Taxation Law Assignment Solution

VerifiedAdded on 2023/06/15

|10

|1771

|164

AI Summary

This assignment solution provides answers to questions related to PayG deductions, superannuation guarantee obligation, computation of net tax payable, GST credits, and PAYG tax withheld. The solution also includes a business activity statement and a reference list. The subject is Taxation Law and the course code and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................5

Reference List:...........................................................................................................................9

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................5

Reference List:...........................................................................................................................9

2TAXATION LAW

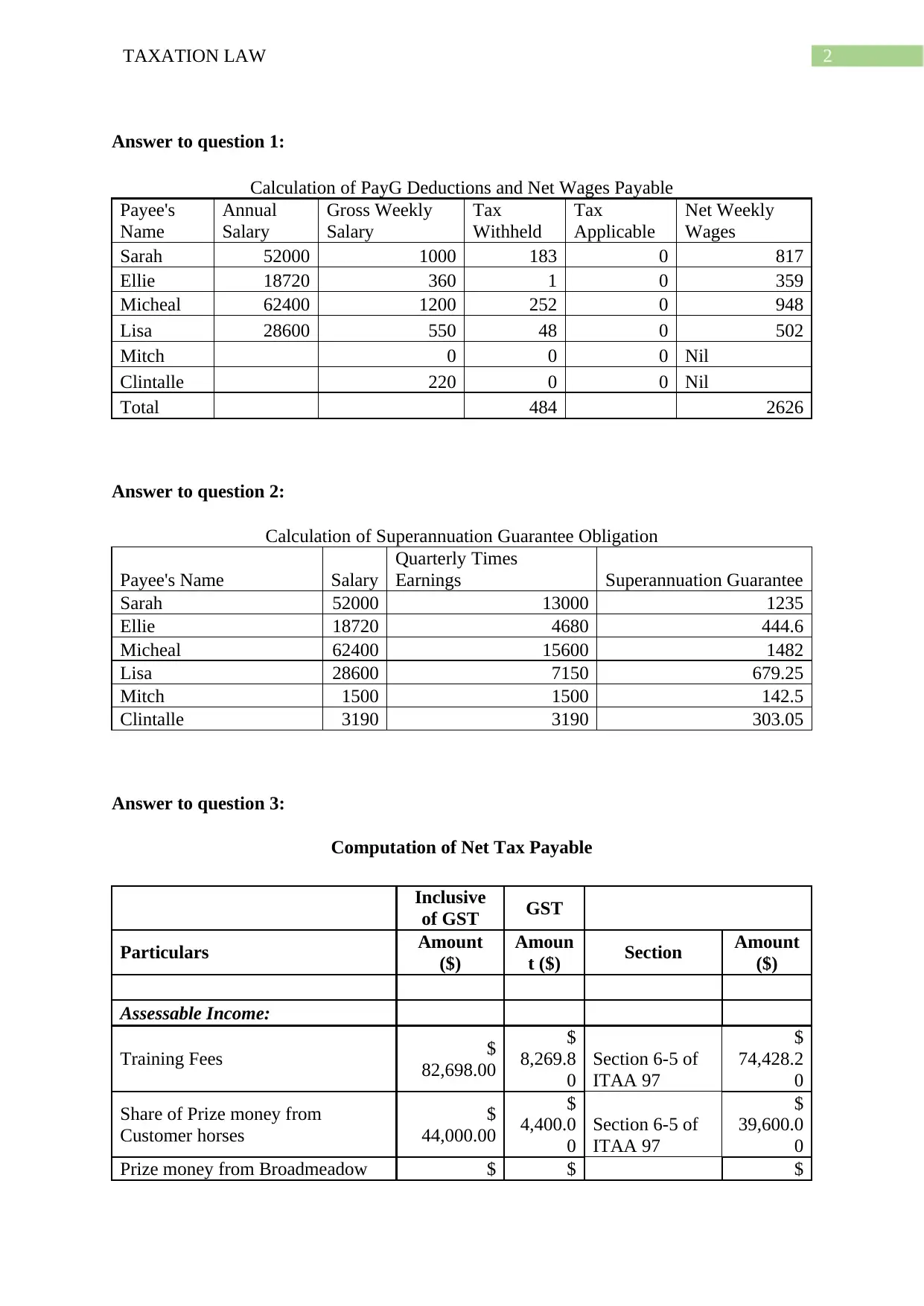

Answer to question 1:

