Taxation Law: Income Tax Computation and Deductibility of Expenses

VerifiedAdded on 2023/06/11

|11

|2161

|202

AI Summary

This article discusses income taxation computation and deductibility of expenses under Taxation Law. It analyzes the impact of taxes on transactions such as winning cash prizes, appearance on television, receipts from salaries and receipts from sports events. The article also explains the rules and applications of various sections of the ITAA 1997 and FBTAA 1986. It concludes with a working note and reference list.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Headings:....................................................................................................................................2

Issue/ Problem presented in the case:.........................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Reference List:...........................................................................................................................8

Table of Contents

Headings:....................................................................................................................................2

Issue/ Problem presented in the case:.........................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................6

Reference List:...........................................................................................................................8

2TAXATION LAW

Headings:

The issue that is presented in the given case study is based on the income taxation

computation. This has been done for creating the taxation income and deductibility of the

expenses for the financial year 2017-2018.

Issue/ Problem presented in the case:

The given case about Kate who is a full time accountant and is concerned about the

consequences of taxes. It is required to make the assessment about the impact of taxes in

relation to the transactions such as winning the cash prize, appearance of television, receipts

from salaries and receipts from events of sports. It is required to ascertain that the collectables

from such transactions can be treated as capital gains tax. The section 8-1 of the ITAA 1997”

is analyzed in terms of whether Kate would be entitled for deductions related to travelling

(Eccleston and Smith 2015). Hence, it is required to answer whether the mentioned section

allow for the tax payer to enjoy the deductions associated with the travelling expenses.

Rule:

It is stated under the section 8-1 of the ITAA 1997 that the maximum earnings that is

earned by an individual are related as ordinary earnings. The section depicts that suich types

of earnings can be earned by individual from sources such as profits generated by them from

involvement in any trading activities or income generated from involvement in any private

jobs such as wages, allowances, bonus, salaries or any other prerequisites. It was held in the

“Scott v Commissioner of Taxation (1935)” that treats the word “income” as the required

principles and terms of art that is considered applicable when the agreement involves the

ordinary conceptions of mankind by treating the receipts as income (Torgler 2016).

When an employer provides benefits to employees during any particular financial

year in regard to the services offered, then such benefits are treated as fringe benefits under

Headings:

The issue that is presented in the given case study is based on the income taxation

computation. This has been done for creating the taxation income and deductibility of the

expenses for the financial year 2017-2018.

Issue/ Problem presented in the case:

The given case about Kate who is a full time accountant and is concerned about the

consequences of taxes. It is required to make the assessment about the impact of taxes in

relation to the transactions such as winning the cash prize, appearance of television, receipts

from salaries and receipts from events of sports. It is required to ascertain that the collectables

from such transactions can be treated as capital gains tax. The section 8-1 of the ITAA 1997”

is analyzed in terms of whether Kate would be entitled for deductions related to travelling

(Eccleston and Smith 2015). Hence, it is required to answer whether the mentioned section

allow for the tax payer to enjoy the deductions associated with the travelling expenses.

Rule:

It is stated under the section 8-1 of the ITAA 1997 that the maximum earnings that is

earned by an individual are related as ordinary earnings. The section depicts that suich types

of earnings can be earned by individual from sources such as profits generated by them from

involvement in any trading activities or income generated from involvement in any private

jobs such as wages, allowances, bonus, salaries or any other prerequisites. It was held in the

“Scott v Commissioner of Taxation (1935)” that treats the word “income” as the required

principles and terms of art that is considered applicable when the agreement involves the

ordinary conceptions of mankind by treating the receipts as income (Torgler 2016).

When an employer provides benefits to employees during any particular financial

year in regard to the services offered, then such benefits are treated as fringe benefits under

3TAXATION LAW

the “section 36 (1) of the FBTAA 1986”. Expenses on part of fringe benefits occur or it is

incurred by employer when such expenditure is incurred by employees and it is paid by

employer. Such expenses are treated as an expenditure on part of employer under the “section

20 of the FBTAA 1986”.

Income does not comprise of the ordinary awards that are received by individual.

Nonetheless, if there exists any satisfactory association or relationship of such awards with

the activities of the tax payer that generates earnings, then they are included in income. As

mentioned that an award for being the best and fairest player was received by the professional

footballer under “Kelly v FCT”. The sum that was received by the player as award had a

sufficient connection to the skills and incidental to his profession.

