Taxation Law of Australia

VerifiedAdded on 2020/02/18

|14

|3073

|31

Homework Assignment

AI Summary

This document presents solved answers to a series of questions related to Australian taxation law. It covers various scenarios, including reward points from airlines, compensation for damaged assets, gifts, fundraising for a club, sports winnings, reimbursements for construction workers, artist expenses, travel expenses between workplaces, and determining tax residency for a foreign student. The solutions analyze each scenario based on relevant tax rulings and case law, explaining whether certain income or expenses are taxable or deductible. The detailed analysis includes references to specific tax rulings (e.g., TR 1999/6, TR 1999/17, TR 95/22) and relevant case law, providing a comprehensive understanding of the application of Australian tax law to diverse situations. The final question involves calculating the tax liability of a foreign student working part-time in Australia while studying, considering the deductibility of education expenses and work-related expenses.

Running head: TAXATION LAW OF AUSTRALIA

Taxation law of Australia

University Name

Student Name

Authors’ Note

Taxation law of Australia

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

TAXATION LAW OF AUSTRALIA

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question (i):..............................................................................................................2

Answer to Question (ii):.............................................................................................................3

Answer to Question (iv):............................................................................................................4

Answer to Question (v):.............................................................................................................4

Answer to Question (vii):...........................................................................................................5

Answer to Question (viii):..........................................................................................................6

Answer to Question (ix):............................................................................................................7

Answer to Question (x):.............................................................................................................7

Answer to Question 2:................................................................................................................7

References................................................................................................................................11

TAXATION LAW OF AUSTRALIA

Table of Contents

Answer to Question 1:................................................................................................................2

Answer to Question (i):..............................................................................................................2

Answer to Question (ii):.............................................................................................................3

Answer to Question (iv):............................................................................................................4

Answer to Question (v):.............................................................................................................4

Answer to Question (vii):...........................................................................................................5

Answer to Question (viii):..........................................................................................................6

Answer to Question (ix):............................................................................................................7

Answer to Question (x):.............................................................................................................7

Answer to Question 2:................................................................................................................7

References................................................................................................................................11

3

TAXATION LAW OF AUSTRALIA

Answer to Question 1:

Answer to Question (i):

The reliable clientele of airline companies is properly rewarded with specific Flight Point as

well as Reward by aviation companies that is essentially under the stipulations mentioned

rulings specified in TR 1999/6 (Lam & Whitney, 2016). The directives of TR 1999/6

mention that reward points or incentives that are accepted by different clientele from

organizations functioning in the airline segment are normally not taken into consideration

under taxation as a specific type of earning (Barkoczy, 2016). Particularly, this regulation

establishes the tax implications of different flight rewards that are accepted from specific

customer loyalty programs. Again, rewards barring the flight rewards are essentially not

taken into consideration in this specific ruling. In essence, for this specific ruling, a specific

flight reward has different characteristics that are mentioned as below:

- The reward necessarily comprises of a free flight, a flight upgrading or else free hotel

space or hiring of car that might be attached to such kinds of flights or else paid

flights (Braithwaite, 2017).

- Flight reward can be considered by a specific member or a particular member of

immediate family (Wu, 2015).

- Flight reward is essentially not transferrable against cash

- Flight reward is also not exchangeable for cash

Nonetheless, fringe benefits also might probably be implemented on particular points as well

as incentive in case of occurrence of below mentioned situations:

TAXATION LAW OF AUSTRALIA

Answer to Question 1:

Answer to Question (i):

The reliable clientele of airline companies is properly rewarded with specific Flight Point as

well as Reward by aviation companies that is essentially under the stipulations mentioned

rulings specified in TR 1999/6 (Lam & Whitney, 2016). The directives of TR 1999/6

mention that reward points or incentives that are accepted by different clientele from

organizations functioning in the airline segment are normally not taken into consideration

under taxation as a specific type of earning (Barkoczy, 2016). Particularly, this regulation

establishes the tax implications of different flight rewards that are accepted from specific

customer loyalty programs. Again, rewards barring the flight rewards are essentially not

taken into consideration in this specific ruling. In essence, for this specific ruling, a specific

flight reward has different characteristics that are mentioned as below:

- The reward necessarily comprises of a free flight, a flight upgrading or else free hotel

space or hiring of car that might be attached to such kinds of flights or else paid

flights (Braithwaite, 2017).

- Flight reward can be considered by a specific member or a particular member of

immediate family (Wu, 2015).

