Taxation Law Case Study: RIP Pty Ltd

VerifiedAdded on 2023/06/11

|12

|3467

|261

AI Summary

This case study discusses the tax treatment of various transactions of RIP Pty Ltd, a funeral director company in Australia. It covers the tax treatment of Easy Funeral Plan, Forfeited Payments Account, trading stock, fully franked dividends, rental space, long service leave, and construction expenditure. The case study uses relevant sections of the Income Tax Assessment Act 1936 and 1997 to provide advice on the tax treatment of each transaction.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW 1

Taxation Law

Student’s Name

Institutional Affiliation

Taxation Law

Student’s Name

Institutional Affiliation

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW 2

Taxation Law

Part A

Facts, Issues, and Conclusion

Facts

RIP Pty Ltd is a private corporation that is a resident of Australia and its primary business

is being a funeral director. In addition to the funeral premises, the company has office facilities, a

chapel, an assembly area, professional rooms and motor vehicles to be able to complete the

operations successfully. On June 2016, RIP Pty Ltd reported a net profit of $2.45m which came

from fees payable after thirty days, under insurance contracts, those received from RIP Finance

Pty Ltd and any amounts paid under a funeral plan which the clients are required to make

periodic contributions in order to be able to meet any funeral costs in the future. The company

has an ‘Easy Funeral Plan’ where the price is fixed and as soon as the money is paid, the client is

guaranteed a comfortable funeral arrangement upon his or her death. However, if the price is not

fully paid by the time the person passes away, the fees of the deceased would be payable under a

‘net 30 days’ invoice or under an insurance contract with the amount being non-refundable. By

the end of the financial year ended 30th June, RIP’s Easy Funeral Plan had a credit balance of

$225,000. Additionally, it is expected that the clients may die abroad, no funeral services may be

provided or their remains may not be recovered, thus amounts paid to the Easy Funeral Plan may

not be drawn upon which may cause refund issues.

Issue

The issue here is that by the end of 30th June, the firm transfers any amount from the Easy

Funeral Plan in connection with defaulting members. As at that date, the Forfeited Payments

Taxation Law

Part A

Facts, Issues, and Conclusion

Facts

RIP Pty Ltd is a private corporation that is a resident of Australia and its primary business

is being a funeral director. In addition to the funeral premises, the company has office facilities, a

chapel, an assembly area, professional rooms and motor vehicles to be able to complete the

operations successfully. On June 2016, RIP Pty Ltd reported a net profit of $2.45m which came

from fees payable after thirty days, under insurance contracts, those received from RIP Finance

Pty Ltd and any amounts paid under a funeral plan which the clients are required to make

periodic contributions in order to be able to meet any funeral costs in the future. The company

has an ‘Easy Funeral Plan’ where the price is fixed and as soon as the money is paid, the client is

guaranteed a comfortable funeral arrangement upon his or her death. However, if the price is not

fully paid by the time the person passes away, the fees of the deceased would be payable under a

‘net 30 days’ invoice or under an insurance contract with the amount being non-refundable. By

the end of the financial year ended 30th June, RIP’s Easy Funeral Plan had a credit balance of

$225,000. Additionally, it is expected that the clients may die abroad, no funeral services may be

provided or their remains may not be recovered, thus amounts paid to the Easy Funeral Plan may

not be drawn upon which may cause refund issues.

Issue

The issue here is that by the end of 30th June, the firm transfers any amount from the Easy

Funeral Plan in connection with defaulting members. As at that date, the Forfeited Payments

TAXATION LAW 3

Account had a credit balance of $16,200. The issue, here, is how the amount in the Forfeited

Payments Account should be treated for the purposes of taxation.

Conclusion

For this case study, the decision of Arthur Murray(NS) Pty Ltd V FCT (1965) 114 CLR

314 can be used. In this case study, Arthur Murray sold dancing lessons which were to be paid

for in the future. On assessing the taxpayer to determine whether this constituted assessable

income, the commissioner concluded that the amount was received in advance for services not

yet earned and thus it would not be liable to tax (Barkoczy, 2010, n.d.).

