Subdividing Land and CGT Implications

VerifiedAdded on 2020/03/16

|11

|3054

|78

AI Summary

This assignment focuses on the capital gains tax (CGT) consequences of subdividing land in Australia. It delves into determining the cost base for each subdivided block, analyzing the holding period, and calculating assessable income based on a hypothetical scenario involving land subdivision and construction. The analysis emphasizes the application of relevant Australian Taxation Office (ATO) guidelines and principles.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Taxation law

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

Question 1..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

Question 2..................................................................................................................................3

Issue........................................................................................................................................3

Regulations.............................................................................................................................3

Applicability...........................................................................................................................3

Conclusion..............................................................................................................................3

References..................................................................................................................................4

QUESTION 1

Issue

Minh was born and brought up in Malaysia and was holding a successful business venture

there only. During June 201, he was given a visa to operate in Australia along with his family

and with the intention to migrate he started a business in Australia. A home was purchased by

him for his own and family in Melbourne, in which his spouse and children will stay and their

children are admitted to the local school. Minh even now is an active partner in a venture in

Kuala Lumpur which has considerable investments that need him to not present in Australia

for the income year. At his non-presence, he resided in his apartment in Kuala Lumpur while

maintaining its social interests. At that time, he spends over 120 days here in Australia, and

on 30 June 2016, he did not establish business nor he make an opinion to settle there

permanently. The issue to determine residential status of Minh and its impact on

Assessability of income.

Regulations

Taxation office sees residency in a different way as the other governmental agencies see it. A

person will be entitled as a resident of Australia for the taxation purpose, when they reside in

Australia, implementing the ordinary definition of this term or meet only one criterion of

three statutory tests (Saad, 2014).

1. Domicile test: An individual permanent domicile must be in Australia until taxation

commissioner is contended that the individual’s permanent residence is outside of

Australia.

2. The test of 183 days: the individual must be there in Australia for 183 days during the

year of income until the individual’s permanent residence is outside of Australia and

they do not have a purpose to reside in Australia (Residency tests, 2016).

3. Test of Commonwealth superannuation fund: individual must be the member of

Commonwealth superannuation fund

According to Taxation Ruling TR 98/17; commissioner of tax assesses the time period of an

individual by which he/she is staying in Australia and is not determined by itself. If they are

an Australian resident for the purpose of the tax, however, influence is not provided to the

proof of permanence, routine consistent with the person who stays in Australia (2.1.2.10

Residence Requirements, 2017).

Issue

Minh was born and brought up in Malaysia and was holding a successful business venture

there only. During June 201, he was given a visa to operate in Australia along with his family

and with the intention to migrate he started a business in Australia. A home was purchased by

him for his own and family in Melbourne, in which his spouse and children will stay and their

children are admitted to the local school. Minh even now is an active partner in a venture in

Kuala Lumpur which has considerable investments that need him to not present in Australia

for the income year. At his non-presence, he resided in his apartment in Kuala Lumpur while

maintaining its social interests. At that time, he spends over 120 days here in Australia, and

on 30 June 2016, he did not establish business nor he make an opinion to settle there

permanently. The issue to determine residential status of Minh and its impact on

Assessability of income.

Regulations

Taxation office sees residency in a different way as the other governmental agencies see it. A

person will be entitled as a resident of Australia for the taxation purpose, when they reside in

Australia, implementing the ordinary definition of this term or meet only one criterion of

three statutory tests (Saad, 2014).

1. Domicile test: An individual permanent domicile must be in Australia until taxation

commissioner is contended that the individual’s permanent residence is outside of

Australia.

2. The test of 183 days: the individual must be there in Australia for 183 days during the

year of income until the individual’s permanent residence is outside of Australia and

they do not have a purpose to reside in Australia (Residency tests, 2016).

3. Test of Commonwealth superannuation fund: individual must be the member of

Commonwealth superannuation fund

According to Taxation Ruling TR 98/17; commissioner of tax assesses the time period of an

individual by which he/she is staying in Australia and is not determined by itself. If they are

an Australian resident for the purpose of the tax, however, influence is not provided to the

proof of permanence, routine consistent with the person who stays in Australia (2.1.2.10

Residence Requirements, 2017).

