Taxation Law: Capital Gains, Ordinary Income, and Deductions

Added on 2023-06-03

22 Pages6093 Words316 Views

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer to question 3:...............................................................................................................11

References:...............................................................................................................................18

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................6

Answer to question 3:...............................................................................................................11

References:...............................................................................................................................18

2TAXATION LAW

Answer to question 1:

According to the Australian taxation office an individual tax payer may make a

capital gains or capital loss when they sell the rental property that is acquired on or after 19th

September 1985. In the circumstances of the sale or disposal or the real estate the time of the

event is treated normally when a person enters into the contract usually when the settlement

is reached (Sadiq et al. 2013). A person may make the capital gains from the sale of the rental

property up to the extent that the capital proceeds that is received by them is greater than the

cost base of the property. A taxpayer might make the capital loss up to the extent that the

property reduce cost base is greater than the capital proceeds.

A gain is treated as the capital gains which is not subjected to income tax under the

ordinary concepts. The income tax liability of the taxpayer includes the net capital gains. In

other words, the net capital gains is included into the assessable income of the taxpayers

(Woellner et al. 2016). The cost base and the reduced cost base of the property comprises of

the amount that is paid for along with the certain incidental costs that are related with

acquiring, holding and selling the property. This includes the legal fees, stamp duty and real

estate agent commission.

A CGT event A1 occurs under “section 104-10 (1) of the ITAA 1997” when the

taxpayer sells any CGT asset. In the current situation it is noticed that Kylie sold an

investment property for $580,000. The selling of investment apartment resulted in “CGT

event A1” under “section 104-10 (1) of the ITAA 1997” (Braithwaite 2017). The apartment

was however bought for $360,000. At the time of acquiring the holiday apartment Kylie

reported an expenses of $5000 and $4000 respectively for stamp duty and valuation costs.

According to the “section 110-25” the cost base of the asset includes the total amount of

money paid to acquire the property. With reference to “section 110-25” expenses on stamp

Answer to question 1:

According to the Australian taxation office an individual tax payer may make a

capital gains or capital loss when they sell the rental property that is acquired on or after 19th

September 1985. In the circumstances of the sale or disposal or the real estate the time of the

event is treated normally when a person enters into the contract usually when the settlement

is reached (Sadiq et al. 2013). A person may make the capital gains from the sale of the rental

property up to the extent that the capital proceeds that is received by them is greater than the

cost base of the property. A taxpayer might make the capital loss up to the extent that the

property reduce cost base is greater than the capital proceeds.

A gain is treated as the capital gains which is not subjected to income tax under the

ordinary concepts. The income tax liability of the taxpayer includes the net capital gains. In

other words, the net capital gains is included into the assessable income of the taxpayers

(Woellner et al. 2016). The cost base and the reduced cost base of the property comprises of

the amount that is paid for along with the certain incidental costs that are related with

acquiring, holding and selling the property. This includes the legal fees, stamp duty and real

estate agent commission.

A CGT event A1 occurs under “section 104-10 (1) of the ITAA 1997” when the

taxpayer sells any CGT asset. In the current situation it is noticed that Kylie sold an

investment property for $580,000. The selling of investment apartment resulted in “CGT

event A1” under “section 104-10 (1) of the ITAA 1997” (Braithwaite 2017). The apartment

was however bought for $360,000. At the time of acquiring the holiday apartment Kylie

reported an expenses of $5000 and $4000 respectively for stamp duty and valuation costs.

According to the “section 110-25” the cost base of the asset includes the total amount of

money paid to acquire the property. With reference to “section 110-25” expenses on stamp

3TAXATION LAW

duty and valuation costs for acquiring the rental property are added to the cost base of the

apartment under the second element.

The third element of the cost base items includes the cost of ownership. The cost of

ownership comprises of the interest, cost of maintenance, repairs and renovation, insurance,

rates and land tax (Bankman et al. 2017). Kylie later reported on 1st July 2009 relating to

costs incurred on renovating the apartment. Kylie incurred renovation cost of $15,000. The

cost of renovating the apartment falls under the third element of cost base under “section

110-25 of the ITAA 1997”. Therefore, the same is added into the cost base of the apartment.

The fourth element of cost base comprises of the capital enhancement and

preservation costs. This includes any form of capital expenditure such as improvement to the

asset that is incurred by the taxpayer in increasing the value of the asset that forms the part of

the fourth element of the cost base under “section 110-25 (5) of the ITAA 1997” (Schenk

2017). The fourth element of cost base includes the capital expenditure that is related to the

installation or moving the asset. Kylie later reports on 1st February 2009 an expenditure of

$40,000 related to addition of second bathroom in the apartment. The cost can be

characterised as improvement to the asset in the form of capital enhancement and falls under

the part of fourth element of cost base.