- Flight reward is essentially not transferrable against cash

- Flight reward is also not exchangeable for cash

Nonetheless, fringe benefits also might probably be implemented on particular points as well

as incentive in case of occurrence of below mentioned situations:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

TAXATION LAW OF AUSTRALIA

- There remains a particular association between both the employer and workers. In

addition to this, the points or else incentives received from the flight are in fact

received by workers bearing in mind different employment proviso (Wu, 2015).

- Flight points or else rewards are delivered to the workforce based on a specific

business deal

The periodic flier compensation accepted by the workers of Web jet for carrying out work

related travel need to be taxed neither as Fringe Benefit nor as taxable income.

Answer to Question (ii):

Individuals from among the consumers receive a payment for damage of the capital asset

specifically during offering service to customer (Davis et al., 2015). However, in this specific

case, the total amount accepted as recompense for diverse harms caused cannot be analysed

under policies of taxation (Braithwaite, 2017). Nevertheless, this can be said to be taxable

under the receiver. The important factors that need to be considered in this regard are as

presented below:

- The resources or in other words the assets can be considered as capital and can be

vigorously utilized in the business functions of the recipient (Miller & Oats, 2016).

- The assets or in other words the resources of the firm have the need to be depreciable

asset. In this case, the estimated depreciation can be assessed for the specific assets

presented in the documentation (Pearce & Pinto, 2015).

- The payment received can be utilized for refurbishing parts of firm’s assets that get

damaged (Pearson, 2017).

A specific amount of funds is received for the damage caused by Crane Hire from the

customers. Essentially, this cannot be taken into account under definite cases of taxation and

TAXATION LAW OF AUSTRALIA

- There remains a particular association between both the employer and workers. In

addition to this, the points or else incentives received from the flight are in fact

received by workers bearing in mind different employment proviso (Wu, 2015).

- Flight points or else rewards are delivered to the workforce based on a specific

business deal

The periodic flier compensation accepted by the workers of Web jet for carrying out work

related travel need to be taxed neither as Fringe Benefit nor as taxable income.

Answer to Question (ii):

Individuals from among the consumers receive a payment for damage of the capital asset

specifically during offering service to customer (Davis et al., 2015). However, in this specific

case, the total amount accepted as recompense for diverse harms caused cannot be analysed

under policies of taxation (Braithwaite, 2017). Nevertheless, this can be said to be taxable

under the receiver. The important factors that need to be considered in this regard are as

presented below:

- The resources or in other words the assets can be considered as capital and can be

vigorously utilized in the business functions of the recipient (Miller & Oats, 2016).

- The assets or in other words the resources of the firm have the need to be depreciable

asset. In this case, the estimated depreciation can be assessed for the specific assets

presented in the documentation (Pearce & Pinto, 2015).

- The payment received can be utilized for refurbishing parts of firm’s assets that get

damaged (Pearson, 2017).

A specific amount of funds is received for the damage caused by Crane Hire from the

customers. Essentially, this cannot be taken into account under definite cases of taxation and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

TAXATION LAW OF AUSTRALIA

this is necessarily not a taxable income of the company given the fact that the above

mentioned circumstances are met (Mitchell et al., 2016).

Answer to Question (iii):

As per the Australian Taxation Office, gifts accepted either in cash or else in kind can be

received by a specific individual but this necessarily cannot be regarded as a constituent of

income (Coxon, 2016). Essentially, small gifts can be treated as a specific class of gift that is

eradicated during period of calculation of income tax of specific individual. On the other

hand, in a specific case where huge amount of gifts are received that again can be converted

into money, the specific amount can be considered for the procedure of evaluation by

receiver (Mitchell et al., 2016).

However, in this specific case, alcohol supplier has offered package of holiday in a foreign

country for free and this is inevitably received by the night club executive. Nevertheless, this

can be regarded as income tax enumeration procedure of executive of the particular night

club (Pearson, 2017).

Answer to Question (iv):

The total amount of funds obtained by the Canoe Club for buying additional canoes was

necessarily discovered to be extra funds collected (Miller & Oats, 2016). Nevertheless, this

was essentially returned to different affiliates of Canoe Club. Again, the supplementary fund

that was collected cannot be considered during the calculation of income tax. By itself, this

cannot be regarded while registering earnings. Fundamentally, this is due to the fact that this

fund cannot be necessarily presented as earning in the alternative supplementary fund that is

given by diverse members (Barkoczy, 2016).

TAXATION LAW OF AUSTRALIA

this is necessarily not a taxable income of the company given the fact that the above

mentioned circumstances are met (Mitchell et al., 2016).

