Taxation Law Australia Question Answer 2022

VerifiedAdded on 2022/10/11

|11

|3022

|13

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation Law Australia

Case Study on Capital Gains Tax and Capital Allowance

Student’s Name:

ID:

Module:

Instructor:

Case Study on Capital Gains Tax and Capital Allowance

Student’s Name:

ID:

Module:

Instructor:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Answer to the question no- 1

Capital Gains Tax Consequences on Sale of Assets by Jasmine

After assessing the case of Jasmin, it is firstly required for Jasmin to understand the Australian

taxation rules and regulations. It is divulged to her that the Australian taxation system requires

the Jasmin to include the capital gain in the income tax return as part of income tax liability. This

increases the total income tax payable by her, at times to a substantial level. Hence it is necessary

for her to compute the CGT at an early stage to arrange for fund to pay the tax as Australian

taxation system does not have any provision of withholding CGT.

It is advised that tax payable by her on the capital gain in the taxation system on the assets which

she purchased on or after 20 September, 1985. Any asset acquired after that date is subject to

CGT excepting some exclusions and exemptions. Australian taxation system does not require

payment of tax on gains on sale of assets in a separate heading, rather the same is assessed

separately but clubbed with the normal income of the assess to arrive at the taxable income and

payable at the applicable income tax rate. When an asset is held for at least 12 months prior to its

sale, it is considered as long term asset and the assessee is allowed a 50% discount on the gain on

sale of the asset for the purpose of calculating CGT liability. For superannuation fund the

discount is 33% (Australian Taxation Office, 2019).

Set off and Carry forward of Loss

As per the Australian taxation system set off and carry forward rules, any loss arising from sale

of asset can be set off against gain from sale of other assets, provided such loss has not occurred

due to sale of any exempt asset, and can be carried forward for indefinite period, but such loss

cannot be set off against any other normal income of the assessee.

Capital Gains Tax (CGT) Event

A CGT event is deemed to have taken place when any or all of the following events take place:

i) The assesse sells or gives away any asset (Australian Government, 2019):

Capital Gains Tax Consequences on Sale of Assets by Jasmine

After assessing the case of Jasmin, it is firstly required for Jasmin to understand the Australian

taxation rules and regulations. It is divulged to her that the Australian taxation system requires

the Jasmin to include the capital gain in the income tax return as part of income tax liability. This

increases the total income tax payable by her, at times to a substantial level. Hence it is necessary

for her to compute the CGT at an early stage to arrange for fund to pay the tax as Australian

taxation system does not have any provision of withholding CGT.

It is advised that tax payable by her on the capital gain in the taxation system on the assets which

she purchased on or after 20 September, 1985. Any asset acquired after that date is subject to

CGT excepting some exclusions and exemptions. Australian taxation system does not require

payment of tax on gains on sale of assets in a separate heading, rather the same is assessed

separately but clubbed with the normal income of the assess to arrive at the taxable income and

payable at the applicable income tax rate. When an asset is held for at least 12 months prior to its

sale, it is considered as long term asset and the assessee is allowed a 50% discount on the gain on

sale of the asset for the purpose of calculating CGT liability. For superannuation fund the

discount is 33% (Australian Taxation Office, 2019).

Set off and Carry forward of Loss

As per the Australian taxation system set off and carry forward rules, any loss arising from sale

of asset can be set off against gain from sale of other assets, provided such loss has not occurred

due to sale of any exempt asset, and can be carried forward for indefinite period, but such loss

cannot be set off against any other normal income of the assessee.

Capital Gains Tax (CGT) Event

A CGT event is deemed to have taken place when any or all of the following events take place:

i) The assesse sells or gives away any asset (Australian Government, 2019):

ii) She could redeems, cancels, or surrenders shares of a company (Australian Government,

2019).

iii) Any asset is lost or destroyed (Australian Government, 2019).

iv)The assesse ceases to be an Australian resident and leaves the country (Australian

Government, 2019).

v) Any payment from a company, other than dividend payment, is received by the assessee

Capital Gains Tax (CGT) Assets

It is advised to her that in Australia all assets are subject to CGT if acquired after 20th September

1985, unless specifically excluded from domain of CGT or exempted on the basis of their cost of

acquisition. A list of CGT assets is given below:

i) Real estate: All assets in the real estate category including vacant land, holiday homes, and

hobby farms.

