Taxation Law Exam - Taxation Law Calculations and Analysis

VerifiedAdded on 2022/11/25

|8

|1861

|269

Homework Assignment

AI Summary

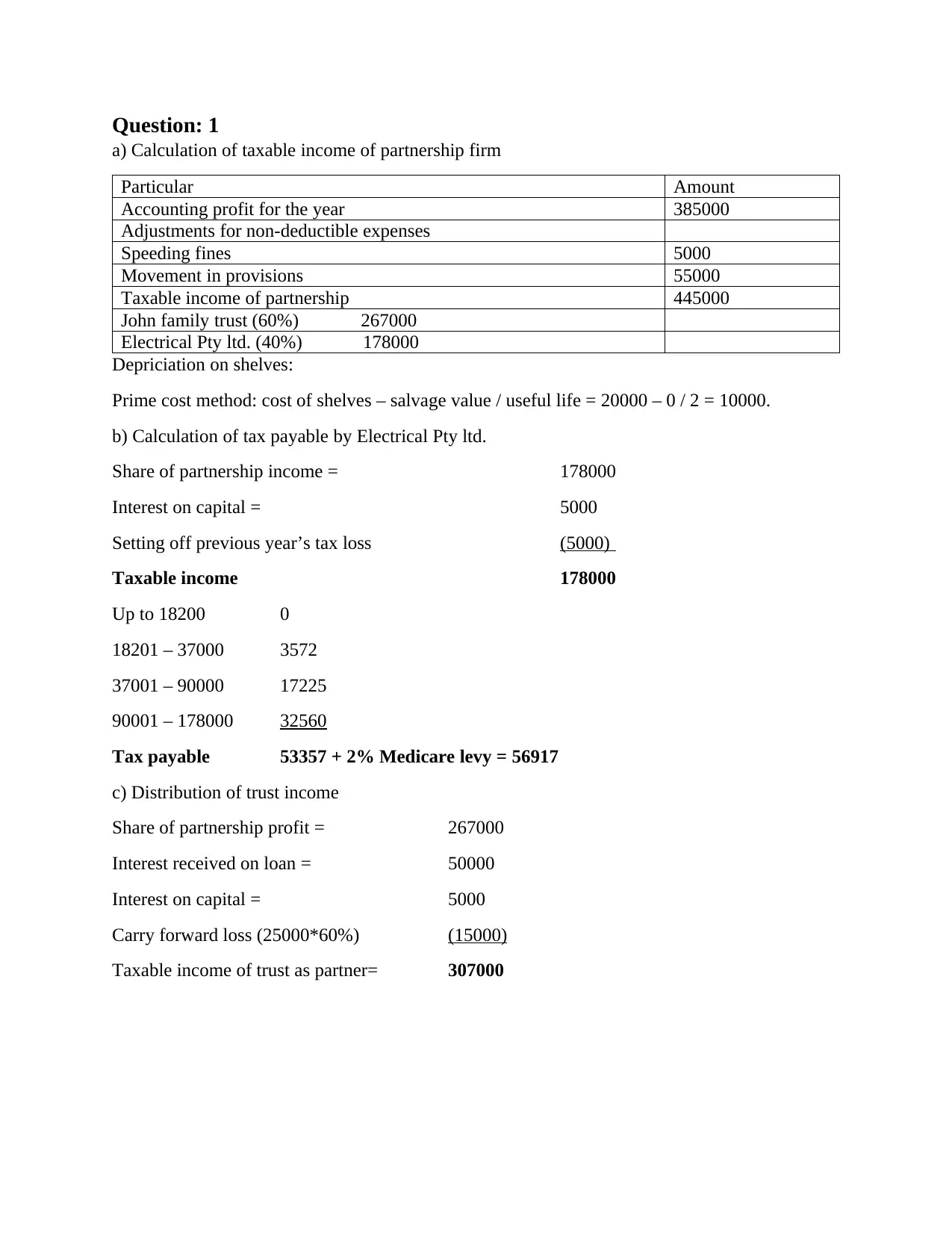

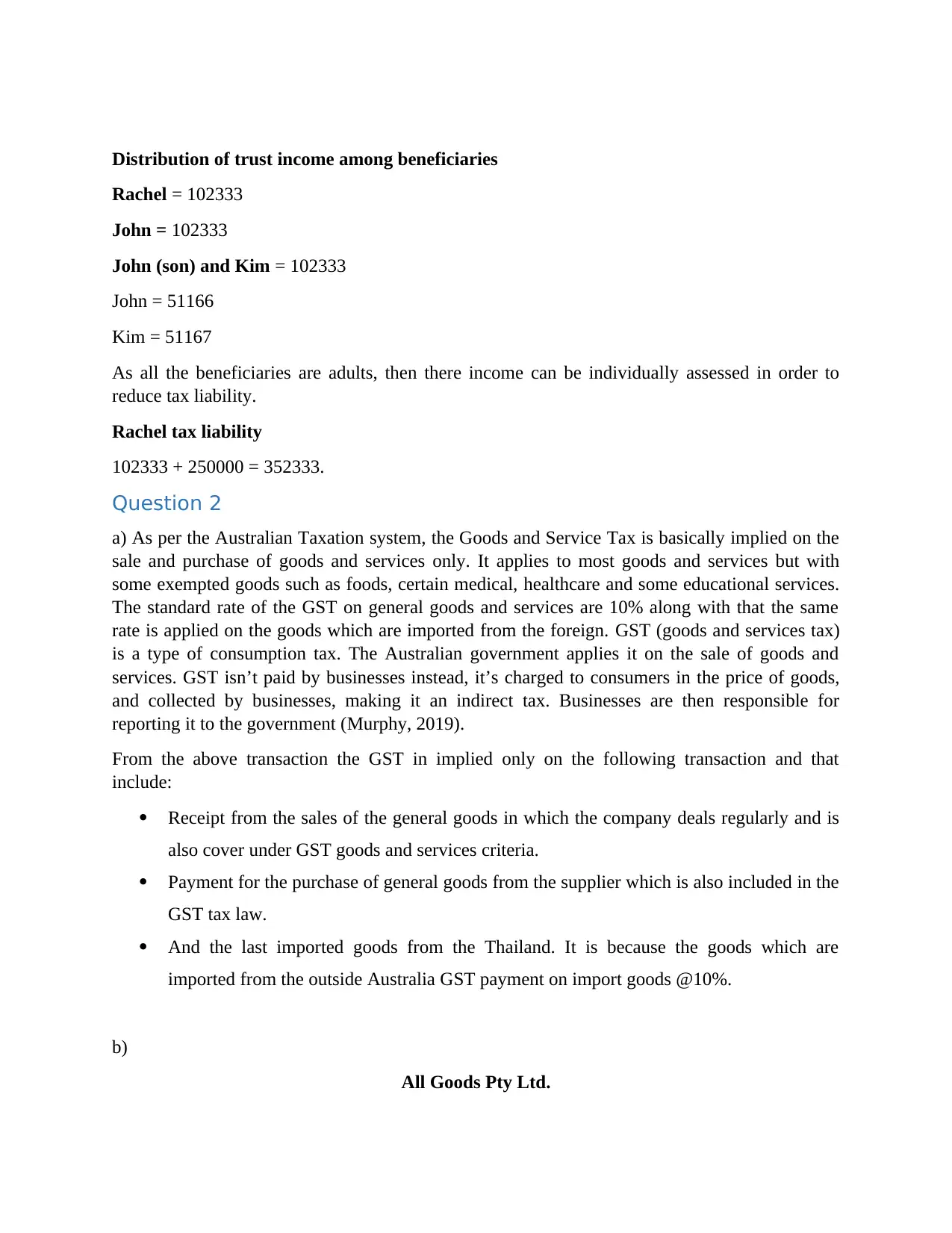

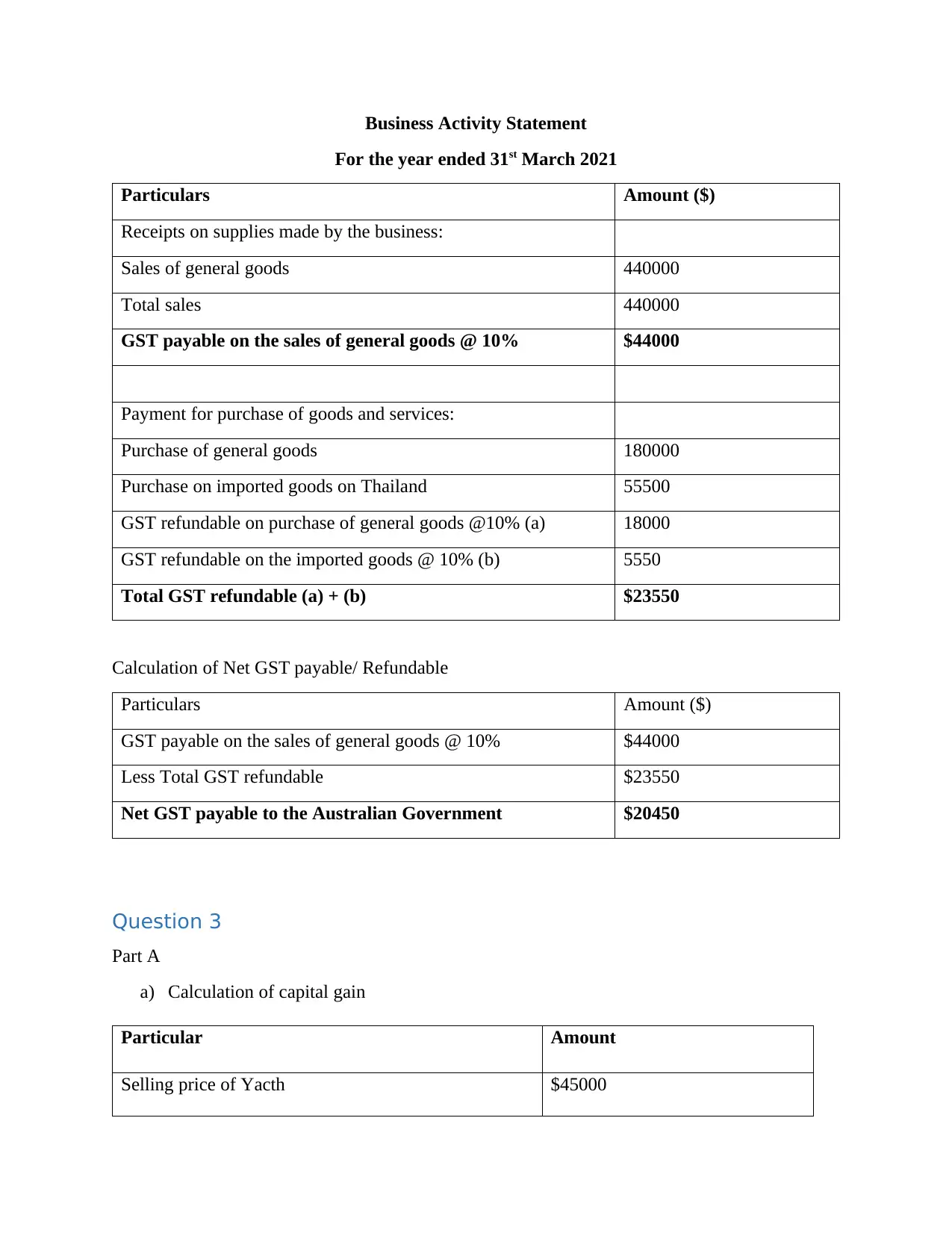

