Taxation Law: Tax on Lottery, Calculation of Taxable Income, Tax Avoidance Case, and Accounting for Capital Gain, Loss and Normal Business Losses in Australia

VerifiedAdded on 2023/06/04

|13

|3534

|447

AI Summary

This article discusses tax on lottery, calculation of taxable income, tax avoidance case, and accounting for capital gain, loss and normal business losses in Australia. It explains the regulations on tax declaration of income from lottery, the accrual basis for tax calculation, and the principle of tax avoidance. It also highlights the impact of tax avoidance on the Australian Tax Office and the measures taken to curb it.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

TAXATION LAW

TAX ON LOTTERY, CALCULATION OF TAXABLE INCOME,TAX AVOIDANCE CASE

AND ACCOUNTING FOR CAPITAL GAIN,LOSS AND NORMAL BUSINESS LOSSES IN

AUSTRALIA.

Course:

Professor’s Name

Institution

City

Date

TAX ON LOTTERY, CALCULATION OF TAXABLE INCOME,TAX AVOIDANCE CASE

AND ACCOUNTING FOR CAPITAL GAIN,LOSS AND NORMAL BUSINESS LOSSES IN

AUSTRALIA.

Course:

Professor’s Name

Institution

City

Date

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW

Question 1;

Australian Tax Office classifies income or rather awards or prizes from gaming

draws, lottery and raffle ticket win as part of other incomes for tax purpose. This is due to the

nature in which these incomes are earned i.e. mainly based on once time event. The regulation

likewise claims for tax declaration of this income except where the income is exempted from tax

if any. However inclusion of this incomes as part of income tax return for that year ideally

depends with our often is that draw conducted and who are the sponsors of the draws.For

instance,Australia Tax Office has outlined that all prize awards or gift of any form whether as

cash or as good that is earned as a result of an activity conducted by any investment company,

building societies, banks, financial institution like credit union and business tycoons has to be

declared as part of income for tax purpose in that year of tax.

The latter award won on this bodies that are in investment is considered income

simply because there is a guarantee payment of the award and likewise the outlets awarding are

venture in business though the main sole purpose is surety of being awarded in case of a draw. It

should likewise be known that the awards to be declared are not only those which are in cash

form, not really even those discounts allowance given on goods and cash, interest free loan

awards, low interest loan issuance, goods like cars, houses and free holidays trips, tickets offered

and any other form of prize should be declared. These prizes that are in tangible goods form its

declaration is expected to be done in value form i.e. as per the cost of the item i.e. purchase

consideration of that asset.

Likewise let it be known that incase where show games are conducted and the

contestants in the arena are the same regularly clients who regularly recognized and thus receive

Question 1;

Australian Tax Office classifies income or rather awards or prizes from gaming

draws, lottery and raffle ticket win as part of other incomes for tax purpose. This is due to the

nature in which these incomes are earned i.e. mainly based on once time event. The regulation

likewise claims for tax declaration of this income except where the income is exempted from tax

if any. However inclusion of this incomes as part of income tax return for that year ideally

depends with our often is that draw conducted and who are the sponsors of the draws.For

instance,Australia Tax Office has outlined that all prize awards or gift of any form whether as

cash or as good that is earned as a result of an activity conducted by any investment company,

building societies, banks, financial institution like credit union and business tycoons has to be

declared as part of income for tax purpose in that year of tax.

The latter award won on this bodies that are in investment is considered income

simply because there is a guarantee payment of the award and likewise the outlets awarding are

venture in business though the main sole purpose is surety of being awarded in case of a draw. It

should likewise be known that the awards to be declared are not only those which are in cash

form, not really even those discounts allowance given on goods and cash, interest free loan

awards, low interest loan issuance, goods like cars, houses and free holidays trips, tickets offered

and any other form of prize should be declared. These prizes that are in tangible goods form its

declaration is expected to be done in value form i.e. as per the cost of the item i.e. purchase

consideration of that asset.

Likewise let it be known that incase where show games are conducted and the

contestants in the arena are the same regularly clients who regularly recognized and thus receive

TAXATION LAW

appearance or game showing winning as a result of the regularly appearance i.e. on loyal

customer perspective, these appearance fees award and game showing prizes has to be declare

for tax purpose as a return simply because the regularly appearance dictates the speculation for

award.

Although all the above prizes and awards won are worth declaration of that tax as part

of income, there exist very special considerations given to ordinary lotteries. Australian Tax

Office (Blakelock and King,2017.Pg.52) has exempted all prizes, gifts and awards that are won

as a result of ordinary lotteries conducted with examples being lotto lotteries and raffle ticket.

These awards on ordinary lotteries are exempted from tax since the participants are never aware

of outcome in any case they play in draw whose outcome is unknown since it is based on

probabilities or chances.

