Taxation Law: Determining Taxable Income and Deductible Expenses

VerifiedAdded on 2023/06/15

|15

|3543

|180

Report

AI Summary

This report provides a detailed analysis of taxation law, focusing on the determination of ordinary income under Section 6-5 of the ITAA 1997 and allowable deductions under Section 8-1 of the ITAA 1997. It addresses issues related to taxable income derived from personal exertion and allowable deductions for expenses incurred during the income year. The analysis includes references to relevant case laws such as Dean v FCT (1997), Stone v Federal Commissioner of Taxation (2005), FCT v Brent (1971), and Harris v FCT (1980). The report also examines the deductibility of various expenses for Bags Co Ltd, including education, travel, conference, and equipment costs, referencing taxation rulings and court cases like FCT v Ronpibon Tin NL (1949) and Magna Alloys & Research Pty Ltd (1980). The report concludes by assessing the tax implications of different income sources and expenses, providing a comprehensive overview of the relevant taxation principles.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1..................................................................................................................2

Heading:.....................................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................8

Answer to question 2:.................................................................................................................8

Heading:.....................................................................................................................................8

Issues:.........................................................................................................................................8

Rule:...........................................................................................................................................8

Application:..............................................................................................................................10

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................14

Table of Contents

Answer to question 1..................................................................................................................2

Heading:.....................................................................................................................................2

Issues:.........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................8

Answer to question 2:.................................................................................................................8

Heading:.....................................................................................................................................8

Issues:.........................................................................................................................................8

Rule:...........................................................................................................................................8

Application:..............................................................................................................................10

Conclusion:..............................................................................................................................13

Reference List:.........................................................................................................................14

2TAXATION LAW

Answer to question 1

Heading:

The problem here is based on the determination of the ordinary income under the

provision stated under the “section 6-5 of the ITAA 1997”. The problem statement also deals

with the expenses that are allowable as deductions under “section 8-1 of the ITAA 1997”1.

Issues:

The issue to the case study of Kate revolves around the ascertainment of taxable

income derived from personal exertion and allowable deductions that can be claimed for

expenses occurred during the income year under “section 8-1”.

Rule:

“Section 6-5 of the ITAA 1997” is concerned with the income that derived by an

individual taxpayer from the personal exertion or in other words income that is obtained from

personal exertion2. The earnings include of salaries, wages and receipt of gratuity relating to

the services provided in the capacity of employee denotes income from personal exertion

under ordinary or statutory conceptsAs held in the case of “Dean v FCT (1997)” the

retention payment that is made to the employee to continue the employment services for a

period of 12 months after takeover will be held as income.

A person that receives money from prize for participating in an activity will not be

considered as income under the statutory and ordinary concepts. However, winning from

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Annette Morgan, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013).

Answer to question 1

Heading:

The problem here is based on the determination of the ordinary income under the

provision stated under the “section 6-5 of the ITAA 1997”. The problem statement also deals

with the expenses that are allowable as deductions under “section 8-1 of the ITAA 1997”1.

Issues:

The issue to the case study of Kate revolves around the ascertainment of taxable

income derived from personal exertion and allowable deductions that can be claimed for

expenses occurred during the income year under “section 8-1”.

Rule:

“Section 6-5 of the ITAA 1997” is concerned with the income that derived by an

individual taxpayer from the personal exertion or in other words income that is obtained from

personal exertion2. The earnings include of salaries, wages and receipt of gratuity relating to

the services provided in the capacity of employee denotes income from personal exertion

under ordinary or statutory conceptsAs held in the case of “Dean v FCT (1997)” the

retention payment that is made to the employee to continue the employment services for a

period of 12 months after takeover will be held as income.

A person that receives money from prize for participating in an activity will not be

considered as income under the statutory and ordinary concepts. However, winning from

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Annette Morgan, Colleen Mortimer and Dale Pinto, A Practical Introduction To Australian

Taxation Law (CCH Australia, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

prize money will be held as taxable income given that the money received from prize money

forms the part of taxpayer’s income earning activity. According to the judgement of the court

in the case of “Stone v Federal Commissioner of Taxation (2005)” where the taxpayer was

policeman and javelin thrower. The taxpayer made derived income from salary and also

received sum from endorsement and prize money3. The court held the taxpayer to be carrying

on the business of the professional athlete and the earnings derived was held as taxable

income.

