Taxation Law: Capital Gain/Loss, Assessable Income for Partners, Trust Income, and Redundancy Payment Taxability

4 Pages894 Words312 Views

Added on 2023-06-06

About This Document

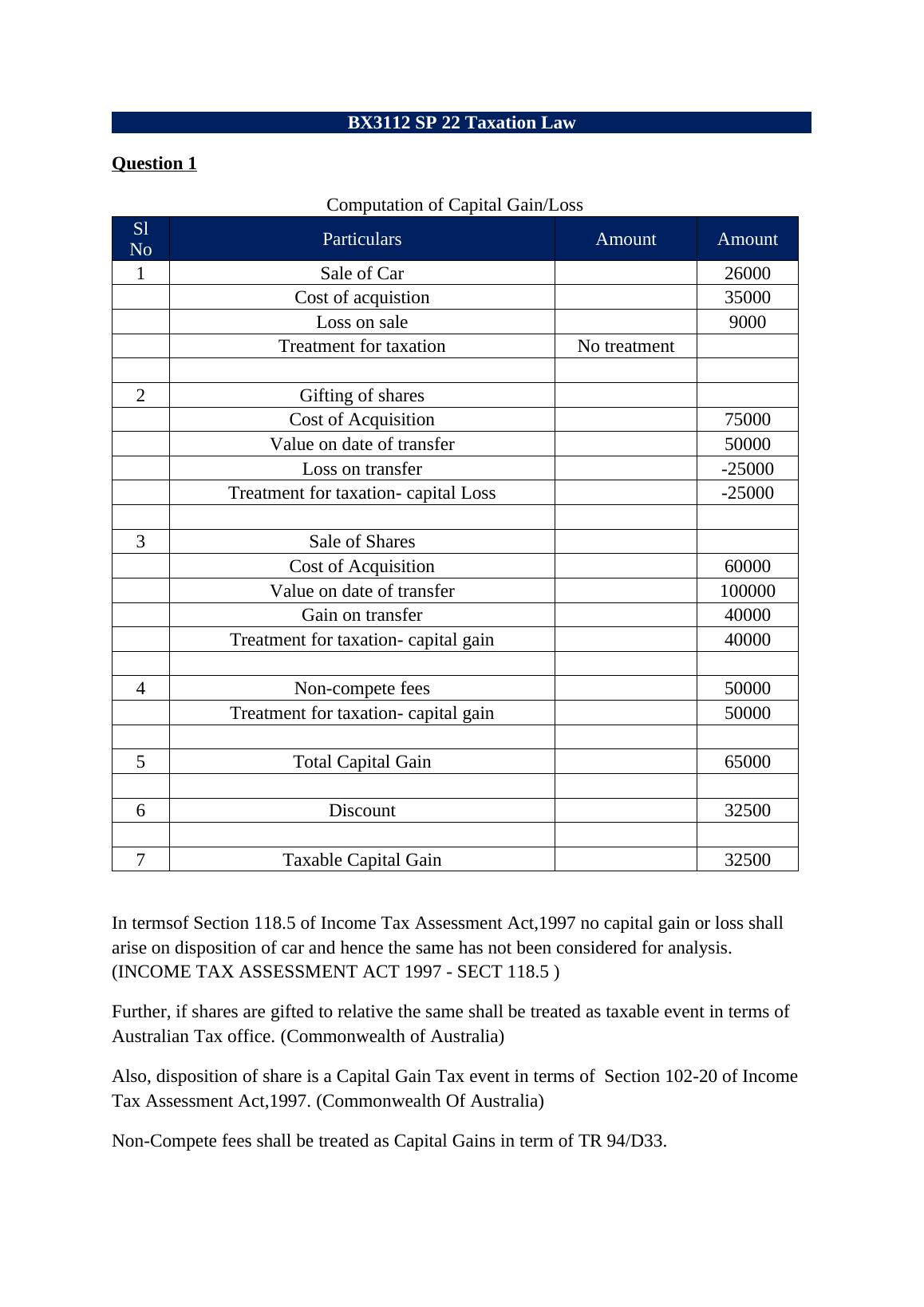

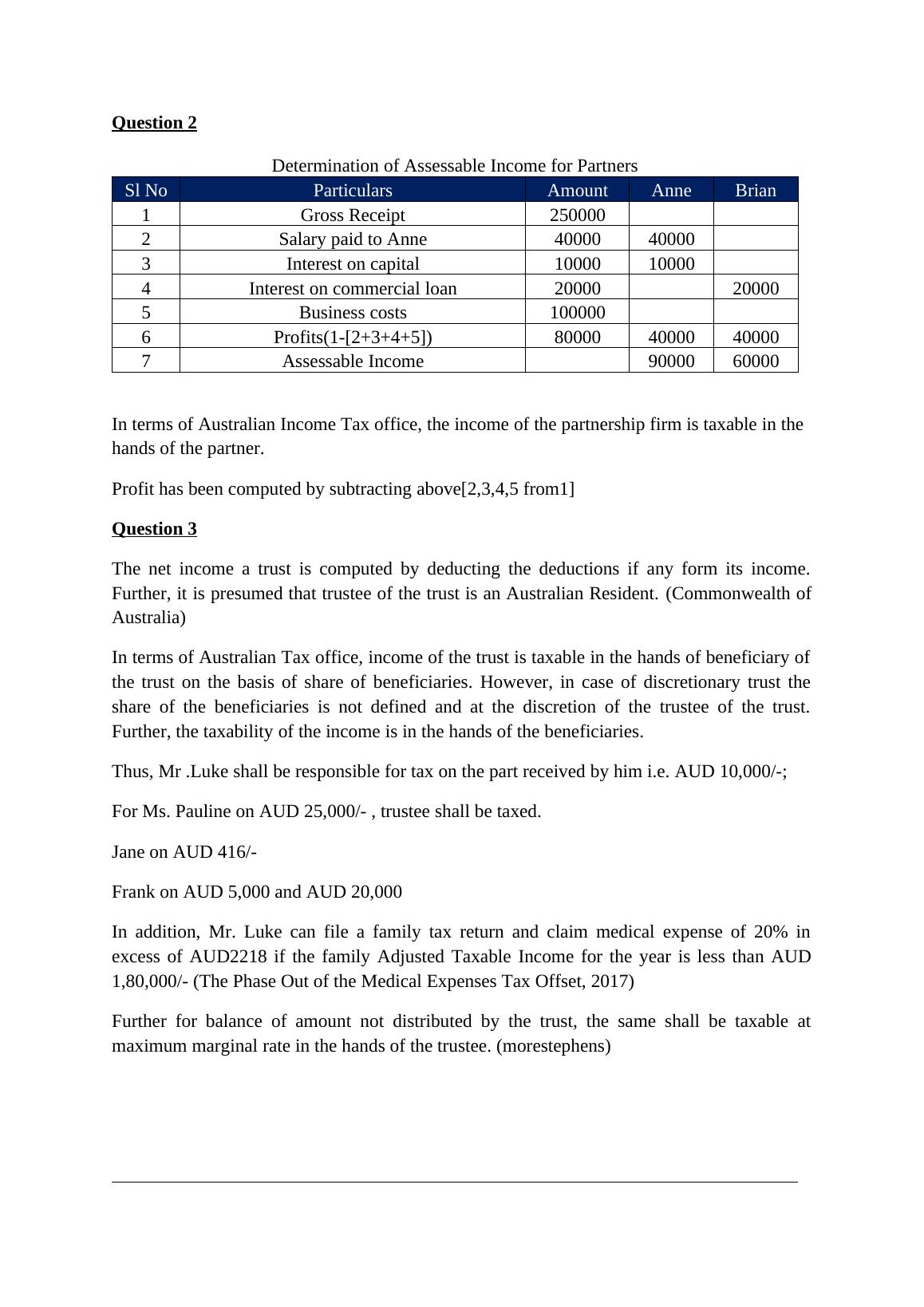

This article discusses the computation of capital gain/loss, assessable income for partners, trust income, and redundancy payment taxability in Taxation Law. It includes relevant sections of the Income Tax Assessment Act, 1997 and Commonwealth of Australia. The article also mentions the tax liability of Mr. Luke and his family, and the medical expense tax offset. Desklib provides solved assignments, essays, and dissertations on Taxation Law.

Taxation Law: Capital Gain/Loss, Assessable Income for Partners, Trust Income, and Redundancy Payment Taxability

Added on 2023-06-06

ShareRelated Documents

End of preview

Want to access all the pages? Upload your documents or become a member.