Taxation Law Assignment: Analysis of Australian Taxation Law

VerifiedAdded on 2020/10/22

|14

|3968

|303

Homework Assignment

AI Summary

This assignment solution comprehensively addresses various facets of Australian taxation law. It begins with an introduction and proceeds to answer several questions covering taxation rulings, details of the Income Tax Assessment Act 1997 regarding tax offsets, and the top tax rates applicable to residents in the 2018/19 tax year. The solution further provides examples of assets exempt from capital gains tax (CGT) and explains CGT event B1. The assignment also includes the formula contained in s4-10(3) ITAA 1997 and discusses the significance of the High Court case, FC of T v Day 2008, in the context of deductions, along with the difference between marginal and average tax rates, and consumption tax. Question 2 delves into allowable tax deductions, providing examples related to interest expenses, phone and internet usage, childcare expenses, theft losses, and election expenses. Question 3 explores CGT implications in scenarios involving land leases, farm purchases, and property sales. Finally, Question 4 analyzes the tax treatment of various income sources, including prizes, business travel, phone benefits, personal injury damages, and income from shares and securities. The assignment concludes with a case study on Nisu, providing a complete overview of Australian taxation principles.

Taxation Law Of

Australia

Australia

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Taxation ruling TR 2018/4 ....................................................................................................1

B) Division of income tax assessment act 1997 details available tax offset...............................1

C) Top tax rate applicable to a resident taxpayer in the 2018/19 tax year...................................1

D) Example of an asset that is exempt from capital gains tax, including its legislative reference

......................................................................................................................................................1

E) CGT event B1 s104-15 tax......................................................................................................2

F) Formula contained in s4-10(3) ITAA 1997.............................................................................2

G) Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of

deductions....................................................................................................................................2

H) Difference between marginal rate of tax and average rate of tax...........................................2

I) Consumption tax......................................................................................................................3

QUESTION 2...................................................................................................................................4

a....................................................................................................................................................4

b....................................................................................................................................................4

c....................................................................................................................................................4

d....................................................................................................................................................4

e....................................................................................................................................................5

QUESTION 3 ..................................................................................................................................5

a. Andy owns some land along with grants a lease to Brian for five years with premium of

$5000............................................................................................................................................5

b. Purchase of 100 acre farm outside Adelaide............................................................................5

C) sale of house that was purchased in 2006...............................................................................5

D) net gain of Chris......................................................................................................................6

QUESTION 4...................................................................................................................................6

A) Prize received worth $2,000 for the best TV advertisement of the year................................6

B) Amount received for business travel.......................................................................................6

C) Phone received from client.....................................................................................................7

INTRODUCTION...........................................................................................................................1

QUESTION 1...................................................................................................................................1

A) Taxation ruling TR 2018/4 ....................................................................................................1

B) Division of income tax assessment act 1997 details available tax offset...............................1

C) Top tax rate applicable to a resident taxpayer in the 2018/19 tax year...................................1

D) Example of an asset that is exempt from capital gains tax, including its legislative reference

......................................................................................................................................................1

E) CGT event B1 s104-15 tax......................................................................................................2

F) Formula contained in s4-10(3) ITAA 1997.............................................................................2

G) Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of

deductions....................................................................................................................................2

H) Difference between marginal rate of tax and average rate of tax...........................................2

I) Consumption tax......................................................................................................................3

QUESTION 2...................................................................................................................................4

a....................................................................................................................................................4

b....................................................................................................................................................4

c....................................................................................................................................................4

d....................................................................................................................................................4

e....................................................................................................................................................5

QUESTION 3 ..................................................................................................................................5

a. Andy owns some land along with grants a lease to Brian for five years with premium of

$5000............................................................................................................................................5

b. Purchase of 100 acre farm outside Adelaide............................................................................5

C) sale of house that was purchased in 2006...............................................................................5

D) net gain of Chris......................................................................................................................6

QUESTION 4...................................................................................................................................6

A) Prize received worth $2,000 for the best TV advertisement of the year................................6

B) Amount received for business travel.......................................................................................6

C) Phone received from client.....................................................................................................7

D) Damage received for personal injury......................................................................................7

E) Income from shares and securities..........................................................................................7

QUESTION 5...................................................................................................................................8

Nisu case study............................................................................................................................8

REFERENCES..............................................................................................................................10

E) Income from shares and securities..........................................................................................7

QUESTION 5...................................................................................................................................8

Nisu case study............................................................................................................................8

