Taxation Law: Calculation of Taxable Profit and Tax Liability for Bloomingdale Florists Pty Ltd

VerifiedAdded on 2023/06/04

|12

|2510

|458

AI Summary

This article provides a detailed calculation of taxable profit and tax liability for Bloomingdale Florists Pty Ltd for the year ended on June 30, 2018. It also discusses the tax implications of compensation received by Matchsticks Limited and profit from sale of land to Matchsticks Limited.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Taxation Law

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1

TAXATION LAW

Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................6

References:....................................................................................................................................11

TAXATION LAW

Contents

Answer to question 1:......................................................................................................................2

Answer to question 2:......................................................................................................................6

References:....................................................................................................................................11

2

TAXATION LAW

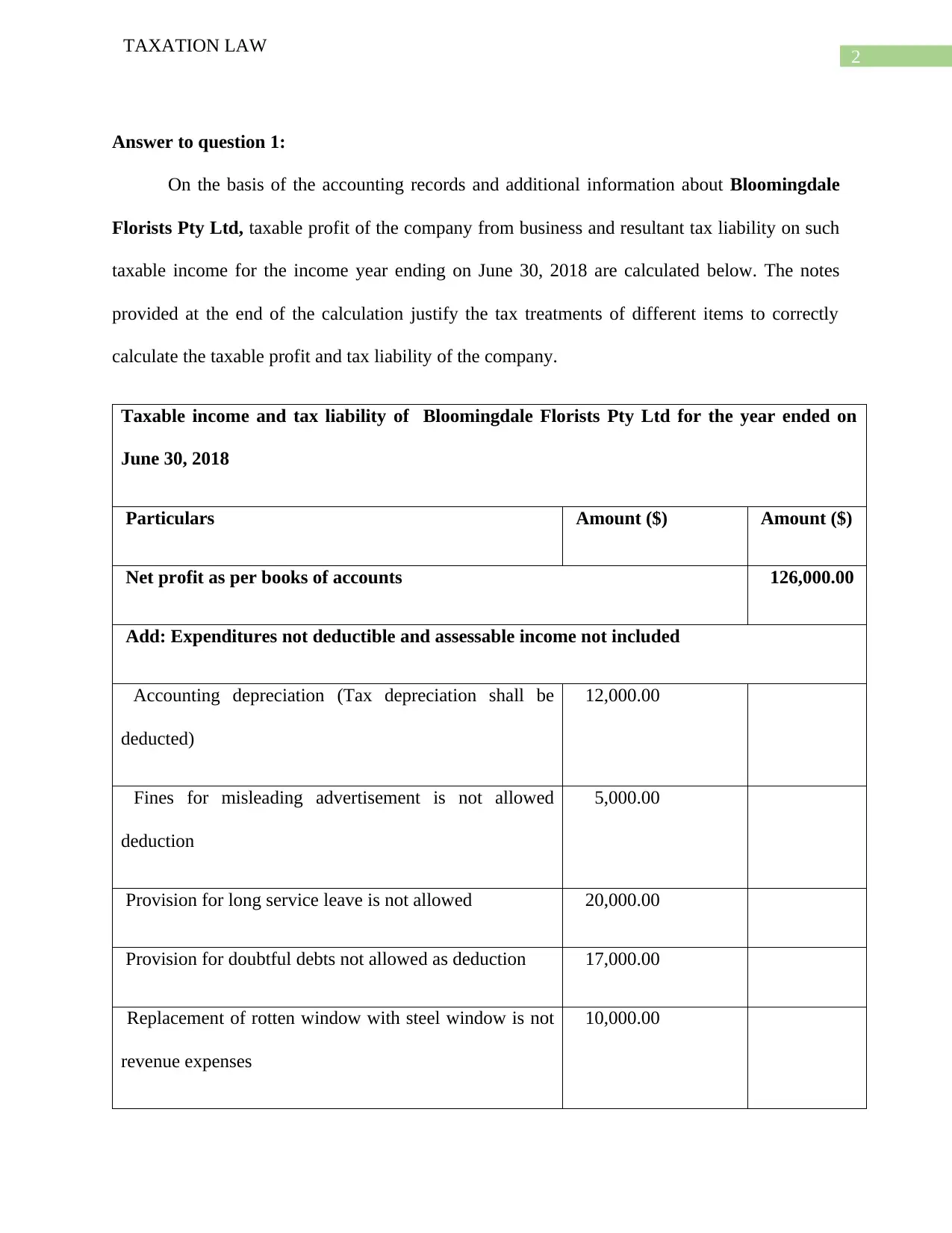

Answer to question 1:

