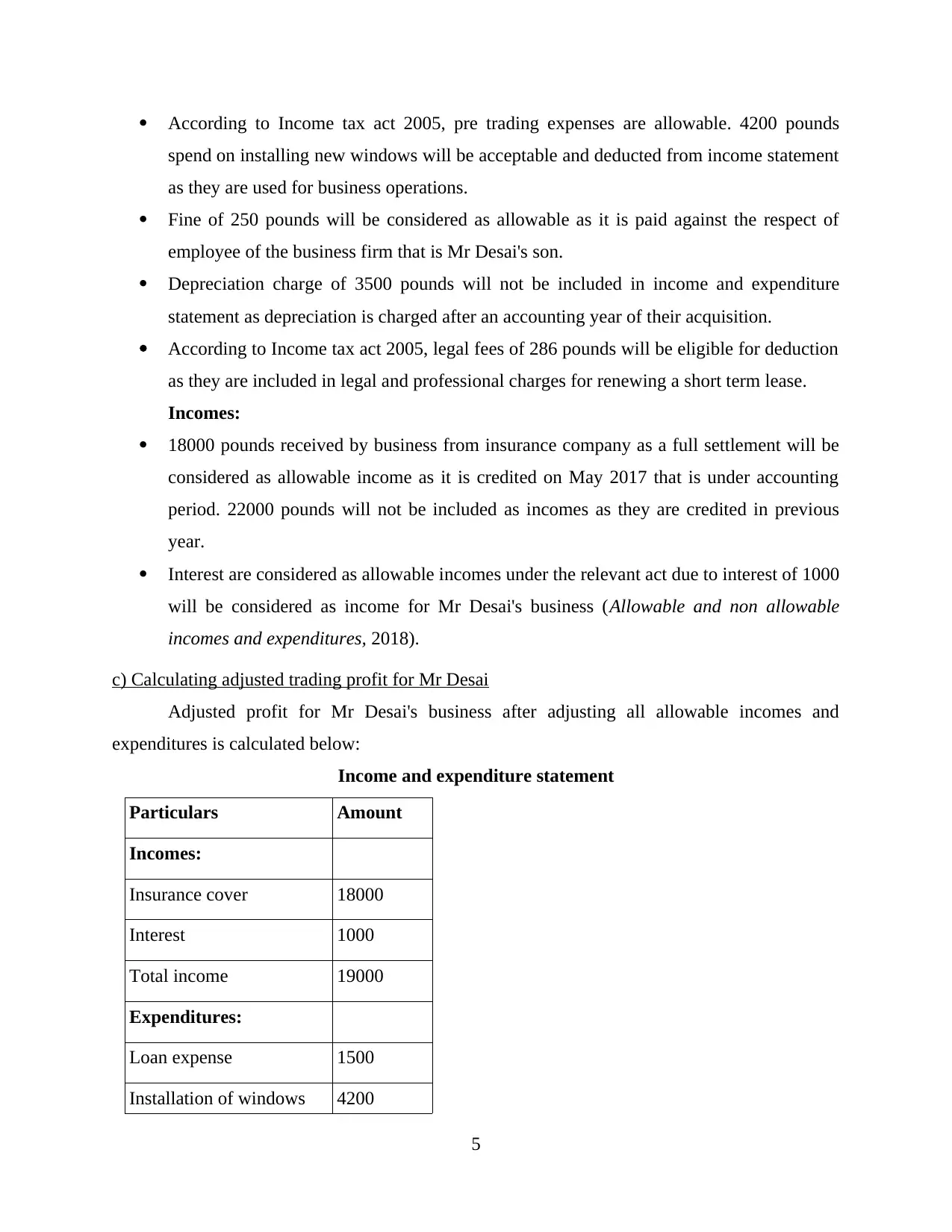

Expenditures:

According to Income tax act 2005, legal and professional charges such as costs of

obtaining loan finance are eligible to be deducted from trading income. The sum of 1500

pounds will be included in income and expenditure statement as loan is acquired for

business purposes due to which, this will be considered as operational expenses.