REFERENCES..............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

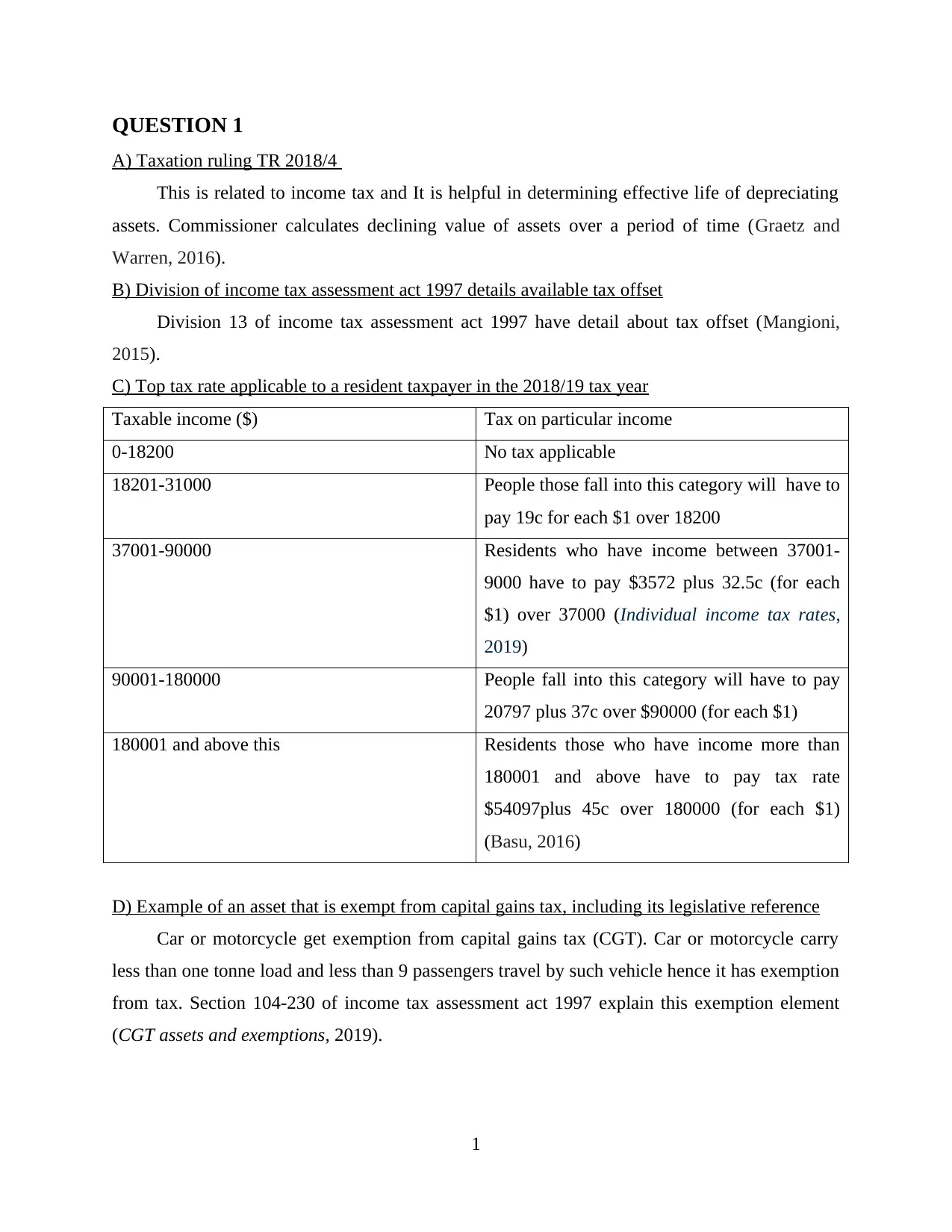

QUESTION 1

A) Taxation ruling TR 2018/4

This is related to income tax and It is helpful in determining effective life of depreciating

assets. Commissioner calculates declining value of assets over a period of time (Graetz and

Warren, 2016).

B) Division of income tax assessment act 1997 details available tax offset

Division 13 of income tax assessment act 1997 have detail about tax offset (Mangioni,

2015).

C) Top tax rate applicable to a resident taxpayer in the 2018/19 tax year

Taxable income ($) Tax on particular income

0-18200 No tax applicable

18201-31000 People those fall into this category will have to

pay 19c for each $1 over 18200

37001-90000 Residents who have income between 37001-

9000 have to pay $3572 plus 32.5c (for each

$1) over 37000 (Individual income tax rates,

2019)

90001-180000 People fall into this category will have to pay

20797 plus 37c over $90000 (for each $1)

180001 and above this Residents those who have income more than

180001 and above have to pay tax rate

$54097plus 45c over 180000 (for each $1)

(Basu, 2016)

D) Example of an asset that is exempt from capital gains tax, including its legislative reference

Car or motorcycle get exemption from capital gains tax (CGT). Car or motorcycle carry

less than one tonne load and less than 9 passengers travel by such vehicle hence it has exemption

from tax. Section 104-230 of income tax assessment act 1997 explain this exemption element

(CGT assets and exemptions, 2019).

1

A) Taxation ruling TR 2018/4

This is related to income tax and It is helpful in determining effective life of depreciating

assets. Commissioner calculates declining value of assets over a period of time (Graetz and

Warren, 2016).

B) Division of income tax assessment act 1997 details available tax offset

Division 13 of income tax assessment act 1997 have detail about tax offset (Mangioni,

2015).