On the basis of the accounting records and additional information about Bloomingdale

Florists Pty Ltd, taxable profit of the company from business and resultant tax liability on such

taxable income for the income year ending on June 30, 2018 are calculated below. The notes

provided at the end of the calculation justify the tax treatments of different items to correctly

calculate the taxable profit and tax liability of the company.

Taxable income and tax liability of Bloomingdale Florists Pty Ltd for the year ended on

June 30, 2018

Particulars Amount ($) Amount ($)

Net profit as per books of accounts 126,000.00

Add: Expenditures not deductible and assessable income not included

Accounting depreciation (Tax depreciation shall be

deducted)

12,000.00

Fines for misleading advertisement is not allowed

deduction

5,000.00

Provision for long service leave is not allowed 20,000.00

Provision for doubtful debts not allowed as deduction 17,000.00

Replacement of rotten window with steel window is not

revenue expenses

10,000.00

TAXATION LAW

Answer to question 1:

On the basis of the accounting records and additional information about Bloomingdale

Florists Pty Ltd, taxable profit of the company from business and resultant tax liability on such

taxable income for the income year ending on June 30, 2018 are calculated below. The notes

provided at the end of the calculation justify the tax treatments of different items to correctly

calculate the taxable profit and tax liability of the company.

Taxable income and tax liability of Bloomingdale Florists Pty Ltd for the year ended on

June 30, 2018

Particulars Amount ($) Amount ($)

Net profit as per books of accounts 126,000.00

Add: Expenditures not deductible and assessable income not included

Accounting depreciation (Tax depreciation shall be

deducted)

12,000.00

Fines for misleading advertisement is not allowed

deduction

5,000.00

Provision for long service leave is not allowed 20,000.00

Provision for doubtful debts not allowed as deduction 17,000.00

Replacement of rotten window with steel window is not

revenue expenses

10,000.00

3

TAXATION LAW

Painting expenses of Company premises is allowed as

deduction

-

Gifts to Paramatta Eels League club is not allowed as

deduction

10,000.00

Borrowing cost is not allowed as expenses as it is capital

cost

3,000.00

Dividend from foreign resident company is taxable

income

1,000.00

Unranked dividend from resident company is assessable

income (9000 x 20%)

1,800.00

Directors' salary in excess of reasonable limits (50000 -

40000)

10,000.00

89,800.00

215,800.00

Less: Expenditures not considered but allowed and income not assessable

Actual long service leave paid 10,000.00

Bad debt written off 15,000.00

Capital allowances allowed for tax purposes 10,000.00

TAXATION LAW

Painting expenses of Company premises is allowed as

deduction

-

Gifts to Paramatta Eels League club is not allowed as

deduction

10,000.00

Borrowing cost is not allowed as expenses as it is capital

cost

3,000.00

Dividend from foreign resident company is taxable

income

1,000.00

Unranked dividend from resident company is assessable

income (9000 x 20%)

1,800.00

Directors' salary in excess of reasonable limits (50000 -

40000)

10,000.00

89,800.00

215,800.00

Less: Expenditures not considered but allowed and income not assessable

Actual long service leave paid 10,000.00

Bad debt written off 15,000.00

Capital allowances allowed for tax purposes 10,000.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4

