Taxation Law: Income, Tax Avoidance, and Property Ownership Analysis

VerifiedAdded on 2023/06/05

|12

|2923

|122

Report

AI Summary

This report delves into various aspects of taxation law. It begins by analyzing whether an annual lottery prize payment constitutes income under the ordinary concepts of Section 6-5 of the ITAA 1997, referencing relevant case law such as Scott v CT and FCT v Blake. The report then examines the principle of tax avoidance established in IRC v Duke of Westminster, discussing its application and relevance in modern Australian tax law. Finally, it addresses the legal implications of joint ownership of rental property, specifically focusing on the treatment of joint owners for income tax purposes, referencing Taxation Ruling TR 93/32 and the case of FC of T v McDonald, and concluding with the application of these principles to a case study involving joint owners Joseph and Jane and their rental property.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................6

References:...............................................................................................................................10

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to question 2:.................................................................................................................4

Answer to question 3:.................................................................................................................4

Answer to question 4:.................................................................................................................6

References:...............................................................................................................................10

2TAXATION LAW

Answer to question 1:

Issues:

Whether the annual payment received by the taxpayer will be treated as the income

with respect to the ordinary sense of “S 6-5, ITAA 1997”?

Laws:

The doctrine of constructive receipt stated under section 6-5 states that an individual

is considered to have received the sum when it is dealt in a manner as directed by the

taxpayer. The taxable income comprises of the ordinary income and statutory income. The

ordinary income forms the part of the taxable income of the taxpayer under “section 6-5,

ITAA 1997” (Miller and Oats 2016). There are certain amount that are not treated as the

taxable income but they are included into the taxpayer’s taxable income based on the specific

provision of the Act.

As per the “section 6-5, ITAA 1997” the taxable income of the taxpayer also includes

the income within the meaning of the ordinary concepts which is better known as the

ordinary income. The court of law in “Scott v CT (1935)” held that income should not be

viewed as the term of art (James and Nobes 2016). It requires application of necessary

principles in determining that the how much of the receipts should be treated as the income

within the ordinary concepts and usages.

Gains generally requires the characterisation by the law court in ascertaining whether

the gains has the character of income. A receipt cannot be treated as the income within the

ordinary meaning unless it is cash or convertible to cash or real gain for the taxpayer

(Fleurbaey and Maniquet 2018). If the taxpayer meets the criteria of both the perquisites of

income then the gain will be treated as the ordinary income if the amount reflects the

Answer to question 1:

Issues:

Whether the annual payment received by the taxpayer will be treated as the income

with respect to the ordinary sense of “S 6-5, ITAA 1997”?

Laws:

The doctrine of constructive receipt stated under section 6-5 states that an individual

is considered to have received the sum when it is dealt in a manner as directed by the

taxpayer. The taxable income comprises of the ordinary income and statutory income. The

ordinary income forms the part of the taxable income of the taxpayer under “section 6-5,

ITAA 1997” (Miller and Oats 2016). There are certain amount that are not treated as the

taxable income but they are included into the taxpayer’s taxable income based on the specific

provision of the Act.

As per the “section 6-5, ITAA 1997” the taxable income of the taxpayer also includes

the income within the meaning of the ordinary concepts which is better known as the

ordinary income. The court of law in “Scott v CT (1935)” held that income should not be

viewed as the term of art (James and Nobes 2016). It requires application of necessary

principles in determining that the how much of the receipts should be treated as the income

within the ordinary concepts and usages.

Gains generally requires the characterisation by the law court in ascertaining whether

the gains has the character of income. A receipt cannot be treated as the income within the

ordinary meaning unless it is cash or convertible to cash or real gain for the taxpayer

(Fleurbaey and Maniquet 2018). If the taxpayer meets the criteria of both the perquisites of

income then the gain will be treated as the ordinary income if the amount reflects the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

characteristics of regular or periodic receipts. Gains having the character of regular or

periodic is most likely to be treated as the ordinary income then the gains that are paid in the

form of lump sum. The court in “FCT v Blake” held that regular or periodic receipts possess

the character of income.