An amount received by the individual might be treated as income if it is derived from

personal exertion. Such income is taken into account for the assessment of income as

ordinary income or statutory income. If sufficient amount of relationship is found to exit

between the prize amount and the tax payer activities, then such amount received as award

should be treated as income. As indicated in the case of “FCT v Stone”, the tax payer

practiced two professions that is one as police and other as sports person that is thrower of

javelin. The tax payer in this case has two source of income that is salary that he or she

received as income from his police profession and involvement in sports also generated

income in the form of prize money and some endorsements. It was help by commissioner that

the income derived by tax payer by being a professional athlete should be treated as income

(Tran-Nam 2016).

Furthermore, taxable income takes into account of all the payments that are received

by individual for promotion, public appearance and endorsements. Therefore, the payment

the “section 36 (1) of the FBTAA 1986”. Expenses on part of fringe benefits occur or it is

incurred by employer when such expenditure is incurred by employees and it is paid by

employer. Such expenses are treated as an expenditure on part of employer under the “section

20 of the FBTAA 1986”.

Income does not comprise of the ordinary awards that are received by individual.

Nonetheless, if there exists any satisfactory association or relationship of such awards with

the activities of the tax payer that generates earnings, then they are included in income. As

mentioned that an award for being the best and fairest player was received by the professional

footballer under “Kelly v FCT”. The sum that was received by the player as award had a

sufficient connection to the skills and incidental to his profession.

An amount received by the individual might be treated as income if it is derived from

personal exertion. Such income is taken into account for the assessment of income as

ordinary income or statutory income. If sufficient amount of relationship is found to exit

between the prize amount and the tax payer activities, then such amount received as award

should be treated as income. As indicated in the case of “FCT v Stone”, the tax payer

practiced two professions that is one as police and other as sports person that is thrower of

javelin. The tax payer in this case has two source of income that is salary that he or she

received as income from his police profession and involvement in sports also generated

income in the form of prize money and some endorsements. It was help by commissioner that

the income derived by tax payer by being a professional athlete should be treated as income

(Tran-Nam 2016).

Furthermore, taxable income takes into account of all the payments that are received

by individual for promotion, public appearance and endorsements. Therefore, the payment

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

received by taxpayer in the case “Kelly v FCT” for public appearance should be treated as

taxable income.

For determination of capital gains in accordance with the “subsection 108-10 (1) of

the ITAA 1997” in order to decrease the capital gains from collectables should take into

account the amount of capital losses that is generated from collectibles. Collectibles under

“section 108-15 (1)” are liable as set. Collectibles on other hand are treated in the form of

disposal and are taken as single set under “section 108-15 (2) of the ITAA 1997” (Berg and

Davidson 2017). In addition to this, there is exemption of capital gains generated from the

acquisition of collectibles of amount $ 500 or less.

Rent is the amount that is paid by individual for using the person property. Rent is

accounted for assessing the income as taxable income as depicted in the case of “Adelaide

Fruit and Produce Exchange Co Ltd (1932)”.

Any item that the tax payer derives it as part of its income is treated as income until

its net value has been realised. As provided in the case of “Brent v FCT” that the media

company provided special rights to the train robber wife to make the publication of life story.

The amount that was received by her by way of such publication is held as income and it is

taken into account for assessing the income tax as it arise from the ordinary concepts of her

rewards (Gilders et al. 2016).

Ordinary income does not include the payments that are received by individual due to

restriction or relinquishing of the rights. It can also be the amount that might be received by

individual for entering into an agreement of not performing anything. Nonetheless, this can

lead to creation of “CGT event D” because it occurs when any contractual rights or any

equitable rights are created by individual in any entity.

received by taxpayer in the case “Kelly v FCT” for public appearance should be treated as

taxable income.

For determination of capital gains in accordance with the “subsection 108-10 (1) of

the ITAA 1997” in order to decrease the capital gains from collectables should take into

account the amount of capital losses that is generated from collectibles. Collectibles under

“section 108-15 (1)” are liable as set. Collectibles on other hand are treated in the form of

disposal and are taken as single set under “section 108-15 (2) of the ITAA 1997” (Berg and

Davidson 2017). In addition to this, there is exemption of capital gains generated from the

acquisition of collectibles of amount $ 500 or less.

Rent is the amount that is paid by individual for using the person property. Rent is

accounted for assessing the income as taxable income as depicted in the case of “Adelaide

Fruit and Produce Exchange Co Ltd (1932)”.

Any item that the tax payer derives it as part of its income is treated as income until

its net value has been realised. As provided in the case of “Brent v FCT” that the media

company provided special rights to the train robber wife to make the publication of life story.