Calculation of PayG Deductions and Net Wages Payable

Payee's

Name

Annual

Salary

Gross Weekly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah 52000 1000 183 0 817

Ellie 18720 360 1 0 359

Micheal 62400 1200 252 0 948

Lisa 28600 550 48 0 502

Mitch 0 0 0 Nil

Clintalle 220 0 0 Nil

Total 484 2626

Answer to question 2:

Calculation of Superannuation Guarantee Obligation

Payee's Name Salary

Quarterly Times

Earnings Superannuation Guarantee

Sarah 52000 13000 1235

Ellie 18720 4680 444.6

Micheal 62400 15600 1482

Lisa 28600 7150 679.25

Mitch 1500 1500 142.5

Clintalle 3190 3190 303.05

Answer to question 3:

Computation of Net Tax Payable

Inclusive

of GST GST

Particulars Amount

($)

Amoun

t ($) Section Amount

($)

Assessable Income:

Training Fees $

82,698.00

$

8,269.8

0

Section 6-5 of

ITAA 97

$

74,428.2

0

Share of Prize money from

Customer horses

$

44,000.00

$

4,400.0

0

Section 6-5 of

ITAA 97

$

39,600.0

0

Prize money from Broadmeadow $ $ $

Answer to question 1:

Calculation of PayG Deductions and Net Wages Payable

Payee's

Name

Annual

Salary

Gross Weekly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah 52000 1000 183 0 817

Ellie 18720 360 1 0 359

Micheal 62400 1200 252 0 948

Lisa 28600 550 48 0 502

Mitch 0 0 0 Nil

Clintalle 220 0 0 Nil

Total 484 2626

Answer to question 2:

Calculation of Superannuation Guarantee Obligation

Payee's Name Salary

Quarterly Times

Earnings Superannuation Guarantee

Sarah 52000 13000 1235

Ellie 18720 4680 444.6

Micheal 62400 15600 1482

Lisa 28600 7150 679.25

Mitch 1500 1500 142.5

Clintalle 3190 3190 303.05

Answer to question 3:

Computation of Net Tax Payable

Inclusive

of GST GST

Particulars Amount

($)

Amoun

t ($) Section Amount

($)

Assessable Income:

