Case Study on Taxation Law: Income, Deductions, and Residency Status

VerifiedAdded on 2023/06/12

|12

|2204

|258

Case Study

AI Summary

This assignment presents a comprehensive case study on taxation law, divided into two parts. The first part involves calculating Dale's taxable income, considering cash receipts, trading stock, wages, rent, and other business expenses. It applies Section 8-1 of the Income Tax Assessment Act 1997 (ITAA 1997) to determine allowable deductions for expenses like lease renewal, superannuation guarantee, telephone, electricity, and insurance. The analysis also addresses the Medicare levy and provides a final calculation of net tax payable. The second part focuses on determining Amity's residency status for tax purposes, examining the Domicile Test, 183 days' test, Ordinary Concept Test, and Superannuation Test. It references relevant case law, such as Applegate v Federal Commissioner of Taxation (1979), to conclude whether Amity is considered an Australian resident under the ITAA 1936 and Domicile Act 1982.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................6

Domicile Test:........................................................................................................................6

183 days’ test:........................................................................................................................7

Resident according to Ordinary Concept Test:......................................................................8

Superannuation Test:..............................................................................................................8

Reference List:.........................................................................................................................10

Table of Contents

Answer to Part 1:........................................................................................................................2

Answer to Part 2:........................................................................................................................6

Domicile Test:........................................................................................................................6

183 days’ test:........................................................................................................................7

Resident according to Ordinary Concept Test:......................................................................8

Superannuation Test:..............................................................................................................8

Reference List:.........................................................................................................................10