Taxation office factors state that weight is given to:

Purpose of existence

family and employment/ business ties

site and maintenance of assets

activities for a livelihood

In accordance with this ruling approach of 6 months is also considered (instead of that 183

days or financial year’s 50%) is usually enough to identify if or if not there is consistency in

behaviour to be a resident. However, in general, there are a large number of ways to identify,

if someone’s personal circumstances can make them a resident or a non-resident, if these

criteria are satisfied then an individual will be said a resident for purposes of taxation

(Bevacqua, 2015).

Lived in Australia from birth

Transferred to Australia to live there on permanent basis

Lived in Australia for more than six months of financial year

Lived in Australia for six months or more than that

Summary of differences in Assessability of income on the basis of residential status

Resident for tax purposes Non-resident for tax purposes

Reduction made in rates of tax at the low

level of income.

Tax payment on each and every dollar (no

allowance for tax-free limit)

Tax charged on income earned through

worldwide sources

Tax is charged only on income generated in

Australia

Tax payment on Medicare and can do

claims on those expenses

Not liable to pay Medicare and cannot do

claims.

Interest income taxable at the marginal

tax rate of taxpayer

Tax on Interest 10% or 45% unless no TFN

or overseas address is provided

CGT liability on global assets Liable for CGT on “taxable Australian

property”

Availability of offset provided from Offsets and LAFHA not available

Purpose of existence

family and employment/ business ties

site and maintenance of assets

activities for a livelihood

In accordance with this ruling approach of 6 months is also considered (instead of that 183

days or financial year’s 50%) is usually enough to identify if or if not there is consistency in

behaviour to be a resident. However, in general, there are a large number of ways to identify,

if someone’s personal circumstances can make them a resident or a non-resident, if these

criteria are satisfied then an individual will be said a resident for purposes of taxation

(Bevacqua, 2015).

Lived in Australia from birth

Transferred to Australia to live there on permanent basis

Lived in Australia for more than six months of financial year

Lived in Australia for six months or more than that

Summary of differences in Assessability of income on the basis of residential status

Resident for tax purposes Non-resident for tax purposes

Reduction made in rates of tax at the low

level of income.

Tax payment on each and every dollar (no

allowance for tax-free limit)

Tax charged on income earned through

worldwide sources

Tax is charged only on income generated in

Australia

Tax payment on Medicare and can do

claims on those expenses

Not liable to pay Medicare and cannot do

claims.

Interest income taxable at the marginal

tax rate of taxpayer

Tax on Interest 10% or 45% unless no TFN

or overseas address is provided

CGT liability on global assets Liable for CGT on “taxable Australian

property”

Availability of offset provided from Offsets and LAFHA not available

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

computation of tax, like LAFHA

According to Taxation Ruling TR 98/17; if someone tends to migrate to Australia for the

purpose of residing there on a permanent basis, then he/she will be considered as the resident

of Australia for the taxation purpose. This refers to:

Income generated from whichever source or country must be specified in the tax

return

One can also do claim for the tax benefits in Australia, like; offset provided from the

computation of tax, tax-free limit, charging of low tax.

A tax file number is required in order to work in Australia, and income tax is the primary tax

which is to be paid on earned income like remuneration, business or investment income. In

the end of assessment year which 30th June, most people file their yearly returns on tax. One

can take advice from a registered agent of tax for the tax payments and will prepare and

submit tax returns on the behalf of them. Agents are registered and entitled to make charged

in order to make and file tax returns. They should be authorized with Tax Practitioners Board

and must pursue strict rules and regulations.

Applicability

In accordance with the given case facts Minh will be considered an Australian resident as

with the intention to migrate he plans to business in Australia and his action (such as the

purchase of residence and admission of his children to local school) also coincides with his

objective of permanent stay in Australia. Thus irrespective of the condition of 183 days he

will be considered a resident for the purpose of computation of tax for the financial year.

Further, the fact that he is an active partner in Kuala Lumpur will not affect the residential

status as he is absent with the objective to operate his existing business but in case if changes

his mind for permanent residence then he will not be considered as an Australian resident.

