Determining Taxable Income and Allowable Deductions under Taxation Law

VerifiedAdded on 2023/06/11

|12

|2334

|127

AI Summary

This article discusses the determination of taxable income and allowable deductions under taxation law using a case study of Kate. It covers the rules and applications of various sections of the ITAA 1997 and FBTAA 1986.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1TAXATION LAW

Table of Contents

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................8

Reference List:.........................................................................................................................10

Table of Contents

Headings:....................................................................................................................................2

Issue:..........................................................................................................................................2

Rule:...........................................................................................................................................2

Application:................................................................................................................................5

Conclusion:................................................................................................................................8

Reference List:.........................................................................................................................10

2TAXATION LAW

Headings:

The following scenario would be determining the taxable income of Kate during the

year ended 2017/18 and would also considered whether the expenditure is allowed as

deductions under “section 8-1 of the ITAA 1997”?

Issue:

The following issue is associated with the determination of the taxable income of

Kate and determining whether the she would be held assessable for ordinary income reported

during the year 2017? The issue takes into the consideration whether Kate would be

permitted to claim an allowable deduction under “section 8-1 of the ITAA 1997”?

Rule:

Denoting the explanation of “section 6-1 of the ITAA 1997” an individual taxpayer is

considered for taxation purpose for the income derived from the personal sources1. This

includes salary income, wages, bonus, fees, allowances or revenue from the business carried

on by the taxpayer. As stated under the “section 6-5 of the ITAA 1997” ordinary income of

the taxpayer constitutes income that comes into the taxpayer. In “Scott v Commissioner of

Taxation (1935)” the expression income should be ascertained in agreement with the

ordinary concepts.

As noted in “section 136 (1) of the FBTAA 1986” fringe benefit constitutes where a

company offers benefit to the employee for their employment2. With reference to “section 20

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Headings:

The following scenario would be determining the taxable income of Kate during the

year ended 2017/18 and would also considered whether the expenditure is allowed as

deductions under “section 8-1 of the ITAA 1997”?

Issue:

The following issue is associated with the determination of the taxable income of

Kate and determining whether the she would be held assessable for ordinary income reported

during the year 2017? The issue takes into the consideration whether Kate would be

permitted to claim an allowable deduction under “section 8-1 of the ITAA 1997”?

Rule:

Denoting the explanation of “section 6-1 of the ITAA 1997” an individual taxpayer is

considered for taxation purpose for the income derived from the personal sources1. This

includes salary income, wages, bonus, fees, allowances or revenue from the business carried

on by the taxpayer. As stated under the “section 6-5 of the ITAA 1997” ordinary income of

the taxpayer constitutes income that comes into the taxpayer. In “Scott v Commissioner of

Taxation (1935)” the expression income should be ascertained in agreement with the

ordinary concepts.

As noted in “section 136 (1) of the FBTAA 1986” fringe benefit constitutes where a

company offers benefit to the employee for their employment2. With reference to “section 20

1 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

2 Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

3TAXATION LAW

of the FBTAA 1986” expense fringe benefit occurs when the expenses of employee is paid by

employer.

Mere prizes are not treated as income. But the amount received from such prizes may

be treated as income when it holds sufficient nexus with the income producing activities of

the taxpayer. In “Kelly v FCT” the professional football player received award for being the

fair player3. The sum received by footballer constituted income as it was incidental to his

work and employment with club. According to “section 6-1 of the ITAA 1997” a taxpayer

obtaining income from personal exertion is included in taxable income as either ordinary or

statutory income. Mere prize wins is not an income but assessable if holds nexus with the

taxpayer’s income earning activities. In “FCT v Stone” the taxpayer received salary as

policewomen and earned prize money from sporting endorsement. According to

commissioner of taxation, the taxpayer was found to be executing the business of

professional athlete and the money received constituted income.

An individual receiving payments from sporting appearance or promotions that has

nexus with the income producing activities then such amount is considered taxable. In “Kelly

v FCT” receipt of payment by taxpayer for public appearance is chargeable earnings. As

stated in “subsection 108-10 (1) of the ITAA 1997” to work out the capital gains losses

obtained from selling collectibles should be only employed in lowering the gains from

collectibles. Collectibles are viewed as single assets under “section 108-15 (2) of the ITAA

1997” and selling of each set is held as portion of collectibles. Moreover, collectibles

purchased for less than $500 should be ignored4.

3 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

4 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

of the FBTAA 1986” expense fringe benefit occurs when the expenses of employee is paid by

employer.