2TAXATION LAW

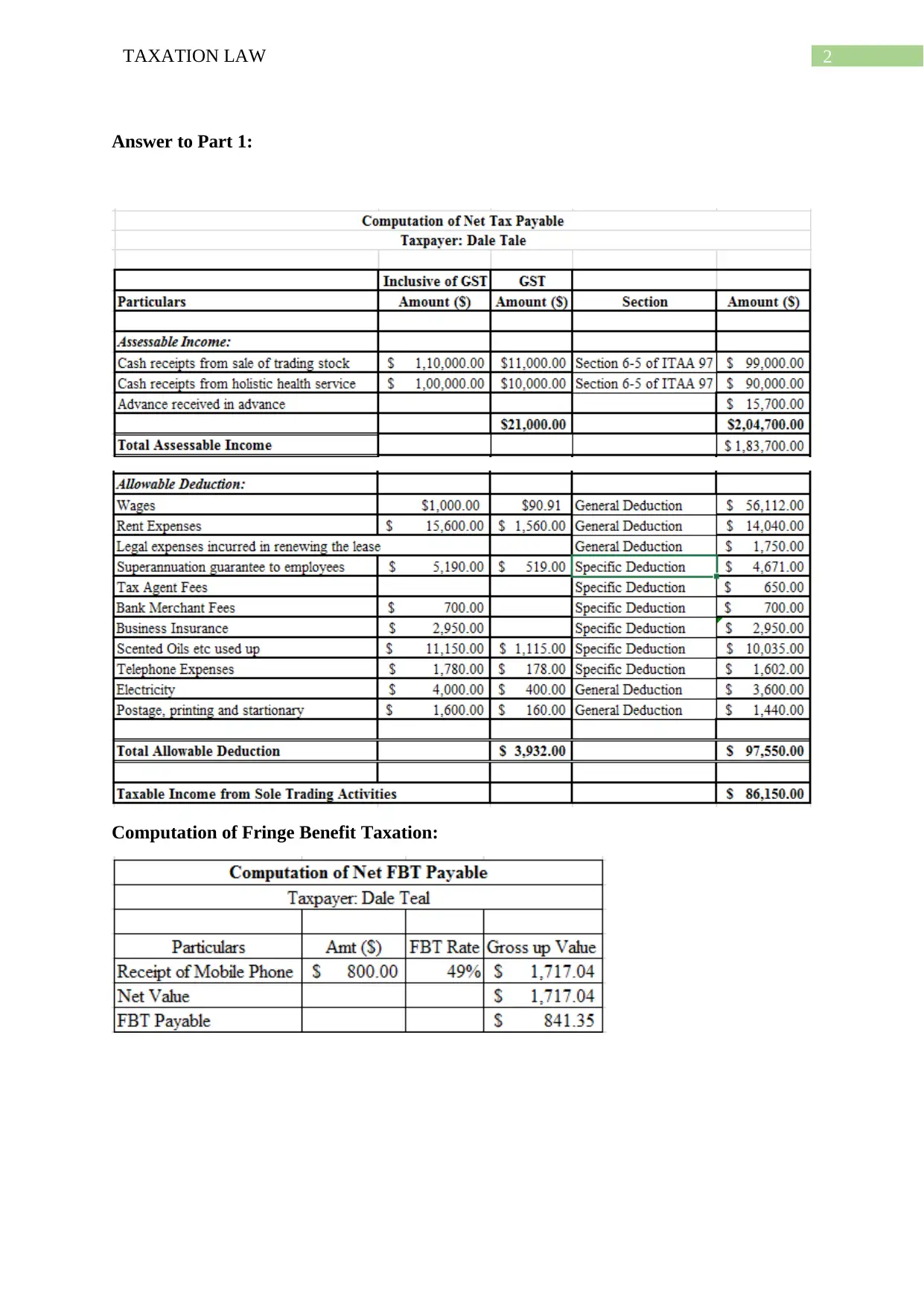

Answer to Part 1:

Computation of Fringe Benefit Taxation:

Answer to Part 1:

Computation of Fringe Benefit Taxation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