It is from this exemption of ordinary lottery prizes that we factor in this case of Set

For Life. In a nutshell the party that is involved in conduction of this Set For Life lottery draw is

Lottery Commission which in actual sense is deemed as an ordinary lottery firm hence by virtual

of this ordinarily aspect automatically any awards or prizes earned from any draw conducted by

this ordinary lottery commission of ‘’Set For Life icon’’ has to be exempted from tax declaration

without fail. It is therefore very certain that the $50000 prize that will be payable for the next

20years to the person winning the Set For Life lottery draw will enjoy tax exemption whether as

the person himself/herself or as estate as depicted in the current regulation on this.

The $50000 prize winning as mentioned in the question in query is therefore not

subjected for tax purpose since it is classified as tax exempt in the Australian Tax Office

regulation. However if this amount of $50000 from the Set For Life lottery draw that is ordinary

is used to acquire an asset whether cumulative or as an installment, in case of disposal of that

appearance or game showing winning as a result of the regularly appearance i.e. on loyal

customer perspective, these appearance fees award and game showing prizes has to be declare

for tax purpose as a return simply because the regularly appearance dictates the speculation for

award.

Although all the above prizes and awards won are worth declaration of that tax as part

of income, there exist very special considerations given to ordinary lotteries. Australian Tax

Office (Blakelock and King,2017.Pg.52) has exempted all prizes, gifts and awards that are won

as a result of ordinary lotteries conducted with examples being lotto lotteries and raffle ticket.

These awards on ordinary lotteries are exempted from tax since the participants are never aware

of outcome in any case they play in draw whose outcome is unknown since it is based on

probabilities or chances.

It is from this exemption of ordinary lottery prizes that we factor in this case of Set

For Life. In a nutshell the party that is involved in conduction of this Set For Life lottery draw is

Lottery Commission which in actual sense is deemed as an ordinary lottery firm hence by virtual

of this ordinarily aspect automatically any awards or prizes earned from any draw conducted by

this ordinary lottery commission of ‘’Set For Life icon’’ has to be exempted from tax declaration

without fail. It is therefore very certain that the $50000 prize that will be payable for the next

20years to the person winning the Set For Life lottery draw will enjoy tax exemption whether as

the person himself/herself or as estate as depicted in the current regulation on this.

The $50000 prize winning as mentioned in the question in query is therefore not

subjected for tax purpose since it is classified as tax exempt in the Australian Tax Office

regulation. However if this amount of $50000 from the Set For Life lottery draw that is ordinary

is used to acquire an asset whether cumulative or as an installment, in case of disposal of that

TAXATION LAW

asset that resulted from the lottery win any gain or loss on disposal has to be declared as capital

gain or loss on the grounds that awardee was now certain that he or she would earn or gain from

that disposal.

Conclusively I wish to state that there is tax exempt on ordinary lottery awards thus

excusing the person who wins the Set For Life voucher of $50000 from being taxed no

declaration of this income as part of taxable in his or her income with reasons well known on the

ground of an ordinary lottery (Philander, 2013.Pg.2.)

Question 2;

Australian Tax Office declares that by use of accrual method all gain or losses are

expected to be allocated on the ground from which a financial arrangement was built between

entities (Tretola, 2013.Pg.4.) It is therefore clear that the allocation of gain or loss is only

applicable upon approval that the financial arrangement results to a benefit whether it is current

or future. It is likewise applicable if the entities who are involved in the financial arrangement

have a proof that in the next rest part of the business life there will be future financial benefit

resulting from it.

It is from this financial arrangement of accrual basis that we see revenue or income or

gain are recognized and earned as soon as a sale transaction is passed in the books of accounts as

an invoice hence not waiting when payment is received. Similarly to expenses whereby they are

only recognized as soon as they are incurred and not when they are paid off. Accrual basis is

mainly applicable to transaction whose sales are done on credit basis hence the need to have an

agreement that as soon as that sale as recognized in an invoice as credit sale automatically is

deemed as part of sales similarly to any expense.

asset that resulted from the lottery win any gain or loss on disposal has to be declared as capital

gain or loss on the grounds that awardee was now certain that he or she would earn or gain from

that disposal.

Conclusively I wish to state that there is tax exempt on ordinary lottery awards thus

excusing the person who wins the Set For Life voucher of $50000 from being taxed no

declaration of this income as part of taxable in his or her income with reasons well known on the

ground of an ordinary lottery (Philander, 2013.Pg.2.)

Question 2;

Australian Tax Office declares that by use of accrual method all gain or losses are

expected to be allocated on the ground from which a financial arrangement was built between

entities (Tretola, 2013.Pg.4.) It is therefore clear that the allocation of gain or loss is only

applicable upon approval that the financial arrangement results to a benefit whether it is current

or future. It is likewise applicable if the entities who are involved in the financial arrangement

have a proof that in the next rest part of the business life there will be future financial benefit

resulting from it.