The residential status of an individual plays a significant role for the purpose of assessment of

income in Australia. In accordance with the given case facts if Minh is Australia resident then

his taxable income will be covered by following provisions:

Tax charged on income earned through worldwide sources

CGT liability on global assets

According to Taxation Ruling TR 98/17; if someone tends to migrate to Australia for the

purpose of residing there on a permanent basis, then he/she will be considered as the resident

of Australia for the taxation purpose. This refers to:

Income generated from whichever source or country must be specified in the tax

return

One can also do claim for the tax benefits in Australia, like; offset provided from the

computation of tax, tax-free limit, charging of low tax.

A tax file number is required in order to work in Australia, and income tax is the primary tax

which is to be paid on earned income like remuneration, business or investment income. In

the end of assessment year which 30th June, most people file their yearly returns on tax. One

can take advice from a registered agent of tax for the tax payments and will prepare and

submit tax returns on the behalf of them. Agents are registered and entitled to make charged

in order to make and file tax returns. They should be authorized with Tax Practitioners Board

and must pursue strict rules and regulations.

Applicability

In accordance with the given case facts Minh will be considered an Australian resident as

with the intention to migrate he plans to business in Australia and his action (such as the

purchase of residence and admission of his children to local school) also coincides with his

objective of permanent stay in Australia. Thus irrespective of the condition of 183 days he

will be considered a resident for the purpose of computation of tax for the financial year.

Further, the fact that he is an active partner in Kuala Lumpur will not affect the residential

status as he is absent with the objective to operate his existing business but in case if changes

his mind for permanent residence then he will not be considered as an Australian resident.

The residential status of an individual plays a significant role for the purpose of assessment of

income in Australia. In accordance with the given case facts if Minh is Australia resident then

his taxable income will be covered by following provisions:

Tax charged on income earned through worldwide sources

CGT liability on global assets

In case he does not attain resident status then his taxable income will be covered by following

provisions:

Tax is charged only on income generated in Australia

Liable for CGT on “taxable Australian property”

These provisions are supported by certain advantages and disadvantages described in

provision part of case study.

Conclusion

On the basis of given facts and Australian taxation provisions; Minh will be

considered as an Australian resident.

Malaysian business and investment income will be assessable in Australia irrespective

of the source of origin as Australian residents is required to pay tax on their global

income. However, in case if he had paid tax in foreign countries then he will be

entitled to take off-set of the same.

QUESTION 2

Issue

Penny is willing to buy a home for her family in suburbs of Melbourne eastern. She wants to

raise funds for the purchase with the amount of $1million sale income of her previous

residence, further, she will be able to become free from debt. Rather, Penny made a purchase

of huge vacant land block for the amount of $1million sale income of her previous residence.

As per her requirements, the land tends to be very large, so she took a loan of additional $1

million in order to build four similar homes on the specified land. Penny took help from the

builder; however, she was engaged in managing and planning the proposed project to reduce

costs. One home was retained by Penny for the purpose of own and family residence and the

left three homes were put into sale and further, they were sold at $1m million each. The issue

is to determine the taxability of capital gain transaction in which penny was engaged.

Regulations

Most of the real estate are subjected to CGT (capital gain tax), this inclusive of rental

premises, holiday homes, business property and hobby farms.

One can get rid of CGT paying if sell a house that is said to their main residential place. One

can only contain a sole main residential place at a specified time period unless and until the

provisions:

Tax is charged only on income generated in Australia

Liable for CGT on “taxable Australian property”

These provisions are supported by certain advantages and disadvantages described in

provision part of case study.

Conclusion

On the basis of given facts and Australian taxation provisions; Minh will be

considered as an Australian resident.

Malaysian business and investment income will be assessable in Australia irrespective

of the source of origin as Australian residents is required to pay tax on their global

income. However, in case if he had paid tax in foreign countries then he will be

entitled to take off-set of the same.

QUESTION 2

Issue

Penny is willing to buy a home for her family in suburbs of Melbourne eastern. She wants to

raise funds for the purchase with the amount of $1million sale income of her previous

residence, further, she will be able to become free from debt. Rather, Penny made a purchase

of huge vacant land block for the amount of $1million sale income of her previous residence.