This case of Arthur Murray can be used to form a decision in this case study since the

company was providing funeral services after death and thus it applies to the accounting

treatment of amounts in the ‘Easy Funeral Plan’. However, there are some instances where the

client could contribute to an ‘Easy Funeral Plan’ to pay in advance for their funeral costs in

future. Ideally, by the financial year ended 30th June, the ‘Easy Funeral Plan’ had a credit balance

of $225,000. As seen in the decision made in Arthur Murray’s case, this amount received in

respect to the provision of funeral services has not yet been earned until future obligations for the

funeral has been discharged and therefore it is not liable to taxes (Barkoczy, 2010, n.d.). This

means that the amount of the ‘Easy Funeral Plan’ should not liable to taxes.

When RIP Pty Ltd derives its income generally other than funeral business, it would be

seen that the company is not carrying on its ordinary business activities and therefore any

amount realized from this would not be included in the taxable income. However, if the

corporation derives its income from its funeral services and related activities, this amount would

be considered to be from ordinary business activities, thus it would be included and thus liable to

taxes due to the fact that it is allowable for tax purposes (Barkoczy, 2010, n.d.). The

Account had a credit balance of $16,200. The issue, here, is how the amount in the Forfeited

Payments Account should be treated for the purposes of taxation.

Conclusion

For this case study, the decision of Arthur Murray(NS) Pty Ltd V FCT (1965) 114 CLR

314 can be used. In this case study, Arthur Murray sold dancing lessons which were to be paid

for in the future. On assessing the taxpayer to determine whether this constituted assessable

income, the commissioner concluded that the amount was received in advance for services not

yet earned and thus it would not be liable to tax (Barkoczy, 2010, n.d.).

This case of Arthur Murray can be used to form a decision in this case study since the

company was providing funeral services after death and thus it applies to the accounting

treatment of amounts in the ‘Easy Funeral Plan’. However, there are some instances where the

client could contribute to an ‘Easy Funeral Plan’ to pay in advance for their funeral costs in

future. Ideally, by the financial year ended 30th June, the ‘Easy Funeral Plan’ had a credit balance

of $225,000. As seen in the decision made in Arthur Murray’s case, this amount received in

respect to the provision of funeral services has not yet been earned until future obligations for the

funeral has been discharged and therefore it is not liable to taxes (Barkoczy, 2010, n.d.). This

means that the amount of the ‘Easy Funeral Plan’ should not liable to taxes.

When RIP Pty Ltd derives its income generally other than funeral business, it would be

seen that the company is not carrying on its ordinary business activities and therefore any

amount realized from this would not be included in the taxable income. However, if the

corporation derives its income from its funeral services and related activities, this amount would

be considered to be from ordinary business activities, thus it would be included and thus liable to

taxes due to the fact that it is allowable for tax purposes (Barkoczy, 2010, n.d.). The

TAXATION LAW 4

commissioner or any taxpayer does not have a choice in the method of accounting for tax since

the respective law must be followed when preparing the statement of taxable income of RIP Pty

Ltd. Another scenario may occur when the client dies abroad. In such a scenario, the amount in

the ‘Easy Funeral Plan’ of $225,000 should be included in the assessable income since it is

evident that the obligations for the funeral arrangements will be discharged (Barkoczy, 2010,

n.d.).

Advice on the Tax Treatment of $16,200 in the ‘Forfeitures Payments Account’

According to section 104-150 of the ITAA 1997, when a deposit is forfeited and a

taxpayer makes a capital gain, the capital gain would be the deposit less the deposit less any

expenses in relation to the sale. However, when the taxpayer makes a capital loss, the capital loss

would be computed as the expenditure in relation to the sale less the deposit forfeited. According

to taxation ruling 97/19 Para 7, a CGT provision applies to the effect that a forfeited deposit may

be considered as a capital gain in certain circumstances. In this case study, RIP Pty Ltd had

$16,200 in the ‘Forfeitures Payments Account’. This amount of $16200 that was paid by

defaulting members would be considered as a capital gain and thus it should be included in the

assessable income under sec 104 -150 of ITAA 1997and TR 97/19. Therefore, the capital gain

attributable to RIP Pty Ltd would be computed as the deposit by the members who defaulted

payment less any expenditure associated with the sale, that is, the funeral services. However,

since RIP Pty Ltd is not incurring any expenses for this amount, the capital gain would just be

the deposit by the defaulted members, that is, $16,200.

Part B

Part a

commissioner or any taxpayer does not have a choice in the method of accounting for tax since

the respective law must be followed when preparing the statement of taxable income of RIP Pty

Ltd. Another scenario may occur when the client dies abroad. In such a scenario, the amount in

the ‘Easy Funeral Plan’ of $225,000 should be included in the assessable income since it is

evident that the obligations for the funeral arrangements will be discharged (Barkoczy, 2010,

n.d.).