It is from this financial arrangement of accrual basis that we see revenue or income or

gain are recognized and earned as soon as a sale transaction is passed in the books of accounts as

an invoice hence not waiting when payment is received. Similarly to expenses whereby they are

only recognized as soon as they are incurred and not when they are paid off. Accrual basis is

mainly applicable to transaction whose sales are done on credit basis hence the need to have an

agreement that as soon as that sale as recognized in an invoice as credit sale automatically is

deemed as part of sales similarly to any expense.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW

It is therefore from this accrual basis that the aspect of tax issue arises. Many will

argues that it is an unfair for a company to declare and pay tax for sales that are indeed pending

payments hence some wish to do so as soon as payment is done. Some are likewise seen to argue

that only those sales done on cash basis are the one that ought to be paid tax for , an argument

that accrual basis method came to resolve hence the tax office require payment of these tax as

soon as invoicing done since that is when is recognized (Woellner, Barkoczy, Murphy, Evans

and Pinto,2010.Pg.32.)

Going with the above definition and analysis of accrual basis for tax purpose thus

exist the need to calculate Corner Pharmacy taxable income for that year based on this method. It

is deemed on accrual basis since a big part of it is on financial arrangement between the bank and

the Pharmaceutical Benefit Scheme Body.

Analysis of items to be considered in calculation of Corners Pharmacy Taxable Income

(Freedman and Crawford, 2010.Pg.85);

$

Note 1.Cost Of Sales = Opening Stock=150000

Add

= Purchases =500000

Less

= Closing Stock =(200000)

Cost of Goods Sold =450000, ideally this is the cost incurred on the items that

were sold it is the cost of sales that indeed has to be factored in a business income calculation so

as to get the gross profit margin. It is mostly deducted from the total sales for it to get the gross

It is therefore from this accrual basis that the aspect of tax issue arises. Many will

argues that it is an unfair for a company to declare and pay tax for sales that are indeed pending

payments hence some wish to do so as soon as payment is done. Some are likewise seen to argue

that only those sales done on cash basis are the one that ought to be paid tax for , an argument

that accrual basis method came to resolve hence the tax office require payment of these tax as

soon as invoicing done since that is when is recognized (Woellner, Barkoczy, Murphy, Evans

and Pinto,2010.Pg.32.)

Going with the above definition and analysis of accrual basis for tax purpose thus

exist the need to calculate Corner Pharmacy taxable income for that year based on this method. It

is deemed on accrual basis since a big part of it is on financial arrangement between the bank and

the Pharmaceutical Benefit Scheme Body.

Analysis of items to be considered in calculation of Corners Pharmacy Taxable Income

(Freedman and Crawford, 2010.Pg.85);

$

Note 1.Cost Of Sales = Opening Stock=150000

Add

= Purchases =500000

Less

= Closing Stock =(200000)

Cost of Goods Sold =450000, ideally this is the cost incurred on the items that

were sold it is the cost of sales that indeed has to be factored in a business income calculation so

as to get the gross profit margin. It is mostly deducted from the total sales for it to get the gross