As per her requirements, the land tends to be very large, so she took a loan of additional $1

million in order to build four similar homes on the specified land. Penny took help from the

builder; however, she was engaged in managing and planning the proposed project to reduce

costs. One home was retained by Penny for the purpose of own and family residence and the

left three homes were put into sale and further, they were sold at $1m million each. The issue

is to determine the taxability of capital gain transaction in which penny was engaged.

Regulations

Most of the real estate are subjected to CGT (capital gain tax), this inclusive of rental

premises, holiday homes, business property and hobby farms.

One can get rid of CGT paying if sell a house that is said to their main residential place. One

can only contain a sole main residential place at a specified time period unless and until the

old residence is put into a sale for the intention to purchase another (Valuation methods –

property, 2017). In this event, the individual is allowed to an extended six-month period as

long as the new place will be considered as their new main residential place. The individual

resides in the old premises for continuous 3 months in the specified time period of 12 months

prior to sell it and it cannot be used to generate rent on that specified period (AO, 2015). The

Australian taxation office does not provides a precise justification of what is needed to form

up the main dwelling, but has given following factors to be taken into account:

Individual and his/her family resides in the residence

Mail has to be delivered on the residential address

Personal possessions must be at the residential place

Registration of vote must be done on the residential address

Connection of gas, phone and electricity to the premises

If a person has lived in their home from the start it was purchased and had not been

rented out either entirely or to a tenant and the size of land must be smaller than 2 hectares,

further, the individual will be entitled a full exception on Capital gain tax during its sale. This

will be useful while planning to live the life of renovator; selling the old one and purchasing

new, renovation and further putting the renovated premises into a sale (Jones, 2015). If at the

same time the individual is not able to earn rental income if individual go down this path, all

profits attained through the process renovation is exempted from CGT.

The main residential place is usually CGT exempted unless and until one has used it rent it

out or to run a business or the land is than 2 hectares.

Most significant factors to consider are:

Lodge records of the real estate, inclusive of own resident (if in near future one wants

to put that on rent or to run a business)

Keep in mind that while selling real estate, at the time (in which one incurs a capital

profit or loss) is when individuals makes an agreement, not at the time of settling.