ii) Shares and Units: Shares and units of unit trusts if those are acquired after 20 September,

1985 are subject to CGT. However when company shares are sold as stock in trade, the same is

not a CGT asset. Gains from sale of shares as business activity is considered as ordinary income

of the assessee and assessable for income tax purpose.

iii) Intangible Assets: Intangible assets like goodwill, license, patent, etc. if those were active

assets prior to sale gives rise to CGT.

vi Collectables: Collectable are those assets which are kept by the assessee for personal

enjoyment or for the enjoyment of associates of the assessee. Collectables for CGT purpose,

according to Section 108 of the Capital Gains Tax 1985 are paintings, drawings, engraves, old

postage stamps, jewellery, rare manuscripts, books, folios, and photographs (Australian Taxation

Office, 2019).

Assets Exempted from CGT

2019).

iii) Any asset is lost or destroyed (Australian Government, 2019).

iv)The assesse ceases to be an Australian resident and leaves the country (Australian

Government, 2019).

v) Any payment from a company, other than dividend payment, is received by the assessee

Capital Gains Tax (CGT) Assets

It is advised to her that in Australia all assets are subject to CGT if acquired after 20th September

1985, unless specifically excluded from domain of CGT or exempted on the basis of their cost of

acquisition. A list of CGT assets is given below:

i) Real estate: All assets in the real estate category including vacant land, holiday homes, and

hobby farms.

ii) Shares and Units: Shares and units of unit trusts if those are acquired after 20 September,

1985 are subject to CGT. However when company shares are sold as stock in trade, the same is

not a CGT asset. Gains from sale of shares as business activity is considered as ordinary income

of the assessee and assessable for income tax purpose.

iii) Intangible Assets: Intangible assets like goodwill, license, patent, etc. if those were active

assets prior to sale gives rise to CGT.

vi Collectables: Collectable are those assets which are kept by the assessee for personal

enjoyment or for the enjoyment of associates of the assessee. Collectables for CGT purpose,

according to Section 108 of the Capital Gains Tax 1985 are paintings, drawings, engraves, old

postage stamps, jewellery, rare manuscripts, books, folios, and photographs (Australian Taxation

Office, 2019).

Assets Exempted from CGT

It is divulged to her that the Australian Taxation Office provides for exemption for certain assets

from CGT on her capital gain. The gains from such assets are not taxable, nor is any loss arising

out of sale of such assets available for setting off capital gains. Such assets are listed below:

i) Pre-CGT Assets: All assets acquired by the assessee before 20 September 1985 are excluded

from computation of CGT (Australian Taxation office, 2019).

i) Main Home of the Assessee: Main home of Jasmin is exempt, even purchased after September

1985, from being subjected to CGT if that is used by the assessee or her family for living, if the

personal belongings of the assessee are kept in the house, if the home is the official mailing

address of the assessee, and if the home has gas and electricity connections. However, if the

assessee was not a resident of Australia while living in the house, no exemption from CGT

liability can be claimed in respect of such house.

ii) Depreciating assets: Any depreciating asset used by the assessee in business solely for taxable

purpose is exempt from CGT. Equipments of business or items kept in property used for rental

purpose are examples of such assets. Gain from sale of any other asset outside of depreciation

pool is taxable as CGT and any loss from such sale can be used for offsetting capital gains.

iii) Personal Use Assets: Personal use assets acquired by the assessee for less than $10,000 or

were such valued when the assessee acquired them are exempt from CGT. Any loss arising out

of sale of such assets is also not available for offsetting capital gains from other assets.

However, Taxation Ruling TR 2004/18 provides certain exceptions to such exemptions. Shares

in private companies or shares in private trust acquired before 20 September, 1985 are subject to

CGT if combination of certain factors give rise CGT event.

iv) Cars and Motor Cycles: According to Sub Section 995 – 1(1) of the Income Tax Assessment

Act 1997, for the purpose of taxation, a car is defined as a vehicle capable of carrying less than 9

passengers and 1 tonne. Any gains from sale of such assets are not to be included for the purpose

of computation of CGT as per Section 118 – 5 of the Income Tax Assessment Act 1997.

However, a car is subject to CGT if it is an antique car. Section 108 – 10(2) deems an item to be

antique if it is at least 100 years old (Australian Taxation Office, 2019).