Training Fees $

82,698.00

$

8,269.8

0

Section 6-5 of

ITAA 97

$

74,428.2

0

Share of Prize money from

Customer horses

$

44,000.00

$

4,400.0

0

Section 6-5 of

ITAA 97

$

39,600.0

0

Prize money from Broadmeadow $ $ $

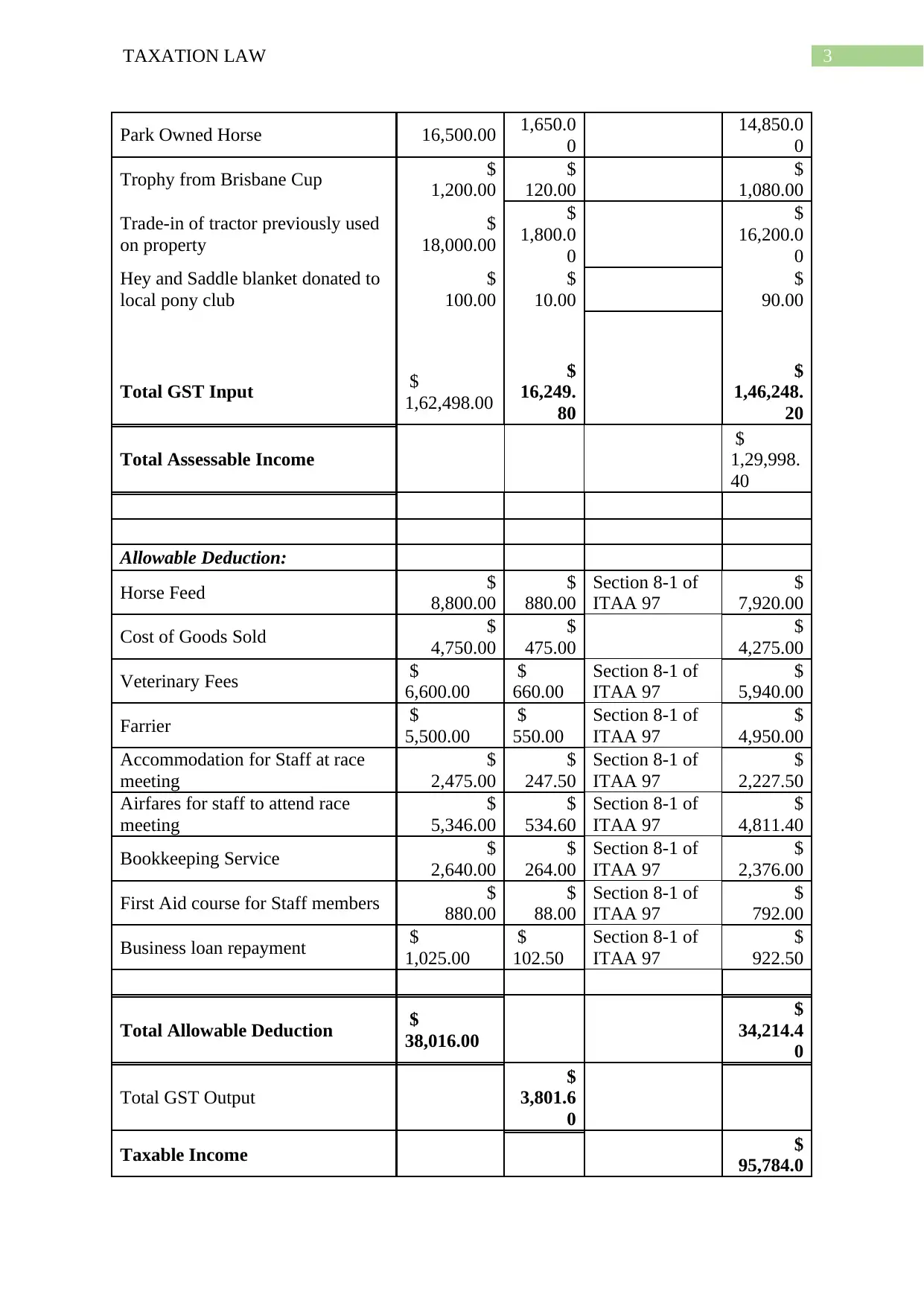

3TAXATION LAW

Park Owned Horse 16,500.00 1,650.0

0

14,850.0

0

Trophy from Brisbane Cup $

1,200.00

$

120.00

$

1,080.00

Trade-in of tractor previously used

on property

$

18,000.00

$

1,800.0

0

$

16,200.0

0

Hey and Saddle blanket donated to

local pony club

$

100.00

$

10.00

$

90.00

Total GST Input $

1,62,498.00

$

16,249.

80

$

1,46,248.

20

Total Assessable Income

$

1,29,998.

40

Allowable Deduction:

Horse Feed $

8,800.00

$

880.00

Section 8-1 of

ITAA 97

$

7,920.00

Cost of Goods Sold $

4,750.00

$

475.00

$

4,275.00

Veterinary Fees $

6,600.00

$

660.00

Section 8-1 of

ITAA 97

$

5,940.00

Farrier $

5,500.00

$

550.00

Section 8-1 of

ITAA 97

$

4,950.00

Accommodation for Staff at race

meeting

$

2,475.00

$

247.50

Section 8-1 of

ITAA 97

$

2,227.50

Airfares for staff to attend race

meeting

$

5,346.00

$

534.60

Section 8-1 of

ITAA 97

$

4,811.40

Bookkeeping Service $

2,640.00

$

264.00

Section 8-1 of

ITAA 97

$

2,376.00

First Aid course for Staff members $

880.00

$

88.00

Section 8-1 of

ITAA 97

$

792.00

Business loan repayment $

1,025.00

$

102.50

Section 8-1 of

ITAA 97

$

922.50

Total Allowable Deduction $

38,016.00

$

34,214.4

0

Total GST Output

$

3,801.6

0

Taxable Income $

95,784.0

Park Owned Horse 16,500.00 1,650.0

0

14,850.0

0

Trophy from Brisbane Cup $

1,200.00

$

120.00

$

1,080.00

Trade-in of tractor previously used

on property

$

18,000.00

$

1,800.0

0

$

16,200.0

0

Hey and Saddle blanket donated to

local pony club

$

100.00

$

10.00

$

90.00

Total GST Input $

1,62,498.00

$

16,249.

80

$

1,46,248.