TAXATION LAW

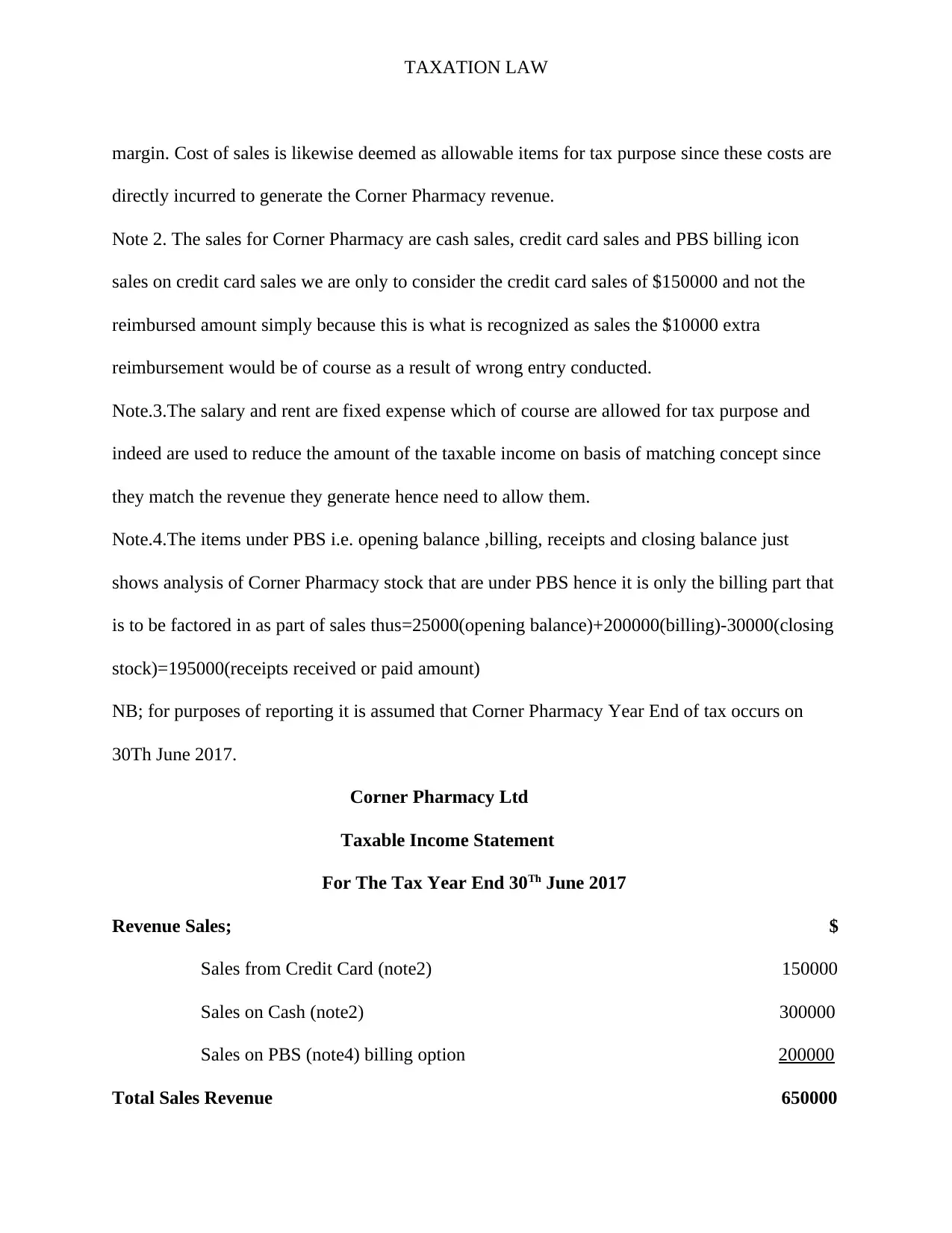

margin. Cost of sales is likewise deemed as allowable items for tax purpose since these costs are

directly incurred to generate the Corner Pharmacy revenue.

Note 2. The sales for Corner Pharmacy are cash sales, credit card sales and PBS billing icon

sales on credit card sales we are only to consider the credit card sales of $150000 and not the

reimbursed amount simply because this is what is recognized as sales the $10000 extra

reimbursement would be of course as a result of wrong entry conducted.

Note.3.The salary and rent are fixed expense which of course are allowed for tax purpose and

indeed are used to reduce the amount of the taxable income on basis of matching concept since

they match the revenue they generate hence need to allow them.

Note.4.The items under PBS i.e. opening balance ,billing, receipts and closing balance just

shows analysis of Corner Pharmacy stock that are under PBS hence it is only the billing part that

is to be factored in as part of sales thus=25000(opening balance)+200000(billing)-30000(closing

stock)=195000(receipts received or paid amount)

NB; for purposes of reporting it is assumed that Corner Pharmacy Year End of tax occurs on

30Th June 2017.

Corner Pharmacy Ltd

Taxable Income Statement

For The Tax Year End 30Th June 2017

Revenue Sales; $

Sales from Credit Card (note2) 150000

Sales on Cash (note2) 300000

Sales on PBS (note4) billing option 200000

Total Sales Revenue 650000

margin. Cost of sales is likewise deemed as allowable items for tax purpose since these costs are

directly incurred to generate the Corner Pharmacy revenue.

Note 2. The sales for Corner Pharmacy are cash sales, credit card sales and PBS billing icon

sales on credit card sales we are only to consider the credit card sales of $150000 and not the

reimbursed amount simply because this is what is recognized as sales the $10000 extra

reimbursement would be of course as a result of wrong entry conducted.

Note.3.The salary and rent are fixed expense which of course are allowed for tax purpose and

indeed are used to reduce the amount of the taxable income on basis of matching concept since

they match the revenue they generate hence need to allow them.

Note.4.The items under PBS i.e. opening balance ,billing, receipts and closing balance just

shows analysis of Corner Pharmacy stock that are under PBS hence it is only the billing part that

is to be factored in as part of sales thus=25000(opening balance)+200000(billing)-30000(closing

stock)=195000(receipts received or paid amount)

NB; for purposes of reporting it is assumed that Corner Pharmacy Year End of tax occurs on

30Th June 2017.