Advice on the Tax Treatment of $16,200 in the ‘Forfeitures Payments Account’

According to section 104-150 of the ITAA 1997, when a deposit is forfeited and a

taxpayer makes a capital gain, the capital gain would be the deposit less the deposit less any

expenses in relation to the sale. However, when the taxpayer makes a capital loss, the capital loss

would be computed as the expenditure in relation to the sale less the deposit forfeited. According

to taxation ruling 97/19 Para 7, a CGT provision applies to the effect that a forfeited deposit may

be considered as a capital gain in certain circumstances. In this case study, RIP Pty Ltd had

$16,200 in the ‘Forfeitures Payments Account’. This amount of $16200 that was paid by

defaulting members would be considered as a capital gain and thus it should be included in the

assessable income under sec 104 -150 of ITAA 1997and TR 97/19. Therefore, the capital gain

attributable to RIP Pty Ltd would be computed as the deposit by the members who defaulted

payment less any expenditure associated with the sale, that is, the funeral services. However,

since RIP Pty Ltd is not incurring any expenses for this amount, the capital gain would just be

the deposit by the defaulted members, that is, $16,200.

Part B

Part a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW 5

According to ITAA 1997 section 70-10(1), a trading stock is anything that has been

produced or acquired or the purpose of exchange, manufacture or sale in the ordinary course of

business. Section 70-10(2) of the ITAA 1997 states that a trading stock does not include CGT

asset or division 230 financial arrangement. RIP Pty Ltd had three types of caskets which the

company had prepaid for $25,000 in June 2016 that had to be delivered in August 2016. The

caskets and accessories would be considered to be trading stock since the items were acquired

for the purpose of sale. The $25,000 would be considered an expense from ordinary activities

and therefore it would be liable to taxes. Ideally, the accrual concept applies that is expenses

would be recorded when incurred and not when paid and therefore the $25,000 would be

incorporated when computing the taxable income of June 2016 (Handley and Maheswaran, 2008,

p.83). This is because has not yet been incurred since it has been paid in advance.

Part b

According to the Income Tax Assessment Act 1936 section 44-1, a shareholder’s

assessable income includes dividends derived out of profits and paid out to the shareholder and

any non-shared dividends that have been paid to the shareholder (resident); dividends paid to

shareholder by the firm from only the profits derived from Australia and non-shared dividends

derived from sources in Australia (non-resident); and those paid to the shareholder and they are

from a permanent establishment out of which profits are derived from sources outside Australia

and non-shared dividends attributable to a permanent establishment whose profits are derived

from sources outside Australia (shareholder is a non-resident that is carrying on a business within

Australia or through a permanent establishment in Australia. RIP Pty Ltd had fully franked cash

dividends amounting to $21,000 which was received from RIP Finance Pty Ltd (Handley and

Maheswaran, 2008, p.84). Since the fully franked dividends were received from a firm that is a

According to ITAA 1997 section 70-10(1), a trading stock is anything that has been

produced or acquired or the purpose of exchange, manufacture or sale in the ordinary course of

business. Section 70-10(2) of the ITAA 1997 states that a trading stock does not include CGT

asset or division 230 financial arrangement. RIP Pty Ltd had three types of caskets which the

company had prepaid for $25,000 in June 2016 that had to be delivered in August 2016. The

caskets and accessories would be considered to be trading stock since the items were acquired

for the purpose of sale. The $25,000 would be considered an expense from ordinary activities

and therefore it would be liable to taxes. Ideally, the accrual concept applies that is expenses

would be recorded when incurred and not when paid and therefore the $25,000 would be

incorporated when computing the taxable income of June 2016 (Handley and Maheswaran, 2008,

p.83). This is because has not yet been incurred since it has been paid in advance.

Part b

According to the Income Tax Assessment Act 1936 section 44-1, a shareholder’s

assessable income includes dividends derived out of profits and paid out to the shareholder and

any non-shared dividends that have been paid to the shareholder (resident); dividends paid to

shareholder by the firm from only the profits derived from Australia and non-shared dividends

derived from sources in Australia (non-resident); and those paid to the shareholder and they are

from a permanent establishment out of which profits are derived from sources outside Australia

and non-shared dividends attributable to a permanent establishment whose profits are derived

from sources outside Australia (shareholder is a non-resident that is carrying on a business within

Australia or through a permanent establishment in Australia. RIP Pty Ltd had fully franked cash

dividends amounting to $21,000 which was received from RIP Finance Pty Ltd (Handley and

Maheswaran, 2008, p.84). Since the fully franked dividends were received from a firm that is a

TAXATION LAW 6

resident of Australia, from the sources derived in Australia and from a permanent establishment

in Australia, the fully franked dividends of $21,000 would be liable to taxation which means that

they would be liable to taxes.