There should be an appropriate association between the receipt and the provision of

services rendered which is the ordinary incident of the provision of services. According to the

judgement of the court in the case of “FCT v Brent (1971)” where the wife of the train

robber was granted an exclusive right by the media company to publish her life story. The

court held that payment received by wife of train robber was the reward for service and will

be regarded as income from personal exertion.

A mere windfall gain could not be characterised as the income. For instance, an

individual receiving money from gambling winnings cannot be held as income except for the

circumstances where the person is carrying on the business of gambling. The court of law in

the case of “Harris v FCT (1980)” has distinguished windfall amount that are received

unexpectedly or infrequently.

A mere prize is not characterized as income. The court of law referring to the

legislation passed in the circumstance of “Moore v Griffiths (1972)” held that mere winning

from prizes was not held as taxable income.

3 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

prize money will be held as taxable income given that the money received from prize money

forms the part of taxpayer’s income earning activity. According to the judgement of the court

in the case of “Stone v Federal Commissioner of Taxation (2005)” where the taxpayer was

policeman and javelin thrower. The taxpayer made derived income from salary and also

received sum from endorsement and prize money3. The court held the taxpayer to be carrying

on the business of the professional athlete and the earnings derived was held as taxable

income.

There should be an appropriate association between the receipt and the provision of

services rendered which is the ordinary incident of the provision of services. According to the

judgement of the court in the case of “FCT v Brent (1971)” where the wife of the train

robber was granted an exclusive right by the media company to publish her life story. The

court held that payment received by wife of train robber was the reward for service and will

be regarded as income from personal exertion.

A mere windfall gain could not be characterised as the income. For instance, an

individual receiving money from gambling winnings cannot be held as income except for the

circumstances where the person is carrying on the business of gambling. The court of law in

the case of “Harris v FCT (1980)” has distinguished windfall amount that are received

unexpectedly or infrequently.

A mere prize is not characterized as income. The court of law referring to the

legislation passed in the circumstance of “Moore v Griffiths (1972)” held that mere winning

from prizes was not held as taxable income.

3 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

A gain which is classified as the mere gift cannot be held as carrying the character of

income. An unsolicited gift will not be the part of income of the recipient simply because

generosity was inspired by the goodwill. The judgement of the court of law in “FCT v Hayes

(1956)” where the accountant received shares in the company from the previous owner of

company could not be held as income.

Periodic receipts having the character of income will be held as assessable income.

The judgement held in the case of “FCT v Dixon (1952)” any form of periodic receipts

received by the taxpayer will be held as assessable income4.

A compensation payment received is mostly considered to be capital where a

substantial amount of inconvenience is caused to the structure. A payment is mostly likely to

be considered as the substitute for the lost income when the inconvenience is incidental to the

that form of business. In the event of “Rowe v FCT (1997)” the court of law held that amount

paid as compensation or reimbursement relating to deductible expenditure cannot be regarded

as income under ordinary concepts. The court of law held that payment was not regarded as

“remuneration” but was held as “reparation”.

Application:

The receipt of $90,000 as salary by Kate represents employment remuneration from

the ordinary concept and will be assessable as income. Citing the reference of “Dean v FCT

(1997)” the receipt of salary by Kate is for the services provided in the capacity of employee

and will be income from personal exertion.

4 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

A gain which is classified as the mere gift cannot be held as carrying the character of

income. An unsolicited gift will not be the part of income of the recipient simply because

generosity was inspired by the goodwill. The judgement of the court of law in “FCT v Hayes

(1956)” where the accountant received shares in the company from the previous owner of

company could not be held as income.

Periodic receipts having the character of income will be held as assessable income.

The judgement held in the case of “FCT v Dixon (1952)” any form of periodic receipts

received by the taxpayer will be held as assessable income4.

A compensation payment received is mostly considered to be capital where a

substantial amount of inconvenience is caused to the structure. A payment is mostly likely to

be considered as the substitute for the lost income when the inconvenience is incidental to the

that form of business. In the event of “Rowe v FCT (1997)” the court of law held that amount

paid as compensation or reimbursement relating to deductible expenditure cannot be regarded

as income under ordinary concepts. The court of law held that payment was not regarded as

“remuneration” but was held as “reparation”.

Application:

The receipt of $90,000 as salary by Kate represents employment remuneration from

the ordinary concept and will be assessable as income. Citing the reference of “Dean v FCT

(1997)” the receipt of salary by Kate is for the services provided in the capacity of employee

and will be income from personal exertion.