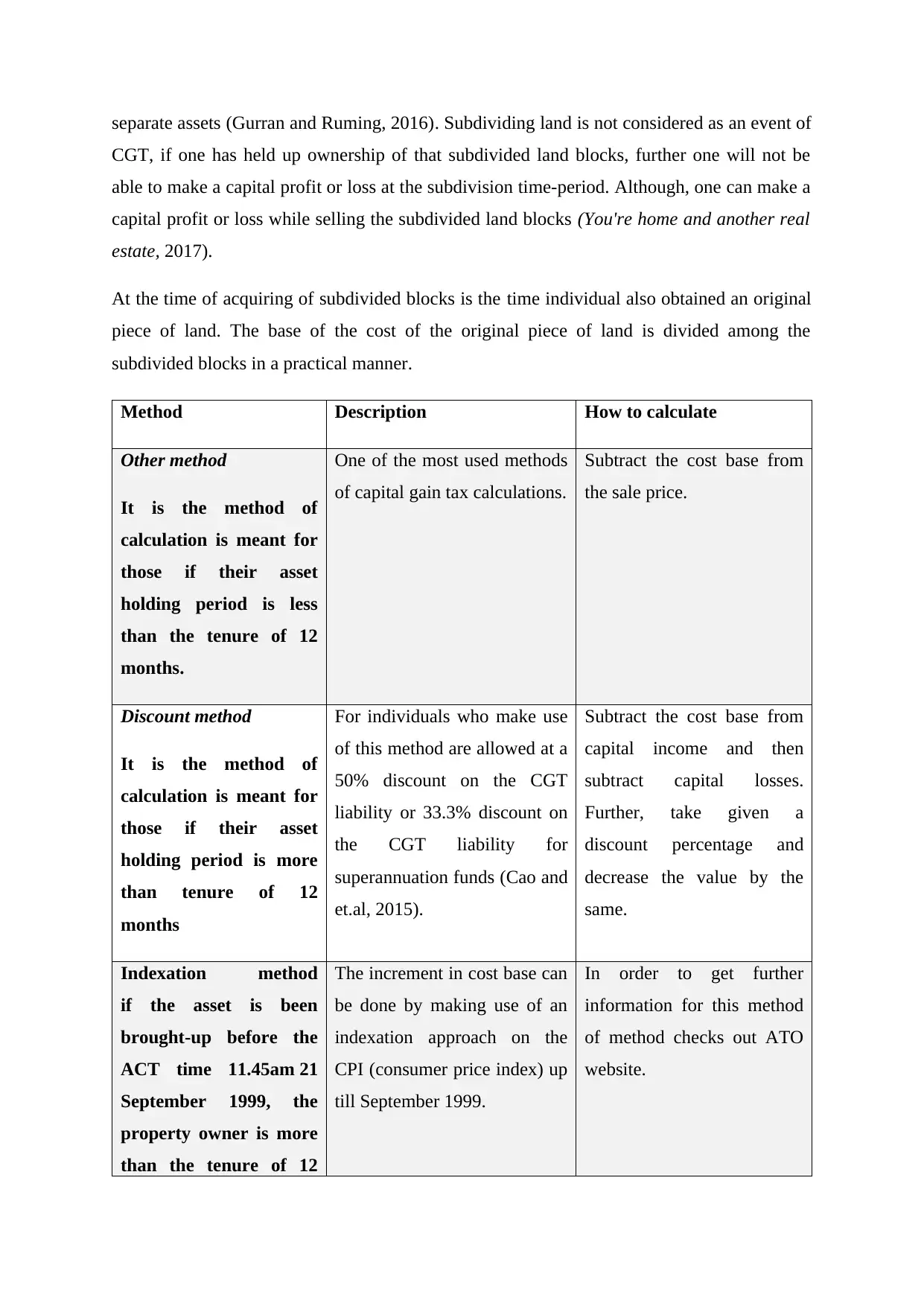

Subdividing land

Is someone subdivides their land block; each block will be given a separate title. For

the purpose of CGT, the original piece of land will be divided in more than two or two

property, 2017). In this event, the individual is allowed to an extended six-month period as

long as the new place will be considered as their new main residential place. The individual

resides in the old premises for continuous 3 months in the specified time period of 12 months

prior to sell it and it cannot be used to generate rent on that specified period (AO, 2015). The

Australian taxation office does not provides a precise justification of what is needed to form

up the main dwelling, but has given following factors to be taken into account:

Individual and his/her family resides in the residence

Mail has to be delivered on the residential address

Personal possessions must be at the residential place

Registration of vote must be done on the residential address

Connection of gas, phone and electricity to the premises

If a person has lived in their home from the start it was purchased and had not been

rented out either entirely or to a tenant and the size of land must be smaller than 2 hectares,

further, the individual will be entitled a full exception on Capital gain tax during its sale. This

will be useful while planning to live the life of renovator; selling the old one and purchasing

new, renovation and further putting the renovated premises into a sale (Jones, 2015). If at the

same time the individual is not able to earn rental income if individual go down this path, all

profits attained through the process renovation is exempted from CGT.

The main residential place is usually CGT exempted unless and until one has used it rent it

out or to run a business or the land is than 2 hectares.

Most significant factors to consider are:

Lodge records of the real estate, inclusive of own resident (if in near future one wants

to put that on rent or to run a business)

Keep in mind that while selling real estate, at the time (in which one incurs a capital

profit or loss) is when individuals makes an agreement, not at the time of settling.

Subdividing land

Is someone subdivides their land block; each block will be given a separate title. For

the purpose of CGT, the original piece of land will be divided in more than two or two

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

separate assets (Gurran and Ruming, 2016). Subdividing land is not considered as an event of

CGT, if one has held up ownership of that subdivided land blocks, further one will not be

able to make a capital profit or loss at the subdivision time-period. Although, one can make a

capital profit or loss while selling the subdivided land blocks (You're home and another real

estate, 2017).

At the time of acquiring of subdivided blocks is the time individual also obtained an original

piece of land. The base of the cost of the original piece of land is divided among the

subdivided blocks in a practical manner.

Method Description How to calculate

Other method

It is the method of

calculation is meant for

those if their asset

holding period is less

than the tenure of 12

months.

One of the most used methods

of capital gain tax calculations.

Subtract the cost base from

the sale price.