Corner Pharmacy Ltd

Taxable Income Statement

For The Tax Year End 30Th June 2017

Revenue Sales; $

Sales from Credit Card (note2) 150000

Sales on Cash (note2) 300000

Sales on PBS (note4) billing option 200000

Total Sales Revenue 650000

TAXATION LAW

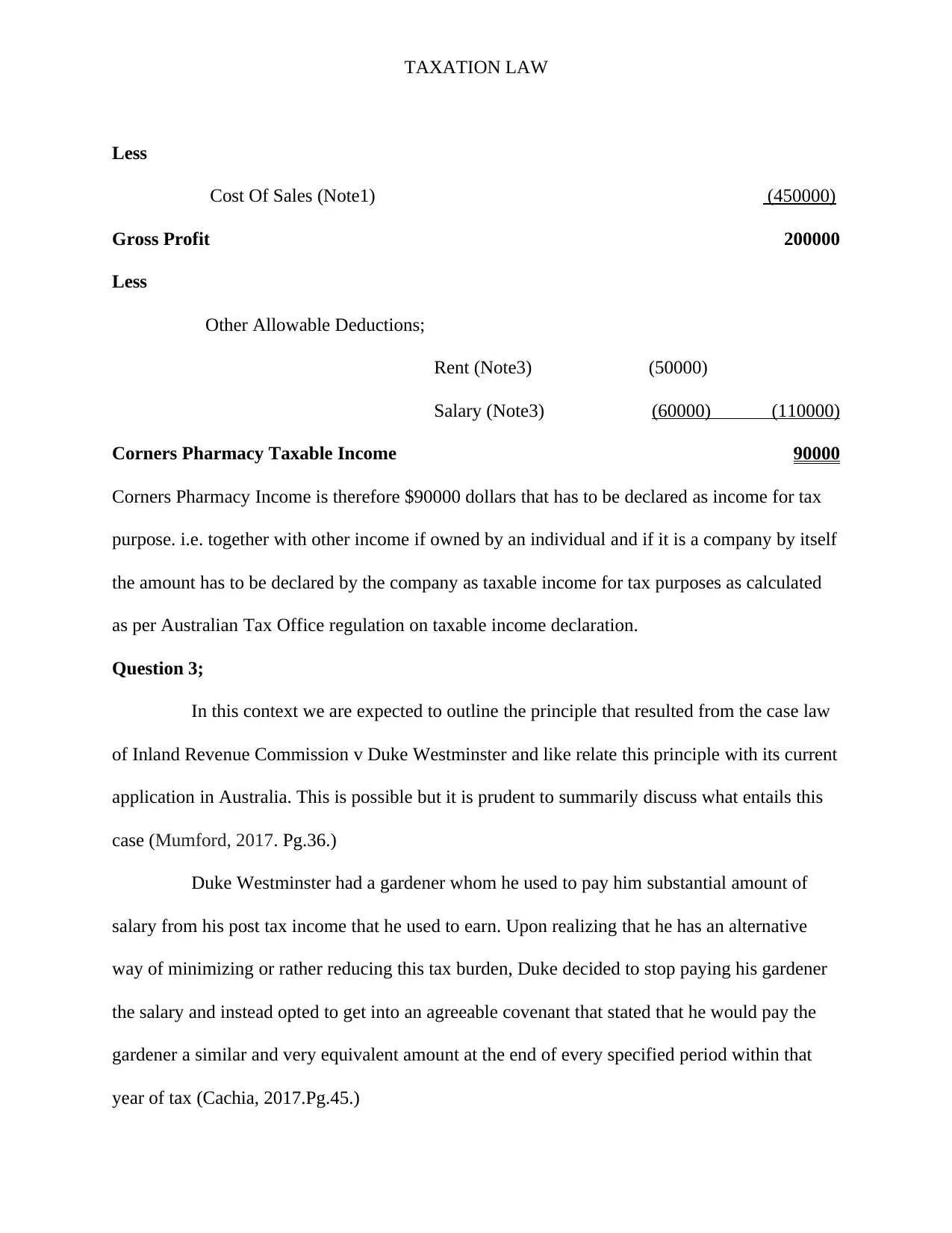

Less

Cost Of Sales (Note1) (450000)

Gross Profit 200000

Less

Other Allowable Deductions;

Rent (Note3) (50000)

Salary (Note3) (60000) (110000)

Corners Pharmacy Taxable Income 90000

Corners Pharmacy Income is therefore $90000 dollars that has to be declared as income for tax

purpose. i.e. together with other income if owned by an individual and if it is a company by itself

the amount has to be declared by the company as taxable income for tax purposes as calculated

as per Australian Tax Office regulation on taxable income declaration.

Question 3;

In this context we are expected to outline the principle that resulted from the case law

of Inland Revenue Commission v Duke Westminster and like relate this principle with its current

application in Australia. This is possible but it is prudent to summarily discuss what entails this

case (Mumford, 2017. Pg.36.)

Duke Westminster had a gardener whom he used to pay him substantial amount of

salary from his post tax income that he used to earn. Upon realizing that he has an alternative

way of minimizing or rather reducing this tax burden, Duke decided to stop paying his gardener

the salary and instead opted to get into an agreeable covenant that stated that he would pay the

gardener a similar and very equivalent amount at the end of every specified period within that

year of tax (Cachia, 2017.Pg.45.)

Less

Cost Of Sales (Note1) (450000)

Gross Profit 200000

Less

Other Allowable Deductions;

Rent (Note3) (50000)

Salary (Note3) (60000) (110000)

Corners Pharmacy Taxable Income 90000

Corners Pharmacy Income is therefore $90000 dollars that has to be declared as income for tax

purpose. i.e. together with other income if owned by an individual and if it is a company by itself

the amount has to be declared by the company as taxable income for tax purposes as calculated

as per Australian Tax Office regulation on taxable income declaration.

Question 3;

In this context we are expected to outline the principle that resulted from the case law

of Inland Revenue Commission v Duke Westminster and like relate this principle with its current

application in Australia. This is possible but it is prudent to summarily discuss what entails this

case (Mumford, 2017. Pg.36.)