Mere prizes are not treated as income. But the amount received from such prizes may

be treated as income when it holds sufficient nexus with the income producing activities of

the taxpayer. In “Kelly v FCT” the professional football player received award for being the

fair player3. The sum received by footballer constituted income as it was incidental to his

work and employment with club. According to “section 6-1 of the ITAA 1997” a taxpayer

obtaining income from personal exertion is included in taxable income as either ordinary or

statutory income. Mere prize wins is not an income but assessable if holds nexus with the

taxpayer’s income earning activities. In “FCT v Stone” the taxpayer received salary as

policewomen and earned prize money from sporting endorsement. According to

commissioner of taxation, the taxpayer was found to be executing the business of

professional athlete and the money received constituted income.

An individual receiving payments from sporting appearance or promotions that has

nexus with the income producing activities then such amount is considered taxable. In “Kelly

v FCT” receipt of payment by taxpayer for public appearance is chargeable earnings. As

stated in “subsection 108-10 (1) of the ITAA 1997” to work out the capital gains losses

obtained from selling collectibles should be only employed in lowering the gains from

collectibles. Collectibles are viewed as single assets under “section 108-15 (2) of the ITAA

1997” and selling of each set is held as portion of collectibles. Moreover, collectibles

purchased for less than $500 should be ignored4.

3 Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

4 Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4TAXATION LAW

Rent represents that sum paid by an individual for use of property. In “Adelaide Fruit

and Produce Exchange Co Ltd (1932)” income from rental property is included in taxpayer’s

assessable income.

An element of income derived by an individual constitutes income up to the realisable

value. The item of income should possess the character of gain for the taxpayer. Reward for

services are usually held assessable as ordinary income under “section 6-5 of the ITAA

1997”5. In “Brent v FCT” the train robber’s wife was granted with the right of narrating the

story of her life and in return received amount that was held as income under ordinary

concepts.

Payment received for relinquishing rights cannot be referred as income because it

constitutes CGT event D16. The reason for classifying the payments as CGT event because it

occurs when an individual forms a contractual or equitable rights in any other entity. An

individual is permitted to claim deductions for legal expenses under “section 8-1 of the ITAA

1997”. In “Federal Commissioner of Taxation v Rowe (1995)” it was held by the

commissioner that necessary characteristics of legal expenses must understood for allowing

as deductions. Expenses that are incidental cost to capital proceeds is a permissible

deductions7.

5 ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

6 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017

7 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Rent represents that sum paid by an individual for use of property. In “Adelaide Fruit

and Produce Exchange Co Ltd (1932)” income from rental property is included in taxpayer’s

assessable income.

An element of income derived by an individual constitutes income up to the realisable

value. The item of income should possess the character of gain for the taxpayer. Reward for

services are usually held assessable as ordinary income under “section 6-5 of the ITAA

1997”5. In “Brent v FCT” the train robber’s wife was granted with the right of narrating the

story of her life and in return received amount that was held as income under ordinary

concepts.

Payment received for relinquishing rights cannot be referred as income because it

constitutes CGT event D16. The reason for classifying the payments as CGT event because it

occurs when an individual forms a contractual or equitable rights in any other entity. An

individual is permitted to claim deductions for legal expenses under “section 8-1 of the ITAA

1997”. In “Federal Commissioner of Taxation v Rowe (1995)” it was held by the

commissioner that necessary characteristics of legal expenses must understood for allowing

as deductions. Expenses that are incidental cost to capital proceeds is a permissible

deductions7.

5 ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

6 ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017

7 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

5TAXATION LAW

The general rule of “section 8-1 of the ITAA 1997” states that expenses that are

preliminary to commencement of income generating activities is not allowed for deductions

since it is not incurred in the course of producing assessable income. In “FCT v Madealena

(1971)” the court denied taxpayer with deductions for getting new employment as it was not

in the course of gaining taxable income.

Application:

Denoting the circumstances of Kate the receipt of salary as professional accountant

represents income from personal exertion. Mentioning the decision of court of in “Scott v

Commissioner of Taxation (1935)” the receipt of salary income constituted income from

personal exertion. Such income would be considered for assessment in respect of the ordinary

concepts under “section 6-5 of the ITAA 1997”8. The employer of the Kate on most

occasions pays her taxpayer and under “section 20 of the FBTAA 1986” these payments

constitutes fringe benefits.

A cash prize of $5,000 received by Kate for the best accountant was associated to her

employment. Mentioning the event of “Kelly v FCT” the amount constituted income as it

was incidental to her work and employment9.