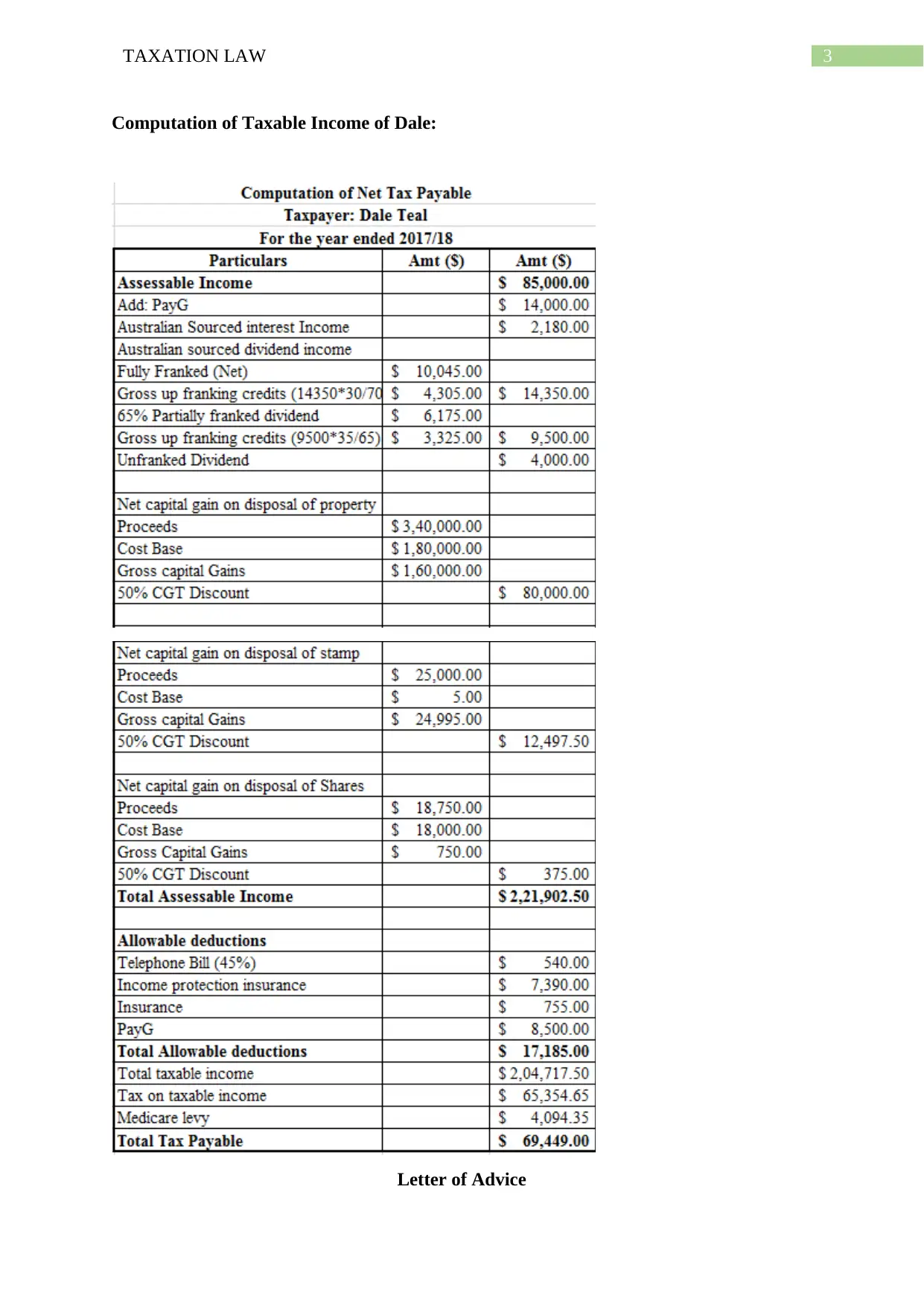

Computation of Taxable Income of Dale:

Letter of Advice

Computation of Taxable Income of Dale:

Letter of Advice

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

To Mr Dale

Respected Sir

I would like to draw your kind attention towards the letter of advice that is concerned

on your net taxable income from your business stands $86,150. Agreeing with “section 8-1

of the Income Tax Assessment Act 1997” you shall be allowed to make entitlement for an

specific deduction for the total sum of $97,550 that is incurred by you during the course of

your business. Expenditure relating to the renewal of lease and superannuation guarantee

provided to employee will be accounted as the permissible general deductions under “section

8-1 of the ITAA 1997” (Woellner et al., 2016). You will be able to deduct from your taxable

earnings any loss or outgoing till the level that the expenses that is suffered by you is having

direct association in producing the assessable income.

Further recommendations can be stated down in respect of the expenses such as

telephone, electricity and stationary charges. These expenses constitute administrative

business expenditure and you can claim an allowable general deductions for the same. These

expenses are characterised as outgoings that is necessarily incurred under positive limbs for

execution of business activities for deriving taxable earnings. Referring to the case of

“Ronpibon Tin NL v Federal Commissioner of Taxation (1979)” expenditure that are

satisfying the test of incidental and relevant is allowable for deductions (Barkoczy, 2016).

Instances obtained from the list of expenditure provided by you also constitute insurance

expenditure that is paid by you for income protection disability. Your insurance expenditure

would be entitled specific deduction with respect to the provision of ITAA 1997.

Referring to the decision of tax commissioner in “High Court in FCT v D.P Smith

81 ATC 4114” the income protection disability expenditure can be regarded for deductions

(Tan et al., 2016). There are expenditure such as wages and rental expenditure of $1,000 and

To Mr Dale

Respected Sir

I would like to draw your kind attention towards the letter of advice that is concerned

on your net taxable income from your business stands $86,150. Agreeing with “section 8-1

of the Income Tax Assessment Act 1997” you shall be allowed to make entitlement for an

specific deduction for the total sum of $97,550 that is incurred by you during the course of

your business. Expenditure relating to the renewal of lease and superannuation guarantee

provided to employee will be accounted as the permissible general deductions under “section

8-1 of the ITAA 1997” (Woellner et al., 2016). You will be able to deduct from your taxable

earnings any loss or outgoing till the level that the expenses that is suffered by you is having

direct association in producing the assessable income.

Further recommendations can be stated down in respect of the expenses such as

telephone, electricity and stationary charges. These expenses constitute administrative

business expenditure and you can claim an allowable general deductions for the same. These

expenses are characterised as outgoings that is necessarily incurred under positive limbs for

execution of business activities for deriving taxable earnings. Referring to the case of

“Ronpibon Tin NL v Federal Commissioner of Taxation (1979)” expenditure that are

satisfying the test of incidental and relevant is allowable for deductions (Barkoczy, 2016).

Instances obtained from the list of expenditure provided by you also constitute insurance

expenditure that is paid by you for income protection disability. Your insurance expenditure

would be entitled specific deduction with respect to the provision of ITAA 1997.

Referring to the decision of tax commissioner in “High Court in FCT v D.P Smith

81 ATC 4114” the income protection disability expenditure can be regarded for deductions

(Tan et al., 2016). There are expenditure such as wages and rental expenditure of $1,000 and

5TAXATION LAW

15,600 respectively. These expenditure is allowed for general deductions under “section 8-1

of the ITAA 1997” they satisfy the criteria of positive limbs and it is incidental to the

business (Cao et al., 2015). You further reported expeditor on tax agent fees and bank

merchant fees. Presumably the expenditure constitute a part of business expenditure that is

incurred in producing the taxable income. Therefore, with respect to “section 8-1 of the

ITAA 1997” you will be allowed to claim an allowable deductions for the tax agent fess and

bank merchant fees.