Discount method

It is the method of

calculation is meant for

those if their asset

holding period is more

than tenure of 12

months

For individuals who make use

of this method are allowed at a

50% discount on the CGT

liability or 33.3% discount on

the CGT liability for

superannuation funds (Cao and

et.al, 2015).

Subtract the cost base from

capital income and then

subtract capital losses.

Further, take given a

discount percentage and

decrease the value by the

same.

Indexation method

if the asset is been

brought-up before the

ACT time 11.45am 21

September 1999, the

property owner is more

than the tenure of 12

The increment in cost base can

be done by making use of an

indexation approach on the

CPI (consumer price index) up

till September 1999.

In order to get further

information for this method

of method checks out ATO

website.

CGT, if one has held up ownership of that subdivided land blocks, further one will not be

able to make a capital profit or loss at the subdivision time-period. Although, one can make a

capital profit or loss while selling the subdivided land blocks (You're home and another real

estate, 2017).

At the time of acquiring of subdivided blocks is the time individual also obtained an original

piece of land. The base of the cost of the original piece of land is divided among the

subdivided blocks in a practical manner.

Method Description How to calculate

Other method

It is the method of

calculation is meant for

those if their asset

holding period is less

than the tenure of 12

months.

One of the most used methods

of capital gain tax calculations.

Subtract the cost base from

the sale price.

Discount method

It is the method of

calculation is meant for

those if their asset

holding period is more

than tenure of 12

months

For individuals who make use

of this method are allowed at a

50% discount on the CGT

liability or 33.3% discount on

the CGT liability for

superannuation funds (Cao and

et.al, 2015).

Subtract the cost base from

capital income and then

subtract capital losses.

Further, take given a

discount percentage and

decrease the value by the

same.

Indexation method

if the asset is been

brought-up before the

ACT time 11.45am 21

September 1999, the

property owner is more

than the tenure of 12

The increment in cost base can

be done by making use of an

indexation approach on the

CPI (consumer price index) up

till September 1999.

In order to get further

information for this method

of method checks out ATO

website.