C) Top tax rate applicable to a resident taxpayer in the 2018/19 tax year

Taxable income ($) Tax on particular income

0-18200 No tax applicable

18201-31000 People those fall into this category will have to

pay 19c for each $1 over 18200

37001-90000 Residents who have income between 37001-

9000 have to pay $3572 plus 32.5c (for each

$1) over 37000 (Individual income tax rates,

2019)

90001-180000 People fall into this category will have to pay

20797 plus 37c over $90000 (for each $1)

180001 and above this Residents those who have income more than

180001 and above have to pay tax rate

$54097plus 45c over 180000 (for each $1)

(Basu, 2016)

D) Example of an asset that is exempt from capital gains tax, including its legislative reference

Car or motorcycle get exemption from capital gains tax (CGT). Car or motorcycle carry

less than one tonne load and less than 9 passengers travel by such vehicle hence it has exemption

from tax. Section 104-230 of income tax assessment act 1997 explain this exemption element

(CGT assets and exemptions, 2019).

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

E) CGT event B1 s104-15 tax

This event is applicable if the organisation make contract with other enterprise. In this first

party can enjoy and use the CGT asset before passing rights to other entity. Title or ownership of

that asset will be passed to other party or entity at the time of end of agreement (Berns, 2018).

F) Formula contained in s4-10(3) ITAA 1997

It is very important for resident and non-resident that to pay income tax if they fall in tax

category. Tax payers calculate their income by using specific formula. Formula of income tax

calculation set is”

Income tax= taxable income*rate)- tax offsets (It is set in s4-10(3))

Taxable income= assessable income- deduction

G) Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of

deductions

FC of T v Day 2008 was the case in which person was working as compliance officer in

Australian custom service department (Clibborn, 2018). It is essential for a public servant that to

fulfil their duties carefully, if individual gets failed to complete their duty on time with efficiency

then individual will be liable to pay compensation for the same. This compensation or legal

expenses are in the form of dismissal, demotion, salary deduction etc. Respondent was charged

in the year 1998 for the first time and in the year 1999 third charges were applicable for him.

Section8-1 (1) of ITA 1997 explains that deduction from assessable income is done only when it

is incurred for gaining additional income (FC of T v DAY, High Court of Australia, 12 November

2008, 2019).

It is essential for each public officer that to complete their duties carefully, they have to

fulfil those obligations for that they are accountable. If they fail to do the same then they may

have to [ay legal expenses in the form of salary deduction or demotion. This application is very

important as it guides officers those who are public servant that they have to work with

dedication otherwise they may lose their job.

H) Difference between marginal rate of tax and average rate of tax

Marginal rate of tax Average rate of tax

It analyses how tax impact on incentive

earning, savings and interest .

It analyses household’s tax burden that means

it measure impact of tax on household’s ability

to consume.

2

This event is applicable if the organisation make contract with other enterprise. In this first

party can enjoy and use the CGT asset before passing rights to other entity. Title or ownership of

that asset will be passed to other party or entity at the time of end of agreement (Berns, 2018).

F) Formula contained in s4-10(3) ITAA 1997

It is very important for resident and non-resident that to pay income tax if they fall in tax

category. Tax payers calculate their income by using specific formula. Formula of income tax

calculation set is”

Income tax= taxable income*rate)- tax offsets (It is set in s4-10(3))

Taxable income= assessable income- deduction

G) Significance of the High Court case, FC of T v Day 2008 ATC 20-064 in the topic of

deductions

FC of T v Day 2008 was the case in which person was working as compliance officer in

Australian custom service department (Clibborn, 2018). It is essential for a public servant that to

fulfil their duties carefully, if individual gets failed to complete their duty on time with efficiency

then individual will be liable to pay compensation for the same. This compensation or legal

expenses are in the form of dismissal, demotion, salary deduction etc. Respondent was charged

in the year 1998 for the first time and in the year 1999 third charges were applicable for him.

Section8-1 (1) of ITA 1997 explains that deduction from assessable income is done only when it

is incurred for gaining additional income (FC of T v DAY, High Court of Australia, 12 November

2008, 2019).

It is essential for each public officer that to complete their duties carefully, they have to

fulfil those obligations for that they are accountable. If they fail to do the same then they may

have to [ay legal expenses in the form of salary deduction or demotion. This application is very

important as it guides officers those who are public servant that they have to work with

dedication otherwise they may lose their job.

H) Difference between marginal rate of tax and average rate of tax

Marginal rate of tax Average rate of tax

It analyses how tax impact on incentive

earning, savings and interest .

It analyses household’s tax burden that means

it measure impact of tax on household’s ability

to consume.

2

It is incremental tax that is paid on additional

income (incremental income)

It is calculated by dividing total amount of tax

from actual (total) income.

It is the percentage of tax which is paid by

person on their next dollar of taxable income.

It is percentage of actual taxable income of

person which is paid by individual.