After considering all the relevant income and transactions reported by you total

amount of tax that would be payable by you stands $19545.75. You shall also be entitled to

Medicare levy of 2% on your taxable income. Therefore the Medicare levy stands $1723 on

your total reportable taxable income. The total amount of net tax that is payable by you

following the considerations of the necessary items reported and after taking note of the

relevant deductions under “section 8-1 of the ITAA 1997” stands $68,327.25.

I hope that the above stated recommendations that has been provided would be

helpful in lowering the tax liability and hope that the recommendations provided has served

as the useful tool to you.

Thank You

15,600 respectively. These expenditure is allowed for general deductions under “section 8-1

of the ITAA 1997” they satisfy the criteria of positive limbs and it is incidental to the

business (Cao et al., 2015). You further reported expeditor on tax agent fees and bank

merchant fees. Presumably the expenditure constitute a part of business expenditure that is

incurred in producing the taxable income. Therefore, with respect to “section 8-1 of the

ITAA 1997” you will be allowed to claim an allowable deductions for the tax agent fess and

bank merchant fees.

After considering all the relevant income and transactions reported by you total

amount of tax that would be payable by you stands $19545.75. You shall also be entitled to

Medicare levy of 2% on your taxable income. Therefore the Medicare levy stands $1723 on

your total reportable taxable income. The total amount of net tax that is payable by you

following the considerations of the necessary items reported and after taking note of the

relevant deductions under “section 8-1 of the ITAA 1997” stands $68,327.25.

I hope that the above stated recommendations that has been provided would be

helpful in lowering the tax liability and hope that the recommendations provided has served

as the useful tool to you.

Thank You

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Answer to Part 2:

The present issue is based on determining whether Amity would be considered as the

Australian occupant for assessment for the income year ended 30 June 2017?

Domicile Test:

The residence is of an individual is determined under the “Domicile Act 1982”. A

person would be considered as the Australian occupant if the person has maintained their

domicile in Australia if the officer is content that the individual’s perpetual place of residence

is outside of Australia.

The taxation ruling of IT 2650 is concerned with providing course of action in

defining whether the individual would who leaves Australia to reside in foreign nation for a

provisional foreign work project ceases to be an Australian resident for income tax purpose

(Braithwaite, 2017). “Subsection 6 (1) of the ITAA 1936” outlines a person to be Australian

occupant if the individual has the residence in Australia except it is contented by the tax

officer that the person has the perpetual place of residence outside of Australia. As evident in

the current case study of Emity, being an Australian resident she undertook the decision of

moving to Kiribati and determined to reside in Australia for a period of two years. As evident

in the current case study of Emity in spite of moving to Kiribati she maintained her home in

Australia however she does not intend to establish home permanently out of Australia.

The projected and the genuine span of stay of a person outside Australia in the abroad

nation is vital. The length and the continuousness of a person’s existence in the abroad nation

along with the permanency of the association that a person has with a specific place of abode

in Australia (Davis et al., 2015). Similarly, in the case of Emity in spite of being away from

Australia she maintained her domicile in Australia. The taxpayer Emity did not established

home outside Australia neither did she abandoned any of her home or place of residence that

Answer to Part 2:

The present issue is based on determining whether Amity would be considered as the

Australian occupant for assessment for the income year ended 30 June 2017?

Domicile Test:

The residence is of an individual is determined under the “Domicile Act 1982”. A

person would be considered as the Australian occupant if the person has maintained their

domicile in Australia if the officer is content that the individual’s perpetual place of residence

is outside of Australia.

The taxation ruling of IT 2650 is concerned with providing course of action in

defining whether the individual would who leaves Australia to reside in foreign nation for a

provisional foreign work project ceases to be an Australian resident for income tax purpose

(Braithwaite, 2017). “Subsection 6 (1) of the ITAA 1936” outlines a person to be Australian

occupant if the individual has the residence in Australia except it is contented by the tax

officer that the person has the perpetual place of residence outside of Australia. As evident in

the current case study of Emity, being an Australian resident she undertook the decision of

moving to Kiribati and determined to reside in Australia for a period of two years. As evident

in the current case study of Emity in spite of moving to Kiribati she maintained her home in

Australia however she does not intend to establish home permanently out of Australia.

