Taxation Law Assignment 1: Broadmeadow Park - Payroll, GST, & FBT

VerifiedAdded on 2023/06/15

|12

|2119

|246

Homework Assignment

AI Summary

This assignment solution delves into various aspects of taxation law, focusing on payroll, GST (Goods and Services Tax), and FBT (Fringe Benefits Tax) within the context of Broadmeadow Park, a horse-racing stable. It includes calculations of PayG deductions and net wages for employees, determination of superannuation guarantee obligations, and computation of net tax payable, considering assessable income and allowable deductions. The analysis addresses the GST implications of different business activities, such as training fees, prize money, and trade-ins, while also examining creditable acquisitions and input tax credits. The assignment applies relevant sections of the Income Tax Assessment Act (ITAA) and Goods and Services Tax Act (GSTR) to determine taxable income and GST liabilities. Finally, it summarizes GST calculations and reporting requirements, providing a comprehensive overview of the taxation issues relevant to Broadmeadow Park's operations.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Reference List:.........................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................2

Answer to question 3:.................................................................................................................2

Answer to question 4:.................................................................................................................5

Answer to question 5:.................................................................................................................6

Reference List:.........................................................................................................................10

2TAXATION LAW

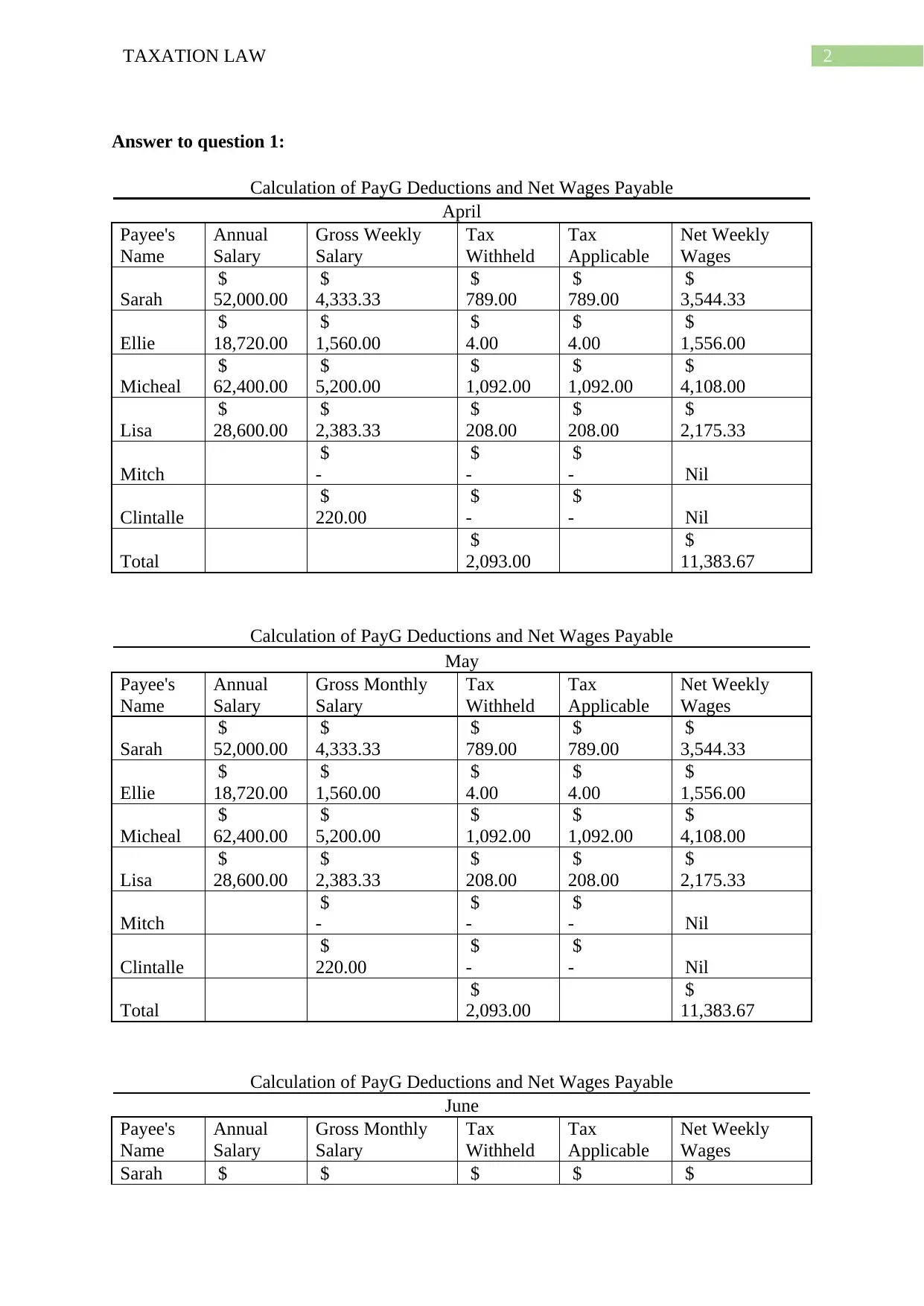

Answer to question 1:

Calculation of PayG Deductions and Net Wages Payable

April

Payee's

Name

Annual

Salary

Gross Weekly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah

$

52,000.00

$

4,333.33

$

789.00

$

789.00

$

3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Calculation of PayG Deductions and Net Wages Payable