While arriving at the final settlement of the investment apartment Kylie reported legal

expenses and real estate commission. The expenses are considered as cost of selling and the

same is subtracted to ascertain the net selling price (Murphy and Higgins 2016). The selling

of investment apartment resulted in capital gains under “CGT event A1” and the net amount

of capital gains is included into the assessable income of Kylie.

Later Kylie granted a three month option of purchasing the rental property to local

property developer which eventually lapsed and resulted in receipt of $10,500. She incurred

duty and valuation costs for acquiring the rental property are added to the cost base of the

apartment under the second element.

The third element of the cost base items includes the cost of ownership. The cost of

ownership comprises of the interest, cost of maintenance, repairs and renovation, insurance,

rates and land tax (Bankman et al. 2017). Kylie later reported on 1st July 2009 relating to

costs incurred on renovating the apartment. Kylie incurred renovation cost of $15,000. The

cost of renovating the apartment falls under the third element of cost base under “section

110-25 of the ITAA 1997”. Therefore, the same is added into the cost base of the apartment.

The fourth element of cost base comprises of the capital enhancement and

preservation costs. This includes any form of capital expenditure such as improvement to the

asset that is incurred by the taxpayer in increasing the value of the asset that forms the part of

the fourth element of the cost base under “section 110-25 (5) of the ITAA 1997” (Schenk

2017). The fourth element of cost base includes the capital expenditure that is related to the

installation or moving the asset. Kylie later reports on 1st February 2009 an expenditure of

$40,000 related to addition of second bathroom in the apartment. The cost can be

characterised as improvement to the asset in the form of capital enhancement and falls under

the part of fourth element of cost base.

While arriving at the final settlement of the investment apartment Kylie reported legal

expenses and real estate commission. The expenses are considered as cost of selling and the

same is subtracted to ascertain the net selling price (Murphy and Higgins 2016). The selling

of investment apartment resulted in capital gains under “CGT event A1” and the net amount

of capital gains is included into the assessable income of Kylie.

Later Kylie granted a three month option of purchasing the rental property to local

property developer which eventually lapsed and resulted in receipt of $10,500. She incurred

4TAXATION LAW

the expense of $500 as the fees paid to solicitor for repairing the contract. Fees paid to the

solicitor for preparing the option contract can be treated as eligible deduction under the

“section 8-1 of the ITAA 1997” because it was incurred in the gaining the assessable income.

According to the “section 108-10 (2) of the ITAA 1997” collectables refers to the

artwork, an antique coin or medallion or a postage stamp that is mainly kept by the taxpayer

for their private usage and enjoyment purpose (Schmalbeck, Zelenak and Lawsky, 2015).

There are certain special rules that are applicable on collectables. The capital gains and

capital losses should be disregarded under “section 118-10 (1) of the ITAA 1997” when the

cost base of the collectable is less than $500. The quarantining rule under “section 108-10

(1)” states that capital loss from the collectables can be only used to offset the capital gains

from the collectables (Seto 2015). Kylie later reports capital gains from the sale of stamp

collection however she has the carry-forward loss of $5000 from the sale of coin. As a result

of this, Kylie under the quarantining rule of “section 108-10 (1)” can only offset the capital

loss that is made from the sale of antique coin.

Shares in company or units in the trust are considered in the similar manner as the

other assets for the purpose of capital gains tax. For an individual investors capital gains tax

is applied on the shares and units when they sell them originating from the CGT event

(Finkelstein 2014). In the current situation it is noticed that Kylie made a capital gains from

the shares of BHP however she had the carry forward loss of $20,000 from the shares during

the income year of 2008-. The gains made from the shares of BHP are offset against the carry

forward loss.

Kylie carried on the business of gymnasium that only made profit once in every ten

year however the gymnasium did not reported profit during the year 2017-18. The loss made

the expense of $500 as the fees paid to solicitor for repairing the contract. Fees paid to the

solicitor for preparing the option contract can be treated as eligible deduction under the

“section 8-1 of the ITAA 1997” because it was incurred in the gaining the assessable income.

According to the “section 108-10 (2) of the ITAA 1997” collectables refers to the

artwork, an antique coin or medallion or a postage stamp that is mainly kept by the taxpayer

for their private usage and enjoyment purpose (Schmalbeck, Zelenak and Lawsky, 2015).

There are certain special rules that are applicable on collectables. The capital gains and

capital losses should be disregarded under “section 118-10 (1) of the ITAA 1997” when the

cost base of the collectable is less than $500. The quarantining rule under “section 108-10

(1)” states that capital loss from the collectables can be only used to offset the capital gains

from the collectables (Seto 2015). Kylie later reports capital gains from the sale of stamp

collection however she has the carry-forward loss of $5000 from the sale of coin. As a result

of this, Kylie under the quarantining rule of “section 108-10 (1)” can only offset the capital

loss that is made from the sale of antique coin.