4

Abusive tax arrangement is the scheme by which assessee tries to deliberately manipulate

taxation law in order to conduct tax evasion. In order to counteract these arrangements, HMRC

can few measures. HM Revenues and Customs is a department of UK Government which is

responsible for collection of taxes. HMRC measures, includes penalties which are levied on

individuals who are involved in abusive tax arrangements. The amount of these penalties are

calculated from the gross consideration which is earned by the assessee from tax evasion (Crook,

Henneberry and Whitehead, 2015).

QUESTION 3

a) General rule that governs whether or not expenditure is allowed when computing trading

profits

According to Section 3(c) of Income tax (Trading and Other Income) Act 2005, trading

profit is the difference between earned income and allowable expenses. General rule of this law

states that taxable profit should be deducted with expenditures which are governed by

governmental authorities. Main aim for developing these type of rules is to levy relevant tax

liabilities on corporate entities and prevent any abusive tax arrangements. While computing

trading profit for the year ending 31 December 2017, Mr. Desai should deduct only allowable

expenses from operational earnings. Allowance expenses includes operational expenses,

depreciation, gifts to employees, donations, legal charges and many more. Disallowed expenses

includes fines, penalties and many more.

b) Items of income and expenditure statement along with their explanation

In order to prepare an adjusted income statement for Mr. Desai's business, it is important

to deduct only those expenses which are allowed by taxation authority of United Kingdom.

Various items of income and expenditure statement along with their explanation is depicted

below:

Expenditures:

According to Income tax act 2005, legal and professional charges such as costs of

obtaining loan finance are eligible to be deducted from trading income. The sum of 1500

pounds will be included in income and expenditure statement as loan is acquired for

business purposes due to which, this will be considered as operational expenses.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to Income tax act 2005, pre trading expenses are allowable. 4200 pounds

spend on installing new windows will be acceptable and deducted from income statement

as they are used for business operations.

Fine of 250 pounds will be considered as allowable as it is paid against the respect of

employee of the business firm that is Mr Desai's son.

Depreciation charge of 3500 pounds will not be included in income and expenditure

statement as depreciation is charged after an accounting year of their acquisition.

According to Income tax act 2005, legal fees of 286 pounds will be eligible for deduction

as they are included in legal and professional charges for renewing a short term lease.

Incomes:

18000 pounds received by business from insurance company as a full settlement will be

considered as allowable income as it is credited on May 2017 that is under accounting

period. 22000 pounds will not be included as incomes as they are credited in previous

year.

Interest are considered as allowable incomes under the relevant act due to interest of 1000

will be considered as income for Mr Desai's business (Allowable and non allowable

incomes and expenditures, 2018).

c) Calculating adjusted trading profit for Mr Desai

Adjusted profit for Mr Desai's business after adjusting all allowable incomes and

expenditures is calculated below:

Income and expenditure statement

Particulars Amount

Incomes:

Insurance cover 18000

Interest 1000

Total income 19000

Expenditures:

Loan expense 1500

Installation of windows 4200

5

spend on installing new windows will be acceptable and deducted from income statement

as they are used for business operations.

Fine of 250 pounds will be considered as allowable as it is paid against the respect of

employee of the business firm that is Mr Desai's son.

Depreciation charge of 3500 pounds will not be included in income and expenditure

statement as depreciation is charged after an accounting year of their acquisition.

According to Income tax act 2005, legal fees of 286 pounds will be eligible for deduction

as they are included in legal and professional charges for renewing a short term lease.

Incomes:

18000 pounds received by business from insurance company as a full settlement will be

considered as allowable income as it is credited on May 2017 that is under accounting

period. 22000 pounds will not be included as incomes as they are credited in previous

year.