Similarly in “Kelly v FCT” the commissioner of taxation assessed the taxpayer based

on the regularity and recurrence rule (Mau and Liebig 2016). The opinion of the court

included that the gains that are one of the number and involves periodicity will be treated as

the income. Evidently in the case of “FCT v Dixon” the periodic receipts are treated as

income since the sum was payable periodically or at least annually.

Application:

The annual payment of lottery winning prize will be treated as income under the

ordinary meaning of “S 6-5, ITAA 1997”. Denoting the explanation of commissioner in

“Scott v CT (1935)” the value of $50,000 will be classified as income because the receipts is

a real gain for the taxpayer and has met both the requisite of ordinary income.

Citing the event of “FCT v Blake” the annual payment of $50,000 not only

constitutes a real gain for the taxpayer but also has the character of income based on the

principles of recurrence or regularity of receipts (Kabinga 2015). Referring to “Kelly v FCT”

the annual payment of $50,000 will be assessed based on the regularity and recurrence rule.

This is because the gains are one of the number and involves periodicity therefore it will be

treated as the income. Therefore, denoting the event of “FCT v Blake” the annual payment of

$50,000 will be treated as income since the sum was payable periodically or at least annually.

Conclusion:

characteristics of regular or periodic receipts. Gains having the character of regular or

periodic is most likely to be treated as the ordinary income then the gains that are paid in the

form of lump sum. The court in “FCT v Blake” held that regular or periodic receipts possess

the character of income.

Similarly in “Kelly v FCT” the commissioner of taxation assessed the taxpayer based

on the regularity and recurrence rule (Mau and Liebig 2016). The opinion of the court

included that the gains that are one of the number and involves periodicity will be treated as

the income. Evidently in the case of “FCT v Dixon” the periodic receipts are treated as

income since the sum was payable periodically or at least annually.

Application:

The annual payment of lottery winning prize will be treated as income under the

ordinary meaning of “S 6-5, ITAA 1997”. Denoting the explanation of commissioner in

“Scott v CT (1935)” the value of $50,000 will be classified as income because the receipts is

a real gain for the taxpayer and has met both the requisite of ordinary income.

Citing the event of “FCT v Blake” the annual payment of $50,000 not only

constitutes a real gain for the taxpayer but also has the character of income based on the

principles of recurrence or regularity of receipts (Kabinga 2015). Referring to “Kelly v FCT”

the annual payment of $50,000 will be assessed based on the regularity and recurrence rule.

This is because the gains are one of the number and involves periodicity therefore it will be

treated as the income. Therefore, denoting the event of “FCT v Blake” the annual payment of

$50,000 will be treated as income since the sum was payable periodically or at least annually.

Conclusion:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

The discussion made above clearly defines that the annual payment involves

recurrence and regular payment. Therefore, the sum of $50,000 will be treated as income

under the ordinary concepts of “section 6-5, ITAA 1997”.