Resident for Tax Purpose

from CGT on her capital gain. The gains from such assets are not taxable, nor is any loss arising

out of sale of such assets available for setting off capital gains. Such assets are listed below:

i) Pre-CGT Assets: All assets acquired by the assessee before 20 September 1985 are excluded

from computation of CGT (Australian Taxation office, 2019).

i) Main Home of the Assessee: Main home of Jasmin is exempt, even purchased after September

1985, from being subjected to CGT if that is used by the assessee or her family for living, if the

personal belongings of the assessee are kept in the house, if the home is the official mailing

address of the assessee, and if the home has gas and electricity connections. However, if the

assessee was not a resident of Australia while living in the house, no exemption from CGT

liability can be claimed in respect of such house.

ii) Depreciating assets: Any depreciating asset used by the assessee in business solely for taxable

purpose is exempt from CGT. Equipments of business or items kept in property used for rental

purpose are examples of such assets. Gain from sale of any other asset outside of depreciation

pool is taxable as CGT and any loss from such sale can be used for offsetting capital gains.

iii) Personal Use Assets: Personal use assets acquired by the assessee for less than $10,000 or

were such valued when the assessee acquired them are exempt from CGT. Any loss arising out

of sale of such assets is also not available for offsetting capital gains from other assets.

However, Taxation Ruling TR 2004/18 provides certain exceptions to such exemptions. Shares

in private companies or shares in private trust acquired before 20 September, 1985 are subject to

CGT if combination of certain factors give rise CGT event.

iv) Cars and Motor Cycles: According to Sub Section 995 – 1(1) of the Income Tax Assessment

Act 1997, for the purpose of taxation, a car is defined as a vehicle capable of carrying less than 9

passengers and 1 tonne. Any gains from sale of such assets are not to be included for the purpose

of computation of CGT as per Section 118 – 5 of the Income Tax Assessment Act 1997.

However, a car is subject to CGT if it is an antique car. Section 108 – 10(2) deems an item to be

antique if it is at least 100 years old (Australian Taxation Office, 2019).

Resident for Tax Purpose

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Residential status of an assessee has important bearing on the treatment of the assessee for tax

purpose. Border Protection and Department of immigration use different standards for the

determination of the residential status of the assessee. By such standards, the Australian Taxation

Office ensures that all the residents of Australia pay income tax as per the set standards

irrespective of where one stays.

Australian Taxation Office (ATO) sets the following criteria for deciding upon residential status

for the purpose of payment of tax. The objective is all residents must pay tax.

i) She has always resided in Australia.

ii) She has come into Australia from a foreign country to live in and does not want to leave

Australia in near future.

iii) The person resided in Australia for at least half of the income year, unless s/he has a home

abroad and has no intention to reside in Australia (Deb, 2018).

iv)The person has come to Australia to study an academic course which is at least 6 months long.

CGT Consequences of Sale of Assets by Jasmine

i) Sale of home for $650,000, acquired for $40,000: Jasmine has made a gain from the sale. But

the gain is not subject to CGT as the home was purchased in 1981 that is prior to CGT

implementation in Australia, the home is Jasmine’s main home, and also Jasmine was An

Australian resident during the time of her stay in the home. Hence the gain is exempted for CGT

purpose (Devereux, & Maffini, 2007).

ii) Sale of car for $10,000, acquired for $31,000: This resulted in capital loss. The car was

purchased in 2011, and typically it is not an antique car as per Section 108 – 10(2) of the Capital

Gains Tax Act 1985. It is exempt from CGT and cannot be used to offset other capital gains, nor

can it be carried forward (Evans, Minas, & Lim, 2015).

iii) Sale of business equipment for $65,000, acquired for $75,000: This resulted in capital loss.

It is disregarded for the purpose of CGT as the asset was solely used for taxable purpose and it

purpose. Border Protection and Department of immigration use different standards for the

determination of the residential status of the assessee. By such standards, the Australian Taxation

Office ensures that all the residents of Australia pay income tax as per the set standards

irrespective of where one stays.

Australian Taxation Office (ATO) sets the following criteria for deciding upon residential status

for the purpose of payment of tax. The objective is all residents must pay tax.

i) She has always resided in Australia.

ii) She has come into Australia from a foreign country to live in and does not want to leave

Australia in near future.

iii) The person resided in Australia for at least half of the income year, unless s/he has a home

abroad and has no intention to reside in Australia (Deb, 2018).

iv)The person has come to Australia to study an academic course which is at least 6 months long.