Kate regularly participates in competition of high-jumping in chase of sporting

brilliance and also wins prizes for her excellence. Mentioning the event of “FCT v Stone”

Kate is found to be executing the business of professional athlete and the money received

constituted income and the sum received is assessable in accordance with the ordinary

8 Kiprotich, B. A. "Principles of Taxation." governance (2016).

9 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education, 2015.

The general rule of “section 8-1 of the ITAA 1997” states that expenses that are

preliminary to commencement of income generating activities is not allowed for deductions

since it is not incurred in the course of producing assessable income. In “FCT v Madealena

(1971)” the court denied taxpayer with deductions for getting new employment as it was not

in the course of gaining taxable income.

Application:

Denoting the circumstances of Kate the receipt of salary as professional accountant

represents income from personal exertion. Mentioning the decision of court of in “Scott v

Commissioner of Taxation (1935)” the receipt of salary income constituted income from

personal exertion. Such income would be considered for assessment in respect of the ordinary

concepts under “section 6-5 of the ITAA 1997”8. The employer of the Kate on most

occasions pays her taxpayer and under “section 20 of the FBTAA 1986” these payments

constitutes fringe benefits.

A cash prize of $5,000 received by Kate for the best accountant was associated to her

employment. Mentioning the event of “Kelly v FCT” the amount constituted income as it

was incidental to her work and employment9.

Kate regularly participates in competition of high-jumping in chase of sporting

brilliance and also wins prizes for her excellence. Mentioning the event of “FCT v Stone”

Kate is found to be executing the business of professional athlete and the money received

constituted income and the sum received is assessable in accordance with the ordinary

8 Kiprotich, B. A. "Principles of Taxation." governance (2016).

9 Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education, 2015.

6TAXATION LAW

concepts of “section 6-5 of the ITAA 1997”10. Later events provides that Kate obtained a sum

of $40,000 for appearance in sporting event. Pointing out the decision in “Kelly v FCT”

receipt of payment by Kate for public appearance is chargeable earnings.

Kate reported a loss from the sale of antique bed side lamp. Mentioning the

explanations of “section 108-10 (2)” Kate must disregard any capital from the sale of

collectibles. Additionally Kate reports a capital gains from the sale of antique lamp however

the cost price of the asset was $400. According to the “section 108-15 (2) of the ITAA 1997”

Kate should disregard the capital gains from Antique lamp because the cost base of asset was

less than $500.

Kate later receives income from rental property and referring to “Adelaide Fruit and

Produce Exchange Co Ltd (1932)” these rental property receipts constitutes periodical

receipts which is assessable under “section 6-5 of the ITAA 1997”.

Kate was paid for appearing in the television interview and narrating the story of her

life outside sports. Mentioning the judgment of “Brent v FCT” the receipt of $30,000 would

be held as income under ordinary concepts of “section 6-5 of the ITAA 1997”11.

Kate later receives in a second agreement a payment of $20,000 for relinquishing the

rights of not giving any similar interview in other television. These amounts results in CGT

event D1 which is considered for assessment purpose. She later incurs a cost of $5,000 for

10 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

concepts of “section 6-5 of the ITAA 1997”10. Later events provides that Kate obtained a sum

of $40,000 for appearance in sporting event. Pointing out the decision in “Kelly v FCT”

receipt of payment by Kate for public appearance is chargeable earnings.

Kate reported a loss from the sale of antique bed side lamp. Mentioning the

explanations of “section 108-10 (2)” Kate must disregard any capital from the sale of

collectibles. Additionally Kate reports a capital gains from the sale of antique lamp however

the cost price of the asset was $400. According to the “section 108-15 (2) of the ITAA 1997”

Kate should disregard the capital gains from Antique lamp because the cost base of asset was

less than $500.

Kate later receives income from rental property and referring to “Adelaide Fruit and

Produce Exchange Co Ltd (1932)” these rental property receipts constitutes periodical

receipts which is assessable under “section 6-5 of the ITAA 1997”.

Kate was paid for appearing in the television interview and narrating the story of her

life outside sports. Mentioning the judgment of “Brent v FCT” the receipt of $30,000 would

be held as income under ordinary concepts of “section 6-5 of the ITAA 1997”11.

Kate later receives in a second agreement a payment of $20,000 for relinquishing the

rights of not giving any similar interview in other television. These amounts results in CGT

event D1 which is considered for assessment purpose. She later incurs a cost of $5,000 for

10 Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

11 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

legal expenses and referring to “Federal Commissioner of Taxation v Rowe (1995)” Kate

would be permitted to claim deductions for legal expenses under “section 8-1 of the ITAA

1997”. The expenses was incidental cost to capital proceeds and it is a permissible

deductions12.