May

Payee's

Name

Annual

Salary

Gross Monthly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah

$

52,000.00

$

4,333.33

$

789.00

$

789.00

$

3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Calculation of PayG Deductions and Net Wages Payable

June

Payee's

Name

Annual

Salary

Gross Monthly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah $ $ $ $ $

Answer to question 1:

Calculation of PayG Deductions and Net Wages Payable

April

Payee's

Name

Annual

Salary

Gross Weekly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah

$

52,000.00

$

4,333.33

$

789.00

$

789.00

$

3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Calculation of PayG Deductions and Net Wages Payable

May

Payee's

Name

Annual

Salary

Gross Monthly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah

$

52,000.00

$

4,333.33

$

789.00

$

789.00

$

3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Calculation of PayG Deductions and Net Wages Payable

June

Payee's

Name

Annual

Salary

Gross Monthly

Salary

Tax

Withheld

Tax

Applicable

Net Weekly

Wages

Sarah $ $ $ $ $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

52,000.00 4,333.33 789.00 789.00 3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Answer to question 2:

Calculation of Superannuation Guarantee Obligation

Payee's

Name Salary

Quarterly Times

Earnings Superannuation Guarantee

Sarah

$

52,000.00

$

13,000.00

$

1,350.00

Ellie

$

18,720.00

$

4,680.00

$

1,350.00

Micheal

$

62,400.00

$

15,600.00

$

1,350.00

Lisa

$

28,600.00

$

7,150.00

$

1,350.00

Mitch

$

1,500.00

$

1,500.00

$

1,350.00

Clintalle

$

3,190.00

$

3,190.00

$

1,350.00

Note: Superannuation guarantee of every employee is $450 for each month

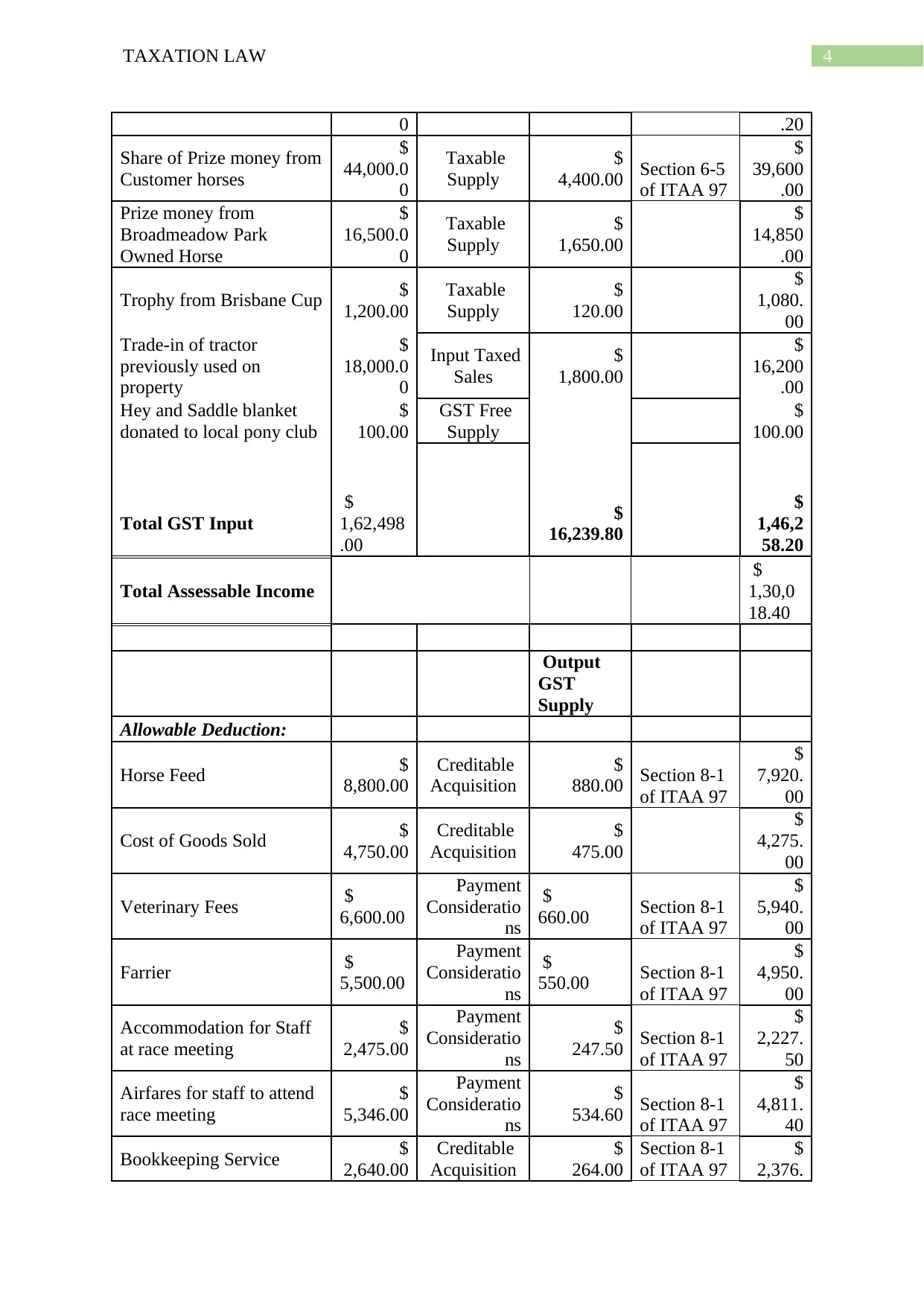

Answer to question 3:

Computation of Net Tax Payable

Inclusiv

e of

GST

Type Input tax

supply

Particulars Amount

($)

Amount

($) Section Amou

nt ($)

Assessable Income:

Training Fees $

82,698.0

Input Taxed

Sales

$

8,269.80

Section 6-5

of ITAA 97

$

74,428

52,000.00 4,333.33 789.00 789.00 3,544.33

Ellie

$

18,720.00

$

1,560.00

$

4.00

$

4.00

$

1,556.00

Micheal

$

62,400.00

$

5,200.00

$

1,092.00

$

1,092.00

$

4,108.00

Lisa

$

28,600.00

$

2,383.33

$

208.00

$

208.00

$

2,175.33

Mitch

$

-

$

-

$

- Nil

Clintalle

$

220.00

$

-

$

- Nil

Total

$

2,093.00

$

11,383.67

Answer to question 2:

Calculation of Superannuation Guarantee Obligation

Payee's

Name Salary

Quarterly Times

Earnings Superannuation Guarantee

Sarah

$

52,000.00

$

13,000.00

$

1,350.00

Ellie

$

18,720.00

$

4,680.00

$

1,350.00

Micheal

$

62,400.00

$

15,600.00

$

1,350.00

Lisa

$

28,600.00

$

7,150.00

$

1,350.00

Mitch

$

1,500.00

$

1,500.00

$

1,350.00

Clintalle

$

3,190.00

$

3,190.00

$

1,350.00

Note: Superannuation guarantee of every employee is $450 for each month

Answer to question 3:

Computation of Net Tax Payable

Inclusiv

e of

GST

Type Input tax

supply

Particulars Amount

($)

Amount

($) Section Amou

nt ($)

Assessable Income:

Training Fees $

82,698.0

Input Taxed

Sales

$

8,269.80

Section 6-5

of ITAA 97

$

74,428

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

0 .20

Share of Prize money from

Customer horses

$

44,000.0

0

Taxable

Supply

$

4,400.00 Section 6-5

of ITAA 97

$

39,600

.00

Prize money from

Broadmeadow Park

Owned Horse

$

16,500.0

0

Taxable

Supply

$

1,650.00

$

14,850

.00

Trophy from Brisbane Cup $

1,200.00

Taxable

Supply

$

120.00

$

1,080.

00

Trade-in of tractor

previously used on

property

$

18,000.0

0

Input Taxed

Sales

$

1,800.00

$

16,200

.00

Hey and Saddle blanket

donated to local pony club

$

100.00

GST Free

Supply

$

100.00

Total GST Input

$

1,62,498

.00

$

16,239.80

$

1,46,2

58.20

Total Assessable Income

$

1,30,0

18.40

Output

GST

Supply

Allowable Deduction:

Horse Feed $

8,800.00

Creditable

Acquisition

$

880.00 Section 8-1

of ITAA 97

$

7,920.

00

Cost of Goods Sold $

4,750.00

Creditable

Acquisition

$

475.00

$

4,275.

00

Veterinary Fees $

6,600.00

Payment

Consideratio

ns

$

660.00 Section 8-1

of ITAA 97

$

5,940.

00

Farrier $

5,500.00

Payment

Consideratio

ns

$

550.00 Section 8-1

of ITAA 97

$

4,950.

00

Accommodation for Staff

at race meeting

$

2,475.00

Payment

Consideratio

ns

$

247.50 Section 8-1

of ITAA 97

$

2,227.

50

Airfares for staff to attend

race meeting

$

5,346.00

Payment

Consideratio

ns

$

534.60 Section 8-1

of ITAA 97

$

4,811.

40

Bookkeeping Service $

2,640.00

Creditable

Acquisition

$

264.00

Section 8-1

of ITAA 97

$

2,376.

0 .20

Share of Prize money from

Customer horses

$

44,000.0

0

Taxable

Supply

$

4,400.00 Section 6-5

of ITAA 97

$

39,600

.00

Prize money from

Broadmeadow Park

Owned Horse

$

16,500.0

0

Taxable

Supply

$

1,650.00

$

14,850

.00

Trophy from Brisbane Cup $

1,200.00

Taxable

Supply

$

120.00

$

1,080.

00

Trade-in of tractor

previously used on

property

$

18,000.0

0

Input Taxed

Sales

$

1,800.00

$

16,200

.00

Hey and Saddle blanket

donated to local pony club

$

100.00

GST Free

Supply

$

100.00

Total GST Input

$

1,62,498

.00

$

16,239.80

$

1,46,2

58.20

Total Assessable Income

$

1,30,0

18.40

Output

GST

Supply

Allowable Deduction:

Horse Feed $

8,800.00

Creditable

Acquisition

$

880.00 Section 8-1

of ITAA 97

$

7,920.

00

Cost of Goods Sold $

4,750.00

Creditable

Acquisition

$

475.00

$

4,275.

00

Veterinary Fees $

6,600.00

Payment

Consideratio

ns

$

660.00 Section 8-1

of ITAA 97

$

5,940.