Part c

RIP Pty Ltd paid an amount of $57,000 on 1st March 2016 for two-years rental space

whose lease was to expire on 28th February 2018. Out of this, $9,500 was expensed to the

account while the remaining $47,500 was capitalized in the statement of financial position. The

question is what amount can be included in the statement of taxable income in order to determine

the assessable income. To answer this, one can look at the case of FC of T v. Krakos Investments

Pty Ltd. In this case, Krakos bought land to build a hotel and leased the hotel premises to another

party (lessee) after several years for $420,000 which was paid for goodwill as agreed by the two

parties. The Federal Court on basing their decision on whether this amount is liable to taxation

had to assess whether this amount was a premium payable or paid for the grant of the lease.

Ideally, a sum can be considered a premium if the amount paid is for the grant of the lease

whereas an amount would be considered rent if the consideration was paid for occupation and

the right of use (Kluwer, 1997, n.d.).

In this case study, a lease occurred between RIP Pty Ltd and another company. Here, RIP

Pty Ltd was the lessee while the other company was the lessor since the other corporation

transferred the right of use of the rented space to RIP Pty Ltd at a consideration to be paid at a

specific period. RIP Pty Ltd paid $57,000 for a rental space for a period of 2-years. This amount

was paid in advance for the whole period that RIP Pty Ltd was to use the rented space. However,

for that financial period, that is, from 1st June 2015 to 30th June 2016, the expense relating to the

rented space amounted to $9,500 while the remainder of $47,500 was capitalized to the balance

resident of Australia, from the sources derived in Australia and from a permanent establishment

in Australia, the fully franked dividends of $21,000 would be liable to taxation which means that

they would be liable to taxes.

Part c

RIP Pty Ltd paid an amount of $57,000 on 1st March 2016 for two-years rental space

whose lease was to expire on 28th February 2018. Out of this, $9,500 was expensed to the

account while the remaining $47,500 was capitalized in the statement of financial position. The

question is what amount can be included in the statement of taxable income in order to determine

the assessable income. To answer this, one can look at the case of FC of T v. Krakos Investments

Pty Ltd. In this case, Krakos bought land to build a hotel and leased the hotel premises to another

party (lessee) after several years for $420,000 which was paid for goodwill as agreed by the two

parties. The Federal Court on basing their decision on whether this amount is liable to taxation

had to assess whether this amount was a premium payable or paid for the grant of the lease.

Ideally, a sum can be considered a premium if the amount paid is for the grant of the lease

whereas an amount would be considered rent if the consideration was paid for occupation and

the right of use (Kluwer, 1997, n.d.).

In this case study, a lease occurred between RIP Pty Ltd and another company. Here, RIP

Pty Ltd was the lessee while the other company was the lessor since the other corporation

transferred the right of use of the rented space to RIP Pty Ltd at a consideration to be paid at a

specific period. RIP Pty Ltd paid $57,000 for a rental space for a period of 2-years. This amount

was paid in advance for the whole period that RIP Pty Ltd was to use the rented space. However,

for that financial period, that is, from 1st June 2015 to 30th June 2016, the expense relating to the

rented space amounted to $9,500 while the remainder of $47,500 was capitalized to the balance

TAXATION LAW 7

sheet in the fixed assets section (Kluwer, 1996, n.d.). When computing the assessable income of

RIP Pty Ltd, the amount of $9,500 was the expense for the year with respect to this rented space

and this, therefore, would be the only amount to be included in the statement of taxable income

for the company when ascertaining the assessable income for the year since it was the only

expense relating to the lease for that period. The other amount of $47,500 has been paid by RIP

Pty Ltd but it has not yet been incurred and therefore it is a prepayment. For this reason, it would

not be liable to taxes.