CGT Consequences of Sale of Assets by Jasmine

i) Sale of home for $650,000, acquired for $40,000: Jasmine has made a gain from the sale. But

the gain is not subject to CGT as the home was purchased in 1981 that is prior to CGT

implementation in Australia, the home is Jasmine’s main home, and also Jasmine was An

Australian resident during the time of her stay in the home. Hence the gain is exempted for CGT

purpose (Devereux, & Maffini, 2007).

ii) Sale of car for $10,000, acquired for $31,000: This resulted in capital loss. The car was

purchased in 2011, and typically it is not an antique car as per Section 108 – 10(2) of the Capital

Gains Tax Act 1985. It is exempt from CGT and cannot be used to offset other capital gains, nor

can it be carried forward (Evans, Minas, & Lim, 2015).

iii) Sale of business equipment for $65,000, acquired for $75,000: This resulted in capital loss.

It is disregarded for the purpose of CGT as the asset was solely used for taxable purpose and it

was active asset prior to sale. The loss cannot be used to offset capital gains neither can it be

carried forward (Feld,., Heckemeyer, & Overesch, 2013).

iv) Sale of goodwill for $65,000: The value of the goodwill cannot be ascertained as it is

internally generated by Jasmine. Moreover the intangible asset was active prior to sale. Hence no

CGT liability arises (Harris, T. S., Hubbard, & Kemsley, 2011).

v) Sale of furniture as set for $5,000, acquired each item for less than $2,000: It is a personal

use asset. The asset is being sold in a set at $10,000, and no single item in the set was acquired

for $10,000 or more. Hence no CGT liability arises (James, 2018).

vi) Sale of second hand paintings for $35,000, each acquired for less than $500: Paintings are

collectable as per ATO for CGT purpose. But here no CGT liability arises as no single painting

was acquired at more than $500 (Niemirowski., Baldwin, & Wearing, 2013).

vii) Sale of painting for $5,000, acquired direct from artist for $1,000: This is collectable,

hence CGT liability arises. No exemption is available as the painting was acquired for more than

$500. The taxable amount is $4,000.

carried forward (Feld,., Heckemeyer, & Overesch, 2013).

iv) Sale of goodwill for $65,000: The value of the goodwill cannot be ascertained as it is

internally generated by Jasmine. Moreover the intangible asset was active prior to sale. Hence no

CGT liability arises (Harris, T. S., Hubbard, & Kemsley, 2011).

v) Sale of furniture as set for $5,000, acquired each item for less than $2,000: It is a personal

use asset. The asset is being sold in a set at $10,000, and no single item in the set was acquired

for $10,000 or more. Hence no CGT liability arises (James, 2018).

vi) Sale of second hand paintings for $35,000, each acquired for less than $500: Paintings are

collectable as per ATO for CGT purpose. But here no CGT liability arises as no single painting

was acquired at more than $500 (Niemirowski., Baldwin, & Wearing, 2013).

vii) Sale of painting for $5,000, acquired direct from artist for $1,000: This is collectable,

hence CGT liability arises. No exemption is available as the painting was acquired for more than

$500. The taxable amount is $4,000.

Answer to the question no- 2

Capital Allowance for CNC Machine Acquired by John

Capital Allowance: It is analyzed that capital allowance is relief allowed to companies for

capital expenditure by allowing it to be expensed over a specified number of years in the

earnings before tax of the company. It is available for specified types of capital expenditures and

for a given period of time.( O'Connor, & Strauch, 2018). For certain types of investment a tax

deduction is available due to decline in the value of the assets (Capital Claims, 2019). Capital

allowance, also called tax depreciation is allowed as the entire cost of the asset cannot be

deducted in the income statement of a single year. As in the case law of PS LA 2009/9 Conduct of

Tax Office Litigation. Capital allowance is applicable to such capital expenditure for which annual

investment allowance (AIA) is not allowed * Wild, D. (2018). The basic difference between

depreciation and capital allowance is that depreciation is not a deductible expenditure and must

be added back to net earnings for the purpose of tax, but capital allowance is tax deductible.

Capital allowance can be claimed for a period up to 40 years (Australian Taxation Office, 2019).