00

Farrier $

5,500.00

Payment

Consideratio

ns

$

550.00 Section 8-1

of ITAA 97

$

4,950.

00

Accommodation for Staff

at race meeting

$

2,475.00

Payment

Consideratio

ns

$

247.50 Section 8-1

of ITAA 97

$

2,227.

50

Airfares for staff to attend

race meeting

$

5,346.00

Payment

Consideratio

ns

$

534.60 Section 8-1

of ITAA 97

$

4,811.

40

Bookkeeping Service $

2,640.00

Creditable

Acquisition

$

264.00

Section 8-1

of ITAA 97

$

2,376.

5TAXATION LAW

00

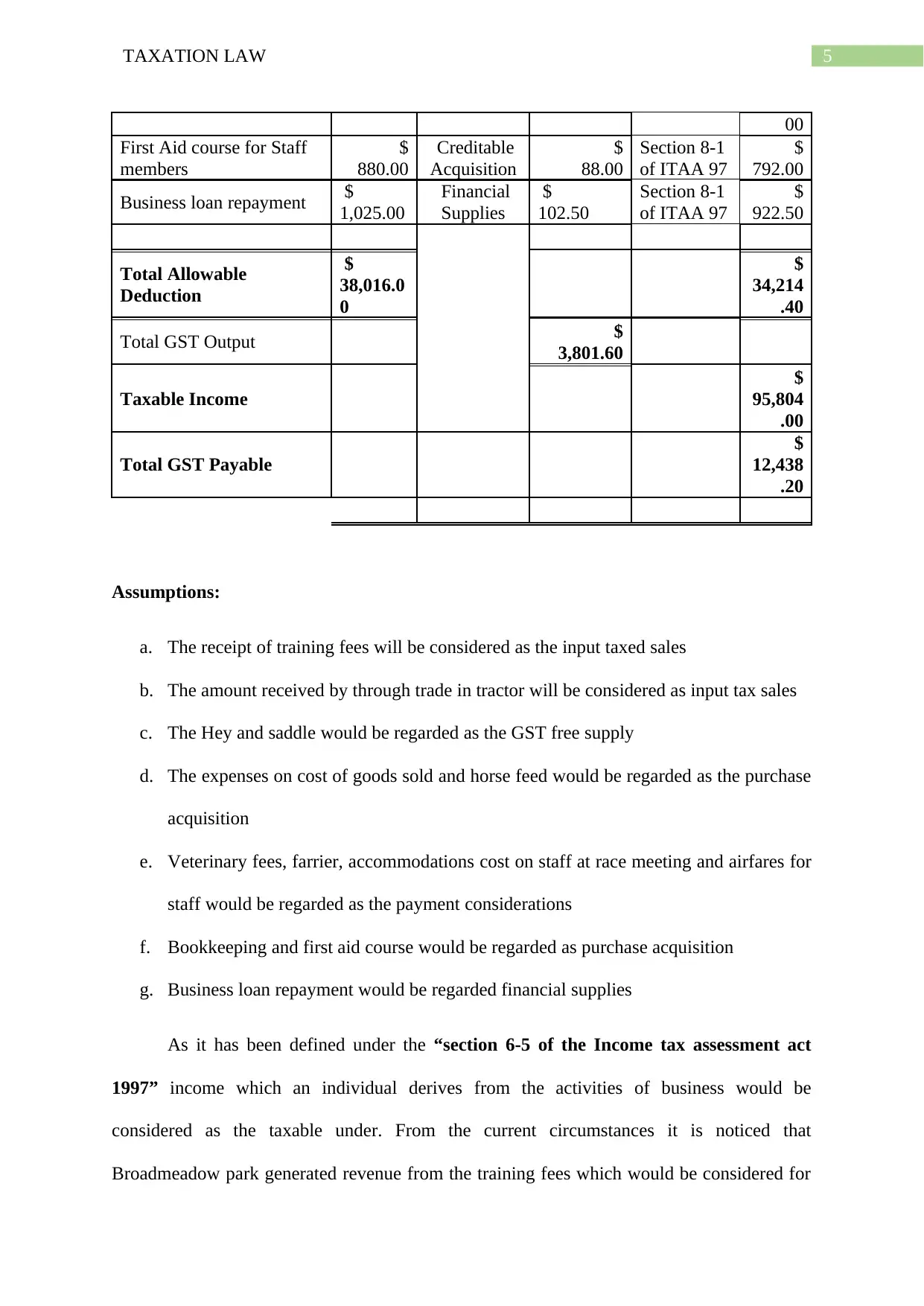

First Aid course for Staff

members

$

880.00

Creditable

Acquisition

$

88.00

Section 8-1

of ITAA 97

$

792.00

Business loan repayment $

1,025.00

Financial

Supplies

$

102.50

Section 8-1

of ITAA 97

$

922.50

Total Allowable

Deduction

$

38,016.0

0

$

34,214

.40

Total GST Output $

3,801.60

Taxable Income

$

95,804

.00

Total GST Payable

$

12,438

.20

Assumptions:

a. The receipt of training fees will be considered as the input taxed sales

b. The amount received by through trade in tractor will be considered as input tax sales

c. The Hey and saddle would be regarded as the GST free supply

d. The expenses on cost of goods sold and horse feed would be regarded as the purchase

acquisition

e. Veterinary fees, farrier, accommodations cost on staff at race meeting and airfares for

staff would be regarded as the payment considerations

f. Bookkeeping and first aid course would be regarded as purchase acquisition

g. Business loan repayment would be regarded financial supplies

As it has been defined under the “section 6-5 of the Income tax assessment act

1997” income which an individual derives from the activities of business would be

considered as the taxable under. From the current circumstances it is noticed that