Part d

According to the Income Tax Assessment Act 1997 section 26-10(1), a long service leave

cannot be deducted from the assessable income except if it was paid in the year of income to the

person going on leave or if it was an accrued leave transfer payment is made in the year of

income. Additionally, section 26-10(2) of the ITAA 1997 states that this accrued payment is any

amount made by a corporation to a person’s leave and when the company is no longer required

to give that person leave pay and to another business when the other business has begun to be

required to make the payments in relation to that leave under the Australian Law (Woellner et al.,

2012, n.d.). According to section 15-5 of the ITAA 1997, the accrued leave transfer payment

must be liable to taxes.

The managing director of RIP Pty Ltd went on a long service leave for three months

where he was to be paid $22,000 in advance. This amount was debited in the accounts of the

business and a contra entry performed on the Provision for Long Service Leave Account. Since

this amount was paid in advance, it is prepaid and therefore it cannot be considered as an accrued

leave transfer payment which is liable to taxes as seen in section 15-5 in the Income Tax

Assessable Act 1997 (Handley and Maheswaran, 2008, p.85). Ideally, an accrual is something

sheet in the fixed assets section (Kluwer, 1996, n.d.). When computing the assessable income of

RIP Pty Ltd, the amount of $9,500 was the expense for the year with respect to this rented space

and this, therefore, would be the only amount to be included in the statement of taxable income

for the company when ascertaining the assessable income for the year since it was the only

expense relating to the lease for that period. The other amount of $47,500 has been paid by RIP

Pty Ltd but it has not yet been incurred and therefore it is a prepayment. For this reason, it would

not be liable to taxes.

Part d

According to the Income Tax Assessment Act 1997 section 26-10(1), a long service leave

cannot be deducted from the assessable income except if it was paid in the year of income to the

person going on leave or if it was an accrued leave transfer payment is made in the year of

income. Additionally, section 26-10(2) of the ITAA 1997 states that this accrued payment is any

amount made by a corporation to a person’s leave and when the company is no longer required

to give that person leave pay and to another business when the other business has begun to be

required to make the payments in relation to that leave under the Australian Law (Woellner et al.,

2012, n.d.). According to section 15-5 of the ITAA 1997, the accrued leave transfer payment

must be liable to taxes.

The managing director of RIP Pty Ltd went on a long service leave for three months

where he was to be paid $22,000 in advance. This amount was debited in the accounts of the

business and a contra entry performed on the Provision for Long Service Leave Account. Since

this amount was paid in advance, it is prepaid and therefore it cannot be considered as an accrued

leave transfer payment which is liable to taxes as seen in section 15-5 in the Income Tax

Assessable Act 1997 (Handley and Maheswaran, 2008, p.85). Ideally, an accrual is something

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW 8

that has been incurred continuously and has not yet been paid while a prepayment or something

paid in advance is an amount that has been paid but has not yet been incurred by the business.

Section 26-10(1) states that any long service leave cannot be deducted from the assessable

income except if it was paid to whom the leave relates to in the year of income or if it was an

accrued leave transfer payment. However, since this amount was paid in advance, then it does

not relate to the year of income and it cannot be considered as an accrued leave transfer payment.

This, therefore, means that the amount of $22,000 paid to the managing director for his or her

long service leave of three months shall be exempt from taxes. Thereby, the amount of $22,000

paid to the managing director for the long service leave is not liable to taxes and therefore it shall

not be liable to taxes and thus it shall not be included in the statement of taxable loss or income.

Part e

According to the ITAA 1997 division 43, a building can deduct construction costs in

relation to a building, extensions, improvements to the building, structural improvements,

improvements to the structural improvements and earthworks in relation to environmental

protection. According to section 43-70(1) of the ITAA 1997, a construction expenditure is any

capital expenditure in relation to the construction of capital works. Section 43-70(2) further

states that a construction expenditure does not include cost of acquiring the land on which the

structure is being built on, any expenses incurred in demolishing the existing structures, costs on

landscaping and plant, and expenditure for a property whose deduction is allowable such as

depreciating assets (subdivision 40-F), primary producers (subdivision 40-G) and expenditure

deductible over time since it has been capitalized (subdivision 40-I).

In this case study, the Board of Directors paid $250,000 for preliminary architectural

designs, they acquired land amounting to $1.25m and they incurred $50,000 to demolish an

that has been incurred continuously and has not yet been paid while a prepayment or something

paid in advance is an amount that has been paid but has not yet been incurred by the business.

Section 26-10(1) states that any long service leave cannot be deducted from the assessable

income except if it was paid to whom the leave relates to in the year of income or if it was an

accrued leave transfer payment. However, since this amount was paid in advance, then it does

not relate to the year of income and it cannot be considered as an accrued leave transfer payment.