The amount that was received by her by way of such publication is held as income and it is

taken into account for assessing the income tax as it arise from the ordinary concepts of her

rewards (Gilders et al. 2016).

Ordinary income does not include the payments that are received by individual due to

restriction or relinquishing of the rights. It can also be the amount that might be received by

individual for entering into an agreement of not performing anything. Nonetheless, this can

lead to creation of “CGT event D” because it occurs when any contractual rights or any

equitable rights are created by individual in any entity.

5TAXATION LAW

An individual can claim deductions for legal fees under “Section 8-1 of the ITAA

1997” provided if the fees received are associated with the activities of taxpayer. It is held as

per the court law “Federal Commissioner of Taxation v Rowe (1995)”that character

attributable to legal expenses should be concluded for the purpose of deductions (Woellner et

al. 2016). In the same way, if there is any expenditure that is associated in the form of

incidental cost related to proceeds generated from capital should be taken into account for

assessment of deduction of taxable income.

According to “section 8-1 of the ITAA 1997” of positive limbs, a taxpayer is allowed

for having an deduction entitlement if any chargeable income is produced because of the

outlays are incurred. Nonetheless, under the negative limbs of “section 8-1 of the ITAA

1997”, deductions cannot be claimed by person if it is of private character. Expenditure

incurred by individual in gaining new employment is not accounted for purpose of deductions

as held in the case “FCT v Madealena (1971)”. This is so because such expenses are not

incurred in the course of producing or gaining taxable income.

Application:

The income generated by Kate as depicted in the case study is from her profession of

working as an accountant in a firm. Personal exertion forms the basis of salary generated by

Kate. Salary received by Kate is held as an income according to the ordinary concepts as

cited by the case “Scott v Commissioner of Taxation (1935)” and treating such income as

taxable under the “section 6-5 of the ITAA 1997”. Payment received by Kate as a taxi

expense forms part of fringe benefits being derived according to “section 20 of the FBTAA

1986” (Dabner 2015).

An individual can claim deductions for legal fees under “Section 8-1 of the ITAA

1997” provided if the fees received are associated with the activities of taxpayer. It is held as

per the court law “Federal Commissioner of Taxation v Rowe (1995)”that character

attributable to legal expenses should be concluded for the purpose of deductions (Woellner et

al. 2016). In the same way, if there is any expenditure that is associated in the form of

incidental cost related to proceeds generated from capital should be taken into account for

assessment of deduction of taxable income.

According to “section 8-1 of the ITAA 1997” of positive limbs, a taxpayer is allowed

for having an deduction entitlement if any chargeable income is produced because of the

outlays are incurred. Nonetheless, under the negative limbs of “section 8-1 of the ITAA

1997”, deductions cannot be claimed by person if it is of private character. Expenditure

incurred by individual in gaining new employment is not accounted for purpose of deductions

as held in the case “FCT v Madealena (1971)”. This is so because such expenses are not

incurred in the course of producing or gaining taxable income.

Application:

The income generated by Kate as depicted in the case study is from her profession of

working as an accountant in a firm. Personal exertion forms the basis of salary generated by

Kate. Salary received by Kate is held as an income according to the ordinary concepts as

cited by the case “Scott v Commissioner of Taxation (1935)” and treating such income as

taxable under the “section 6-5 of the ITAA 1997”. Payment received by Kate as a taxi

expense forms part of fringe benefits being derived according to “section 20 of the FBTAA

1986” (Dabner 2015).

6TAXATION LAW

For being the best accountant, a cash award was received by Kate and such award would be

assessed for income tax purpose as it is associated with the producing activities by citing the

case “Kelly v FCT”.

It is indicated that Kate often participates in sporting activities for which she receives

sevetal prizes. The amount received as an award will be assessed for taxation under “section

6-5 of the ITAA 1997”.

Kate purchased an antique bed side lamp of amount $ 700 for which was sold at loss

of $ 200. Any capital loss generated from personal assets should be disregarded under

“section 108-10 (2)”. The amount received by Kate for appearing in the interview is held as

taxable income under the “section 6-5 of the ITAA 1997”.