Duke Westminster had a gardener whom he used to pay him substantial amount of

salary from his post tax income that he used to earn. Upon realizing that he has an alternative

way of minimizing or rather reducing this tax burden, Duke decided to stop paying his gardener

the salary and instead opted to get into an agreeable covenant that stated that he would pay the

gardener a similar and very equivalent amount at the end of every specified period within that

year of tax (Cachia, 2017.Pg.45.)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TAXATION LAW

According to Inland Revenue Tax Office regulation at this time of Duke Case, the law

allowed Duke to claim this equivalent amount he was to pay the gardener as an allowable

expense for tax purpose hence reducing the tax liability burden and surtax in totality

(Likhovski,2006.Pg.45.) This indeed did not sound legally friendly to Inland Revenue

Commission for tax purpose hence opted to file a suit against Duke Westminster with the case

citing that Duke was evading paying tax by claiming allowable that were not within the

regulation of the tax man (Hayward, 2014.Pg.52.)

Upon hearing the case, judge Lord Tomlin ruled in favor of Duke claiming that this

arrangement had no traces of tax evasion hence ruled further by saying that every tax payer is

allowed by the law to conduct his or her own local arrangements under his works so as to free

himself from any tax attached to his venture if he legally succeeds in that arrange no body in

whatsoever means is allowed to compel him to pay the tax whether it is appreciative or not to the

Inland Commissioner or not his arrangement is legally accepted in the law (Christians,

2014.Pg.39.)

This case therefore resulted to a principle of tax avoidance which is defined as an

arrangement of financial affairs that is legal in nature that sees into it that tax burden is

minimized as per the set regulation (Ostwal and Vijayaraghavan, 2010.Pg.35.) In Australia tax

avoidance has not been fair to the tax man at all over the recent years; this is so due to

conversion of this policy to tax fraud and at some point tax evasion. Tax payers have taken

advantage of tax avoidance to a point whereby they are seen engaging themselves in tax fraud

activities hoping that they will get relieve in court on aspect of tax avoidance.

According to Inland Revenue Tax Office regulation at this time of Duke Case, the law

allowed Duke to claim this equivalent amount he was to pay the gardener as an allowable

expense for tax purpose hence reducing the tax liability burden and surtax in totality

(Likhovski,2006.Pg.45.) This indeed did not sound legally friendly to Inland Revenue

Commission for tax purpose hence opted to file a suit against Duke Westminster with the case

citing that Duke was evading paying tax by claiming allowable that were not within the

regulation of the tax man (Hayward, 2014.Pg.52.)

Upon hearing the case, judge Lord Tomlin ruled in favor of Duke claiming that this

arrangement had no traces of tax evasion hence ruled further by saying that every tax payer is

allowed by the law to conduct his or her own local arrangements under his works so as to free

himself from any tax attached to his venture if he legally succeeds in that arrange no body in

whatsoever means is allowed to compel him to pay the tax whether it is appreciative or not to the

Inland Commissioner or not his arrangement is legally accepted in the law (Christians,

2014.Pg.39.)

This case therefore resulted to a principle of tax avoidance which is defined as an

arrangement of financial affairs that is legal in nature that sees into it that tax burden is

minimized as per the set regulation (Ostwal and Vijayaraghavan, 2010.Pg.35.) In Australia tax

avoidance has not been fair to the tax man at all over the recent years; this is so due to

conversion of this policy to tax fraud and at some point tax evasion. Tax payers have taken

advantage of tax avoidance to a point whereby they are seen engaging themselves in tax fraud

activities hoping that they will get relieve in court on aspect of tax avoidance.

TAXATION LAW

Over the years Australian courts have seen litigation suits that involved tax payers

who have evaded tax as others fraudulently engage themselves in actions that are seen to shift tax

burden to unlawful tax bracket. This ideally has minimized revenue being collected by the tax

man in Australia hence causing deficit in countries revenue. It is through these activities of fraud

and evasion that has indeed affected Australia to a point that they were forced to introduce

agencies that would help them curb tax evasion and fraud (Dyreng, Hanlon and Maydew,

2008.Pg.80.)

Over the years tax avoidance has never been fair for Australian Tax Office since these

agencies were given full support to secure the tax man i.e. Australia Tax Office its initial position

on tax collection. Tax avoidance has affected Australia task office till 2016 when these agencies

were formed (Martins, 2018.Pg.75.) The first agency to be formed was Tax Avoidance Task

whose core purpose was to scrutinize tax related issues of multinational firms, wealthy investors,

large groups i.e. both private and public to a point where these entities a paying the right tax and

within the right period.

Tax avoidance task force had to ensure that there exist tax compliance by these

entities hence a great improvement in the integrity of Australian Tax System. This tax avoidance

agency indeed brought this into books to a point that the citizens came to appreciate the essence

of indeed complying with tax department requirement hence on revenue bases the government

was able to redeem back their tax collection capacity (Desai and Dharmapala, 2009.540.)