This, therefore, means that the amount of $22,000 paid to the managing director for his or her

long service leave of three months shall be exempt from taxes. Thereby, the amount of $22,000

paid to the managing director for the long service leave is not liable to taxes and therefore it shall

not be liable to taxes and thus it shall not be included in the statement of taxable loss or income.

Part e

According to the ITAA 1997 division 43, a building can deduct construction costs in

relation to a building, extensions, improvements to the building, structural improvements,

improvements to the structural improvements and earthworks in relation to environmental

protection. According to section 43-70(1) of the ITAA 1997, a construction expenditure is any

capital expenditure in relation to the construction of capital works. Section 43-70(2) further

states that a construction expenditure does not include cost of acquiring the land on which the

structure is being built on, any expenses incurred in demolishing the existing structures, costs on

landscaping and plant, and expenditure for a property whose deduction is allowable such as

depreciating assets (subdivision 40-F), primary producers (subdivision 40-G) and expenditure

deductible over time since it has been capitalized (subdivision 40-I).

In this case study, the Board of Directors paid $250,000 for preliminary architectural

designs, they acquired land amounting to $1.25m and they incurred $50,000 to demolish an

TAXATION LAW 9

existing structure in 2013. In this year, only the amount of $250,000 incurred on the preliminary

architectural designs is allowable for tax purposes while the cost of land of $1.25 million and the

amount incurred to demolish an existing structure of $50,000 are disallowable. On September

2014, RIP Pty Ltd constructed the new premises at $2.5 million. This amount is allowable since

it consists capital expenditure in relation to the construction of the capital works. on 1st June

2015, the company installed fitting and equipment and began their operations in August 2015.

Furthermore, by September, an on-site car parking was completed at a cost of $125,000. The

fitting and equipment are excluded from taxes since they are grouped under depreciating assets

(subdivision 40-F). The on-site car parking, on the other hand, is liable to taxes since it is

considered as an extension to the building and therefore it must be included in the assessable

income. Lastly, by January 2016, RIP Pty Ltd had completed landscaping of the site at a cost of

$40,000. This amount is disallowable as seen in section 43-70(2) of the Income Tax Assessment

Act 1997. However, only the income for the year beginning 1st June 2015 to 30 June 2016 will be

included in the statement of taxable income since it is expected by the Australian standard that a

company computes the taxable income for the income year. For this part, all other amounts relate

to the prior income tax periods except the cost of landscaping of $40,000, fittings and equipment

purchased during the year and the on-site car parking cost of $125,000. Despite this, only the

cost of on-site car parking would be included in the statement of taxable income or loss when

determining the assessable income since the other expenditures are disallowable as seen in

section 43-70(2) of the ITAA 1997. Below is the computation of the assessable income of RIP