4 Braithwaite, Valerie, ed. Taxing democracy: Understanding tax avoidance and evasion.

Routledge, 2017.

5TAXATION LAW

Kate in her spare time participates in high-jumping competitions that led her winning

prize of $60,000 and sports equipment of $20,000 from high-jumping competition. Referring

to “Stone v FCT (2005)” winning from prize money will be held as taxable income under

“section 6-5 of the ITAA 1997” since she regularly participated in such completion in pursuit

of excellence5. Kate carried on the activities of professional athlete and the earnings derived

was held as taxable income. Additionally, the receipt of $20,000 sporting equipment by Kate

will be classified as CGT asset under section 108-5 of the ITAA 1997.

The receipt of $10,000 by Kate had an appropriate relationship between the receipt

and the provision of services rendered which is in the ordinary occurrence of the provision of

services. Citing the reference of “FCT v Brent (1971)” the amount of $10,000 will be

included in the assessable income since it is reward for service that originated from the

personal exertion.

The receipt of $3000 sum from gambling by Kate cannot be held as income in other

words the sum won by Kate is a mere windfall gain that could not be characterised as the

income. By citing the reference of “Harris v FCT (1980)” the amount received by Kate from

gambling is received unexpectedly and did not had regular character of income6.

By referring to the event of “Moore v Griffiths (1972)” the winning of $1000 from

horse competition by Kate at the local ranch is again mere winning from prizes.

5 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Canberra: Treasury working paper 2001 (2015).

6 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The accounting

review 91.1 (2015): 47-68.

Kate in her spare time participates in high-jumping competitions that led her winning

prize of $60,000 and sports equipment of $20,000 from high-jumping competition. Referring

to “Stone v FCT (2005)” winning from prize money will be held as taxable income under

“section 6-5 of the ITAA 1997” since she regularly participated in such completion in pursuit

of excellence5. Kate carried on the activities of professional athlete and the earnings derived

was held as taxable income. Additionally, the receipt of $20,000 sporting equipment by Kate

will be classified as CGT asset under section 108-5 of the ITAA 1997.

The receipt of $10,000 by Kate had an appropriate relationship between the receipt

and the provision of services rendered which is in the ordinary occurrence of the provision of

services. Citing the reference of “FCT v Brent (1971)” the amount of $10,000 will be

included in the assessable income since it is reward for service that originated from the

personal exertion.

The receipt of $3000 sum from gambling by Kate cannot be held as income in other

words the sum won by Kate is a mere windfall gain that could not be characterised as the

income. By citing the reference of “Harris v FCT (1980)” the amount received by Kate from

gambling is received unexpectedly and did not had regular character of income6.

By referring to the event of “Moore v Griffiths (1972)” the winning of $1000 from

horse competition by Kate at the local ranch is again mere winning from prizes.

5 Cao, Liangyue, et al. "Understanding the economy-wide efficiency and incidence of major

Australian taxes." Canberra: Treasury working paper 2001 (2015).

6 Davis, Angela K., et al. "Do socially responsible firms pay more taxes?." The accounting

review 91.1 (2015): 47-68.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

Consequently, the act of engaging in horse riding by Kate was occasionally and the prize

winning from such competition cannot be held taxable since it lacked an income character.

Kate received a generous gift of $2000 in the Christmas party from her grandparents.

Gain that is categorized as the mere gift cannot be regarded as having the nature of income.

An unsolicited receipt of gift by Kate will not form the part of income simply because

generosity was inspired by her grandparents to gift her. Citing the reference of “FCT v

Hayes (1956)” the receipt of $2000 by Kate could not be held as income since mere gift is

not characterized as taxable income7.

Kate derived a rental income of $20,000 from her rental property in Blue Mountains.

Citing the reference of “Federal Commissioner of Taxation v Dixon (1952)” the receipt of

rental income by Kate is a periodic receipts having the character of income and the same will

be held as assessable income.

As per ATO an individual receiving compensation payment for the loss of profit

making structure is held as capital in nature. Kate rental property was destroyed by the

seasonal bushfire. The compensation payment received by Kate represents a payment that is

mostly likely to be considered as the substitute for the lost income. The payment of insurance

received by Kate is mostly considered to be capital where a substantial amount of loss is

caused to the rental property8. Referring to the judgement of court of law in “Rowe v FCT

(1997)” compensation received for loss of property cannot be regarded as income under

7 Chardon, Toni, Mark Brimble, and Brett Freudenberg. "Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]." Taxation Today 102 (2017): 17-25.