20

Total Assessable Income

$

1,29,998.

40

Allowable Deduction:

Horse Feed $

8,800.00

$

880.00

Section 8-1 of

ITAA 97

$

7,920.00

Cost of Goods Sold $

4,750.00

$

475.00

$

4,275.00

Veterinary Fees $

6,600.00

$

660.00

Section 8-1 of

ITAA 97

$

5,940.00

Farrier $

5,500.00

$

550.00

Section 8-1 of

ITAA 97

$

4,950.00

Accommodation for Staff at race

meeting

$

2,475.00

$

247.50

Section 8-1 of

ITAA 97

$

2,227.50

Airfares for staff to attend race

meeting

$

5,346.00

$

534.60

Section 8-1 of

ITAA 97

$

4,811.40

Bookkeeping Service $

2,640.00

$

264.00

Section 8-1 of

ITAA 97

$

2,376.00

First Aid course for Staff members $

880.00

$

88.00

Section 8-1 of

ITAA 97

$

792.00

Business loan repayment $

1,025.00

$

102.50

Section 8-1 of

ITAA 97

$

922.50

Total Allowable Deduction $

38,016.00

$

34,214.4

0

Total GST Output

$

3,801.6

0

Taxable Income $

95,784.0

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

0

Total GST Payable

$

12,448.2

0

As stated under “section 6-5 of the Income tax assessment act 1997” income that is

earned directly from the business activities will be considered as the assessable income. As

evident from the present situation it is found that Broadmeadow Park earned income from

training fees will be held assessable under “section 6-5 of the ITAA 1997” (Barkoczy 2016).

There were other receipts such as share of prize money, trophy from Brisbane Cup and trade

in tractor would be considered for assessment and would attract tax liability.

Additionally, the receipts derived would be considered for GST under the GSTR 1999

for the receipts of supplies. Furthermore, it has been noticed that a Broeadmeadow incurred

expenditure which can be considered as allowable deductions under “section 8-1 of the

ITAA 1997”. A business can claim an allowable deduction for the salaries and wages that is

paid by the company to their workers along with the superannuation contribution made for

them (Woellner et al. 2016). Since the business carried on by the Jimmy is a company

therefore, as per the Australian taxation office Broadmeadow can claim an allowable

deduction for the wages that is paid by the company to the workers. Additionally, it has also

been found that Broadmeadow incurred a superannuation expenditure on the employees.

Therefore, the business can claim an allowable deduction on the superannuation contribution

which they make in compliance with the super fund for the certain employees.

The taxation ruling of 97/17 states that a deduction under “section 32-5 of the ITAA

1997” would not be considered as an allowable deduction since they are entertainment by

food or drink. Jimmy, incurs an expenditure on the local restaurant for its customers.

“Division 32 of the ITAA” states the general prohibition regarding the deductibility of the

0

Total GST Payable

$

12,448.2

0

As stated under “section 6-5 of the Income tax assessment act 1997” income that is

earned directly from the business activities will be considered as the assessable income. As

evident from the present situation it is found that Broadmeadow Park earned income from

training fees will be held assessable under “section 6-5 of the ITAA 1997” (Barkoczy 2016).

There were other receipts such as share of prize money, trophy from Brisbane Cup and trade

in tractor would be considered for assessment and would attract tax liability.

Additionally, the receipts derived would be considered for GST under the GSTR 1999

for the receipts of supplies. Furthermore, it has been noticed that a Broeadmeadow incurred

expenditure which can be considered as allowable deductions under “section 8-1 of the

ITAA 1997”. A business can claim an allowable deduction for the salaries and wages that is

paid by the company to their workers along with the superannuation contribution made for

them (Woellner et al. 2016). Since the business carried on by the Jimmy is a company

therefore, as per the Australian taxation office Broadmeadow can claim an allowable

deduction for the wages that is paid by the company to the workers. Additionally, it has also

been found that Broadmeadow incurred a superannuation expenditure on the employees.

Therefore, the business can claim an allowable deduction on the superannuation contribution

which they make in compliance with the super fund for the certain employees.

The taxation ruling of 97/17 states that a deduction under “section 32-5 of the ITAA

1997” would not be considered as an allowable deduction since they are entertainment by

food or drink. Jimmy, incurs an expenditure on the local restaurant for its customers.