I) Consumption tax

It is the tax which is paid by person on purchasing of particular goods and services. It is in

the form of sales taxes, excise, import duties etc. Such kind of taxes are paid by consumers those

who pay higher retail prices for their purchased goods. Vendors, local or state government

collect that tax fund. Different tax rates are applicable on different commodities that highly

depends upon the luxury or necessity of item. There is huge difference between consumption and

income tax, as consumption tax is applicable when a person spends some money whereas income

tax is applicable when individual earn some money. Consumption tax helps in raising economic

efficiency.

3

income (incremental income)

It is calculated by dividing total amount of tax

from actual (total) income.

It is the percentage of tax which is paid by

person on their next dollar of taxable income.

It is percentage of actual taxable income of

person which is paid by individual.

I) Consumption tax

It is the tax which is paid by person on purchasing of particular goods and services. It is in

the form of sales taxes, excise, import duties etc. Such kind of taxes are paid by consumers those

who pay higher retail prices for their purchased goods. Vendors, local or state government

collect that tax fund. Different tax rates are applicable on different commodities that highly

depends upon the luxury or necessity of item. There is huge difference between consumption and

income tax, as consumption tax is applicable when a person spends some money whereas income

tax is applicable when individual earn some money. Consumption tax helps in raising economic

efficiency.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

Assessment of allowable tax deduction is enumerated below:

a.

Given case presents that Brett incurred interest expenses on loan with regards to meet

obligation pertaining to employee wages. In this regard, business entity can claim for deduction

pertaining to expenditure associated with business activities. ATO’s guidelines clearly present

that one can claim for deduction when all the expenses are incurred for running or carry out

business (Deductions, 2019). Thus, it can be stated that deductions are allowed on interest

amount associated with loan.

b.

As per the Australian taxation office (ATO), one can claim for deduction if phone or

internet is used for work related aspects. By doing assessment, it has found that when phone is

used for both work and private purpose then deduction considered by ATO up to the amount

related to working practices (Claiming mobile phone, internet and home phone expenses, 2019).

In the current case, Julie incurred $500 as mobile phone charge but out of this 40% relates to

personal work. On the basis of this, only $300 ($500 * 60%) comes under the category of

allowable deduction during the current tax period.

c.

On the basis of given case scenario Sally paid $1200 to babysitter for looking after her

children. As per ATO rules and regulations, Sally can claim for deduction or childcare tax credit.

As, Sally incurred such expenses for the sake of employment which in turn fulfils the conditions

imposed by ATO (Can You Write Off Babysitting Expenses?, 2019). Referring all such aspects, it

can be stated that Sally can reduce the level of taxes owed due to babysitter expenses.

d.

Referring Income Tax Assessment Act (1997), it can be presented that losses occurred

due to theft falls under the category of tax deduction. According to ATO , one can deduct loss

only when it occurred in the income year. Further, deduction is allowed when loss occurred due

to employee’s theft. Cited case situation clearly presents that loss of $20000 occurred as Jerry’s

long term employee stole goods. Thus, according to income tax rules Jerry can claim for

deduction.

4

Assessment of allowable tax deduction is enumerated below:

a.

Given case presents that Brett incurred interest expenses on loan with regards to meet

obligation pertaining to employee wages. In this regard, business entity can claim for deduction

pertaining to expenditure associated with business activities. ATO’s guidelines clearly present

that one can claim for deduction when all the expenses are incurred for running or carry out

business (Deductions, 2019). Thus, it can be stated that deductions are allowed on interest

amount associated with loan.

b.

As per the Australian taxation office (ATO), one can claim for deduction if phone or

internet is used for work related aspects. By doing assessment, it has found that when phone is

used for both work and private purpose then deduction considered by ATO up to the amount

related to working practices (Claiming mobile phone, internet and home phone expenses, 2019).

In the current case, Julie incurred $500 as mobile phone charge but out of this 40% relates to

personal work. On the basis of this, only $300 ($500 * 60%) comes under the category of

allowable deduction during the current tax period.

c.

On the basis of given case scenario Sally paid $1200 to babysitter for looking after her

children. As per ATO rules and regulations, Sally can claim for deduction or childcare tax credit.

As, Sally incurred such expenses for the sake of employment which in turn fulfils the conditions

imposed by ATO (Can You Write Off Babysitting Expenses?, 2019). Referring all such aspects, it

can be stated that Sally can reduce the level of taxes owed due to babysitter expenses.

d.

Referring Income Tax Assessment Act (1997), it can be presented that losses occurred

due to theft falls under the category of tax deduction. According to ATO , one can deduct loss

only when it occurred in the income year. Further, deduction is allowed when loss occurred due

to employee’s theft. Cited case situation clearly presents that loss of $20000 occurred as Jerry’s

long term employee stole goods. Thus, according to income tax rules Jerry can claim for

deduction.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

e.