TAXATION LAW

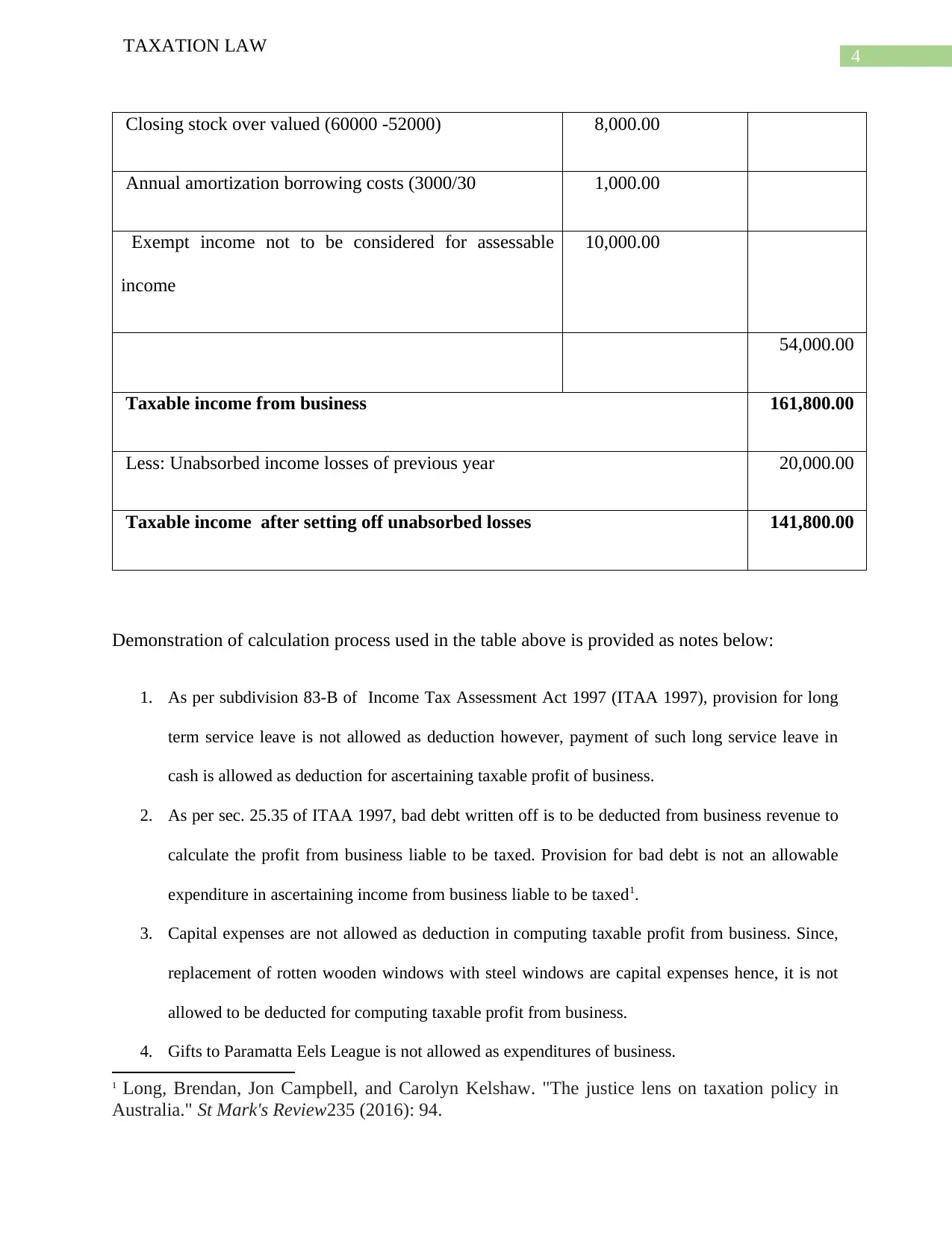

Closing stock over valued (60000 -52000) 8,000.00

Annual amortization borrowing costs (3000/30 1,000.00

Exempt income not to be considered for assessable

income

10,000.00

54,000.00

Taxable income from business 161,800.00

Less: Unabsorbed income losses of previous year 20,000.00

Taxable income after setting off unabsorbed losses 141,800.00

Demonstration of calculation process used in the table above is provided as notes below:

1. As per subdivision 83-B of Income Tax Assessment Act 1997 (ITAA 1997), provision for long

term service leave is not allowed as deduction however, payment of such long service leave in

cash is allowed as deduction for ascertaining taxable profit of business.

2. As per sec. 25.35 of ITAA 1997, bad debt written off is to be deducted from business revenue to

calculate the profit from business liable to be taxed. Provision for bad debt is not an allowable

expenditure in ascertaining income from business liable to be taxed1.