Capital allowance has been introduced in the Australian corporate taxation by the Uniform

Capital Allowance (UCA) Rule on 1 July, 2001 for all types of depreciating assets (Australian

Taxation Office, 2019). The UCA has provided a set of general rules for determining the cost of

the asset for capital allowance due to decline in value of depreciating assets (Australian Taxation

Office, 2019). Deduction in respect of certain assets which was not available before can be

claimed in the new rule (Australian Taxation Office, 2019).

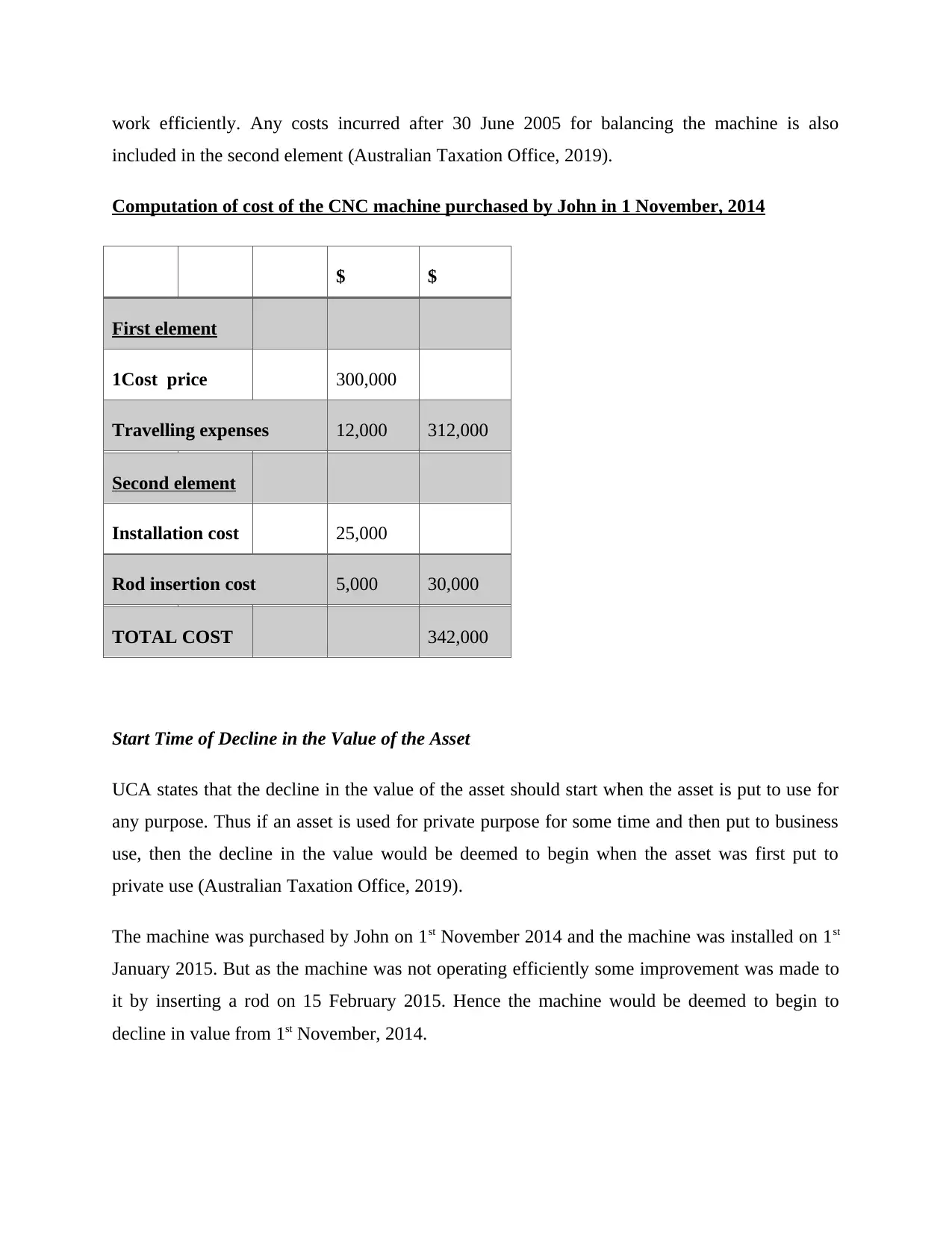

Cost of the CNC Machine for the Purpose of Capital Allowance

For determination of the amount of capital allowance, the cost of the asset has to be determined

in accordance with rules prescribed in the UCA. For the purpose of capital allowance

computation, two types of costs are to be considered. The first is called first element in which all

the cots directly involved for acquiring the asset are to be included. These costs are the purchase

price of the asset and any other expense directly involved for holding the asset like travelling

expenses. The second element includes such costs as are incurred for bringing the asset in to

present usable condition like installation expenses and improvement expenses to make the asset