“Division 32 of the ITAA” states the general prohibition regarding the deductibility of the

5TAXATION LAW

expenditure incurred on entertainment. As held in the case of “Bow and others v. Heatly

(1960) STL 311” stated that entertainment expenditure incurred on meal would be

considered as non-allowable deduction. Therefore, the meal expenditure would constitute as

fringe benefit under the “Fringe Benefit Tax Assessment Act 1986” and would be subjected

to Fringe Benefit Tax (Woellner et al. 2016). Additionally, “Division 9A under Part III of

the FBTAA” provides an employer that provides meal entertainment to the associates to

consider the value of the benefit by using either of the two methods. Therefore, in respect of

the “Section 8-1 of the ITAA 1997” Jimmy can claim an allowable deduction for the

expenses incurred and the GST amount would be payable in respect of the GSTR 1999.

Answer to question 4:

According to the Australian taxation office a person can GST credits given that the

business is registered to claim GST credits. As a result, Jimmy can claim a GST credits

however he would be required to obtain a GST registration. Since Jimmy has obtained the

registration, he can claim GST credits for the amount of GST that is included in the price he

pays for the things that is used in his business. However, it is found that Farrier is not

registered for GST and Jimmy would not be allowed for claiming GST credits since the

Farrier is not registered for GST.

There are large number of factors that ascertains whether an acquisition would be

considered as creditable purpose and for which input tax credit can be claimed. The practical

guidance in this regard is that Farrier is not registered for GST and it cannot be considered as

the creditable acquisition.

Answer to question 5:

Goods and

services tax (GST)

for the above mentioned QUARTER

expenditure incurred on entertainment. As held in the case of “Bow and others v. Heatly

(1960) STL 311” stated that entertainment expenditure incurred on meal would be

considered as non-allowable deduction. Therefore, the meal expenditure would constitute as

fringe benefit under the “Fringe Benefit Tax Assessment Act 1986” and would be subjected

to Fringe Benefit Tax (Woellner et al. 2016). Additionally, “Division 9A under Part III of

the FBTAA” provides an employer that provides meal entertainment to the associates to

consider the value of the benefit by using either of the two methods. Therefore, in respect of

the “Section 8-1 of the ITAA 1997” Jimmy can claim an allowable deduction for the

expenses incurred and the GST amount would be payable in respect of the GSTR 1999.

Answer to question 4:

According to the Australian taxation office a person can GST credits given that the

business is registered to claim GST credits. As a result, Jimmy can claim a GST credits

however he would be required to obtain a GST registration. Since Jimmy has obtained the

registration, he can claim GST credits for the amount of GST that is included in the price he

pays for the things that is used in his business. However, it is found that Farrier is not

registered for GST and Jimmy would not be allowed for claiming GST credits since the

Farrier is not registered for GST.

There are large number of factors that ascertains whether an acquisition would be

considered as creditable purpose and for which input tax credit can be claimed. The practical

guidance in this regard is that Farrier is not registered for GST and it cannot be considered as

the creditable acquisition.

Answer to question 5:

Goods and

services tax (GST)