Interest are considered as allowable incomes under the relevant act due to interest of 1000

will be considered as income for Mr Desai's business (Allowable and non allowable

incomes and expenditures, 2018).

c) Calculating adjusted trading profit for Mr Desai

Adjusted profit for Mr Desai's business after adjusting all allowable incomes and

expenditures is calculated below:

Income and expenditure statement

Particulars Amount

Incomes:

Insurance cover 18000

Interest 1000

Total income 19000

Expenditures:

Loan expense 1500

Installation of windows 4200

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fine 250

Legal fee 286

Total expenditure 6236

Net profit 12764

After adjusting all income and expenditures, net income of Mr Desai's business

ascertained as 12764 pounds.

QUESTION 4

a) Date for registering for VAT

According to Value Added tax Act 1994, threshold limit for VAT registration for 2017 is

85000 pounds (Threshold limit for VAT, 2018.). If any business entity exceeds this limit then

they have to pay fine. VAT registration must be done within 30 days of exceeding this limit. In

this case of Mr Desai, his business touched this threshold limit on November 2017, as his

business earned a sum of 165000 pounds (20000 in August + 40000 in September + 105000 in

November). Mr Desai must register his firm with VAT till 31 December 2017. This information

of registration for VAT must be notified to HMRC as soon as business has touched threshold

limit of 85000 pounds.

b) How and when Desai will have to submit its quarterly VAT liability

Mr. Desai will submit his quarterly VAT liability for the fourth quarter (October,

November and December) on 7 February 2018. As Vat return should be filed online within one

month and seven days of the end of the relevant quarter. This return will be filed using total Vat

input and output.

c) Benefit of Flat – scheme for business

Flat rate scheme is a system of VAT which advice all small business entities to register

for Vat even if they is no requirement as they are earning as much of its threshold limit. This

scheme enables a business entity to generate their VAT unique number by which trust on the

organisation builds which leads towards profitability. By using this scheme, small businesses can

claim back VAT on capital expenditures and services (Bond and Guceri, 2012).

6

Legal fee 286

Total expenditure 6236

Net profit 12764

After adjusting all income and expenditures, net income of Mr Desai's business

ascertained as 12764 pounds.

QUESTION 4

a) Date for registering for VAT

According to Value Added tax Act 1994, threshold limit for VAT registration for 2017 is

85000 pounds (Threshold limit for VAT, 2018.). If any business entity exceeds this limit then

they have to pay fine. VAT registration must be done within 30 days of exceeding this limit. In

this case of Mr Desai, his business touched this threshold limit on November 2017, as his

business earned a sum of 165000 pounds (20000 in August + 40000 in September + 105000 in

November). Mr Desai must register his firm with VAT till 31 December 2017. This information

of registration for VAT must be notified to HMRC as soon as business has touched threshold

limit of 85000 pounds.

b) How and when Desai will have to submit its quarterly VAT liability

Mr. Desai will submit his quarterly VAT liability for the fourth quarter (October,

November and December) on 7 February 2018. As Vat return should be filed online within one

month and seven days of the end of the relevant quarter. This return will be filed using total Vat

input and output.

c) Benefit of Flat – scheme for business

Flat rate scheme is a system of VAT which advice all small business entities to register

for Vat even if they is no requirement as they are earning as much of its threshold limit. This

scheme enables a business entity to generate their VAT unique number by which trust on the

organisation builds which leads towards profitability. By using this scheme, small businesses can

claim back VAT on capital expenditures and services (Bond and Guceri, 2012).

6

d) Advice for customer default in their payment

When a business entity faces situation where customers default in their payments, there

are various methods for handling these situations such as develop strict rules and policies, initiate

legal, proceedings, chase the debt and report a default. For Mr Desai's business it is consider that

this firm should develop strict rules for payment by creditors as it will bring efficiency in

organisation.

CONCLUSION

From the above project report, it has been ascertained that taxation is a legal system

which levies tax on individuals and corporate entity. After conducting various analysis it is

ascertained that Mr Desai is involved in an tax evasion process. Trading profit is calculated by

including allowable incomes and expenditures only in order to ensure effective taxation system

by government.