3. Capital expenses are not allowed as deduction in computing taxable profit from business. Since,

replacement of rotten wooden windows with steel windows are capital expenses hence, it is not

allowed to be deducted for computing taxable profit from business.

4. Gifts to Paramatta Eels League is not allowed as expenditures of business.

1 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

TAXATION LAW

Closing stock over valued (60000 -52000) 8,000.00

Annual amortization borrowing costs (3000/30 1,000.00

Exempt income not to be considered for assessable

income

10,000.00

54,000.00

Taxable income from business 161,800.00

Less: Unabsorbed income losses of previous year 20,000.00

Taxable income after setting off unabsorbed losses 141,800.00

Demonstration of calculation process used in the table above is provided as notes below:

1. As per subdivision 83-B of Income Tax Assessment Act 1997 (ITAA 1997), provision for long

term service leave is not allowed as deduction however, payment of such long service leave in

cash is allowed as deduction for ascertaining taxable profit of business.

2. As per sec. 25.35 of ITAA 1997, bad debt written off is to be deducted from business revenue to

calculate the profit from business liable to be taxed. Provision for bad debt is not an allowable

expenditure in ascertaining income from business liable to be taxed1.

3. Capital expenses are not allowed as deduction in computing taxable profit from business. Since,

replacement of rotten wooden windows with steel windows are capital expenses hence, it is not

allowed to be deducted for computing taxable profit from business.

4. Gifts to Paramatta Eels League is not allowed as expenditures of business.

1 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

5

TAXATION LAW

5. Capital allowances for tax purposes amounting to $10,000 is to be treated accordingly.

6. Since the closing stock was taken at $60,000 instead of $52,000 hence, cost of goods sold is

understated by $8,000. Hence, the same is to be added back to the accounting profit for taxable

purpose2.

7. Section 25.25 of ITAA 1997 provides that borrowing cost incurred at the time of borrowing is to

be spread over the period of loan. Thus, the entire borrowing cost is not allowed as expenditure in

computing taxable profit from business. Borrowing cost is to be spread over the loan period3.

8. Outstanding trade debts is assessable income until unless there is substantial doubt as to the final

recovery of such debt. Hence, the amount is correctly included in ascertaining taxable profit of

the business. Income from retail sales is assessable income and needs to be included in

calculation of assessable income. Since, it is already included in sales thus, there is no

requirement to make any adjustment to the accounting profit for calculation taxable profit of

business4.

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

3 n, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia." Economic

Modelling 44 (2015): 44-53.

4 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

TAXATION LAW

5. Capital allowances for tax purposes amounting to $10,000 is to be treated accordingly.

6. Since the closing stock was taken at $60,000 instead of $52,000 hence, cost of goods sold is

understated by $8,000. Hence, the same is to be added back to the accounting profit for taxable

purpose2.

7. Section 25.25 of ITAA 1997 provides that borrowing cost incurred at the time of borrowing is to

be spread over the period of loan. Thus, the entire borrowing cost is not allowed as expenditure in

computing taxable profit from business. Borrowing cost is to be spread over the loan period3.

8. Outstanding trade debts is assessable income until unless there is substantial doubt as to the final

recovery of such debt. Hence, the amount is correctly included in ascertaining taxable profit of

the business. Income from retail sales is assessable income and needs to be included in

calculation of assessable income. Since, it is already included in sales thus, there is no

requirement to make any adjustment to the accounting profit for calculation taxable profit of

business4.

2 Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

3 n, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on corporate tax

avoidance spanning the global financial crisis: Evidence from Australia." Economic

Modelling 44 (2015): 44-53.

4 Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

6

TAXATION LAW

9. Unranked dividend and dividend receive from foreign companies are assessable income and to be

considered for computing taxable income.

10. Since, Tax Commissioner restrict the reasonable amount of salary for the directors at $40,000

thus, excess amount of salary is to be added back to accounting profit5.

11. Unabsorbed losses of previous period is allowed to be set off against the business income of

current year to ascertain the net taxable income of a business.