months

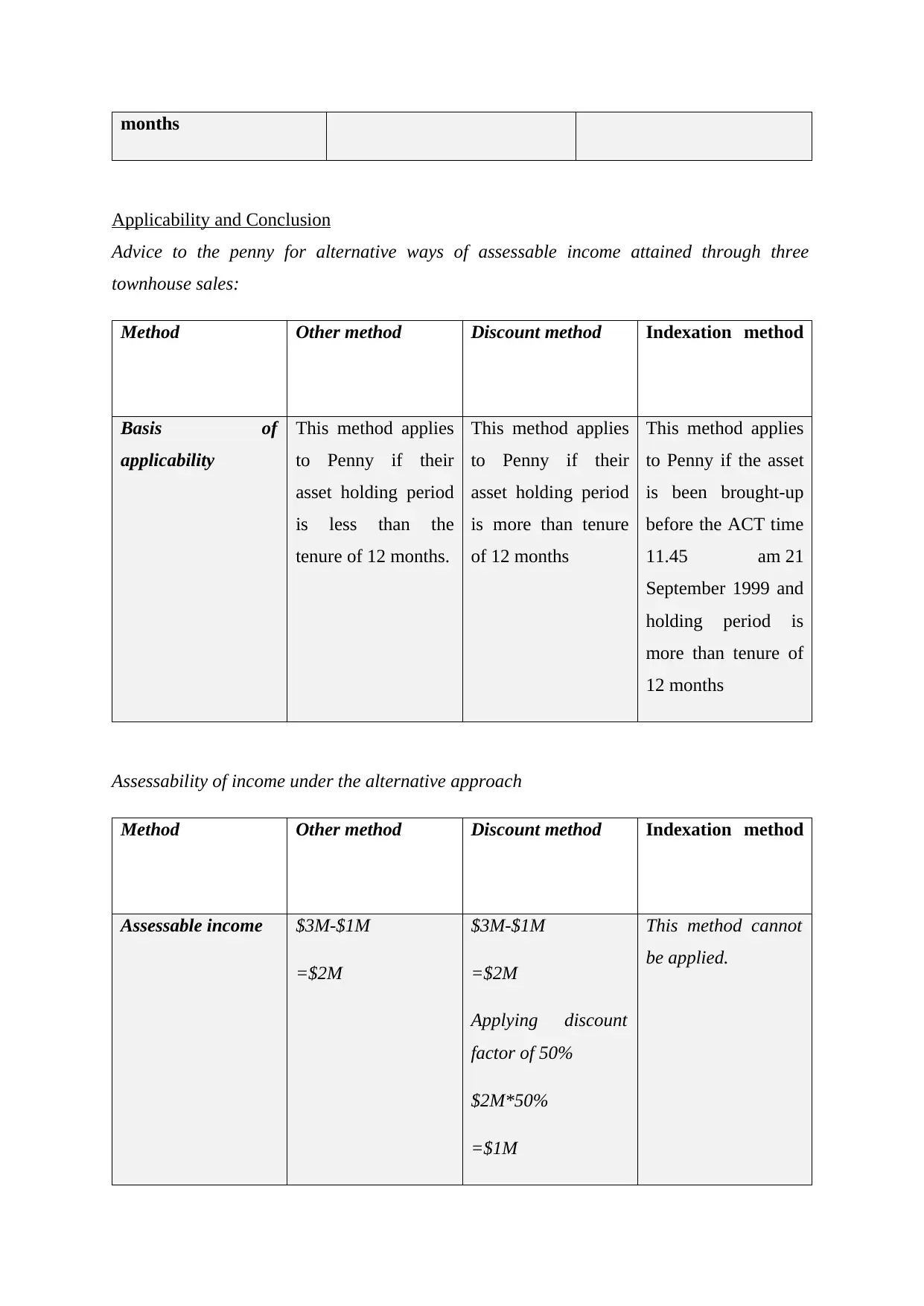

Applicability and Conclusion

Advice to the penny for alternative ways of assessable income attained through three

townhouse sales:

Method Other method Discount method Indexation method

Basis of

applicability

This method applies

to Penny if their

asset holding period

is less than the

tenure of 12 months.

This method applies

to Penny if their

asset holding period

is more than tenure

of 12 months

This method applies

to Penny if the asset

is been brought-up

before the ACT time

11.45 am 21

September 1999 and

holding period is

more than tenure of

12 months

Assessability of income under the alternative approach

Method Other method Discount method Indexation method

Assessable income $3M-$1M

=$2M

$3M-$1M

=$2M

Applying discount

factor of 50%

$2M*50%

=$1M

This method cannot

be applied.

Applicability and Conclusion

Advice to the penny for alternative ways of assessable income attained through three

townhouse sales:

Method Other method Discount method Indexation method

Basis of

applicability

This method applies

to Penny if their

asset holding period

is less than the

tenure of 12 months.

This method applies

to Penny if their

asset holding period

is more than tenure

of 12 months

This method applies

to Penny if the asset

is been brought-up

before the ACT time

11.45 am 21

September 1999 and

holding period is

more than tenure of

12 months

Assessability of income under the alternative approach

Method Other method Discount method Indexation method

Assessable income $3M-$1M

=$2M

$3M-$1M

=$2M

Applying discount

factor of 50%

$2M*50%

=$1M

This method cannot

be applied.

Correct outcome in this case

In accordance with the given case facts; other method will be applied because holding period

of a new block of land will be considered as the previous transaction of selling a land in

against of $1M is exempted as it was her main residence so same will not be covered under

purview assessable income. In this aspect; it has been assumed that Penny resides in the old

premises for continuous 3 months in the specified time period of 12 months prior to sell it

and it is not used to generate rent on that specified period. It is because; case description

clearly states that it is her old main residence in which she resides with her family

On selling the three units provisions of divisions will be applicable in which she subdivides

their land block; each block will be given a separate title. For the purpose of CGT, the

original piece of land is divided in four separate assets. Subdividing land is not considered as

an event of CGT, as she has hold ownership of that subdivided land blocks, further she will

not be able to make a capital profit or loss at the subdivision time-period. Although, she has

to pay tax on capital profit or loss while selling the subdivided land blocks (You're home and

another real estate, 2017).Thus; cost of block of land will be considered as acquisition cost

and due to absence of specific facts more prudent assumption is that holding period of asset is

less than 12 months as block has been purchased and construction has been started on the

same. Henceforth; assessable income for this transaction will be $2M.