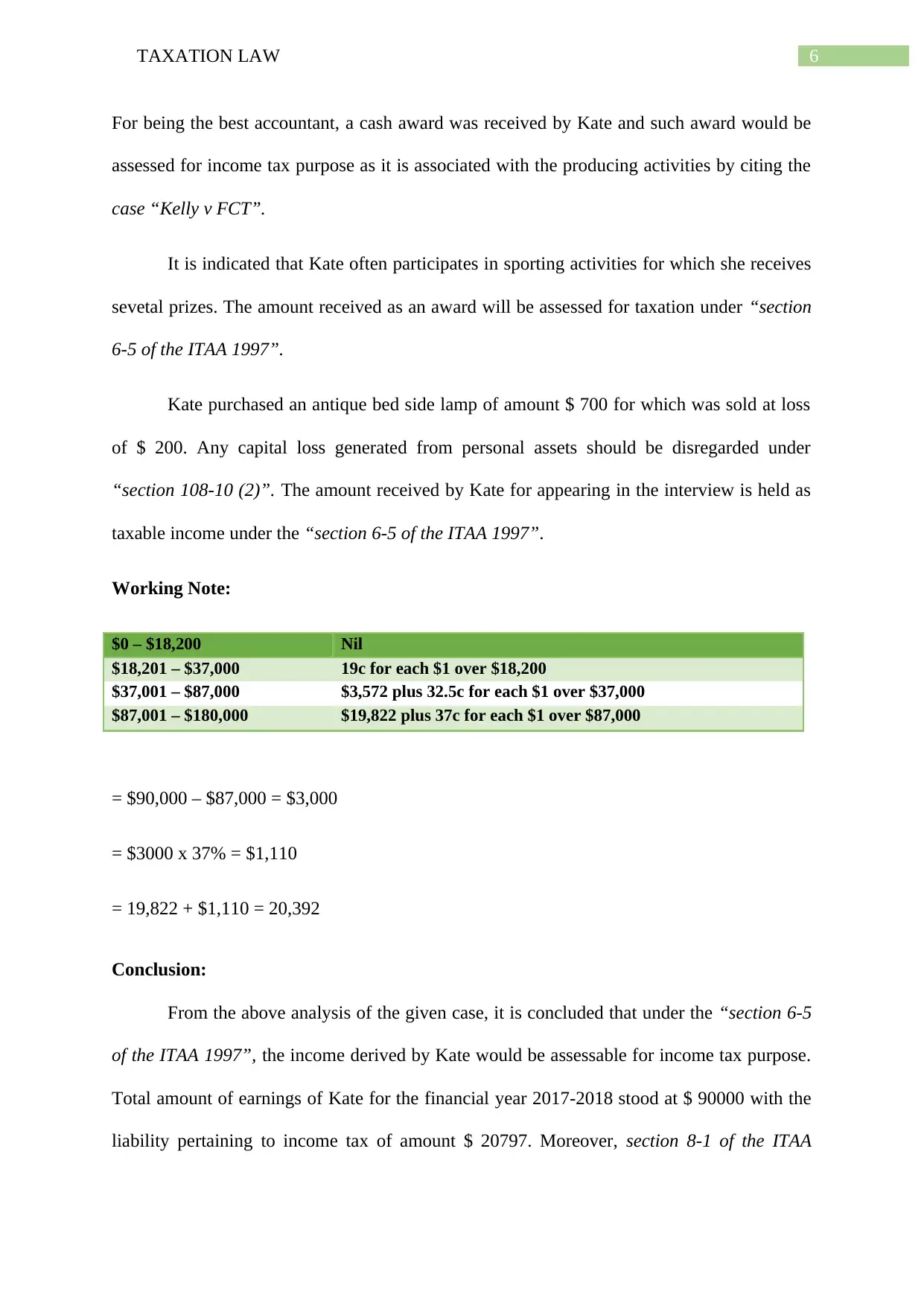

Working Note:

$0 – $18,200 Nil

$18,201 – $37,000 19c for each $1 over $18,200

$37,001 – $87,000 $3,572 plus 32.5c for each $1 over $37,000

$87,001 – $180,000 $19,822 plus 37c for each $1 over $87,000

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Conclusion:

From the above analysis of the given case, it is concluded that under the “section 6-5

of the ITAA 1997”, the income derived by Kate would be assessable for income tax purpose.

Total amount of earnings of Kate for the financial year 2017-2018 stood at $ 90000 with the

liability pertaining to income tax of amount $ 20797. Moreover, section 8-1 of the ITAA

For being the best accountant, a cash award was received by Kate and such award would be

assessed for income tax purpose as it is associated with the producing activities by citing the

case “Kelly v FCT”.

It is indicated that Kate often participates in sporting activities for which she receives

sevetal prizes. The amount received as an award will be assessed for taxation under “section

6-5 of the ITAA 1997”.

Kate purchased an antique bed side lamp of amount $ 700 for which was sold at loss

of $ 200. Any capital loss generated from personal assets should be disregarded under

“section 108-10 (2)”. The amount received by Kate for appearing in the interview is held as

taxable income under the “section 6-5 of the ITAA 1997”.