Answer to question 2:

Issue:

The following are the issues in this case:

I. What is the tax implications of $1,000,000 received as compensation from one of the

customers of Matchstick Limited for termination of contract?

II. Tax implications of profit of $10,000,000 from sale of land to Matchstick Limited.

Rules:

Div. 6 of Income Tax Assessment Act 1997 (ITAA 1997) provides that receipt of damages and

compensation will be treated as ordinary or statutory income of business assessable for

computation of taxable income. Eligible Termination Payments, here in after referred as ETPs, is

considered as ordinary or statutory business income under div. 6 of ITAA 1997. However,

5 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Transitioning from an

Historical to a Contemporary Use of Tax Record Data for Measuring Top Incomes in

Australia." Economic Papers: A journal of applied economics and policy37, no. 2 (2018): 113-

145.

TAXATION LAW

9. Unranked dividend and dividend receive from foreign companies are assessable income and to be

considered for computing taxable income.

10. Since, Tax Commissioner restrict the reasonable amount of salary for the directors at $40,000

thus, excess amount of salary is to be added back to accounting profit5.

11. Unabsorbed losses of previous period is allowed to be set off against the business income of

current year to ascertain the net taxable income of a business.

Answer to question 2:

Issue:

The following are the issues in this case:

I. What is the tax implications of $1,000,000 received as compensation from one of the

customers of Matchstick Limited for termination of contract?

II. Tax implications of profit of $10,000,000 from sale of land to Matchstick Limited.

Rules:

Div. 6 of Income Tax Assessment Act 1997 (ITAA 1997) provides that receipt of damages and

compensation will be treated as ordinary or statutory income of business assessable for

computation of taxable income. Eligible Termination Payments, here in after referred as ETPs, is

considered as ordinary or statutory business income under div. 6 of ITAA 1997. However,

5 Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Transitioning from an

Historical to a Contemporary Use of Tax Record Data for Measuring Top Incomes in

Australia." Economic Papers: A journal of applied economics and policy37, no. 2 (2018): 113-

145.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

TAXATION LAW

compensation receipt as damages shall either be considered as ordinary income or capital gain

depending on the circumstances of each case.

ITAA provides that practical consequences must be considered to characterize the receipts of

compensation as ordinary income or capital gain. Income of capital gain is to be decided by

considering the circumstances of each case.

The character of the compensation received for damages in the hand of the recipient shall be

considered to characterize the compensation and its taxability. If the payment was to compensate

of loss of income then the same would be considered as ordinary income. In case the payment

was in capital account then the payment would be considered for capital gain6.

As per s6-5 of ITAA 1997, if the compensation is pertaining to income or to replace loss of

profit then such compensations shall be considered as ordinary income (s6-5 of ITAA 1997) and

accordingly, taxable as ordinary income.

ATO provides that in case of assets sold by a business then, resultant profit or loss from such

sale be considered as capital gain or capital loss for computation of tax liability of the business.

A company is not allowed to use discount method to calculate capital from sale of non-current

assets. In case of sale of land the proceeds received from sale shall be reduced by the cost of land

to calculate the amount of capital gain7.

6 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57, no. 1 (2017): 49-63.

7 Barnett, Katy, and Sirko Harder. Remedies in Australian private law. Cambridge University

Press, 2014.

TAXATION LAW

compensation receipt as damages shall either be considered as ordinary income or capital gain

depending on the circumstances of each case.

ITAA provides that practical consequences must be considered to characterize the receipts of

compensation as ordinary income or capital gain. Income of capital gain is to be decided by

considering the circumstances of each case.

The character of the compensation received for damages in the hand of the recipient shall be

considered to characterize the compensation and its taxability. If the payment was to compensate

of loss of income then the same would be considered as ordinary income. In case the payment

was in capital account then the payment would be considered for capital gain6.

As per s6-5 of ITAA 1997, if the compensation is pertaining to income or to replace loss of

profit then such compensations shall be considered as ordinary income (s6-5 of ITAA 1997) and

accordingly, taxable as ordinary income.

ATO provides that in case of assets sold by a business then, resultant profit or loss from such

sale be considered as capital gain or capital loss for computation of tax liability of the business.