The projected and the genuine span of stay of a person outside Australia in the abroad

nation is vital. The length and the continuousness of a person’s existence in the abroad nation

along with the permanency of the association that a person has with a specific place of abode

in Australia (Davis et al., 2015). Similarly, in the case of Emity in spite of being away from

Australia she maintained her domicile in Australia. The taxpayer Emity did not established

home outside Australia neither did she abandoned any of her home or place of residence that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

she held in Australia. Referring to the case of “Applegate v Federal Commissioner of

Taxation (1979)” the federal court viewed whether the taxpayer perpetual place of residence

was outside of Australia (Saad, 2014). Additionally, the federal commissioner also stated that

the permanent does not constitute perpetual or endlessly and the same is assessed based on

the objectivity of each year.

The court of law has stated that each year of income should be looked upon

separately. In the current case of Amity in important subject is that whether the taxpayer has

abandoned any place of residence that she held in Australia. Amity in the current case has not

abandoned her place of residence (Miller & Oats, 2016). With respect to “subsection 6 (1) of

the ITAA 1997” she would be viewed as the Australian resident because the actual and the

intended length of stay in Kiribati was 18 months and conclusively her permanent place of

abode in Australia. As per domicile act 1982 Emity would be considered as the Resident of

Australia since she has met the criteria of Domicile Test.

183 days’ test:

The 183 days’ test defines that a person who is a resident of Australia and has been

existent in Australia for either continuously or in breakdowns for more six months of the

income year would be considered as the Australia resident (Middleton, 2015). However, an

exception to this case is that if person would not be viewed as the Australian occupant if the

tax officer is satisfied that the persons permanent place of abode is outside of Australia and

does not intends to take up the residency in Australia.

As evident in the current case of Emity she has remained outside of Australia during

the year 2016 and only returned in 2017. Therefore, she has been outside of Australia from

2016 till July 2017. She would not be considered as the Australian resident under the 183

days’ test since she and her husband were not present in Australia. However, despite the

she held in Australia. Referring to the case of “Applegate v Federal Commissioner of

Taxation (1979)” the federal court viewed whether the taxpayer perpetual place of residence

was outside of Australia (Saad, 2014). Additionally, the federal commissioner also stated that

the permanent does not constitute perpetual or endlessly and the same is assessed based on

the objectivity of each year.

The court of law has stated that each year of income should be looked upon

separately. In the current case of Amity in important subject is that whether the taxpayer has

abandoned any place of residence that she held in Australia. Amity in the current case has not

abandoned her place of residence (Miller & Oats, 2016). With respect to “subsection 6 (1) of

the ITAA 1997” she would be viewed as the Australian resident because the actual and the

intended length of stay in Kiribati was 18 months and conclusively her permanent place of

abode in Australia. As per domicile act 1982 Emity would be considered as the Resident of

Australia since she has met the criteria of Domicile Test.

183 days’ test:

The 183 days’ test defines that a person who is a resident of Australia and has been

existent in Australia for either continuously or in breakdowns for more six months of the

income year would be considered as the Australia resident (Middleton, 2015). However, an

exception to this case is that if person would not be viewed as the Australian occupant if the

tax officer is satisfied that the persons permanent place of abode is outside of Australia and

does not intends to take up the residency in Australia.

As evident in the current case of Emity she has remained outside of Australia during

the year 2016 and only returned in 2017. Therefore, she has been outside of Australia from

2016 till July 2017. She would not be considered as the Australian resident under the 183

days’ test since she and her husband were not present in Australia. However, despite the

8TAXATION LAW

absence of Emity from Australia she has maintained her domicile in Australia following her

return to Australia. Referring to the verdict of “Applegate v Federal Commissioner of

Taxation (1979)” she is said to have constructive resident of Australia (Robin & Barkoczy,

2018).

Resident according to Ordinary Concept Test:

The ordinary concepts test is regarded as the primary test in ascertain the residential

status of an individual. In the current context of Emily and her husband the ordinary concept

test has been applied to determine the residential status (Blakelock & King, 2017). The

ordinary concept test is applied since Emity has been resident of Australia. Referring to the

case of “Federal Commissioner of Taxation v Miller (1946)” the history of presence and

nationality for Emity is considered to be an Australian. Therefore, this forms the fact and

degree in ascertaining her physical presence in Australia.