Shares in company or units in the trust are considered in the similar manner as the

other assets for the purpose of capital gains tax. For an individual investors capital gains tax

is applied on the shares and units when they sell them originating from the CGT event

(Finkelstein 2014). In the current situation it is noticed that Kylie made a capital gains from

the shares of BHP however she had the carry forward loss of $20,000 from the shares during

the income year of 2008-. The gains made from the shares of BHP are offset against the carry

forward loss.

Kylie carried on the business of gymnasium that only made profit once in every ten

year however the gymnasium did not reported profit during the year 2017-18. The loss made

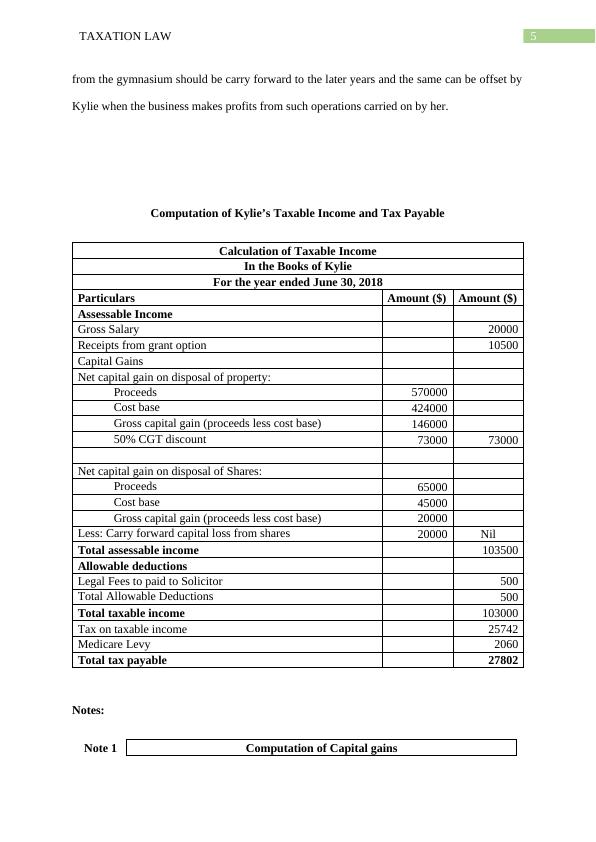

5TAXATION LAW

from the gymnasium should be carry forward to the later years and the same can be offset by

Kylie when the business makes profits from such operations carried on by her.

Computation of Kylie’s Taxable Income and Tax Payable

Calculation of Taxable Income

In the Books of Kylie

For the year ended June 30, 2018

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 20000

Receipts from grant option 10500

Capital Gains

Net capital gain on disposal of property:

Proceeds 570000

Cost base 424000

Gross capital gain (proceeds less cost base) 146000

50% CGT discount 73000 73000

Net capital gain on disposal of Shares:

Proceeds 65000

Cost base 45000

Gross capital gain (proceeds less cost base) 20000

Less: Carry forward capital loss from shares 20000 Nil

Total assessable income 103500

Allowable deductions

Legal Fees to paid to Solicitor 500

Total Allowable Deductions 500

Total taxable income 103000

Tax on taxable income 25742

Medicare Levy 2060

Total tax payable 27802

Notes:

Note 1 Computation of Capital gains

from the gymnasium should be carry forward to the later years and the same can be offset by

Kylie when the business makes profits from such operations carried on by her.

Computation of Kylie’s Taxable Income and Tax Payable

Calculation of Taxable Income

In the Books of Kylie

For the year ended June 30, 2018

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 20000

Receipts from grant option 10500

Capital Gains

Net capital gain on disposal of property:

Proceeds 570000

Cost base 424000

Gross capital gain (proceeds less cost base) 146000

50% CGT discount 73000 73000

Net capital gain on disposal of Shares:

Proceeds 65000

Cost base 45000

Gross capital gain (proceeds less cost base) 20000

Less: Carry forward capital loss from shares 20000 Nil

Total assessable income 103500

Allowable deductions

Legal Fees to paid to Solicitor 500

Total Allowable Deductions 500

Total taxable income 103000

Tax on taxable income 25742

Medicare Levy 2060

Total tax payable 27802

Notes:

Note 1 Computation of Capital gains

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Taxation Law | Assignment-3lg...

|12

|2579

|19

Taxationlg...

|8

|1656

|94

Taxation Law: CGT, Personal Exertion Income, and Interest on Loanlg...

|12

|2873

|89

TAXATION LAW. Taxation Law Name of the Student Name oflg...

|5

|470

|261

Taxation Lawlg...

|13

|2954

|1

Capital Gain Tax | Taxation Law | Assignmentlg...

|7

|1164

|20