A company is not allowed to use discount method to calculate capital from sale of non-current

assets. In case of sale of land the proceeds received from sale shall be reduced by the cost of land

to calculate the amount of capital gain7.

6 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57, no. 1 (2017): 49-63.

7 Barnett, Katy, and Sirko Harder. Remedies in Australian private law. Cambridge University

Press, 2014.

8

TAXATION LAW

Carapark Holdings Ltd v FCT (1967) 115 CLR 653, 660:

The above case ruling provides explanation as to the reason of treating of insurance claim

received for death of one of the employees as income of the company. The factor to be

considered is the character of the compensation. Thus, if the compensation is on revenue account

then it is to be considered as ordinary income whereas if the same os on capital account then it

will be considered as capital gain8.

Application:

Applying the provisions of s6-5 of ITAA 1997, the compensation received it is clear that one of

the customers of Matchsticks Limited has paid a compensation of $1,000,000 for terminating the

contract with the company. Since, the contract was to sale woods of the company in the ordinary

course of business hence, the compensation paid by Strike a Light Pty Ltd is receipt to

compensate the loss of ordinary revenue. Hence, the amount of compensation received by

Matchsticks Limited is to be treated as ordinary income as per s6-5 of ITAA 19979. Accordingly,

the amount of compensation received by Matchsticks Pty Ltd is ordinary income to be assessable

as business income of the company, shall be taxed accordingly10.

8 Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

9 Eslake, Saul. "Reforming the Australian taxation system: a principled approach." Australian

Financial Review Tax Reform Summit (2015).

10 Mapp III, Richard C., John M. Peterson, and Robert Q. Johnson. "Qualified and nonqualified

deferred compensation plans in small businesses: creative uses and problem solving." In Tax

TAXATION LAW

Carapark Holdings Ltd v FCT (1967) 115 CLR 653, 660:

The above case ruling provides explanation as to the reason of treating of insurance claim

received for death of one of the employees as income of the company. The factor to be

considered is the character of the compensation. Thus, if the compensation is on revenue account

then it is to be considered as ordinary income whereas if the same os on capital account then it

will be considered as capital gain8.

Application:

Applying the provisions of s6-5 of ITAA 1997, the compensation received it is clear that one of

the customers of Matchsticks Limited has paid a compensation of $1,000,000 for terminating the

contract with the company. Since, the contract was to sale woods of the company in the ordinary

course of business hence, the compensation paid by Strike a Light Pty Ltd is receipt to

compensate the loss of ordinary revenue. Hence, the amount of compensation received by

Matchsticks Limited is to be treated as ordinary income as per s6-5 of ITAA 19979. Accordingly,

the amount of compensation received by Matchsticks Pty Ltd is ordinary income to be assessable

as business income of the company, shall be taxed accordingly10.

8 Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

9 Eslake, Saul. "Reforming the Australian taxation system: a principled approach." Australian

Financial Review Tax Reform Summit (2015).

10 Mapp III, Richard C., John M. Peterson, and Robert Q. Johnson. "Qualified and nonqualified

deferred compensation plans in small businesses: creative uses and problem solving." In Tax

9

TAXATION LAW

The sale on profit of land though was not acquired with the objective or intention to sale at the

time of acquisition but the resultant profit from sale of such land shall be treated as capital gain

of the business. The company has realized a profit of $10,000,000 from sale of the land. Hence,

the amount of capital gain from sale of land is $10,000,000 for the tax year ending on June 30,

2018. The company shall be liable to pay tax on its ordinary income as well as capital gain as per

the applicable rate of tax11.

Conclusion:

As per the provisions of Income Tax Assessment Act 1997 (s6-5 of the act) the compensation of

$1,000,000 receipt by Matchsticks Limited is in the nature of ordinary income to the company

and shall be considered in calculating the business income of the company.

The realized gain from sale of land, i.e. $10,000,000 is capital gain of Matchstick Limited and

shall be taxed accordingly in the hands of the company.

Conference (Marshall-Wythe School of Law). William and Mary Tax Conference, no. 63, pp.

1_1-1_26. College of William and Mary, Marshall-Wythe School of Law, 2017.

11 Borden, Bradley T. "Income-Based Effective Tax Rates and Choice-of-Entity Consideratins

Under the 2017 Tax Act." (2018).