Emity did not permanently establish home in Kiribati and did not resided in Australia

permanently. Despite the fact that she was physically present in Kiribati however the

temporary nature of stay for Emity cannot be considered sufficient to determine that her

permanent place of residence was outside Australia. As a result of this, Emity under the

ordinary concept test will be considered as the Australian occupant since she has satisfied the

conditions of Resident according to the ordinary concept.

Superannuation Test:

A person under the commonwealth superannuation fund constitute a person that are

eligible employee of the government and is sent aboard to carry-out the government related

work (Fry, 2017). The superannuation test is usually applicable to the commonwealth public

servants generally the overseas diplomats residing abroad. Similarly, in the current case of

absence of Emity from Australia she has maintained her domicile in Australia following her

return to Australia. Referring to the verdict of “Applegate v Federal Commissioner of

Taxation (1979)” she is said to have constructive resident of Australia (Robin & Barkoczy,

2018).

Resident according to Ordinary Concept Test:

The ordinary concepts test is regarded as the primary test in ascertain the residential

status of an individual. In the current context of Emily and her husband the ordinary concept

test has been applied to determine the residential status (Blakelock & King, 2017). The

ordinary concept test is applied since Emity has been resident of Australia. Referring to the

case of “Federal Commissioner of Taxation v Miller (1946)” the history of presence and

nationality for Emity is considered to be an Australian. Therefore, this forms the fact and

degree in ascertaining her physical presence in Australia.

Emity did not permanently establish home in Kiribati and did not resided in Australia

permanently. Despite the fact that she was physically present in Kiribati however the

temporary nature of stay for Emity cannot be considered sufficient to determine that her

permanent place of residence was outside Australia. As a result of this, Emity under the

ordinary concept test will be considered as the Australian occupant since she has satisfied the

conditions of Resident according to the ordinary concept.

Superannuation Test:

A person under the commonwealth superannuation fund constitute a person that are

eligible employee of the government and is sent aboard to carry-out the government related

work (Fry, 2017). The superannuation test is usually applicable to the commonwealth public

servants generally the overseas diplomats residing abroad. Similarly, in the current case of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Emity she is not a government employee therefore the superannuation test would not be

applicable on Emity.

On a conclusive Emily would be regarded as the Australian resident under the

Domcile test since she has met the criteria set under the provision of “Domcile Act 1982”.

Emity she is not a government employee therefore the superannuation test would not be

applicable on Emity.

On a conclusive Emily would be regarded as the Australian resident under the

Domcile test since she has met the criteria set under the provision of “Domcile Act 1982”.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

Reference List:

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The accounting review, 91(1), 47-68.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and

Securities Law Journal, 33, 555-580.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET AL.).

(2018). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

Reference List:

Barkoczy, S. (2016). Foundations of taxation law 2016. OUP Catalogue.

Blakelock, S., & King, P. (2017). Taxation law: The advance of ATO data

matching. Proctor, The, 37(6), 18.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., ... & Wende, S.

(2015). Understanding the economy-wide efficiency and incidence of major

Australian taxes. Canberra: Treasury working paper, 2001.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The accounting review, 91(1), 47-68.

Fry, M. (2017). Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the

Australian Taxation Office. The APPEA Journal, 57(1), 49-63.

Middleton, T. (2015). Banning, disqualification and licensing powers: ACCC, APRA, ASIC

and the ATO–regulatory overlap, penalty privilege and law reform. Company and

Securities Law Journal, 33, 555-580.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET AL.).

(2018). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press.

Saad, N. (2014). Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, 1069-1075.

11TAXATION LAW

Tan, L. M., Braithwaite, V., & Reinhart, M. (2016). Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice. International

Small Business Journal, 34(3), 329-344.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

Tan, L. M., Braithwaite, V., & Reinhart, M. (2016). Why do small business taxpayers stay

with their practitioners? Trust, competence and aggressive advice. International

Small Business Journal, 34(3), 329-344.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C., & Pinto, D. (2016). Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

![Taxation Law: Spriggs v Federal Commissioner of Taxation [2007]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fdocument%2Fpages%2Fspriggs-taxation-law-case-page-2.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.