Capital Allowance for CNC Machine Acquired by John

Capital Allowance: It is analyzed that capital allowance is relief allowed to companies for

capital expenditure by allowing it to be expensed over a specified number of years in the

earnings before tax of the company. It is available for specified types of capital expenditures and

for a given period of time.( O'Connor, & Strauch, 2018). For certain types of investment a tax

deduction is available due to decline in the value of the assets (Capital Claims, 2019). Capital

allowance, also called tax depreciation is allowed as the entire cost of the asset cannot be

deducted in the income statement of a single year. As in the case law of PS LA 2009/9 Conduct of

Tax Office Litigation. Capital allowance is applicable to such capital expenditure for which annual

investment allowance (AIA) is not allowed * Wild, D. (2018). The basic difference between

depreciation and capital allowance is that depreciation is not a deductible expenditure and must

be added back to net earnings for the purpose of tax, but capital allowance is tax deductible.

Capital allowance can be claimed for a period up to 40 years (Australian Taxation Office, 2019).

Capital allowance has been introduced in the Australian corporate taxation by the Uniform

Capital Allowance (UCA) Rule on 1 July, 2001 for all types of depreciating assets (Australian

Taxation Office, 2019). The UCA has provided a set of general rules for determining the cost of

the asset for capital allowance due to decline in value of depreciating assets (Australian Taxation

Office, 2019). Deduction in respect of certain assets which was not available before can be

claimed in the new rule (Australian Taxation Office, 2019).

Cost of the CNC Machine for the Purpose of Capital Allowance

For determination of the amount of capital allowance, the cost of the asset has to be determined

in accordance with rules prescribed in the UCA. For the purpose of capital allowance

computation, two types of costs are to be considered. The first is called first element in which all

the cots directly involved for acquiring the asset are to be included. These costs are the purchase

price of the asset and any other expense directly involved for holding the asset like travelling

expenses. The second element includes such costs as are incurred for bringing the asset in to

present usable condition like installation expenses and improvement expenses to make the asset

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

work efficiently. Any costs incurred after 30 June 2005 for balancing the machine is also

included in the second element (Australian Taxation Office, 2019).

Computation of cost of the CNC machine purchased by John in 1 November, 2014

$ $

First element

1Cost price 300,000

Travelling expenses 12,000 312,000

Second element

Installation cost 25,000

Rod insertion cost 5,000 30,000

TOTAL COST 342,000

Start Time of Decline in the Value of the Asset

UCA states that the decline in the value of the asset should start when the asset is put to use for

any purpose. Thus if an asset is used for private purpose for some time and then put to business

use, then the decline in the value would be deemed to begin when the asset was first put to

private use (Australian Taxation Office, 2019).

The machine was purchased by John on 1st November 2014 and the machine was installed on 1st

January 2015. But as the machine was not operating efficiently some improvement was made to

it by inserting a rod on 15 February 2015. Hence the machine would be deemed to begin to

decline in value from 1st November, 2014.

included in the second element (Australian Taxation Office, 2019).

Computation of cost of the CNC machine purchased by John in 1 November, 2014

$ $

First element

1Cost price 300,000

Travelling expenses 12,000 312,000

Second element

Installation cost 25,000

Rod insertion cost 5,000 30,000

TOTAL COST 342,000

Start Time of Decline in the Value of the Asset

UCA states that the decline in the value of the asset should start when the asset is put to use for

any purpose. Thus if an asset is used for private purpose for some time and then put to business

use, then the decline in the value would be deemed to begin when the asset was first put to

private use (Australian Taxation Office, 2019).

The machine was purchased by John on 1st November 2014 and the machine was installed on 1st

January 2015. But as the machine was not operating efficiently some improvement was made to

it by inserting a rod on 15 February 2015. Hence the machine would be deemed to begin to

decline in value from 1st November, 2014.