This achievement by Tax Avoidance Task agency that saw into it the bouncing back

of tax compliance as well as tax collection was as a result of multinational anti-avoidance

legislation and legislation on diversions of profits. It is therefore clear that the principle of tax

avoidance that resulted from IRC V Duke Westminster negatively affected Australian Tax Office

Over the years Australian courts have seen litigation suits that involved tax payers

who have evaded tax as others fraudulently engage themselves in actions that are seen to shift tax

burden to unlawful tax bracket. This ideally has minimized revenue being collected by the tax

man in Australia hence causing deficit in countries revenue. It is through these activities of fraud

and evasion that has indeed affected Australia to a point that they were forced to introduce

agencies that would help them curb tax evasion and fraud (Dyreng, Hanlon and Maydew,

2008.Pg.80.)

Over the years tax avoidance has never been fair for Australian Tax Office since these

agencies were given full support to secure the tax man i.e. Australia Tax Office its initial position

on tax collection. Tax avoidance has affected Australia task office till 2016 when these agencies

were formed (Martins, 2018.Pg.75.) The first agency to be formed was Tax Avoidance Task

whose core purpose was to scrutinize tax related issues of multinational firms, wealthy investors,

large groups i.e. both private and public to a point where these entities a paying the right tax and

within the right period.

Tax avoidance task force had to ensure that there exist tax compliance by these

entities hence a great improvement in the integrity of Australian Tax System. This tax avoidance

agency indeed brought this into books to a point that the citizens came to appreciate the essence

of indeed complying with tax department requirement hence on revenue bases the government

was able to redeem back their tax collection capacity (Desai and Dharmapala, 2009.540.)

This achievement by Tax Avoidance Task agency that saw into it the bouncing back

of tax compliance as well as tax collection was as a result of multinational anti-avoidance

legislation and legislation on diversions of profits. It is therefore clear that the principle of tax

avoidance that resulted from IRC V Duke Westminster negatively affected Australian Tax Office

TAXATION LAW

on tax collection due to tax fraud and evasion swap advantage to a point of introduction of

agencies to curb the monster (Sikka, 2012.Pg.25.)

Question 4;

Australian Tax Office is very keen on losses that are deemed business related since

most tax payers are seen to fraud the tax man and use loss that are not related to net off other

incomes they earn (Slemrod, 2009.Pg.390.) ATO on losses is likewise very categorical that only

those business loss incurred on business related aspect is deemed ready to be carried forward. In

the context rental loss the law requires rental owners to proof that the loss is indeed i.e. genuine

by clearly indicating that indeed it deed all that was required to control the loss.

It is likewise clear that for a rental loss to be netted off one income it must proof that

there is proper connection to the operation of that firm. For instance in this case of rental loss

Joseph has to proof that he entirely controls and manage the operations of the rental such that the

loss incurred was not out of malice for operation (Isa, 2014.Pg.60.) In this case if Joseph indeed

has incurred the loss out of his efforts of ensuring the rental business property operates in a

manner that was to earn him income, since the agreement to have all the 100% portion of the loss

be incurred by Joseph he is indeed allowed by the law to net off his accountant professional

income less the loss on rental. However if he has not been taking care of the rental property thus

the cause of the loss he is barred by the regulation to claim this loss as allowable deduction.

In case of disposal of this rental property of Joseph and Jane ideally it is expected that

a capital gain or loss occurs hence the agreement ratio policy stands whereby if it is again on

disposal a capital gain has to be disclosed by Joseph at 20% the amount as addition in his

accountancy income while the 80% has to be declare by Jane as her rental income (Piketty,

2015.Pg.50.) However the agreement seems to do some tax avoidance relieve simply because

on tax collection due to tax fraud and evasion swap advantage to a point of introduction of

agencies to curb the monster (Sikka, 2012.Pg.25.)

Question 4;

Australian Tax Office is very keen on losses that are deemed business related since

most tax payers are seen to fraud the tax man and use loss that are not related to net off other

incomes they earn (Slemrod, 2009.Pg.390.) ATO on losses is likewise very categorical that only

those business loss incurred on business related aspect is deemed ready to be carried forward. In

the context rental loss the law requires rental owners to proof that the loss is indeed i.e. genuine

by clearly indicating that indeed it deed all that was required to control the loss.

It is likewise clear that for a rental loss to be netted off one income it must proof that

there is proper connection to the operation of that firm. For instance in this case of rental loss

Joseph has to proof that he entirely controls and manage the operations of the rental such that the

loss incurred was not out of malice for operation (Isa, 2014.Pg.60.) In this case if Joseph indeed

has incurred the loss out of his efforts of ensuring the rental business property operates in a

manner that was to earn him income, since the agreement to have all the 100% portion of the loss

be incurred by Joseph he is indeed allowed by the law to net off his accountant professional

income less the loss on rental. However if he has not been taking care of the rental property thus

the cause of the loss he is barred by the regulation to claim this loss as allowable deduction.

In case of disposal of this rental property of Joseph and Jane ideally it is expected that

a capital gain or loss occurs hence the agreement ratio policy stands whereby if it is again on

disposal a capital gain has to be disclosed by Joseph at 20% the amount as addition in his

accountancy income while the 80% has to be declare by Jane as her rental income (Piketty,

2015.Pg.50.) However the agreement seems to do some tax avoidance relieve simply because

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TAXATION LAW

when it comes to gain sharing and the fact that Joseph has an extra income his portion of income

is less while Jane is more similarly to what happens in cases of loss (Mellon, 2016.Pg.56)if it is a

business loss Joseph is allowed the 100% portion so as to minimize the taxable income from his

accountancy professional amount and incase of capital loss the 100% portion is seen to minimize

his capital gain (Burman, 2010.Pg.4) but of course on future basis.