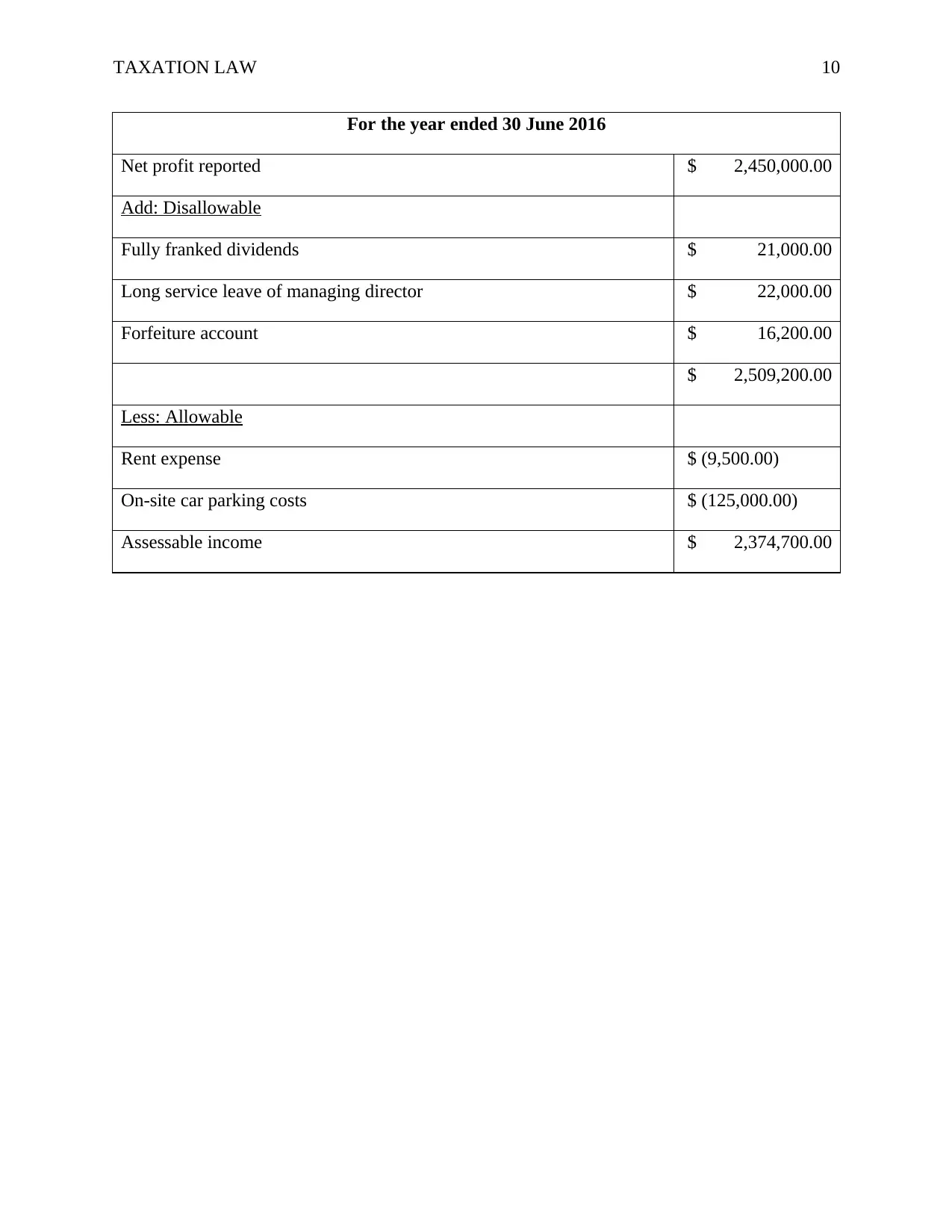

Pty Ltd.

RIP Pty Ltd

Statement of taxable income

existing structure in 2013. In this year, only the amount of $250,000 incurred on the preliminary

architectural designs is allowable for tax purposes while the cost of land of $1.25 million and the

amount incurred to demolish an existing structure of $50,000 are disallowable. On September

2014, RIP Pty Ltd constructed the new premises at $2.5 million. This amount is allowable since

it consists capital expenditure in relation to the construction of the capital works. on 1st June

2015, the company installed fitting and equipment and began their operations in August 2015.

Furthermore, by September, an on-site car parking was completed at a cost of $125,000. The

fitting and equipment are excluded from taxes since they are grouped under depreciating assets

(subdivision 40-F). The on-site car parking, on the other hand, is liable to taxes since it is

considered as an extension to the building and therefore it must be included in the assessable

income. Lastly, by January 2016, RIP Pty Ltd had completed landscaping of the site at a cost of

$40,000. This amount is disallowable as seen in section 43-70(2) of the Income Tax Assessment

Act 1997. However, only the income for the year beginning 1st June 2015 to 30 June 2016 will be

included in the statement of taxable income since it is expected by the Australian standard that a

company computes the taxable income for the income year. For this part, all other amounts relate

to the prior income tax periods except the cost of landscaping of $40,000, fittings and equipment

purchased during the year and the on-site car parking cost of $125,000. Despite this, only the

cost of on-site car parking would be included in the statement of taxable income or loss when

determining the assessable income since the other expenditures are disallowable as seen in

section 43-70(2) of the ITAA 1997. Below is the computation of the assessable income of RIP

Pty Ltd.

RIP Pty Ltd

Statement of taxable income

TAXATION LAW 10

For the year ended 30 June 2016

Net profit reported $ 2,450,000.00

Add: Disallowable

Fully franked dividends $ 21,000.00

Long service leave of managing director $ 22,000.00

Forfeiture account $ 16,200.00

$ 2,509,200.00

Less: Allowable

Rent expense $ (9,500.00)

On-site car parking costs $ (125,000.00)

Assessable income $ 2,374,700.00

For the year ended 30 June 2016

Net profit reported $ 2,450,000.00

Add: Disallowable

Fully franked dividends $ 21,000.00

Long service leave of managing director $ 22,000.00

Forfeiture account $ 16,200.00

$ 2,509,200.00

Less: Allowable

Rent expense $ (9,500.00)

On-site car parking costs $ (125,000.00)

Assessable income $ 2,374,700.00

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW 11

References

Barkoczy, S., 2010. Australian tax casebook. CCH Australia Limited. [Accessed on 29th May

2018].