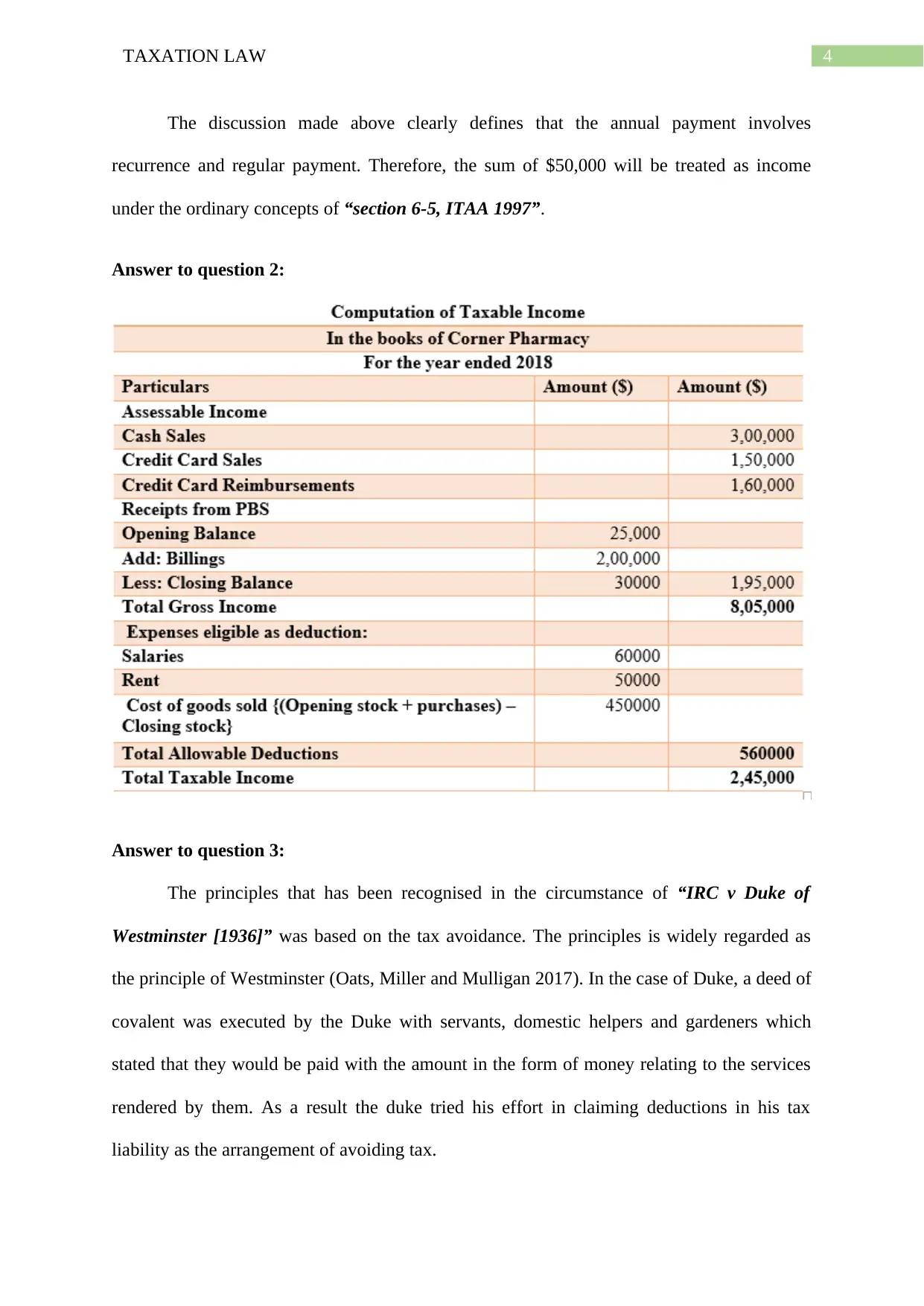

Answer to question 2:

Answer to question 3:

The principles that has been recognised in the circumstance of “IRC v Duke of

Westminster [1936]” was based on the tax avoidance. The principles is widely regarded as

the principle of Westminster (Oats, Miller and Mulligan 2017). In the case of Duke, a deed of

covalent was executed by the Duke with servants, domestic helpers and gardeners which

stated that they would be paid with the amount in the form of money relating to the services

rendered by them. As a result the duke tried his effort in claiming deductions in his tax

liability as the arrangement of avoiding tax.

The discussion made above clearly defines that the annual payment involves

recurrence and regular payment. Therefore, the sum of $50,000 will be treated as income

under the ordinary concepts of “section 6-5, ITAA 1997”.

Answer to question 2:

Answer to question 3:

The principles that has been recognised in the circumstance of “IRC v Duke of

Westminster [1936]” was based on the tax avoidance. The principles is widely regarded as

the principle of Westminster (Oats, Miller and Mulligan 2017). In the case of Duke, a deed of

covalent was executed by the Duke with servants, domestic helpers and gardeners which

stated that they would be paid with the amount in the form of money relating to the services

rendered by them. As a result the duke tried his effort in claiming deductions in his tax

liability as the arrangement of avoiding tax.