In accordance with ATO rules candidate, who participating in election, is allowable to do

claim for deduction purpose. As per the cited case, expenditure incurred in local government

election and party accounts for $5000 & $2000 respectively. ATO states that only $1000

deduction is allowed that incurred in local government election (Election expenses, 2019). On

the basis of such aspect, out of $5000, election expenses of $4000 will be the part of taxable

income. Further, tax will also be calculated on the expenses of $2000 as no deduction are

allowed on this.

QUESTION 3

a. Andy owns some land along with grants a lease to Brian for five years with premium of $5000

It is short lease as computation of CGT as short lease is slightly very complex. The lease

with useful life is less than 50 years as wasting asset. This depreciate over time with allowable

base cost for CGT with objective to imply lease depreciation. The allowable cost of base is

original cost of acquisition multiplied with fraction of S/P where S is percentage through lease

depreciation table for years of lease with assignment of date. However, P is replicated as

percentage through lease depreciation table for years of lease remaining purchase date. The

grants for short lease as premium retained with grant must split among amount chargeable to

income tax (Capital gains tax on property leases, 2019). (Property income rule ITTOIA 2005 S

277 (4)) along with amount chargeable to CGT. The capital element chargeable to CGT is 2% *

(N-1) * P. N is number of years of the lease and P as premium retained.

b. Purchase of 100 acre farm outside Adelaide

There was exchange for sum of $40000 to Farm Ltd, as per time value concept its value

would increase. Thus, it would be excluded from sum of $800000 and chargeable from capital

gain tax.

C) sale of house that was purchased in 2006

If the property is being purchased after September 21, 1999, and the individual was in the

ownership condition for more than 12 months, the 50% CGT discount will be applicable over the

property.

Jemie and Oliva purchased house in January 2006 and put it into the rent. They were in

the ownership condition for more than 12 months. In this regard, it completes the consequence of

2018/19 tax and hence, 50% discount would be applicable for Jamie and Olivia

5

In accordance with ATO rules candidate, who participating in election, is allowable to do

claim for deduction purpose. As per the cited case, expenditure incurred in local government

election and party accounts for $5000 & $2000 respectively. ATO states that only $1000

deduction is allowed that incurred in local government election (Election expenses, 2019). On

the basis of such aspect, out of $5000, election expenses of $4000 will be the part of taxable

income. Further, tax will also be calculated on the expenses of $2000 as no deduction are

allowed on this.

QUESTION 3

a. Andy owns some land along with grants a lease to Brian for five years with premium of $5000

It is short lease as computation of CGT as short lease is slightly very complex. The lease

with useful life is less than 50 years as wasting asset. This depreciate over time with allowable

base cost for CGT with objective to imply lease depreciation. The allowable cost of base is

original cost of acquisition multiplied with fraction of S/P where S is percentage through lease

depreciation table for years of lease with assignment of date. However, P is replicated as

percentage through lease depreciation table for years of lease remaining purchase date. The

grants for short lease as premium retained with grant must split among amount chargeable to

income tax (Capital gains tax on property leases, 2019). (Property income rule ITTOIA 2005 S

277 (4)) along with amount chargeable to CGT. The capital element chargeable to CGT is 2% *

(N-1) * P. N is number of years of the lease and P as premium retained.

b. Purchase of 100 acre farm outside Adelaide

There was exchange for sum of $40000 to Farm Ltd, as per time value concept its value

would increase. Thus, it would be excluded from sum of $800000 and chargeable from capital

gain tax.

C) sale of house that was purchased in 2006

If the property is being purchased after September 21, 1999, and the individual was in the

ownership condition for more than 12 months, the 50% CGT discount will be applicable over the

property.

Jemie and Oliva purchased house in January 2006 and put it into the rent. They were in

the ownership condition for more than 12 months. In this regard, it completes the consequence of