8 Cynthia Coleman and Kerrie Sadiq, Principles Of Taxation Law 2013.

Consequently, the act of engaging in horse riding by Kate was occasionally and the prize

winning from such competition cannot be held taxable since it lacked an income character.

Kate received a generous gift of $2000 in the Christmas party from her grandparents.

Gain that is categorized as the mere gift cannot be regarded as having the nature of income.

An unsolicited receipt of gift by Kate will not form the part of income simply because

generosity was inspired by her grandparents to gift her. Citing the reference of “FCT v

Hayes (1956)” the receipt of $2000 by Kate could not be held as income since mere gift is

not characterized as taxable income7.

Kate derived a rental income of $20,000 from her rental property in Blue Mountains.

Citing the reference of “Federal Commissioner of Taxation v Dixon (1952)” the receipt of

rental income by Kate is a periodic receipts having the character of income and the same will

be held as assessable income.

As per ATO an individual receiving compensation payment for the loss of profit

making structure is held as capital in nature. Kate rental property was destroyed by the

seasonal bushfire. The compensation payment received by Kate represents a payment that is

mostly likely to be considered as the substitute for the lost income. The payment of insurance

received by Kate is mostly considered to be capital where a substantial amount of loss is

caused to the rental property8. Referring to the judgement of court of law in “Rowe v FCT

(1997)” compensation received for loss of property cannot be regarded as income under

7 Chardon, Toni, Mark Brimble, and Brett Freudenberg. "Tax and superannuation literacy:

Australian and New Zealand perspectives [Part 1]." Taxation Today 102 (2017): 17-25.

8 Cynthia Coleman and Kerrie Sadiq, Principles Of Taxation Law 2013.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

ordinary concepts since the payment cannot be held as “remuneration” but it is classified as

“reparation”.

In compliance with the “section 8-1 of the ITAA 1997” the allowable expenditure of

$40,000 that is reported by Kate will be held as allowable deduction by assuming that the

expenses occurred is for deriving the assessable income.

Conclusion:

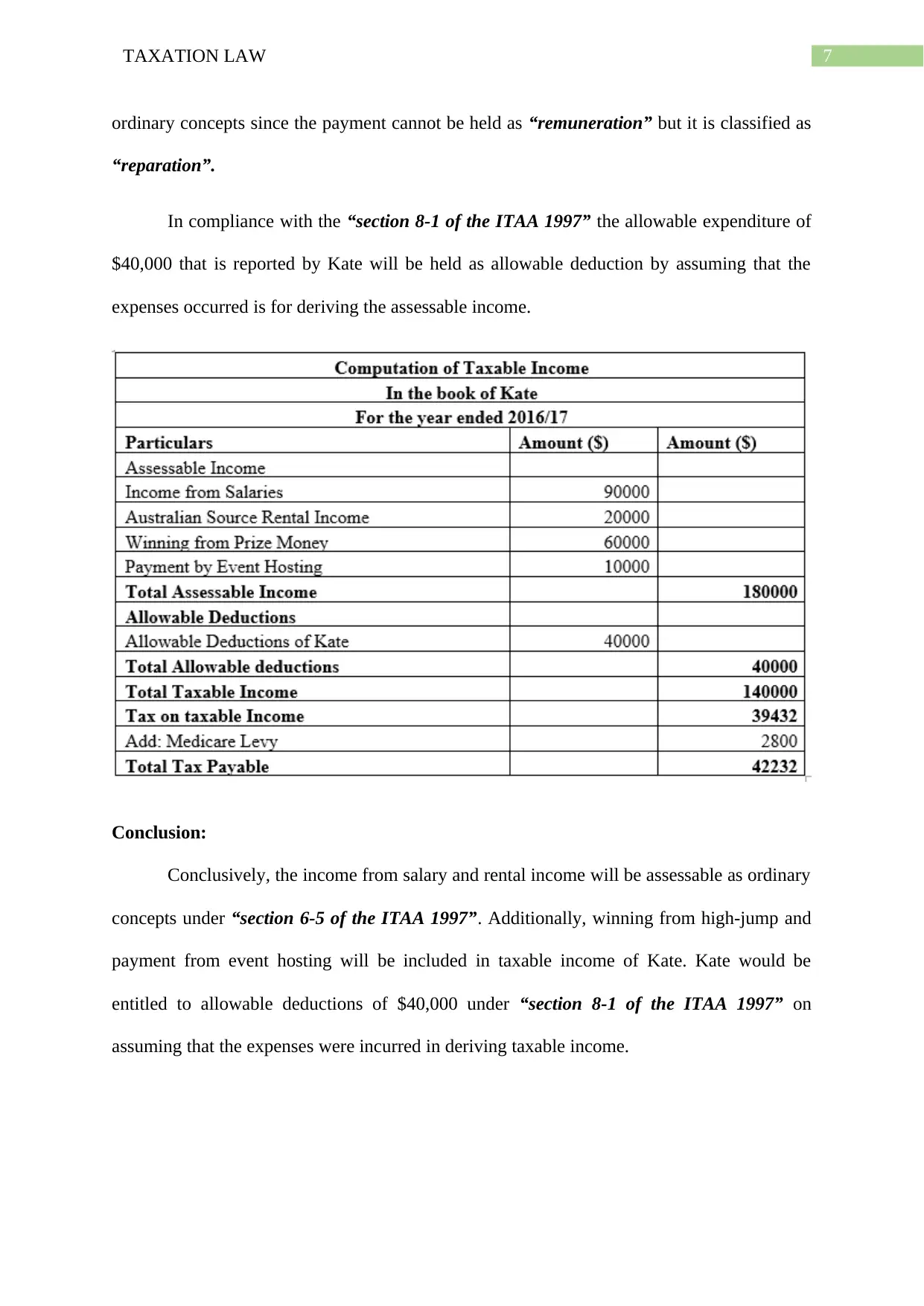

Conclusively, the income from salary and rental income will be assessable as ordinary

concepts under “section 6-5 of the ITAA 1997”. Additionally, winning from high-jump and

payment from event hosting will be included in taxable income of Kate. Kate would be

entitled to allowable deductions of $40,000 under “section 8-1 of the ITAA 1997” on

assuming that the expenses were incurred in deriving taxable income.

ordinary concepts since the payment cannot be held as “remuneration” but it is classified as

“reparation”.

In compliance with the “section 8-1 of the ITAA 1997” the allowable expenditure of

$40,000 that is reported by Kate will be held as allowable deduction by assuming that the

expenses occurred is for deriving the assessable income.

Conclusion:

Conclusively, the income from salary and rental income will be assessable as ordinary

concepts under “section 6-5 of the ITAA 1997”. Additionally, winning from high-jump and

payment from event hosting will be included in taxable income of Kate. Kate would be

entitled to allowable deductions of $40,000 under “section 8-1 of the ITAA 1997” on

assuming that the expenses were incurred in deriving taxable income.

8TAXATION LAW

Answer to question 2:

Heading:

The current problem is relating to the ascertainment of claiming deductions under

section 8-1 of the ITAA 1997 arising from loss and outgoings that is occurred during the

income year of 2016-17.

Issues:

The issue examines the deduction of expenses such as occurred by Bags Co Ltd and

providing advice on education expenses, travel expenses, conference and equipment cost

under section 8-1 of the ITAA 19979.

Rule:

As held under section 8-1 there are two positive limbs where an individual can claim

deductions from their assessable income any form of loss or outgoing up to the extent when

the expenses is occurred in gaining taxable income or generating taxable income. As held in

“FCT v Ronpibon Tin NL (1949)” expenses that are incidental and relevant will be

considered as allowable deductions given it is incurred in generating taxable income10.

Legal expenditure incurred by the taxpayer to prevent the defamatory statements

would be considered as an allowable deductions section 8-1 of the ITAA 1997. The court in

9 Davison, Mark, Ann Monotti, and Leanne Wiseman. Australian intellectual property law.

Cambridge University Press, 2015.

10 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office." The APPEA Journal 57.1 (2017): 49-63.

Answer to question 2:

Heading:

The current problem is relating to the ascertainment of claiming deductions under

section 8-1 of the ITAA 1997 arising from loss and outgoings that is occurred during the

income year of 2016-17.

Issues:

The issue examines the deduction of expenses such as occurred by Bags Co Ltd and

providing advice on education expenses, travel expenses, conference and equipment cost

under section 8-1 of the ITAA 19979.

Rule:

As held under section 8-1 there are two positive limbs where an individual can claim

deductions from their assessable income any form of loss or outgoing up to the extent when

the expenses is occurred in gaining taxable income or generating taxable income. As held in

“FCT v Ronpibon Tin NL (1949)” expenses that are incidental and relevant will be

considered as allowable deductions given it is incurred in generating taxable income10.