5TAXATION LAW

The principles that was established in Duke’s case was that taxpayers as well as the

companies are permitted to arrange their financial statement in such a way that they does not

breach the terms of law while lowering their tax liabilities (Basu 2016). The principle that

was established in Duke’s case was of apparently purposive method of not revealing the

original character of the transaction that was entered with the legitimate sole purpose of tax

avoidance. The principle that was established in the case of Duke has developed into the

collective practice of cancelling the transaction which was entered with no legal purpose but

to change the nature of profits, loss or appropriation.

As obvious from the case of “IRC v Duke of Westminster [1936]” the pay could be

treated as permissible deductions given the payment was yearly in character to the servants

and gardeners (Sikka 2017). Under such circumstances that was only permitted to claim the

permissible tax deductions for the yearly payment that was made for the services that was

rendered by the servants and gardeners. The Duke’s case stands as the suggestion that

avoiding tax is allowed until and unless it follows the recognised act (Weichenrieder 2018).

The circumstances of the Duke explained that the basic principles which was established

related to the deed of covalent that can assist in reducing the liability of taxation. The tax

liability can be only reduced if it is permitted under the act and claims are made for only the

annual payment.

The relevant principle established in the Duke case in the modern age of Australia as

the principle of tax avoidance. However, the government of Australia in the recent years has

made an extended work in reducing the gap of taxation (Mellon 2016). As understood from

the preceding discussion the Australian government has made an effort in increasing the

revenue through extensive collection of tax where the taxpayers are required to make plan for

paying the less amount of tax. The principle that was established in the Duke was can be

The principles that was established in Duke’s case was that taxpayers as well as the

companies are permitted to arrange their financial statement in such a way that they does not

breach the terms of law while lowering their tax liabilities (Basu 2016). The principle that

was established in Duke’s case was of apparently purposive method of not revealing the

original character of the transaction that was entered with the legitimate sole purpose of tax

avoidance. The principle that was established in the case of Duke has developed into the

collective practice of cancelling the transaction which was entered with no legal purpose but

to change the nature of profits, loss or appropriation.

As obvious from the case of “IRC v Duke of Westminster [1936]” the pay could be

treated as permissible deductions given the payment was yearly in character to the servants

and gardeners (Sikka 2017). Under such circumstances that was only permitted to claim the

permissible tax deductions for the yearly payment that was made for the services that was

rendered by the servants and gardeners. The Duke’s case stands as the suggestion that

avoiding tax is allowed until and unless it follows the recognised act (Weichenrieder 2018).

The circumstances of the Duke explained that the basic principles which was established

related to the deed of covalent that can assist in reducing the liability of taxation. The tax

liability can be only reduced if it is permitted under the act and claims are made for only the

annual payment.

The relevant principle established in the Duke case in the modern age of Australia as

the principle of tax avoidance. However, the government of Australia in the recent years has

made an extended work in reducing the gap of taxation (Mellon 2016). As understood from

the preceding discussion the Australian government has made an effort in increasing the

revenue through extensive collection of tax where the taxpayers are required to make plan for

paying the less amount of tax. The principle that was established in the Duke was can be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

applied in the present age of Australia by stating that the tax avoidance is viewed as a

person’s effort in avoiding the duty from the community.

Answer to question 4:

Issues:

The issue here is based on determining whether the joint owners of the rental property

are treated as the owners under the general law?

Rule:

As specified in “taxation ruling of TR 93/32” an examination of the taxpayer’s

position based on joint ownership whose activities does not comprises of performing of the

business. The ruling is helpful in providing explanation based on which the taxation

commissioner will accept splitting of net income and net loss originating from the rental

property among the joint owners for the taxation purpose (Genser and Holzmann 2016). The

ruling explains that the joint owners of the property that is rented out represents the

partnership relating to the income tax purpose but the joint ownership does not amount to the

partnership based on the general law.