2018/19 tax and hence, 50% discount would be applicable for Jamie and Olivia

5

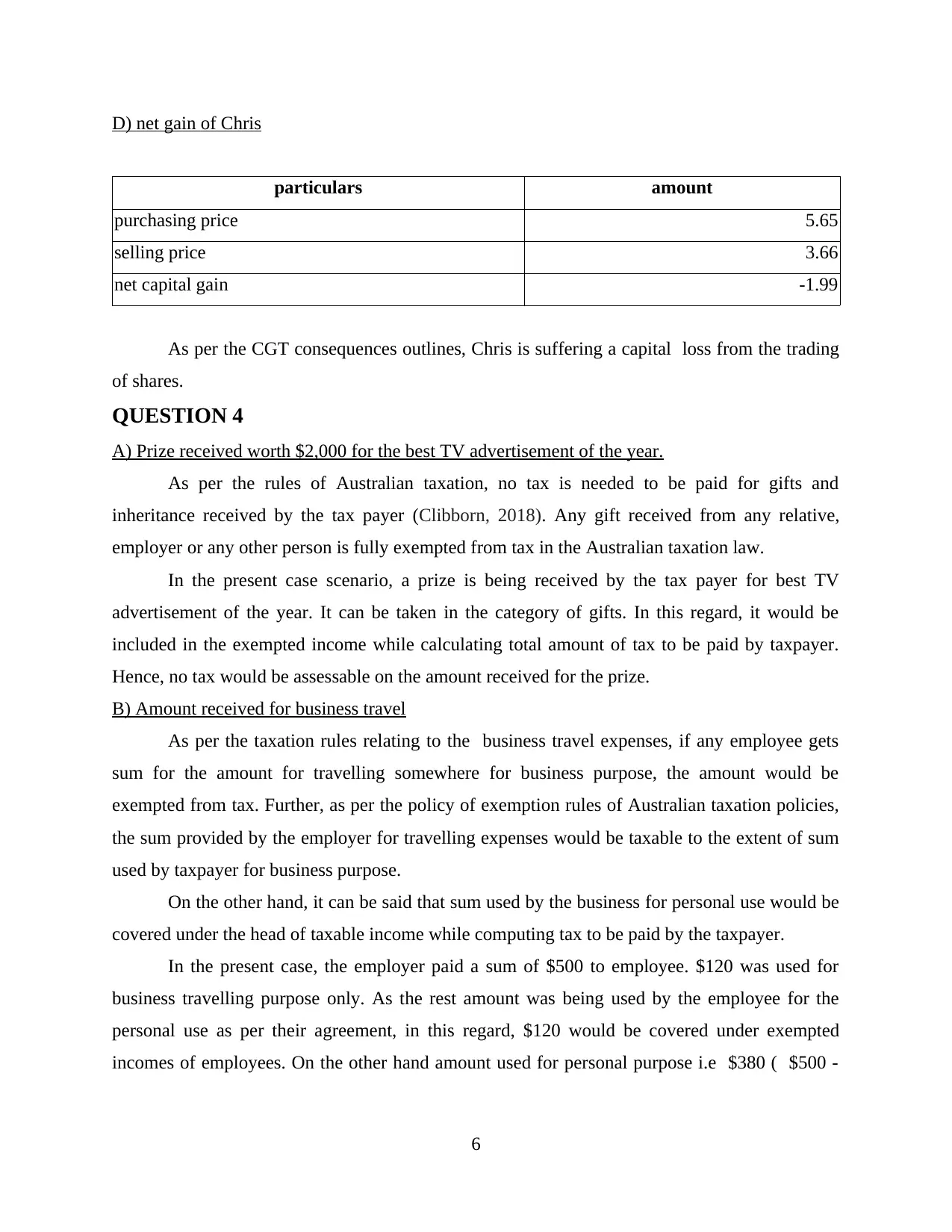

D) net gain of Chris

particulars amount

purchasing price 5.65

selling price 3.66

net capital gain -1.99

As per the CGT consequences outlines, Chris is suffering a capital loss from the trading

of shares.

QUESTION 4

A) Prize received worth $2,000 for the best TV advertisement of the year.

As per the rules of Australian taxation, no tax is needed to be paid for gifts and

inheritance received by the tax payer (Clibborn, 2018). Any gift received from any relative,

employer or any other person is fully exempted from tax in the Australian taxation law.

In the present case scenario, a prize is being received by the tax payer for best TV

advertisement of the year. It can be taken in the category of gifts. In this regard, it would be

included in the exempted income while calculating total amount of tax to be paid by taxpayer.

Hence, no tax would be assessable on the amount received for the prize.

B) Amount received for business travel

As per the taxation rules relating to the business travel expenses, if any employee gets

sum for the amount for travelling somewhere for business purpose, the amount would be

exempted from tax. Further, as per the policy of exemption rules of Australian taxation policies,

the sum provided by the employer for travelling expenses would be taxable to the extent of sum

used by taxpayer for business purpose.

On the other hand, it can be said that sum used by the business for personal use would be

covered under the head of taxable income while computing tax to be paid by the taxpayer.

In the present case, the employer paid a sum of $500 to employee. $120 was used for

business travelling purpose only. As the rest amount was being used by the employee for the

personal use as per their agreement, in this regard, $120 would be covered under exempted

incomes of employees. On the other hand amount used for personal purpose i.e $380 ( $500 -

6

particulars amount

purchasing price 5.65

selling price 3.66

net capital gain -1.99

As per the CGT consequences outlines, Chris is suffering a capital loss from the trading

of shares.

QUESTION 4

A) Prize received worth $2,000 for the best TV advertisement of the year.

As per the rules of Australian taxation, no tax is needed to be paid for gifts and

inheritance received by the tax payer (Clibborn, 2018). Any gift received from any relative,

employer or any other person is fully exempted from tax in the Australian taxation law.

In the present case scenario, a prize is being received by the tax payer for best TV

advertisement of the year. It can be taken in the category of gifts. In this regard, it would be

included in the exempted income while calculating total amount of tax to be paid by taxpayer.

Hence, no tax would be assessable on the amount received for the prize.