Legal expenditure incurred by the taxpayer to prevent the defamatory statements

would be considered as an allowable deductions section 8-1 of the ITAA 1997. The court in

9 Davison, Mark, Ann Monotti, and Leanne Wiseman. Australian intellectual property law.

Cambridge University Press, 2015.

10 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability

of Australia to tax economic activity in offshore hubs and the position of the Australian

Taxation Office." The APPEA Journal 57.1 (2017): 49-63.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

the case of “Magna Alloys & Research Pty Ltd (1980)” stated that the company is allowed to

claim deductions for legal expenditure occurred in defending against the defamatory charges

will be considered as allowable deduction11.

As stated under “taxation ruling of TR 93/30” expenditure that is occurred with the

taxpayer home are considered personal or domestic in character and they do not qualify as

allowable deductions for taxpayer under section 8-1. However, an exception to this rule is

that where the portion of home is used for generating income and having the character of

place of business then the expenses incurred such as lease, rent and taxes might be partially

considered for deductions. The court of law in “FCT v Swinford (1984)” allowed the

scriptwriter for claiming deductions relating to the portion of rent paid for the flat where the

taxpayer dedicated a separate room for writing script since the taxpayer did not had separate

business premises.

According to “taxation ruling of TR 98/9” Self-education expenditure incurred to

maintain or increase the skill of taxpayer in occupation where the taxpayer is engaged or

particularly for improving the earning capacity of taxpayer will be considered as allowable

deductions. As held in “Highfield v FCT (1982)” a dentist was allowed to claim allowable

deductions for expenses incurred in course fees, travel and expenses related to Master of

Science in Periodontics12. The court held that expenses were occurred necessarily in

executing the business since the purpose of undertaking the degree was to advance his

practice.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

12 Paul Kenny, Australian Tax 2013 (LexisNexis Butterworths, 2013).

the case of “Magna Alloys & Research Pty Ltd (1980)” stated that the company is allowed to

claim deductions for legal expenditure occurred in defending against the defamatory charges

will be considered as allowable deduction11.

As stated under “taxation ruling of TR 93/30” expenditure that is occurred with the

taxpayer home are considered personal or domestic in character and they do not qualify as

allowable deductions for taxpayer under section 8-1. However, an exception to this rule is

that where the portion of home is used for generating income and having the character of

place of business then the expenses incurred such as lease, rent and taxes might be partially

considered for deductions. The court of law in “FCT v Swinford (1984)” allowed the

scriptwriter for claiming deductions relating to the portion of rent paid for the flat where the

taxpayer dedicated a separate room for writing script since the taxpayer did not had separate

business premises.

According to “taxation ruling of TR 98/9” Self-education expenditure incurred to

maintain or increase the skill of taxpayer in occupation where the taxpayer is engaged or

particularly for improving the earning capacity of taxpayer will be considered as allowable

deductions. As held in “Highfield v FCT (1982)” a dentist was allowed to claim allowable

deductions for expenses incurred in course fees, travel and expenses related to Master of

Science in Periodontics12. The court held that expenses were occurred necessarily in

executing the business since the purpose of undertaking the degree was to advance his

practice.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

12 Paul Kenny, Australian Tax 2013 (LexisNexis Butterworths, 2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

According to legislative response in section 25-100 of the ITAA 1997 an individual is

allowed to claim an allowable deductions relating to expenses incurred on travelling. As held

in “FCT v Wiener” the teacher was allowed to claim allowable deduction for expenses

incurred on travel between the place of work and home with first and last school attended

every day.

Division 40 of capital allowance provides under section 40-25 (1) that a unit can

claim allowable deduction for amount that are equivalent to decline in value for the income

year of the depreciating asset which is held during the year. Furthermore, division 40-25

allows deductions reduced when the asset decline in value is in respect to its use for the

purpose other than taxable purpose.

Application:

As evident from the case study Bag Co Ltd occurred expenditure on trading stock and

payment of wages to employees. Furthermore, it is noted that Bag Co Ltd also incurred

expenses relating to rent paid to occupy the retail premises in the income year. The expenses

incurred by Bag Co Ltd are occurred under section 8-1 of the positive limbs and a deduction

can be claimed from its assessable income. Citing the reference of “FCT v Ronpibon Tin NL

(1949)” expenses incurred by Bag Co Ltd are incidental and relevant will be considered as

allowable deductions13.