for the above mentioned QUARTER

6TAXATION LAW

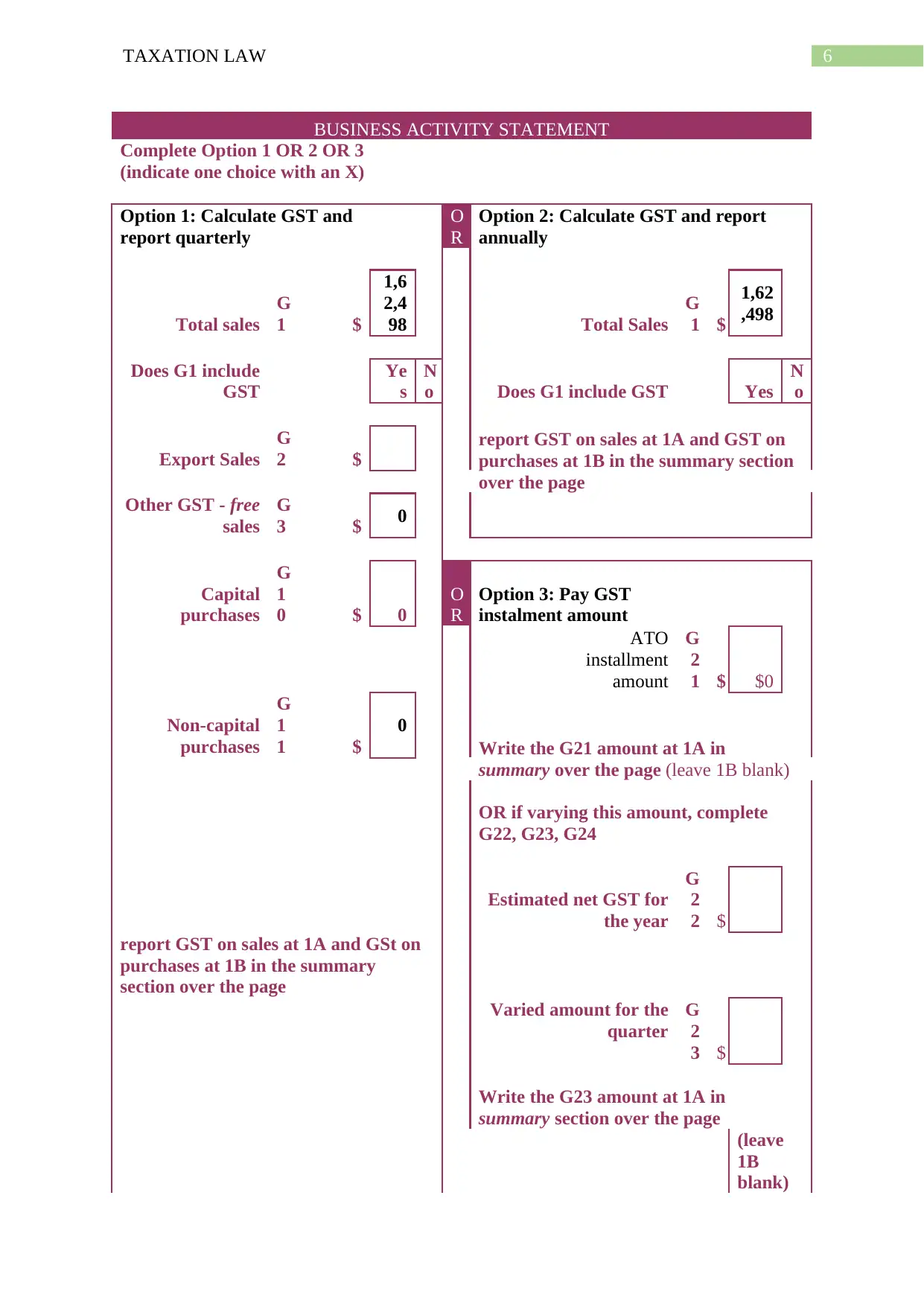

BUSINESS ACTIVITY STATEMENT

Complete Option 1 OR 2 OR 3

(indicate one choice with an X)

Option 1: Calculate GST and

report quarterly

O

R

Option 2: Calculate GST and report

annually

Total sales

G

1 $

1,6

2,4

98 Total Sales

G

1 $

1,62

,498

Does G1 include

GST

Ye

s

N

o

O

R Does G1 include GST Yes

N

o

Export Sales

G

2 $

O

R

report GST on sales at 1A and GST on

purchases at 1B in the summary section

over the page

Other GST - free

sales

G

3 $ 0 O

R

Capital

purchases

G

1

0 $ 0

O

R

Option 3: Pay GST

instalment amount

ATO

installment

amount

G

2

1 $ $0

Non-capital

purchases

G

1

1 $

0 O

R Write the G21 amount at 1A in

summary over the page (leave 1B blank)

OR if varying this amount, complete

G22, G23, G24

Estimated net GST for

the year

G

2

2 $

report GST on sales at 1A and GSt on

purchases at 1B in the summary

section over the page

Varied amount for the

quarter

G

2

3 $

Write the G23 amount at 1A in

summary section over the page

(leave

1B

blank)

BUSINESS ACTIVITY STATEMENT

Complete Option 1 OR 2 OR 3

(indicate one choice with an X)

Option 1: Calculate GST and

report quarterly

O

R

Option 2: Calculate GST and report

annually

Total sales

G

1 $

1,6

2,4

98 Total Sales

G

1 $

1,62

,498

Does G1 include

GST

Ye

s

N

o

O

R Does G1 include GST Yes

N

o

Export Sales

G

2 $

O

R

report GST on sales at 1A and GST on

purchases at 1B in the summary section

over the page

Other GST - free

sales

G

3 $ 0 O

R

Capital

purchases

G

1

0 $ 0

O

R

Option 3: Pay GST

instalment amount

ATO

installment

amount

G

2

1 $ $0

Non-capital

purchases

G

1

1 $

0 O

R Write the G21 amount at 1A in

summary over the page (leave 1B blank)