.

when it comes to gain sharing and the fact that Joseph has an extra income his portion of income

is less while Jane is more similarly to what happens in cases of loss (Mellon, 2016.Pg.56)if it is a

business loss Joseph is allowed the 100% portion so as to minimize the taxable income from his

accountancy professional amount and incase of capital loss the 100% portion is seen to minimize

his capital gain (Burman, 2010.Pg.4) but of course on future basis.

.

TAXATION LAW

References;

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18

Burman, L.E., 2010. The labyrinth of capital gains tax policy: A guide for the perplexed.

Brookings Institution Press.

Cachia, F., 2017. Aggressive Tax Planning: An Analysis from an EU Perspective. EC Tax

Review, 26(5), pp.257-273

Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

Desai, M.A. and Dharmapala, D., 2009. Corporate tax avoidance and firm value. The review of

Economics and Statistics, 91(3), pp.537-546.

Dyreng, S.D., Hanlon, M. and Maydew, E.L., 2008. Long-run corporate tax avoidance. the

accounting review, 83(1), pp.61-82.

Freedman, J. and Crawford, C., 2010. Small business taxation.

Hayward, R. ed., 2014. Valuation: principles into practice. Taylor & Francis.

Isa, K., 2014. Tax complexities in the Malaysian corporate tax system: minimise to

maximize. International Journal of Law and Management, 56(1), pp.50-65.

Likhovski, A., 2006. Tax law and public opinion: Explaining IRC v. Duke of Westminster

References;

Blakelock, S. and King, P., 2017. Taxation law: The advance of ATO data matching. Proctor,

The, 37(6), p.18

Burman, L.E., 2010. The labyrinth of capital gains tax policy: A guide for the perplexed.

Brookings Institution Press.

Cachia, F., 2017. Aggressive Tax Planning: An Analysis from an EU Perspective. EC Tax

Review, 26(5), pp.257-273

Christians, A., 2014. Avoidance, evasion, and taxpayer morality. Wash. UJL & Pol'y, 44, p.39.

Desai, M.A. and Dharmapala, D., 2009. Corporate tax avoidance and firm value. The review of

Economics and Statistics, 91(3), pp.537-546.

Dyreng, S.D., Hanlon, M. and Maydew, E.L., 2008. Long-run corporate tax avoidance. the

accounting review, 83(1), pp.61-82.

Freedman, J. and Crawford, C., 2010. Small business taxation.

Hayward, R. ed., 2014. Valuation: principles into practice. Taylor & Francis.

Isa, K., 2014. Tax complexities in the Malaysian corporate tax system: minimise to

maximize. International Journal of Law and Management, 56(1), pp.50-65.

Likhovski, A., 2006. Tax law and public opinion: Explaining IRC v. Duke of Westminster

TAXATION LAW

Martins, P., 2018. TD 2017/20. Taxation in Australia, 52(10), p.562.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge

Ostwal, T.P. and Vijayaraghavan, V., 2010. Anti-Avoidance Measures. National Law School of

India Review, 22(2), pp.59-103.

Philander, K.S., 2013. A normative analysis of gambling tax policy. UNLV Gaming Research &

Review Journal, 17(2), p.2.

Piketty, T., 2015. About capital in the twenty-first century.American Economic Review, 105(5),

pp.48-53.

Sikka, P., 2012. The tax avoidance industry. Radical Statistics,107, pp.15-30.

Slemrod, J., 2009. Lessons for tax policy in the Great Recession. National Tax Journal, pp.387-

397.

Tretola, J., 2013. Turning gambling silver into tax gold?.Revenue Law Journal, 23(1), p.5.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

Martins, P., 2018. TD 2017/20. Taxation in Australia, 52(10), p.562.

Mellon, A.W., 2016. Taxation: the people’s business. Pickle Partners Publishing.

Mumford, A., 2017. Taxing culture: towards a theory of tax collection law. Routledge

Ostwal, T.P. and Vijayaraghavan, V., 2010. Anti-Avoidance Measures. National Law School of

India Review, 22(2), pp.59-103.

Philander, K.S., 2013. A normative analysis of gambling tax policy. UNLV Gaming Research &

Review Journal, 17(2), p.2.

Piketty, T., 2015. About capital in the twenty-first century.American Economic Review, 105(5),

pp.48-53.

Sikka, P., 2012. The tax avoidance industry. Radical Statistics,107, pp.15-30.

Slemrod, J., 2009. Lessons for tax policy in the Great Recession. National Tax Journal, pp.387-

397.

Tretola, J., 2013. Turning gambling silver into tax gold?.Revenue Law Journal, 23(1), p.5.

Woellner, R.H., Barkoczy, S., Murphy, S., Evans, C. and Pinto, D., 2010. Australian taxation

law. CCH Australia.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.