Bag Co Ltd also incurred legal expenses in defending legal actions for misconduct

which can be considered allowable deductions “section 8-1 of the ITAA 1997”14. Citing the

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

14 ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

According to legislative response in section 25-100 of the ITAA 1997 an individual is

allowed to claim an allowable deductions relating to expenses incurred on travelling. As held

in “FCT v Wiener” the teacher was allowed to claim allowable deduction for expenses

incurred on travel between the place of work and home with first and last school attended

every day.

Division 40 of capital allowance provides under section 40-25 (1) that a unit can

claim allowable deduction for amount that are equivalent to decline in value for the income

year of the depreciating asset which is held during the year. Furthermore, division 40-25

allows deductions reduced when the asset decline in value is in respect to its use for the

purpose other than taxable purpose.

Application:

As evident from the case study Bag Co Ltd occurred expenditure on trading stock and

payment of wages to employees. Furthermore, it is noted that Bag Co Ltd also incurred

expenses relating to rent paid to occupy the retail premises in the income year. The expenses

incurred by Bag Co Ltd are occurred under section 8-1 of the positive limbs and a deduction

can be claimed from its assessable income. Citing the reference of “FCT v Ronpibon Tin NL

(1949)” expenses incurred by Bag Co Ltd are incidental and relevant will be considered as

allowable deductions13.

Bag Co Ltd also incurred legal expenses in defending legal actions for misconduct

which can be considered allowable deductions “section 8-1 of the ITAA 1997”14. Citing the

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’

view." Procedia-Social and Behavioral Sciences 109 (2014): 1069-1075.

14 ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

11TAXATION LAW

reference of “Magna Alloys & Research Pty Ltd (1980)” Bag Co Ltd can claim deductions

for legal expenditure occurred in defending against the misconduct charges up to the extent

they are occurred in gaining the taxable income.

Sally an employee of Bag Co Ltd incurred expenses on lease apartment for

maintaining an office to carry-out the accountancy work. Citing the reference of “FCT v

Swinford (1984)” sally would be allowed to claim allowable deduction for home office

expenses under section 8-1 of the ITAA 199715. Sally later incurred expenses on self-

education expenses for enrolling in Master of professional accounting to advance in her

career. With reference to “Highfield v FCT (1982)” sally will be able to claim allowable

deduction for improving the earning capacity of taxpayer.

Sally occurred travelling expenses on attending chartered accountants conference and

incurs $700 on air travel and $1000 accommodations. The expenses incurred by Sally on

travelling and air accommodations were for improving her income earning capacity and with

reference to “FCT v Wiener” she will be allowed to claim deductions on travelling

expenses16. Sally will be further able to claim capital allowance deductions under section 40-

25 (1) for decline in value of computer equipment in respect to 80% of the work purpose.

Prime Cost Method:

15 R. H Woellner, Australian Taxation Law 2012 (CCH Australia, 2013).

16 Richard E Krever, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

reference of “Magna Alloys & Research Pty Ltd (1980)” Bag Co Ltd can claim deductions

for legal expenditure occurred in defending against the misconduct charges up to the extent

they are occurred in gaining the taxable income.

Sally an employee of Bag Co Ltd incurred expenses on lease apartment for

maintaining an office to carry-out the accountancy work. Citing the reference of “FCT v

Swinford (1984)” sally would be allowed to claim allowable deduction for home office

expenses under section 8-1 of the ITAA 199715. Sally later incurred expenses on self-

education expenses for enrolling in Master of professional accounting to advance in her

career. With reference to “Highfield v FCT (1982)” sally will be able to claim allowable

deduction for improving the earning capacity of taxpayer.

Sally occurred travelling expenses on attending chartered accountants conference and

incurs $700 on air travel and $1000 accommodations. The expenses incurred by Sally on

travelling and air accommodations were for improving her income earning capacity and with

reference to “FCT v Wiener” she will be allowed to claim deductions on travelling

expenses16. Sally will be further able to claim capital allowance deductions under section 40-

25 (1) for decline in value of computer equipment in respect to 80% of the work purpose.

Prime Cost Method:

15 R. H Woellner, Australian Taxation Law 2012 (CCH Australia, 2013).

16 Richard E Krever, Australian Taxation Law Cases 2013 (Thomson Reuters, 2013).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.