OR if varying this amount, complete

G22, G23, G24

Estimated net GST for

the year

G

2

2 $

report GST on sales at 1A and GSt on

purchases at 1B in the summary

section over the page

Varied amount for the

quarter

G

2

3 $

Write the G23 amount at 1A in

summary section over the page

(leave

1B

blank)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

Reason code for

variation

G

2

4 $

PAYG Tax withheld PAYG income tax installment

Total Salary,

wages and other

payments

W

1

$

2,6

26

Complete Option 1 OR

2

Amount withheld

from payments

shown at W1

W

2

$ 484

Option 1: Pay a PAYG

instalment amount

ATO Instalment amount T

7

$ 167

90

Amount withheld

where no ABN is

quoted

W

4

$

Write the T7 amount at 5A in summary

section below OR if varying this amount,

complete T8,T9,T4

Other amounts

withheld

W

3

$ Estimated tax for year T

8

$

Total amounts

witheld

(W2+W4+W3)

W

5

$ 484

Varied amount for the

quarter

T

9

$

Write the W5 amount in the Summary

section below

Write the T9 amount at 5A in the

Summary section below

Reason code for

variation

T

4

OR

Option 2: Calculate PAYG instalment

using income x rate

PAYG instalment

income

T

1

$ 1,47

,725

Commissioner's rate T

2

0.00

%

%

OR

New varied rate T

3

%

T1 x T2 (or T3)

T

1

1 $ 0

Reason for code

variation

T

4

Reason code for

variation

G

2

4 $

PAYG Tax withheld PAYG income tax installment

Total Salary,

wages and other

payments

W

1

$

2,6

26

Complete Option 1 OR

2

Amount withheld

from payments

shown at W1

W

2

$ 484

Option 1: Pay a PAYG

instalment amount

ATO Instalment amount T

7

$ 167

90

Amount withheld

where no ABN is

quoted

W

4

$

Write the T7 amount at 5A in summary

section below OR if varying this amount,

complete T8,T9,T4

Other amounts

withheld

W

3

$ Estimated tax for year T

8

$

Total amounts

witheld

(W2+W4+W3)

W

5

$ 484

Varied amount for the

quarter

T

9

$

Write the W5 amount in the Summary

section below

Write the T9 amount at 5A in the

Summary section below

Reason code for

variation

T

4

OR

Option 2: Calculate PAYG instalment

using income x rate

PAYG instalment

income

T

1

$ 1,47

,725

Commissioner's rate T

2

0.00

%

%

OR

New varied rate T

3

%

T1 x T2 (or T3)