Broadmeadow park generated revenue from the training fees which would be considered for

00

First Aid course for Staff

members

$

880.00

Creditable

Acquisition

$

88.00

Section 8-1

of ITAA 97

$

792.00

Business loan repayment $

1,025.00

Financial

Supplies

$

102.50

Section 8-1

of ITAA 97

$

922.50

Total Allowable

Deduction

$

38,016.0

0

$

34,214

.40

Total GST Output $

3,801.60

Taxable Income

$

95,804

.00

Total GST Payable

$

12,438

.20

Assumptions:

a. The receipt of training fees will be considered as the input taxed sales

b. The amount received by through trade in tractor will be considered as input tax sales

c. The Hey and saddle would be regarded as the GST free supply

d. The expenses on cost of goods sold and horse feed would be regarded as the purchase

acquisition

e. Veterinary fees, farrier, accommodations cost on staff at race meeting and airfares for

staff would be regarded as the payment considerations

f. Bookkeeping and first aid course would be regarded as purchase acquisition

g. Business loan repayment would be regarded financial supplies

As it has been defined under the “section 6-5 of the Income tax assessment act

1997” income which an individual derives from the activities of business would be

considered as the taxable under. From the current circumstances it is noticed that

Broadmeadow park generated revenue from the training fees which would be considered for

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

assessment under the “section 6-5 of the ITAA 1997”. It is noteworthy to denote that there

were other receipts that would be considered for assessment namely share of prize money,

trophy from Brisbane Cup and trade in tractor.

One of the important consideration in this regard is that receipts would be considered

for GST under the “GSTR act 1999” relating to the receipts of the taxable supplies.

Additionally, it is found that Broadmeadow has incurred an expenses that would be treated as

the allowable deductions under the under “section 8-1 of the ITAA 1997” (Robin 2017). A

business will be allowed to claim an allowable deductions relating to the expenditure that is

incurred by the company for their workers together with the contribution for the

superannuation made for the workers.

The business carried by the Broadmeadow is a company and according to the

guidelines of the Australian taxation office Broadmeadow shall be entitled to claim an

allowable deductions relating to the wages that the company pay to its workers. In addition to

this, Broadmeadow has incurred an expenditure relating to the superannuation expenditure on

its workers. As result of this, in accordance with the “section 8-1 of the ITAA 1997”

broadmeadow will be entitled to claim an allowable deduction for the expenditure incurred

on the superannuation fund of its workers.

As it has been defined under the “taxation ruling of 97/17” an important

consideration has been staed under the “section 32-5 of the ITAA 1997” regarding the non-

allowance of the deductions incurred on entertainment of food and meal for its customers in

the local restaurant. Furthermore, “division 32 of the ITAA 1997” provides a prohibition

concerning the deduction of the expenses that is associated on the entertainment of the

employees.

assessment under the “section 6-5 of the ITAA 1997”. It is noteworthy to denote that there

were other receipts that would be considered for assessment namely share of prize money,

trophy from Brisbane Cup and trade in tractor.

One of the important consideration in this regard is that receipts would be considered

for GST under the “GSTR act 1999” relating to the receipts of the taxable supplies.

Additionally, it is found that Broadmeadow has incurred an expenses that would be treated as

the allowable deductions under the under “section 8-1 of the ITAA 1997” (Robin 2017). A

business will be allowed to claim an allowable deductions relating to the expenditure that is

incurred by the company for their workers together with the contribution for the

superannuation made for the workers.

The business carried by the Broadmeadow is a company and according to the

guidelines of the Australian taxation office Broadmeadow shall be entitled to claim an

allowable deductions relating to the wages that the company pay to its workers. In addition to

this, Broadmeadow has incurred an expenditure relating to the superannuation expenditure on

its workers. As result of this, in accordance with the “section 8-1 of the ITAA 1997”

broadmeadow will be entitled to claim an allowable deduction for the expenditure incurred

on the superannuation fund of its workers.

As it has been defined under the “taxation ruling of 97/17” an important

consideration has been staed under the “section 32-5 of the ITAA 1997” regarding the non-

allowance of the deductions incurred on entertainment of food and meal for its customers in

the local restaurant. Furthermore, “division 32 of the ITAA 1997” provides a prohibition

concerning the deduction of the expenses that is associated on the entertainment of the

employees.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

According to the judgement stated in the case of “Bow and others v. Heatly (1960)

STL 311” the spending incurred on the meal would be treated as the non-allowable

deductions (Miller and Oats 2016). Additionally, the expenditure on entertainment of the

employees by broadmeadow would be treated as the fringe benefit under the “Fringe Benefit

Tax Assessment Act 1986” and it would be considered for Fringe benefit which would be

liable for Fringe Benefit Tax. Furthermore, in accordance with the “section 8-1 of the ITAA

1997” Jimmy would be able to claim an allowable deductions relating to the expenditure

incurred for its business activities and the GST would be considered payable in regard to the

GSTR act 1999.