References

Deb, R. (2018). Tax Reforms and GST: A Systematic Literature Review. Journal of Commerce

and Accounting Research, 7(1), 40.

Devereux, M., & Maffini, G. (2007). The Impact of Taxation on the Location of Captial, Firms

and Profit: a Survey of Empirical Evidence.

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F., 30, 735.

Feld, L. P., Heckemeyer, J. H., & Overesch, M. (2013). Capital structure choice and company

taxation: A meta-study. Journal of Banking & Finance, 37(8), 2850-2866.

Harris, T. S., Hubbard, R. G., & Kemsley, D. (2011). The share price effects of dividend taxes and tax

imputation credits. Journal of Public Economics, 79(3), 569-596.

James, K. (2018). Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Niemirowski, P., Baldwin, S., & Wearing, A. J. (2013). Tax related behaviours, beliefs, attitudes and

values and taxpayer compliance in Australia. J. Austl. Tax'n, 6, 132.

O'Connor, A., & Strauch, M. (2018). New GST payment obligations for residential property

transactions. Taxation in Australia, 52(9), 507.

Wild, D. (2018). Time for a tax revolution. Institute of Public Affairs Review: A Quarterly

Review of Politics and Public Affairs, The, 70(1), 28.

Australian Government (2019). Capital Gains Tax (CGT). [online] Retrieved from

https://www.business.gov.au/finance/taxation/capital-gains-tax on 21 September 2019

Australian Taxation Office (2019). CGT assets and exemptions. [online] Retrieved from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Exemptions1 on 21 September 2019

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-

allowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline in

value of depreciating assets. [online] Retrieved from

Deb, R. (2018). Tax Reforms and GST: A Systematic Literature Review. Journal of Commerce

and Accounting Research, 7(1), 40.

Devereux, M., & Maffini, G. (2007). The Impact of Taxation on the Location of Captial, Firms

and Profit: a Survey of Empirical Evidence.

Evans, C., Minas, J., & Lim, Y. (2015). Taxing personal capital gains in Australia: An alternative

way forward. Austl. Tax F., 30, 735.

Feld, L. P., Heckemeyer, J. H., & Overesch, M. (2013). Capital structure choice and company

taxation: A meta-study. Journal of Banking & Finance, 37(8), 2850-2866.

Harris, T. S., Hubbard, R. G., & Kemsley, D. (2011). The share price effects of dividend taxes and tax

imputation credits. Journal of Public Economics, 79(3), 569-596.

James, K. (2018). Applying the GST to imports of low-value goods in Australia. Applying the

GST to imports of low value goods in Australia,(2018), 47.

Niemirowski, P., Baldwin, S., & Wearing, A. J. (2013). Tax related behaviours, beliefs, attitudes and

values and taxpayer compliance in Australia. J. Austl. Tax'n, 6, 132.

O'Connor, A., & Strauch, M. (2018). New GST payment obligations for residential property

transactions. Taxation in Australia, 52(9), 507.

Wild, D. (2018). Time for a tax revolution. Institute of Public Affairs Review: A Quarterly

Review of Politics and Public Affairs, The, 70(1), 28.

Australian Government (2019). Capital Gains Tax (CGT). [online] Retrieved from

https://www.business.gov.au/finance/taxation/capital-gains-tax on 21 September 2019

Australian Taxation Office (2019). CGT assets and exemptions. [online] Retrieved from

https://www.ato.gov.au/general/capital-gains-tax/cgt-assets-and-exemptions/

#Exemptions1 on 21 September 2019

Australian Taxation Office (2019). Other capital assets and expense deductions. [online]

retrieved from https://www.ato.gov.au/business/depreciation-and-capital-expenses-and-

allowances/other-capital-asset-and-expense-deductions/ on 21 September 2019

Australian Taxation Office (2019). Uniform capital allowance system: calculating the decline in

value of depreciating assets. [online] Retrieved from

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

https://www.ato.gov.au/Business/Depreciation-and-capital-expenses-and-allowances/In-

detail/Depreciating-assets/Uniform-capital-allowance-system--calculating-the-decline-in-

value-of-a-depreciating-asset/ on 21 September 2019

detail/Depreciating-assets/Uniform-capital-allowance-system--calculating-the-decline-in-

value-of-a-depreciating-asset/ on 21 September 2019

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.