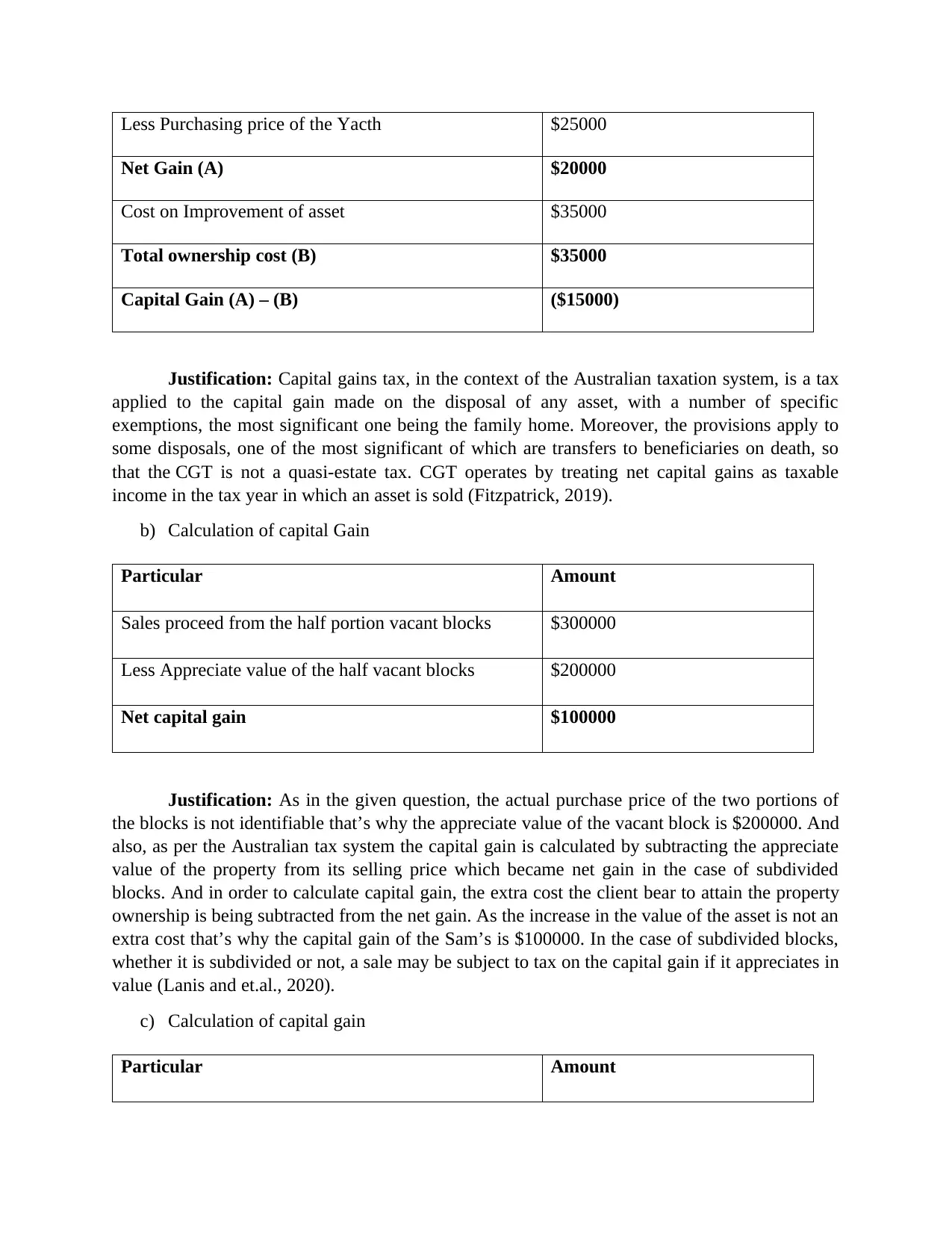

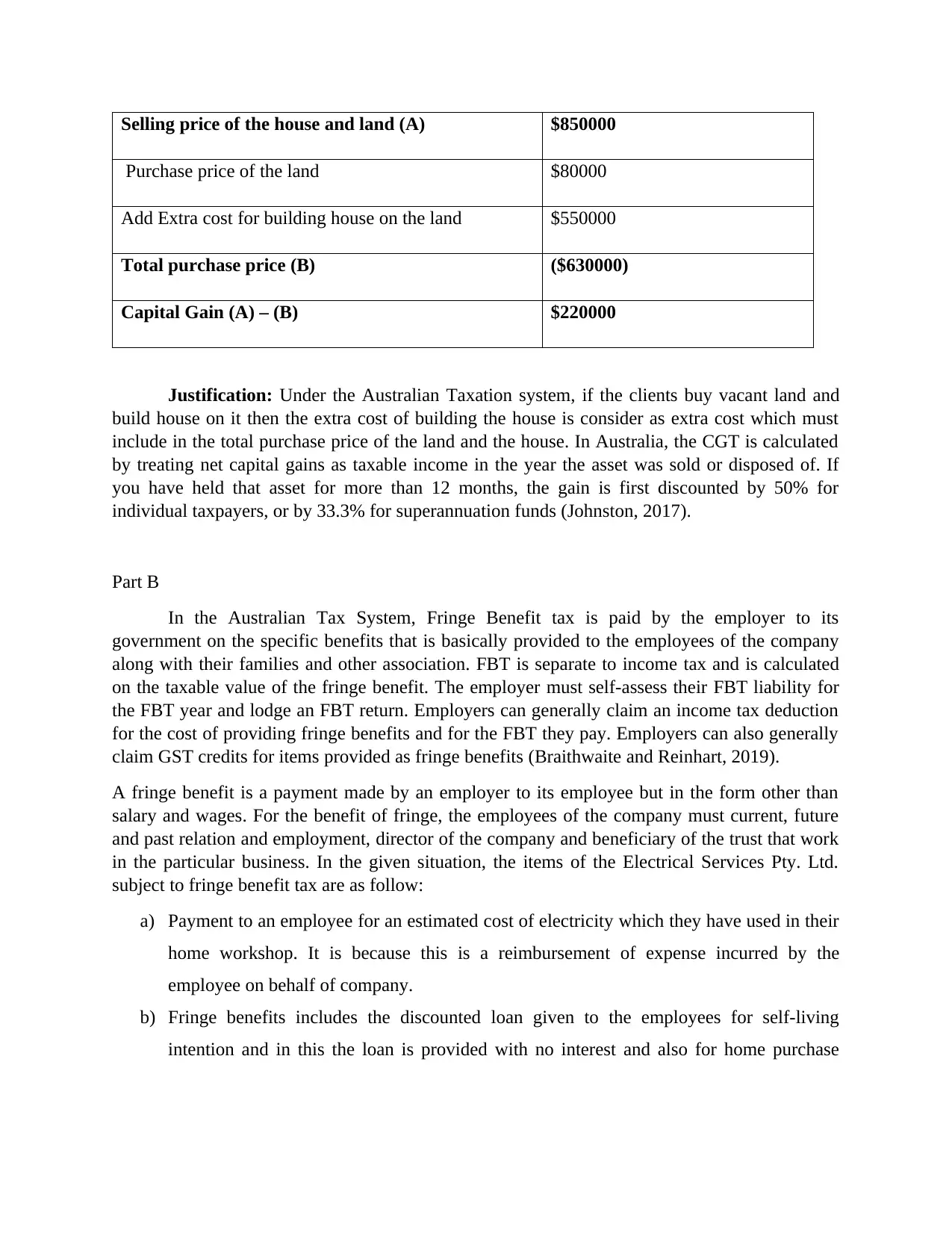

This document provides a comprehensive solution to a taxation law exam, addressing several key areas of Australian taxation. The solution begins with the calculation of taxable income for a partnership firm, including adjustments for non-deductible expenses and depreciation. It then proceeds to calculate the tax payable by a company, considering its share of partnership income and setting off previous year's tax losses. The document also includes the distribution of trust income among beneficiaries. The second part of the solution delves into Goods and Services Tax (GST) calculations, outlining the transactions subject to GST, and provides a Business Activity Statement (BAS) with detailed calculations of GST payable or refundable. The final section addresses capital gains tax (CGT), calculating capital gains on the sale of assets, subdivided blocks, and a house and land. It also covers fringe benefit tax (FBT), identifying items subject to FBT and providing justifications based on Australian taxation provisions.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.