B) Amount received for business travel

As per the taxation rules relating to the business travel expenses, if any employee gets

sum for the amount for travelling somewhere for business purpose, the amount would be

exempted from tax. Further, as per the policy of exemption rules of Australian taxation policies,

the sum provided by the employer for travelling expenses would be taxable to the extent of sum

used by taxpayer for business purpose.

On the other hand, it can be said that sum used by the business for personal use would be

covered under the head of taxable income while computing tax to be paid by the taxpayer.

In the present case, the employer paid a sum of $500 to employee. $120 was used for

business travelling purpose only. As the rest amount was being used by the employee for the

personal use as per their agreement, in this regard, $120 would be covered under exempted

incomes of employees. On the other hand amount used for personal purpose i.e $380 ( $500 -

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

$120 ) would be considered under taxable incomes while calculating total tax liability of the

employee

C) Phone received from client

The Australian taxation system has included all types of gifts and grants received within

the previous year would be exempted from tax (Berns, 2018). These gifts and grants can be

received by the taxpayer from any individual either employer, any supplier, customers, etc.

in the present case, client has provided iPhone worth $1000. it would be included in the

gifts and grants category and hence would be exempted from tax.

D) Damage received for personal injury

As per the clauses of ATO in context to the damages or claims received by a person for

personal injury, would be covered under tax free incomes. In the present case, the taxpayer has

been awarded for the personal injury by an individual for car accident. Therefore, the amount

would be covered under tax free incomes of taxpayer.

E) Income from shares and securities

According to the rules of federal legislations of Australia, of if any trader of shares and

securities gains, any trader gains income due to change in the market condition, the amount

would be taxable to taxpayer at the time of trading the security (Mangioni, V., 2015).

In the given case, taxpayer has gained $2.5 by retaining the shares due to change in the

market condition. This gain would be included in the capital gain at the time of calculating tax

from the trading of security.

7

employee

C) Phone received from client

The Australian taxation system has included all types of gifts and grants received within

the previous year would be exempted from tax (Berns, 2018). These gifts and grants can be

received by the taxpayer from any individual either employer, any supplier, customers, etc.

in the present case, client has provided iPhone worth $1000. it would be included in the

gifts and grants category and hence would be exempted from tax.

D) Damage received for personal injury

As per the clauses of ATO in context to the damages or claims received by a person for

personal injury, would be covered under tax free incomes. In the present case, the taxpayer has

been awarded for the personal injury by an individual for car accident. Therefore, the amount

would be covered under tax free incomes of taxpayer.

E) Income from shares and securities

According to the rules of federal legislations of Australia, of if any trader of shares and

securities gains, any trader gains income due to change in the market condition, the amount

would be taxable to taxpayer at the time of trading the security (Mangioni, V., 2015).

In the given case, taxpayer has gained $2.5 by retaining the shares due to change in the

market condition. This gain would be included in the capital gain at the time of calculating tax

from the trading of security.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 5

Nisu case study

Income tax in Australia is being imposed by the federal government on the taxable income of

individual and corporations. Income tax is levied on progressive rates and the tax is not levy on

income of partnership and trust but it taxed on its distribution to the partners or beneficiaries.

Income tax is the most important source of the revenue for the government within the Australian

Taxation System. Income tax calculated in two statutes they are Income Tax Assessment Act

1936 and Income Tax Assessment 1997 (Berns, 2018). Taxable income is basically the

difference between the assessable income and allowable deductions. Three main type of

assessable income for individual taxpayers are personal earnings, business income and capital

gains. As like many other countries income tax is charged on the wages and salaries given in the

Australia often results in refund payables to taxpayers. An employee also must quote to the

employers for their tax file numbers so the employer can withhold the tax from the pay of the

employer. While this is not covered in offence to fail to provide an employer, a bank or financial

institution with a TFN that is tax file number and in the absence of this number, payers are

required to withhold tax at the rate of 47% stating as first dollar. Similarly, banks are also hold

the highest marginal rate of income tax. Income tax is imposed by the federal government on the

taxable income of the individual and corporation. The Low Income Tax Offset (LITO) is a tax

rebate for Australian-resident individuals on lower incomes. For 2015-16, in addition to the tax-

free threshold of $18,200, the LITO is $445 until the individual's taxable income reaches

$37,000. The LITO is then reduced by 1.5c for every dollar of taxable income above $37,000,

and cuts out when taxable income reaches $66,667.

Case study

The present case study of the report is based on a Nepali student who prefer to study in Australia.

The student is also doing job over there (Graetz and Warren, 2016). Nisu arrives in Australia on

30th December 2018 from Nepal for the enrolment in the Masters of Accounting program at

CQU Sydney campus. He comes Australia with the intention of studying for three years in

Australia. He also gets the part-time job in the bookshop with one of his roommates. He lives in

rental house with the sharing of four students and it not far from the university and he also makes

lots of his friends, joins local soccer team and is well in studies and job. However, on 30th of

8

Nisu case study

Income tax in Australia is being imposed by the federal government on the taxable income of

individual and corporations. Income tax is levied on progressive rates and the tax is not levy on

income of partnership and trust but it taxed on its distribution to the partners or beneficiaries.