Answer to question 4:

According to the “taxation ruling of GSTR 2008/1” an individual would be able to

claim the input tax credit given that the taxpayer has made creditable acquisition or

importation (Miller and Oats 2016). To make the creditable acquisition or importation the

person would be required to make the importation which is entirely or partially for creditable

purpose. The taxation ruling of GSTR 2008/1 defines that there are some factors that helps in

determining whether the acquisition is for importation or for acquisition relating to the

creditable purpose. As evident in the present situation it is noticed that Broadmeadow has

made creditable acquisition for which it would be entitled to claim the input tax credit.

The acquisition that is made by the Broadmeadow is at the time of carrying on of the

enterprise which was domestic in nature. Additionally, the importation that is made by the

Broadmeadow would be liable for claiming an input tax. The goods and service tax act 1999

provides that the usual entitlement of the input tax credit from making the creditable

acquisitions and creditable importations. As it is noticed that the expenses incurred by

Broadmeadow was for acquiring anything that was entirely or solely for the creditable

purpose and the supply made will be considered as the taxable supply. “Section 11-15 of the

According to the judgement stated in the case of “Bow and others v. Heatly (1960)

STL 311” the spending incurred on the meal would be treated as the non-allowable

deductions (Miller and Oats 2016). Additionally, the expenditure on entertainment of the

employees by broadmeadow would be treated as the fringe benefit under the “Fringe Benefit

Tax Assessment Act 1986” and it would be considered for Fringe benefit which would be

liable for Fringe Benefit Tax. Furthermore, in accordance with the “section 8-1 of the ITAA

1997” Jimmy would be able to claim an allowable deductions relating to the expenditure

incurred for its business activities and the GST would be considered payable in regard to the

GSTR act 1999.

Answer to question 4:

According to the “taxation ruling of GSTR 2008/1” an individual would be able to

claim the input tax credit given that the taxpayer has made creditable acquisition or

importation (Miller and Oats 2016). To make the creditable acquisition or importation the

person would be required to make the importation which is entirely or partially for creditable

purpose. The taxation ruling of GSTR 2008/1 defines that there are some factors that helps in

determining whether the acquisition is for importation or for acquisition relating to the

creditable purpose. As evident in the present situation it is noticed that Broadmeadow has

made creditable acquisition for which it would be entitled to claim the input tax credit.

The acquisition that is made by the Broadmeadow is at the time of carrying on of the

enterprise which was domestic in nature. Additionally, the importation that is made by the

Broadmeadow would be liable for claiming an input tax. The goods and service tax act 1999

provides that the usual entitlement of the input tax credit from making the creditable

acquisitions and creditable importations. As it is noticed that the expenses incurred by

Broadmeadow was for acquiring anything that was entirely or solely for the creditable

purpose and the supply made will be considered as the taxable supply. “Section 11-15 of the

8TAXATION LAW

GSTR 2000” provides that an individual taxpayer acquires anything for the creditable

purpose up to the extent that the individual has acquired it in the course of carrying on of the

business enterprise.

As held in the case of “HP Mercantile Pty Ltd v Commissioner of Taxation” the

judgement of the court stated that under the legislative scheme the taxpayer would be entitled

to claim the input tax credit to make sure that the output tax payable by the taxpayer should

not be imposed on the value that includes tax payable (Robin 2017). Broadmedow Park under

the present situation would be able to claim an input tax credit for the acquisition that is made

by it relating to the supplies.

Table Representing Creditable Acquisition

Type

Particulars

Assessable Income:

Training Fees Input Taxed Sales

Share of Prize money from Customer horses Taxable Supply

Prize money from Broadmeadow Park Owned Horse Taxable Supply

Trophy from Brisbane Cup Taxable Supply

Trade-in of tractor previously used on property Input Taxed Sales

Hey and Saddle blanket donated to local pony club GST Free Supply

Total GST Input

Total Assessable Income

Allowable Deduction:

Horse Feed Creditable Acquisition

Cost of Goods Sold Creditable Acquisition

Veterinary Fees Payment Considerations

Farrier Payment Considerations

Accommodation for Staff at race meeting Payment Considerations

Airfares for staff to attend race meeting Payment Considerations

Bookkeeping Service Creditable Acquisition

GSTR 2000” provides that an individual taxpayer acquires anything for the creditable

purpose up to the extent that the individual has acquired it in the course of carrying on of the

business enterprise.

As held in the case of “HP Mercantile Pty Ltd v Commissioner of Taxation” the

judgement of the court stated that under the legislative scheme the taxpayer would be entitled

to claim the input tax credit to make sure that the output tax payable by the taxpayer should

not be imposed on the value that includes tax payable (Robin 2017). Broadmedow Park under

the present situation would be able to claim an input tax credit for the acquisition that is made

by it relating to the supplies.