7

When a business entity faces situation where customers default in their payments, there

are various methods for handling these situations such as develop strict rules and policies, initiate

legal, proceedings, chase the debt and report a default. For Mr Desai's business it is consider that

this firm should develop strict rules for payment by creditors as it will bring efficiency in

organisation.

CONCLUSION

From the above project report, it has been ascertained that taxation is a legal system

which levies tax on individuals and corporate entity. After conducting various analysis it is

ascertained that Mr Desai is involved in an tax evasion process. Trading profit is calculated by

including allowable incomes and expenditures only in order to ensure effective taxation system

by government.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals

Bond, S. and Guceri, I., 2012. Trends in UK BERD after the introduction of R&D tax credits.

Crook, T., Henneberry, J. and Whitehead, C., 2015. Introduction. Planning Gain: Providing

Infrastructure and Affordable Housing, pp.1-19.

Heald, D., Geaughan, N. and Colin, R., 2013. Financial arrangements for UK devolution. In

Remaking the Union (pp. 29-58). Routledge.

Kim, J., and et.al., 2013. Attitudes towards road pricing and environmental taxation among US

and UK students. Transportation Research Part A: Policy and Practice. 48. pp.50-62.

Meade, J. E., 2013. The Structure and Reform of Direct Taxation (Routledge Revivals).

Routledge.

Online

Badges of trade. 2010. [Online]. Available through:

<http://www1.lexisnexis.co.uk/taxtutor/public/business/2a_business_tax/2a10-

01(F).pdf>

Salt V Chamberlain. 2018. [Online]. Available through:

<https://www.taxation.co.uk/Articles/2011/06/29/277131/youre-trading>

Difference between tax evasion and tax avoidance. 2015. [Online]. Available through:

<https://keydifferences.com/difference-between-tax-avoidance-and-tax-evasion.html>

Allowable and non allowable incomes and expenditures. 2018. [Online]. Available through:

<https://www.acowtancy.com/textbook/acca-tx/b3-income-from-self-employment/b3c-

allowable-expenditure/notes>

Threshold limit for VAT. 2018. [Online]. Available through:

<https://www.kashflow.com/should-i-register-for-vat/>

8

Books and Journals

Bond, S. and Guceri, I., 2012. Trends in UK BERD after the introduction of R&D tax credits.

Crook, T., Henneberry, J. and Whitehead, C., 2015. Introduction. Planning Gain: Providing

Infrastructure and Affordable Housing, pp.1-19.

Heald, D., Geaughan, N. and Colin, R., 2013. Financial arrangements for UK devolution. In

Remaking the Union (pp. 29-58). Routledge.

Kim, J., and et.al., 2013. Attitudes towards road pricing and environmental taxation among US

and UK students. Transportation Research Part A: Policy and Practice. 48. pp.50-62.

Meade, J. E., 2013. The Structure and Reform of Direct Taxation (Routledge Revivals).

Routledge.

Online

Badges of trade. 2010. [Online]. Available through:

<http://www1.lexisnexis.co.uk/taxtutor/public/business/2a_business_tax/2a10-

01(F).pdf>

Salt V Chamberlain. 2018. [Online]. Available through:

<https://www.taxation.co.uk/Articles/2011/06/29/277131/youre-trading>

Difference between tax evasion and tax avoidance. 2015. [Online]. Available through:

<https://keydifferences.com/difference-between-tax-avoidance-and-tax-evasion.html>

Allowable and non allowable incomes and expenditures. 2018. [Online]. Available through:

<https://www.acowtancy.com/textbook/acca-tx/b3-income-from-self-employment/b3c-

allowable-expenditure/notes>

Threshold limit for VAT. 2018. [Online]. Available through:

<https://www.kashflow.com/should-i-register-for-vat/>

8

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.