Income tax is the most important source of the revenue for the government within the Australian

Taxation System. Income tax calculated in two statutes they are Income Tax Assessment Act

1936 and Income Tax Assessment 1997 (Berns, 2018). Taxable income is basically the

difference between the assessable income and allowable deductions. Three main type of

assessable income for individual taxpayers are personal earnings, business income and capital

gains. As like many other countries income tax is charged on the wages and salaries given in the

Australia often results in refund payables to taxpayers. An employee also must quote to the

employers for their tax file numbers so the employer can withhold the tax from the pay of the

employer. While this is not covered in offence to fail to provide an employer, a bank or financial

institution with a TFN that is tax file number and in the absence of this number, payers are

required to withhold tax at the rate of 47% stating as first dollar. Similarly, banks are also hold

the highest marginal rate of income tax. Income tax is imposed by the federal government on the

taxable income of the individual and corporation. The Low Income Tax Offset (LITO) is a tax

rebate for Australian-resident individuals on lower incomes. For 2015-16, in addition to the tax-

free threshold of $18,200, the LITO is $445 until the individual's taxable income reaches

$37,000. The LITO is then reduced by 1.5c for every dollar of taxable income above $37,000,

and cuts out when taxable income reaches $66,667.

Case study

The present case study of the report is based on a Nepali student who prefer to study in Australia.

The student is also doing job over there (Graetz and Warren, 2016). Nisu arrives in Australia on

30th December 2018 from Nepal for the enrolment in the Masters of Accounting program at

CQU Sydney campus. He comes Australia with the intention of studying for three years in

Australia. He also gets the part-time job in the bookshop with one of his roommates. He lives in

rental house with the sharing of four students and it not far from the university and he also makes

lots of his friends, joins local soccer team and is well in studies and job. However, on 30th of

8

June 2019 he has to return to Nepal due to the family commitment and unfortunately withdraw

from the university with no prospect of returning.

Taxation of income is based on the principle of residence. Australia has some specific

rules for determining the tax for residence as well as for the source of income usually for the

place of business or either employment. Non-residents have to pay taxes only for the income

earned in the Australia. Foreigners arriving in Australia and work over there are qualified as

temporary resident in order to get tax reductions. Four test to determine whether an individual is

resident for the income tax purposes are

• If they are making contribution to a commonwealth superannuation fund,

• In Australia for more than half of the year.

• They have domiciled or permanent place of abode in Australia.

• If they dwell permanently or for a considerable time in Australia.

As Nisu resides in Australia only for the six months so he is not being considered as the resident

of Australia. If Nisu resides in Australia for more than 6 months than only he will be considered

as resident of Australia for the income tax purposes for the year 2018-19.

As Nisu is non-resident he only needs to lodge a tax return if he has the income which is taxable

in Australia. From 1st January 2017, person who is not staying in Australia are working in the

country for the short time period are not considered as resident and they are subject to a special

tax regime and they need to file the income tax return as they earn the income from an Australian

source.

Australian financial year runs from 1st July to 30th June and for to determine whether he is

considered as an Australian resident or non-resident is little complicated in the case of Nisu and

is depend on the situation. Yet if he lived in Australia for more than 183 days for the given year

than only he will be considered as a resident of Australia but he only lives for 183 days so he is

considered as non-resident of Australia.

9

from the university with no prospect of returning.

Taxation of income is based on the principle of residence. Australia has some specific

rules for determining the tax for residence as well as for the source of income usually for the

place of business or either employment. Non-residents have to pay taxes only for the income

earned in the Australia. Foreigners arriving in Australia and work over there are qualified as

temporary resident in order to get tax reductions. Four test to determine whether an individual is

resident for the income tax purposes are

• If they are making contribution to a commonwealth superannuation fund,

• In Australia for more than half of the year.

• They have domiciled or permanent place of abode in Australia.

• If they dwell permanently or for a considerable time in Australia.

As Nisu resides in Australia only for the six months so he is not being considered as the resident

of Australia. If Nisu resides in Australia for more than 6 months than only he will be considered

as resident of Australia for the income tax purposes for the year 2018-19.

As Nisu is non-resident he only needs to lodge a tax return if he has the income which is taxable

in Australia. From 1st January 2017, person who is not staying in Australia are working in the

country for the short time period are not considered as resident and they are subject to a special

tax regime and they need to file the income tax return as they earn the income from an Australian

source.

Australian financial year runs from 1st July to 30th June and for to determine whether he is

considered as an Australian resident or non-resident is little complicated in the case of Nisu and

is depend on the situation. Yet if he lived in Australia for more than 183 days for the given year

than only he will be considered as a resident of Australia but he only lives for 183 days so he is

considered as non-resident of Australia.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.