Table Representing Creditable Acquisition

Type

Particulars

Assessable Income:

Training Fees Input Taxed Sales

Share of Prize money from Customer horses Taxable Supply

Prize money from Broadmeadow Park Owned Horse Taxable Supply

Trophy from Brisbane Cup Taxable Supply

Trade-in of tractor previously used on property Input Taxed Sales

Hey and Saddle blanket donated to local pony club GST Free Supply

Total GST Input

Total Assessable Income

Allowable Deduction:

Horse Feed Creditable Acquisition

Cost of Goods Sold Creditable Acquisition

Veterinary Fees Payment Considerations

Farrier Payment Considerations

Accommodation for Staff at race meeting Payment Considerations

Airfares for staff to attend race meeting Payment Considerations

Bookkeeping Service Creditable Acquisition

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

First Aid course for Staff members Creditable Acquisition

Business loan repayment Financial Supplies

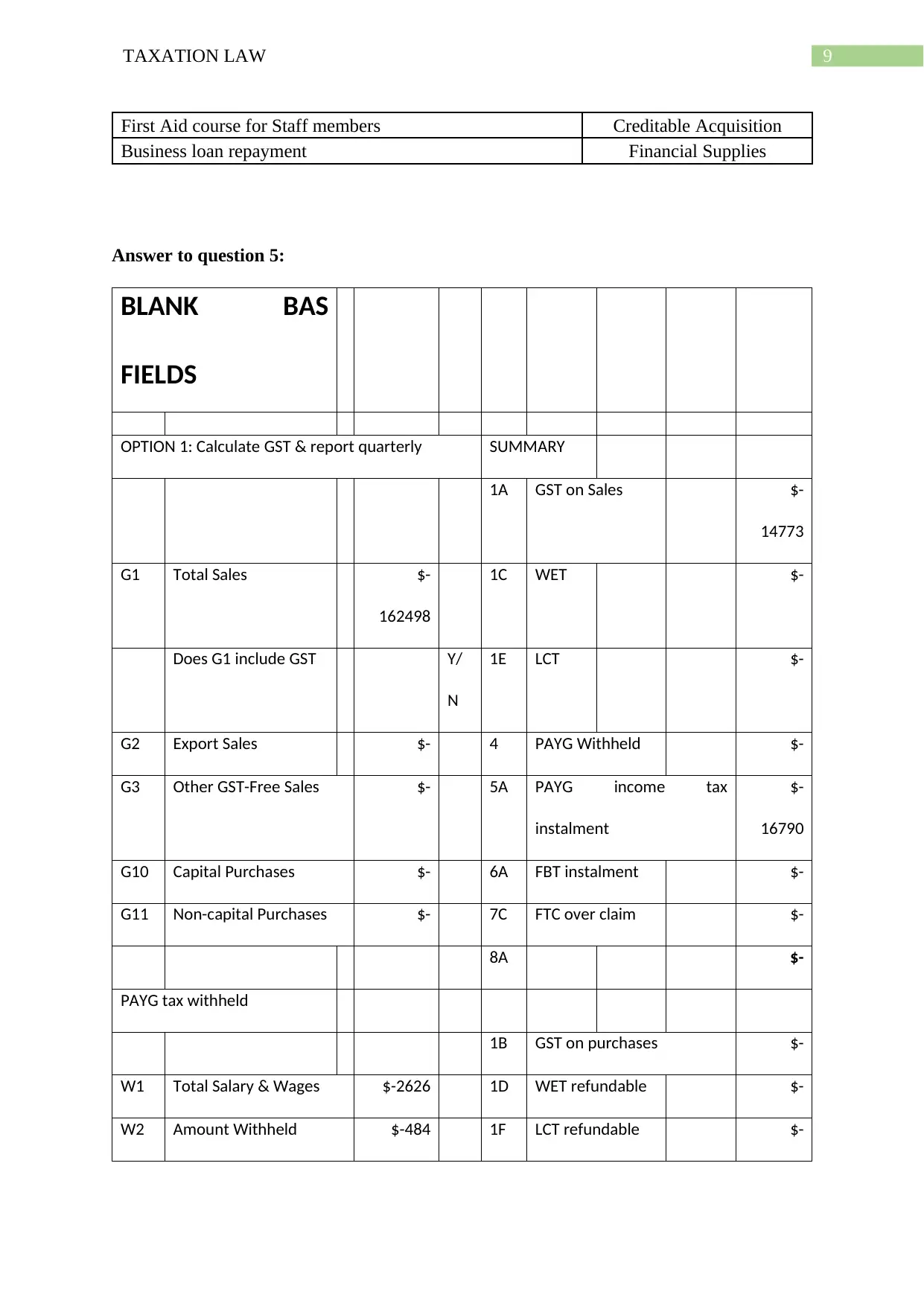

Answer to question 5:

BLANK BAS

FIELDS

OPTION 1: Calculate GST & report quarterly SUMMARY

1A GST on Sales $-

14773

G1 Total Sales $-

162498

1C WET $-

Does G1 include GST Y/

N

1E LCT $-

G2 Export Sales $- 4 PAYG Withheld $-

G3 Other GST-Free Sales $- 5A PAYG income tax

instalment

$-

16790

G10 Capital Purchases $- 6A FBT instalment $-

G11 Non-capital Purchases $- 7C FTC over claim $-

8A $-

PAYG tax withheld

1B GST on purchases $-

W1 Total Salary & Wages $-2626 1D WET refundable $-

W2 Amount Withheld $-484 1F LCT refundable $-

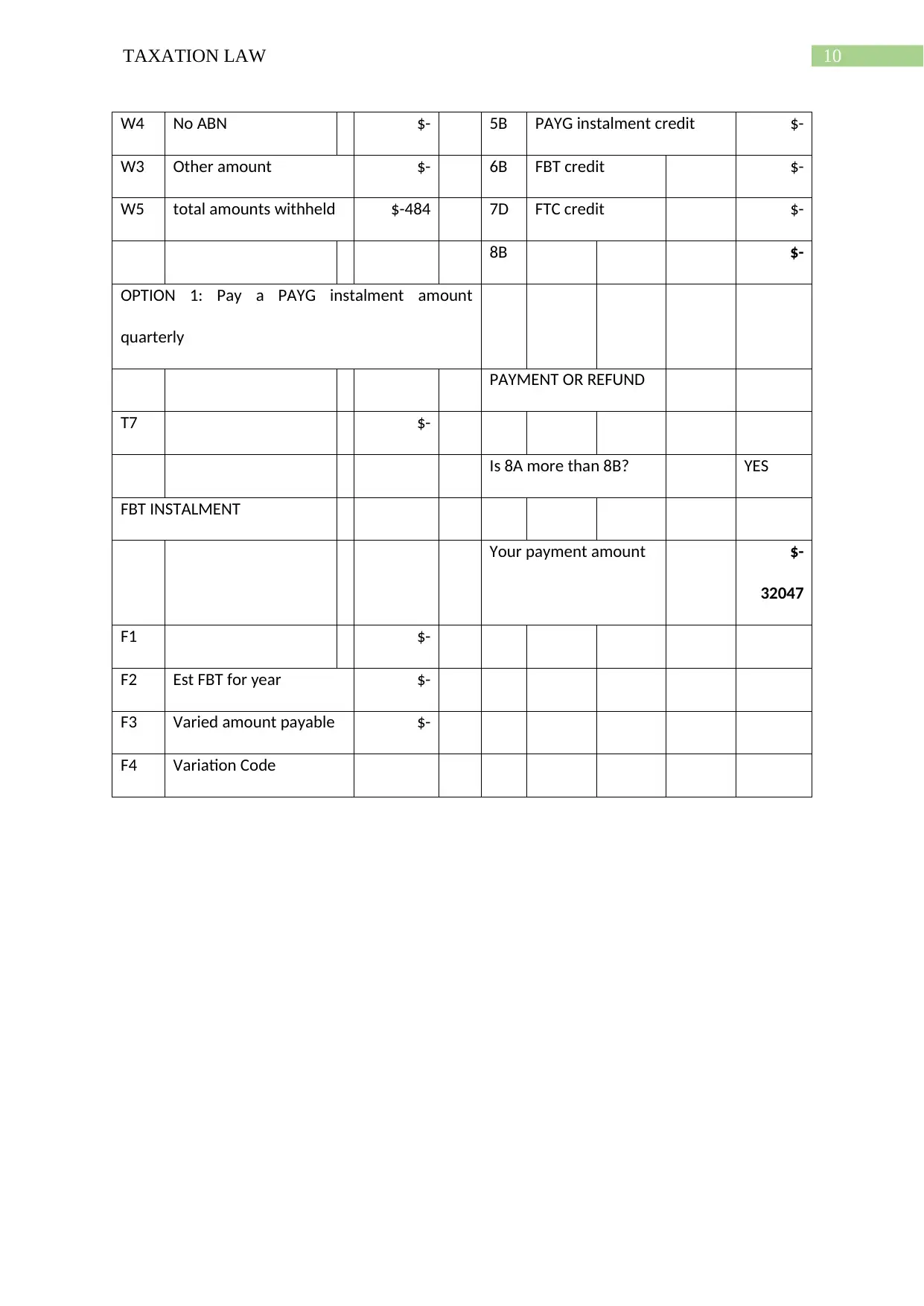

First Aid course for Staff members Creditable Acquisition

Business loan repayment Financial Supplies

Answer to question 5:

BLANK BAS

FIELDS

OPTION 1: Calculate GST & report quarterly SUMMARY

1A GST on Sales $-

14773

G1 Total Sales $-

162498

1C WET $-

Does G1 include GST Y/

N

1E LCT $-

G2 Export Sales $- 4 PAYG Withheld $-

G3 Other GST-Free Sales $- 5A PAYG income tax

instalment

$-

16790

G10 Capital Purchases $- 6A FBT instalment $-

G11 Non-capital Purchases $- 7C FTC over claim $-

8A $-

PAYG tax withheld

1B GST on purchases $-

W1 Total Salary & Wages $-2626 1D WET refundable $-

W2 Amount Withheld $-484 1F LCT refundable $-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

W4 No ABN $- 5B PAYG instalment credit $-

W3 Other amount $- 6B FBT credit $-

W5 total amounts withheld $-484 7D FTC credit $-

8B $-

OPTION 1: Pay a PAYG instalment amount

quarterly

PAYMENT OR REFUND

T7 $-

Is 8A more than 8B? YES

FBT INSTALMENT

Your payment amount $-

32047

F1 $-

F2 Est FBT for year $-

F3 Varied amount payable $-

F4 Variation Code

W4 No ABN $- 5B PAYG instalment credit $-

W3 Other amount $- 6B FBT credit $-

W5 total amounts withheld $-484 7D FTC credit $-

8B $-

OPTION 1: Pay a PAYG instalment amount

quarterly

PAYMENT OR REFUND

T7 $-

Is 8A more than 8B? YES

FBT INSTALMENT

Your payment amount $-

32047

F1 $-

F2 Est FBT for year $-

F3 Varied amount payable $-

F4 Variation Code

11TAXATION LAW

Reference List:

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

Reference List:

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

ROBIN, H., 2017. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.