In the later instances it was noticed that Kate in search of employment travelled to

Melbourne to attend the job interview an expenses of $400 on airfares and $800 for

accommodations. Mentioning the explanations of “section 8-1 of the ITAA 1997” expenses

that are preliminary to commencement of income generating activities is not allowed for

deductions since it is not incurred in the course of producing assessable income. Referring to

“FCT v Madealena (1971)” Kate would be denied allowable deduction for the expenses

incurred by her since it was preliminary to commencement of income generating activities

and is not incurred in the course of producing assessable income.

12 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

legal expenses and referring to “Federal Commissioner of Taxation v Rowe (1995)” Kate

would be permitted to claim deductions for legal expenses under “section 8-1 of the ITAA

1997”. The expenses was incidental cost to capital proceeds and it is a permissible

deductions12.

In the later instances it was noticed that Kate in search of employment travelled to

Melbourne to attend the job interview an expenses of $400 on airfares and $800 for

accommodations. Mentioning the explanations of “section 8-1 of the ITAA 1997” expenses

that are preliminary to commencement of income generating activities is not allowed for

deductions since it is not incurred in the course of producing assessable income. Referring to

“FCT v Madealena (1971)” Kate would be denied allowable deduction for the expenses

incurred by her since it was preliminary to commencement of income generating activities

and is not incurred in the course of producing assessable income.