Working Note:

$0 – $18,200 Nil

$18,201 – $37,000 19c for each $1 over $18,200

$37,001 – $87,000 $3,572 plus 32.5c for each $1 over $37,000

$87,001 – $180,000 $19,822 plus 37c for each $1 over $87,000

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Conclusion:

From the above analysis of the given case, it is concluded that under the “section 6-5

of the ITAA 1997”, the income derived by Kate would be assessable for income tax purpose.

Total amount of earnings of Kate for the financial year 2017-2018 stood at $ 90000 with the

liability pertaining to income tax of amount $ 20797. Moreover, section 8-1 of the ITAA

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

1997” Kate is also entitled to deductions in relation to rental property and other deductions

that are allowable.

1997” Kate is also entitled to deductions in relation to rental property and other deductions

that are allowable.

8TAXATION LAW

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Berg, C. and Davidson, S., 2017. " Stop this greed": The tax-avoidance political campaign in

the OECD and Australia. Econ Journal Watch, 14(1), p.77.

Bird, R.M. and Zolt, E.M., 2014. Redistribution via taxation: the limited role of the personal

income tax in developing countries. Annals of Economics and Finance, 15(2), pp.625-683.

Dabner, J.H., 2015. The Australian tax office/tax profession partnership: Lessons from a pilot

interview program.

Eccleston, R. and Smith, H., 2015. Fixing Funding in the Australian Federation: Issues and

Options for State Tax Reform. Australian Journal of Public Administration, 74(4), pp.435-

447.

Enste, D.H., 2018. The shadow economy in OECD and EU accession countries–empirical

evidence for the influence of institutions, liberalization, taxation and regulation. In Size,

Causes and Consequences of the Underground Economy (pp. 135-150). Routledge.

Gilders, F.M., Taylor, C.J., Walpole, M., Burton, M. and Ciro, T., 2016. Understanding

Taxation Law 2016. LexisNexis Butterworths.

STEPHEN. BARKOCZY, 2018. FOUNDATIONS OF TAXATION LAW, 2018. OXFORD

University Press.

Tan, L.M. and Xiaoqian Liu, E., 2016. SMEs Tax Compliance: A Matter of Trust. Austl. Tax

F., 31, p.527.

Torgler, B., 2016. Tax compliance and data: What is available and what is needed. Australian

Economic Review, 49(3), pp.352-364.

Reference List:

Barkoczy, S., 2016. Foundations of taxation law 2016. OUP Catalogue.

Berg, C. and Davidson, S., 2017. " Stop this greed": The tax-avoidance political campaign in

the OECD and Australia. Econ Journal Watch, 14(1), p.77.

Bird, R.M. and Zolt, E.M., 2014. Redistribution via taxation: the limited role of the personal

income tax in developing countries. Annals of Economics and Finance, 15(2), pp.625-683.

Dabner, J.H., 2015. The Australian tax office/tax profession partnership: Lessons from a pilot

interview program.

Eccleston, R. and Smith, H., 2015. Fixing Funding in the Australian Federation: Issues and

Options for State Tax Reform. Australian Journal of Public Administration, 74(4), pp.435-

447.

Enste, D.H., 2018. The shadow economy in OECD and EU accession countries–empirical

evidence for the influence of institutions, liberalization, taxation and regulation. In Size,

Causes and Consequences of the Underground Economy (pp. 135-150). Routledge.

Gilders, F.M., Taylor, C.J., Walpole, M., Burton, M. and Ciro, T., 2016. Understanding

Taxation Law 2016. LexisNexis Butterworths.

STEPHEN. BARKOCZY, 2018. FOUNDATIONS OF TAXATION LAW, 2018. OXFORD

University Press.

Tan, L.M. and Xiaoqian Liu, E., 2016. SMEs Tax Compliance: A Matter of Trust. Austl. Tax

F., 31, p.527.

Torgler, B., 2016. Tax compliance and data: What is available and what is needed. Australian

Economic Review, 49(3), pp.352-364.

9TAXATION LAW

Tran-Nam, B., 2016. Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-44).

Palgrave Macmillan, London.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Tran-Nam, B., 2016. Tax Reform and Tax Simplification: Conceptual and Measurement

Issues and Australian Experiences. In The Complexity of Tax Simplification (pp. 11-44).

Palgrave Macmillan, London.

Woellner, R., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2016. Australian Taxation

Law 2016. OUP Catalogue.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.