T

1

1 $ 0

Reason for code

variation

T

4

8TAXATION LAW

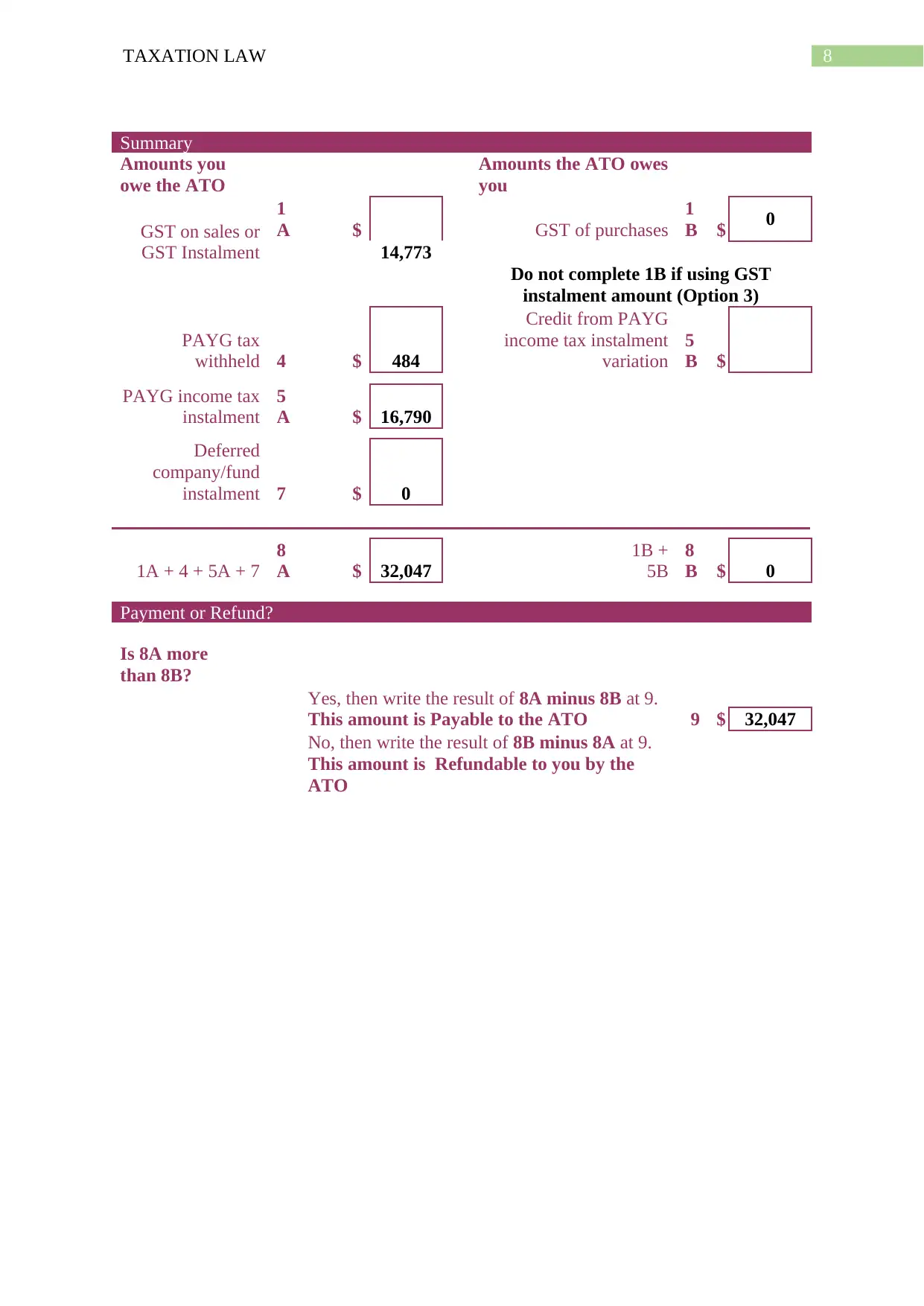

Summary

Amounts you

owe the ATO

Amounts the ATO owes

you

GST on sales or

GST Instalment

1

A $

14,773

GST of purchases

1

B $ 0

Do not complete 1B if using GST

instalment amount (Option 3)

PAYG tax

withheld 4 $ 484

Credit from PAYG

income tax instalment

variation

5

B $

PAYG income tax

instalment

5

A $ 16,790

Deferred

company/fund

instalment 7 $ 0

1A + 4 + 5A + 7

8

A $ 32,047

1B +

5B

8

B $ 0

Payment or Refund?

Is 8A more

than 8B?

Yes, then write the result of 8A minus 8B at 9.

This amount is Payable to the ATO 9 $ 32,047

No, then write the result of 8B minus 8A at 9.

This amount is Refundable to you by the

ATO

Summary

Amounts you

owe the ATO

Amounts the ATO owes

you

GST on sales or

GST Instalment

1

A $

14,773

GST of purchases

1

B $ 0

Do not complete 1B if using GST

instalment amount (Option 3)

PAYG tax

withheld 4 $ 484

Credit from PAYG

income tax instalment

variation

5

B $

PAYG income tax

instalment

5

A $ 16,790

Deferred

company/fund

instalment 7 $ 0

1A + 4 + 5A + 7

8

A $ 32,047

1B +

5B

8

B $ 0

Payment or Refund?

Is 8A more

than 8B?

Yes, then write the result of 8A minus 8B at 9.

This amount is Payable to the ATO 9 $ 32,047

No, then write the result of 8B minus 8A at 9.

This amount is Refundable to you by the

ATO

9TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

Reference List:

Barkoczy, S., 2016. Foundations of Taxation Law 2016. OUP Catalogue.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian

Taxation Law Select: Legislation and Commentary 2016. Oxford University Press.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.