Under the “taxation ruling of TR 93/32”the joint owners of the rental property are

usually not treated as the partners under the general law (Keen and Mullins 2017). The

agreement relating to partnership among the joint owners regardless of whether in oral or

writing does not has any impact on the share of rental property net income or net losses.

applied in the present age of Australia by stating that the tax avoidance is viewed as a

person’s effort in avoiding the duty from the community.

Answer to question 4:

Issues:

The issue here is based on determining whether the joint owners of the rental property

are treated as the owners under the general law?

Rule:

As specified in “taxation ruling of TR 93/32” an examination of the taxpayer’s

position based on joint ownership whose activities does not comprises of performing of the

business. The ruling is helpful in providing explanation based on which the taxation

commissioner will accept splitting of net income and net loss originating from the rental

property among the joint owners for the taxation purpose (Genser and Holzmann 2016). The

ruling explains that the joint owners of the property that is rented out represents the

partnership relating to the income tax purpose but the joint ownership does not amount to the

partnership based on the general law.

Under the “taxation ruling of TR 93/32”the joint owners of the rental property are

usually not treated as the partners under the general law (Keen and Mullins 2017). The

agreement relating to partnership among the joint owners regardless of whether in oral or

writing does not has any impact on the share of rental property net income or net losses.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

The term ownership expresses a form of entitlement to use the highest amount of the

lawful interest on what is owned. Joint holders of the rental property will be holding the

property in the form of joint owners (Bamford 2018). One of the most important aspect for

joint owners and tenants in common is that they will hold the rental property in their legal

interest. The lawful interest that ultimately determines dividing of net income and net profit

amid the joint owners of the property.

Joint owners of the property are the joint tenants that have similar lawful interest in

the property (Woellner et al. 2016). This signifies that the property holders should be sharing

the net losses and profit based on 50% share with necessary requisite feature are existent for

the joint owners of that property.

Referring to the general suggestion that was made, it is very appropriate to explain the

owners of the property that are rented out in the McDonalds case as the joint holders in

investment apart from treating as the partners in the business operations (Bankman et al.

2017). As a result of this, the rental property joint owners are not treated as the partners under

the general law based on the result that they are not subjected to general law of partnership

including both the profits and loss from the property.

In “FC of T v McDonald (1987)” the taxpayer and his wife both legitimately owned

two units as the joint owners (Schenk 2017). The taxpayer rented out both the property. The

arrangement of partnership was made in such a manner that Mr McDonald would be entitled

to only 25% of the net income from the rental property while the remaining 75% of the net

income would be allocated to Mrs McDonald. The arrangement of the partnership between

the husband and wife was such that Mr McDonald would be bearing full amount of loss that

is originating from the rental property.

The term ownership expresses a form of entitlement to use the highest amount of the

lawful interest on what is owned. Joint holders of the rental property will be holding the

property in the form of joint owners (Bamford 2018). One of the most important aspect for

joint owners and tenants in common is that they will hold the rental property in their legal

interest. The lawful interest that ultimately determines dividing of net income and net profit

amid the joint owners of the property.

Joint owners of the property are the joint tenants that have similar lawful interest in

the property (Woellner et al. 2016). This signifies that the property holders should be sharing

the net losses and profit based on 50% share with necessary requisite feature are existent for

the joint owners of that property.

Referring to the general suggestion that was made, it is very appropriate to explain the

owners of the property that are rented out in the McDonalds case as the joint holders in

investment apart from treating as the partners in the business operations (Bankman et al.

2017). As a result of this, the rental property joint owners are not treated as the partners under

the general law based on the result that they are not subjected to general law of partnership

including both the profits and loss from the property.

In “FC of T v McDonald (1987)” the taxpayer and his wife both legitimately owned

two units as the joint owners (Schenk 2017). The taxpayer rented out both the property. The

arrangement of partnership was made in such a manner that Mr McDonald would be entitled

to only 25% of the net income from the rental property while the remaining 75% of the net

income would be allocated to Mrs McDonald. The arrangement of the partnership between

the husband and wife was such that Mr McDonald would be bearing full amount of loss that

is originating from the rental property.