In accordance with the given case facts; other method will be applied because holding period

of a new block of land will be considered as the previous transaction of selling a land in

against of $1M is exempted as it was her main residence so same will not be covered under

purview assessable income. In this aspect; it has been assumed that Penny resides in the old

premises for continuous 3 months in the specified time period of 12 months prior to sell it

and it is not used to generate rent on that specified period. It is because; case description

clearly states that it is her old main residence in which she resides with her family

On selling the three units provisions of divisions will be applicable in which she subdivides

their land block; each block will be given a separate title. For the purpose of CGT, the

original piece of land is divided in four separate assets. Subdividing land is not considered as

an event of CGT, as she has hold ownership of that subdivided land blocks, further she will

not be able to make a capital profit or loss at the subdivision time-period. Although, she has

to pay tax on capital profit or loss while selling the subdivided land blocks (You're home and

another real estate, 2017).Thus; cost of block of land will be considered as acquisition cost

and due to absence of specific facts more prudent assumption is that holding period of asset is

less than 12 months as block has been purchased and construction has been started on the

same. Henceforth; assessable income for this transaction will be $2M.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Books and Journals

AO, M.D.A., 2015. Modernising the Australian Taxation Office: Vision, people, systems and

values. eJournal of Tax Research, 13(1), p.1.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Gurran, N. and Ruming, K., 2016. Less planning, more development? Housing and urban

reform discourses in Australia. Journal of Economic Policy Reform, 19(3), pp.262-280.

Jones, S., 2015. Your primary residence and CGT: capital gains tax. Tax Breaks

Newsletter, 2015(351), pp.5-6.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Online

2.1.2.10 Residence Requirements. 2017. [Online]. Available through

<http://guides.dss.gov.au/family-assistance-guide/2/1/2/10>. [Accessed on 2nd October 2017].

Residency tests. 2016. [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-your-tax-

residency/Residency-tests/>. [Accessed on 2nd October 2017].

Valuation methods – property. 2017. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/In-detail/Market-valuations/Market-

valuation-for-tax-purposes/?page=10>. [Accessed on 2nd October 2017].

Your home and other real estate. 2017. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/>.

[Accessed on 2nd October 2017].

Books and Journals

AO, M.D.A., 2015. Modernising the Australian Taxation Office: Vision, people, systems and

values. eJournal of Tax Research, 13(1), p.1.

Bevacqua, J., 2015. ATO accountability and taxpayer fairness: An assessment of the proposal

to split the Australian taxation office. UNSWLJ, 38, p.995.

Cao, L., Hosking, A., Kouparitsas, M., Mullaly, D., Rimmer, X., Shi, Q., Stark, W. and

Wende, S., 2015. Understanding the economy-wide efficiency and incidence of major

Australian taxes. Treasury WP, 1.

Gurran, N. and Ruming, K., 2016. Less planning, more development? Housing and urban

reform discourses in Australia. Journal of Economic Policy Reform, 19(3), pp.262-280.

Jones, S., 2015. Your primary residence and CGT: capital gains tax. Tax Breaks

Newsletter, 2015(351), pp.5-6.

Saad, N., 2014. Tax knowledge, tax complexity and tax compliance: Taxpayers’

view. Procedia-Social and Behavioral Sciences, 109, pp.1069-1075.

Online

2.1.2.10 Residence Requirements. 2017. [Online]. Available through

<http://guides.dss.gov.au/family-assistance-guide/2/1/2/10>. [Accessed on 2nd October 2017].

Residency tests. 2016. [Online]. Available through

<https://www.ato.gov.au/Individuals/International-tax-for-individuals/Work-out-your-tax-

residency/Residency-tests/>. [Accessed on 2nd October 2017].

Valuation methods – property. 2017. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/In-detail/Market-valuations/Market-

valuation-for-tax-purposes/?page=10>. [Accessed on 2nd October 2017].

Your home and other real estate. 2017. [Online]. Available through

<https://www.ato.gov.au/General/Capital-gains-tax/Your-home-and-other-real-estate/>.

[Accessed on 2nd October 2017].

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.