TAXATION LAW

The sale on profit of land though was not acquired with the objective or intention to sale at the

time of acquisition but the resultant profit from sale of such land shall be treated as capital gain

of the business. The company has realized a profit of $10,000,000 from sale of the land. Hence,

the amount of capital gain from sale of land is $10,000,000 for the tax year ending on June 30,

2018. The company shall be liable to pay tax on its ordinary income as well as capital gain as per

the applicable rate of tax11.

Conclusion:

As per the provisions of Income Tax Assessment Act 1997 (s6-5 of the act) the compensation of

$1,000,000 receipt by Matchsticks Limited is in the nature of ordinary income to the company

and shall be considered in calculating the business income of the company.

The realized gain from sale of land, i.e. $10,000,000 is capital gain of Matchstick Limited and

shall be taxed accordingly in the hands of the company.

Conference (Marshall-Wythe School of Law). William and Mary Tax Conference, no. 63, pp.

1_1-1_26. College of William and Mary, Marshall-Wythe School of Law, 2017.

11 Borden, Bradley T. "Income-Based Effective Tax Rates and Choice-of-Entity Consideratins

Under the 2017 Tax Act." (2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10

TAXATION LAW

References:

Barnett, Katy, and Sirko Harder. Remedies in Australian private law. Cambridge University

Press, 2014.

Borden, Bradley T. "Income-Based Effective Tax Rates and Choice-of-Entity Consideratins

Under the 2017 Tax Act." (2018).

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Transitioning from an Historical

to a Contemporary Use of Tax Record Data for Measuring Top Incomes in Australia." Economic

Papers: A journal of applied economics and policy37, no. 2 (2018): 113-145.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Eslake, Saul. "Reforming the Australian taxation system: a principled approach." Australian

Financial Review Tax Reform Summit (2015).

Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57, no. 1 (2017): 49-63.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Mapp III, Richard C., John M. Peterson, and Robert Q. Johnson. "Qualified and nonqualified

deferred compensation plans in small businesses: creative uses and problem solving." In Tax

Conference (Marshall-Wythe School of Law). William and Mary Tax Conference, no. 63, pp.

1_1-1_26. College of William and Mary, Marshall-Wythe School of Law, 2017.

TAXATION LAW

References:

Barnett, Katy, and Sirko Harder. Remedies in Australian private law. Cambridge University

Press, 2014.

Borden, Bradley T. "Income-Based Effective Tax Rates and Choice-of-Entity Consideratins

Under the 2017 Tax Act." (2018).

Burkhauser, Richard V., Markus H. Hahn, and Roger Wilkins. "Transitioning from an Historical

to a Contemporary Use of Tax Record Data for Measuring Top Incomes in Australia." Economic

Papers: A journal of applied economics and policy37, no. 2 (2018): 113-145.

Chardon, Toni, Brett Freudenberg, and Mark Brimble. "Tax literacy in Australia: not knowing

your deduction from your offset." Austl. Tax F. 31 (2016): 321.

Eslake, Saul. "Reforming the Australian taxation system: a principled approach." Australian

Financial Review Tax Reform Summit (2015).

Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of

Australia to tax economic activity in offshore hubs and the position of the Australian Taxation

Office." The APPEA Journal 57, no. 1 (2017): 49-63.

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Mapp III, Richard C., John M. Peterson, and Robert Q. Johnson. "Qualified and nonqualified

deferred compensation plans in small businesses: creative uses and problem solving." In Tax

Conference (Marshall-Wythe School of Law). William and Mary Tax Conference, no. 63, pp.

1_1-1_26. College of William and Mary, Marshall-Wythe School of Law, 2017.

11

TAXATION LAW

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

TAXATION LAW

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

Richardson, Grant, Grantley Taylor, and Roman Lanis. "The impact of financial distress on

corporate tax avoidance spanning the global financial crisis: Evidence from

Australia." Economic Modelling 44 (2015): 44-53.

Woellner, Robin, Stephen Barkoczy, Shirley Murphy, Chris Evans, and Dale Pinto. "Australian

Taxation Law 2016." OUP Catalogue (2016).

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.