8TAXATION LAW

The taxation commissioner contended that there was no partnership under the general

law. The only relevant partnership between the husband and wife was that of the joint

ownership (Murphy and Higgins 2016). Since the parties were the joint owners of the

property they must share the loss and profit equally based on the outcome that the

respondents should be entitled to half portion of the loss. Evidently, both the husband and

wife were the joint owners of the property, their arrangement of sharing income and loss in

the different percentage will be entirely unsuccessful.

Application:

The case study provides that Joseph and Jane are the joint owners of the rental

property. Their arrangement included sharing of profit and loss of 20% to Joseph while 80%

of the net income to Jane. The arrangement of partnership also required Joseph to shoulder

the full amount of loss. A reference can be made relating to the interpretation stated in

“taxation ruling of TR 93/32” that the Joseph and Jane will be treated as the joint owners for

the income tax purpose but not the joint owners under the general law (Schmalbeck, Zelenak

and Lawsky 2015). The agreement relating to partnership between Joseph and Jane regardless

of whether in oral or writing does not has any impact on the share of rental property net

income or net losses.

As Joseph and Jane are the joint holders of the rental property, they will be holding

that property in their legal interest. This indicates that Joseph and Jane being the joint holders

should be sharing the net losses and profit based on 50% share since necessary requisite

feature of co-ownership are existent in that property (Simmons et al. 2017). Since Joseph and

Jane are the joint owners of the rental property they will not be treated as the partners under

the general law based on the result that they are not subjected to general law of partnership

including both the profits and loss derived from the property.

The taxation commissioner contended that there was no partnership under the general

law. The only relevant partnership between the husband and wife was that of the joint

ownership (Murphy and Higgins 2016). Since the parties were the joint owners of the

property they must share the loss and profit equally based on the outcome that the

respondents should be entitled to half portion of the loss. Evidently, both the husband and

wife were the joint owners of the property, their arrangement of sharing income and loss in

the different percentage will be entirely unsuccessful.

Application:

The case study provides that Joseph and Jane are the joint owners of the rental

property. Their arrangement included sharing of profit and loss of 20% to Joseph while 80%

of the net income to Jane. The arrangement of partnership also required Joseph to shoulder

the full amount of loss. A reference can be made relating to the interpretation stated in

“taxation ruling of TR 93/32” that the Joseph and Jane will be treated as the joint owners for

the income tax purpose but not the joint owners under the general law (Schmalbeck, Zelenak

and Lawsky 2015). The agreement relating to partnership between Joseph and Jane regardless

of whether in oral or writing does not has any impact on the share of rental property net

income or net losses.

As Joseph and Jane are the joint holders of the rental property, they will be holding

that property in their legal interest. This indicates that Joseph and Jane being the joint holders

should be sharing the net losses and profit based on 50% share since necessary requisite

feature of co-ownership are existent in that property (Simmons et al. 2017). Since Joseph and

Jane are the joint owners of the rental property they will not be treated as the partners under

the general law based on the result that they are not subjected to general law of partnership

including both the profits and loss derived from the property.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Stating the occasion of “FC of T v McDonald (1987)” both Joseph and Jane would be

entitled to share one half of the $50,000 loss that arise from subletting the property (Motro

2016). There was no partnership under the general law and the only relevant partnership that

prevailed between the husband and wife was that of the joint ownership.

In the alternative state of affairs, given that Joseph and Jane decides to sell the

property then the capital gains or the capital loss must be shared equally. As obvious, both

Joseph and Jane are the joint owners of the property, their arrangement of sharing income and

loss in the different percentage will be entirely ineffectual.

Conclusion:

The discussion stated above can be concluded by stating that the partnership between

Joseph and Jane is not a partnership under the general law. They must share all the losses and

income equally between themselves.

Stating the occasion of “FC of T v McDonald (1987)” both Joseph and Jane would be

entitled to share one half of the $50,000 loss that arise from subletting the property (Motro

2016). There was no partnership under the general law and the only relevant partnership that

prevailed between the husband and wife was that of the joint ownership.