12 Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

8TAXATION LAW

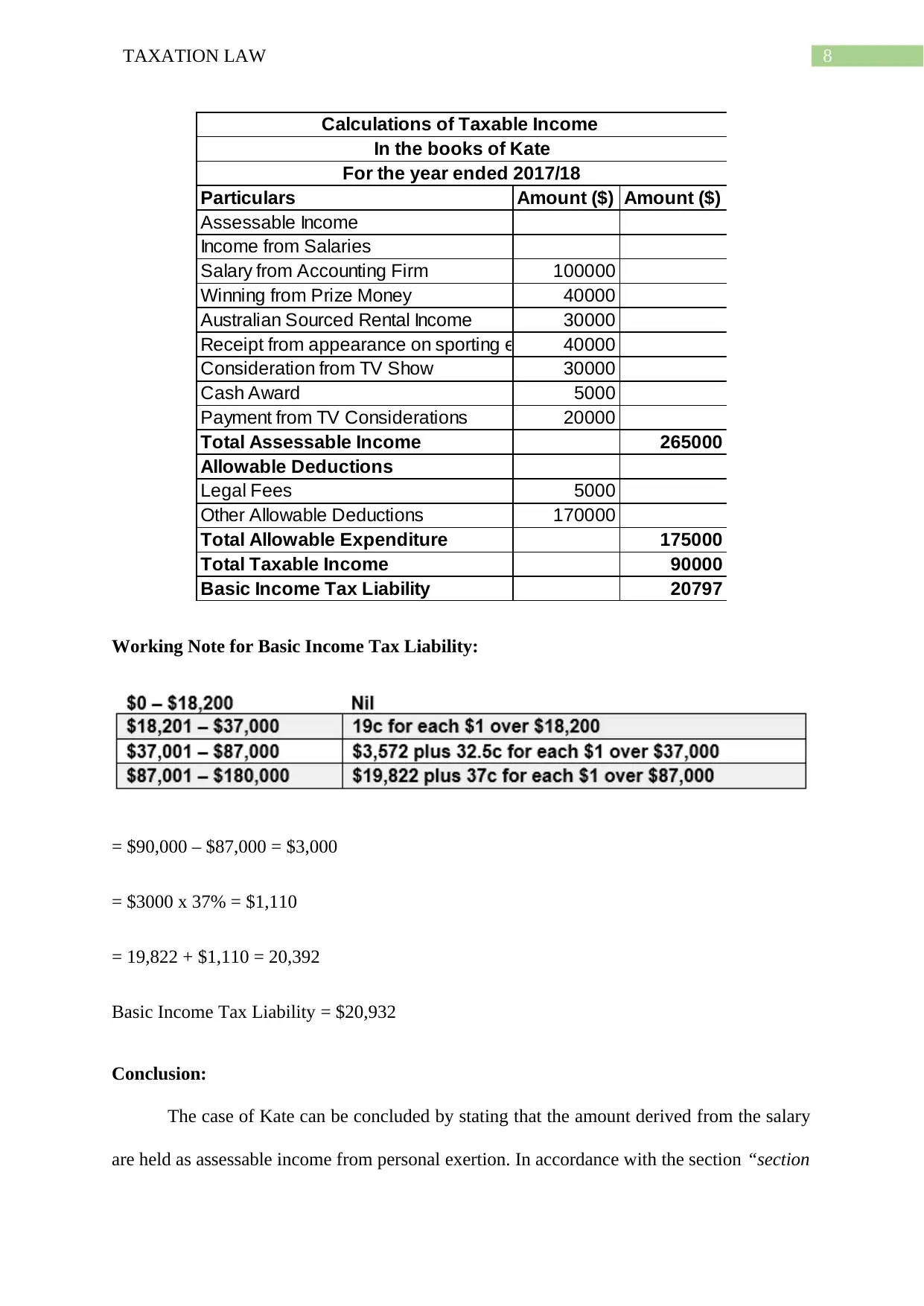

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries

Salary from Accounting Firm 100000

Winning from Prize Money 40000

Australian Sourced Rental Income 30000

Receipt from appearance on sporting evets 40000

Consideration from TV Show 30000

Cash Award 5000

Payment from TV Considerations 20000

Total Assessable Income 265000

Allowable Deductions

Legal Fees 5000

Other Allowable Deductions 170000

Total Allowable Expenditure 175000

Total Taxable Income 90000

Basic Income Tax Liability 20797

Calculations of Taxable Income

In the books of Kate

For the year ended 2017/18

Working Note for Basic Income Tax Liability:

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Basic Income Tax Liability = $20,932

Conclusion:

The case of Kate can be concluded by stating that the amount derived from the salary

are held as assessable income from personal exertion. In accordance with the section “section

Particulars Amount ($) Amount ($)

Assessable Income

Income from Salaries

Salary from Accounting Firm 100000

Winning from Prize Money 40000

Australian Sourced Rental Income 30000

Receipt from appearance on sporting evets 40000

Consideration from TV Show 30000

Cash Award 5000

Payment from TV Considerations 20000

Total Assessable Income 265000

Allowable Deductions

Legal Fees 5000

Other Allowable Deductions 170000

Total Allowable Expenditure 175000

Total Taxable Income 90000

Basic Income Tax Liability 20797

Calculations of Taxable Income

In the books of Kate

For the year ended 2017/18

Working Note for Basic Income Tax Liability:

= $90,000 – $87,000 = $3,000

= $3000 x 37% = $1,110

= 19,822 + $1,110 = 20,392

Basic Income Tax Liability = $20,932

Conclusion:

The case of Kate can be concluded by stating that the amount derived from the salary

are held as assessable income from personal exertion. In accordance with the section “section

9TAXATION LAW

6-5 of the ITAA 1997” the cash awards, rents, television consideration payment etc

constituted income from ordinary concepts that would be considered for assessment under

section 6-5 of the ITAA 1997. Furthermore, Kate would be able to claim allowable

deductions for the amount reported under “section 8-1 of the ITAA 1997”.

6-5 of the ITAA 1997” the cash awards, rents, television consideration payment etc

constituted income from ordinary concepts that would be considered for assessment under

section 6-5 of the ITAA 1997. Furthermore, Kate would be able to claim allowable

deductions for the amount reported under “section 8-1 of the ITAA 1997”.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10TAXATION LAW

Reference List:

Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education, 2015.

Kiprotich, B. A. "Principles of Taxation." governance (2016).

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

Reference List:

Bankman, Joseph, et al. Federal Income Taxation. Wolters Kluwer Law & Business, 2017.

Barkoczy, Stephen. "Foundations of taxation law 2016." OUP Catalogue (2016).

Basu, Subhajit. Global perspectives on e-commerce taxation law. Routledge, 2016.

Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data

matching." Proctor, The 37.6 (2017): 18.

Jones, Sally, and Shelley Rhoades-Catanach. Principles of Taxation for Business and

Investment Planning. McGraw-Hill Higher Education, 2015.

Kiprotich, B. A. "Principles of Taxation." governance (2016).

Long, Brendan, Jon Campbell, and Carolyn Kelshaw. "The justice lens on taxation policy in

Australia." St Mark's Review235 (2016): 94.

Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury

Publishing, 2016.

ROBIN & BARKOCZY WOELLNER (STEPHEN & MURPHY, SHIRLEY ET

AL.). AUSTRALIAN TAXATION LAW 2018. OXFORD University Press, 2018.

ROBIN, H. AUSTRALIAN TAXATION LAW 2017. OXFORD University Press, 2017.

Schmalbeck, Richard, Lawrence Zelenak, and Sarah B. Lawsky. Federal Income Taxation.

Wolters Kluwer Law & Business, 2015.

Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

11TAXATION LAW

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.