Handley, J. C., and Maheswaran, K., 2008, A measure of the efficacy of the Australian

imputation tax system. Economic Record, 84(264), 82-94. [Accessed on 29th May 2018].

Income Tax Assessment Act 1997-Sect 104-150: Summary of the CGT Events. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sec 70-10: Meaning of Trading Stock. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s70.10.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1936-Sect 44-1: Dividends. Commonwealth Consolidation Acts.

[Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s44.html [Accessed on

29th May 2018].

Income Tax Assessment Act 1997-Sect 26-10: Leave Payments. Commonwealth Consolidation

Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s26.10.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sect 43.20: Capital Works to Division 43. Commonwealth

Consolidation Acts. [Online]. Available at

References

Barkoczy, S., 2010. Australian tax casebook. CCH Australia Limited. [Accessed on 29th May

2018].

Handley, J. C., and Maheswaran, K., 2008, A measure of the efficacy of the Australian

imputation tax system. Economic Record, 84(264), 82-94. [Accessed on 29th May 2018].

Income Tax Assessment Act 1997-Sect 104-150: Summary of the CGT Events. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sec 70-10: Meaning of Trading Stock. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s70.10.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1936-Sect 44-1: Dividends. Commonwealth Consolidation Acts.

[Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s44.html [Accessed on

29th May 2018].

Income Tax Assessment Act 1997-Sect 26-10: Leave Payments. Commonwealth Consolidation

Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s26.10.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sect 43.20: Capital Works to Division 43. Commonwealth

Consolidation Acts. [Online]. Available at

TAXATION LAW 12

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s43.20.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sect 15-5: General Interest Charge. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s5.15.html [Accessed on

29th May 2018].

Kluwer, W., 1996, FC of T v. Krakos Investments Pty Ltd 96 ATC 4063; (1995) 133 ALR 545.

CCH iKnow. [Online]. Available at

https://iknow.cch.com.au/document/atagUio540142sl16721306/fc-of-t-v-krakos-

investments-pty-ltd-federal-court-of-australia-full-court-19-december-1995 [Accessed

on 29th May 2018].

Kluwer, W., 1997, Income Tax Assessment Act 1997-Sect 43-70: Construction Expenditure.

CCH iKnow. [Online]. Available at

https://iknow.cch.com.au/document/atagUio695356sl24359645/income-tax-assessment-

act-1997-section-43-70-what-is-construction-expenditure [Accessed on 29th May 2018].

TR 97/19, 1997, Income Tax: Taxation Ruling, para 7. [Online]. Available at

http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR9719/NAT/ATO%27

[Accessed on 29th May 2018].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2012. Australian taxation law.

CCH Australia. [Accessed on 29th May 2018].

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s43.20.html [Accessed

on 29th May 2018].

Income Tax Assessment Act 1997-Sect 15-5: General Interest Charge. Commonwealth

Consolidation Acts. [Online]. Available at

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s5.15.html [Accessed on

29th May 2018].

Kluwer, W., 1996, FC of T v. Krakos Investments Pty Ltd 96 ATC 4063; (1995) 133 ALR 545.

CCH iKnow. [Online]. Available at

https://iknow.cch.com.au/document/atagUio540142sl16721306/fc-of-t-v-krakos-

investments-pty-ltd-federal-court-of-australia-full-court-19-december-1995 [Accessed

on 29th May 2018].

Kluwer, W., 1997, Income Tax Assessment Act 1997-Sect 43-70: Construction Expenditure.

CCH iKnow. [Online]. Available at

https://iknow.cch.com.au/document/atagUio695356sl24359645/income-tax-assessment-

act-1997-section-43-70-what-is-construction-expenditure [Accessed on 29th May 2018].

TR 97/19, 1997, Income Tax: Taxation Ruling, para 7. [Online]. Available at

http://law.ato.gov.au/atolaw/view.htm?locid=%27TXR/TR9719/NAT/ATO%27

[Accessed on 29th May 2018].

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2012. Australian taxation law.

CCH Australia. [Accessed on 29th May 2018].

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.