In the alternative state of affairs, given that Joseph and Jane decides to sell the

property then the capital gains or the capital loss must be shared equally. As obvious, both

Joseph and Jane are the joint owners of the property, their arrangement of sharing income and

loss in the different percentage will be entirely ineffectual.

Conclusion:

The discussion stated above can be concluded by stating that the partnership between

Joseph and Jane is not a partnership under the general law. They must share all the losses and

income equally between themselves.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

References:

Bamford, D., 2018. Arguing for a New Form of Taxation: Lifetime Hourly

Averaging. Journal of Applied Philosophy, 35(2), pp.280-299.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Genser, B. and Holzmann, R., 2016. The taxation of internationally portable pensions: Fiscal

issues and policy options.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Kabinga, M., 2015. Established principles of taxation. Tax justice & poverty.

Keen, M. and Mullins, P., 2017. International corporate taxation and the extractive industries:

principles, practice, problems. International Taxation and the Extractive Industries, New

York and London: Routledge.

Mau, S. and Liebig, S., 2016. When is a Taxation System Just? Attitudes towards General

Taxation Principles and towards the Justice of One’s Own Tax Burden. In Social Justice,

Legitimacy and the Welfare State (pp. 115-140). Routledge.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

References:

Bamford, D., 2018. Arguing for a New Form of Taxation: Lifetime Hourly

Averaging. Journal of Applied Philosophy, 35(2), pp.280-299.

Bankman, J., Shaviro, D.N., Stark, K.J. and Kleinbard, E.D., 2017. Federal Income Taxation.

Wolters Kluwer Law & Business.

Basu, S., 2016. Global perspectives on e-commerce taxation law. Routledge.

Fleurbaey, M. and Maniquet, F., 2018. Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), pp.1029-79.

Genser, B. and Holzmann, R., 2016. The taxation of internationally portable pensions: Fiscal

issues and policy options.

James, S.R. and Nobes, C., 2016. Economics of Taxation: Principles, Policy and Practice.

Fiscal Publications.

Kabinga, M., 2015. Established principles of taxation. Tax justice & poverty.

Keen, M. and Mullins, P., 2017. International corporate taxation and the extractive industries:

principles, practice, problems. International Taxation and the Extractive Industries, New

York and London: Routledge.

Mau, S. and Liebig, S., 2016. When is a Taxation System Just? Attitudes towards General

Taxation Principles and towards the Justice of One’s Own Tax Burden. In Social Justice,

Legitimacy and the Welfare State (pp. 115-140). Routledge.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Miller, A. and Oats, L., 2016. Principles of international taxation. Bloomsbury Publishing.

11TAXATION LAW

Motro, S., 2016. The Income Tax Map: A Bird's-eye View of Federal Income Taxation for

Law Students.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Oats, L., Miller, A. and Mulligan, E., 2017. Principles of International Taxation.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Simmons, D.L., McMahon, M.J., Borden, B.T. and Ventry, D.J., 2017. Federal Income

Taxation. Foundation Press.

Weichenrieder, A., 2018. Digitalization and taxation: Beware ad hoc measures (No. 64).

SAFE Policy Letter.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Motro, S., 2016. The Income Tax Map: A Bird's-eye View of Federal Income Taxation for

Law Students.

Murphy, K.E. and Higgins, M., 2016. Concepts in Federal Taxation 2017. Cengage

Learning.

Oats, L., Miller, A. and Mulligan, E., 2017. Principles of International Taxation.

Schenk, D.H., 2017. Federal Taxation of S Corporations. Law Journal Press.

Schmalbeck, R., Zelenak, L. and Lawsky, S.B., 2015. Federal Income Taxation. Wolters

Kluwer Law & Business.

Sikka, P., 2017, December. Accounting and taxation: Conjoined twins or separate siblings?.

In Accounting forum(Vol. 41, No. 4, pp. 390-405). Elsevier.

Simmons, D.L., McMahon, M.J., Borden, B.T. and Ventry, D.J., 2017. Federal Income

Taxation. Foundation Press.

Weichenrieder, A., 2018. Digitalization and taxation: Beware ad hoc measures (No. 64).

SAFE Policy Letter.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.