Answer to Question (iii):

As per the Australian Taxation Office, gifts accepted either in cash or else in kind can be

received by a specific individual but this necessarily cannot be regarded as a constituent of

income (Coxon, 2016). Essentially, small gifts can be treated as a specific class of gift that is

eradicated during period of calculation of income tax of specific individual. On the other

hand, in a specific case where huge amount of gifts are received that again can be converted

into money, the specific amount can be considered for the procedure of evaluation by

receiver (Mitchell et al., 2016).

However, in this specific case, alcohol supplier has offered package of holiday in a foreign

country for free and this is inevitably received by the night club executive. Nevertheless, this

can be regarded as income tax enumeration procedure of executive of the particular night

club (Pearson, 2017).

Answer to Question (iv):

The total amount of funds obtained by the Canoe Club for buying additional canoes was

necessarily discovered to be extra funds collected (Miller & Oats, 2016). Nevertheless, this

was essentially returned to different affiliates of Canoe Club. Again, the supplementary fund

that was collected cannot be considered during the calculation of income tax. By itself, this

cannot be regarded while registering earnings. Fundamentally, this is due to the fact that this

fund cannot be necessarily presented as earning in the alternative supplementary fund that is

given by diverse members (Barkoczy, 2016).

6

TAXATION LAW OF AUSTRALIA

Answer to Question (v):

Profits or gains that are acquired by sports person can be considered under the Taxation

stipulations mentioned under TR 1999/17 (Lam & Whitney, 2016). Nonetheless, as per the

stipulations stated under this directive, gains of any type or a specific sum of money received

by a particular sport person can be regarded as an earning that is necessarily taxable. In

addition to this, cumulative receipts also become a particular fraction of the earnings that is

put through taxation (Pearce & Pinto, 2015). Nevertheless, in the current state of affairs, the

overall amount that is received by the football player of Australia from the television

marketing corporation can be regarded as an earning that is taxable as per the general concept

(Pearson, 2017).

Answer to Question (vi):

Basically, reimbursement along with the allowance for different construction workers can be

stated under the guidelines declared under TR 95/22 (Davis et al., 2015). In essence, as per

the rulings stated under the TR 95/22, workers operating for diverse construction together

with building business are inevitably comprised of different facets as mentioned below:

- Workforce employed for the purpose of development of building.

- Project manager is occupied for construction together with development of particular

building and many other associated things (Miller & Oats, 2016).

- Beginner, carpenter along with apprentice

- Particular places that include construction sites in which different supervisors carry

out their tasks (Mitchell et al., 2016).

In essence, expenditure that is essentially incurred with regard to aptitude for

development of building is clearly explained as the compensation of the labourers

operating in the segment of construction as well as building development (Pearson, 2017).

TAXATION LAW OF AUSTRALIA

Answer to Question (v):

Profits or gains that are acquired by sports person can be considered under the Taxation

stipulations mentioned under TR 1999/17 (Lam & Whitney, 2016). Nonetheless, as per the

stipulations stated under this directive, gains of any type or a specific sum of money received

by a particular sport person can be regarded as an earning that is necessarily taxable. In

addition to this, cumulative receipts also become a particular fraction of the earnings that is

put through taxation (Pearce & Pinto, 2015). Nevertheless, in the current state of affairs, the

overall amount that is received by the football player of Australia from the television

marketing corporation can be regarded as an earning that is taxable as per the general concept

(Pearson, 2017).

Answer to Question (vi):

Basically, reimbursement along with the allowance for different construction workers can be

stated under the guidelines declared under TR 95/22 (Davis et al., 2015). In essence, as per

the rulings stated under the TR 95/22, workers operating for diverse construction together

with building business are inevitably comprised of different facets as mentioned below:

- Workforce employed for the purpose of development of building.

- Project manager is occupied for construction together with development of particular

building and many other associated things (Miller & Oats, 2016).

- Beginner, carpenter along with apprentice

- Particular places that include construction sites in which different supervisors carry

out their tasks (Mitchell et al., 2016).

In essence, expenditure that is essentially incurred with regard to aptitude for

development of building is clearly explained as the compensation of the labourers

operating in the segment of construction as well as building development (Pearson, 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

TAXATION LAW OF AUSTRALIA

Answer to Question (vii):

Particularly, during the period of tax calculation, specific disbursement for short time period

considered from the perspective of an artiste necessarily can be authorized with the following

deductions:-

- Education of unit along with software (Bauer, 2016).

- Course fee for a specific term that is inevitably for short term period for subject such

as art (Braithwaite, 2017).

- Proposed meals for a particular amount of expenditure

- Travelling cost that is driven for the particular course

Nevertheless, expenditure mentioned above can be regarded for cases of deductions. This can

also be permitted only if the expenditures are connected to administration of arts course.

However, this can be taken into account for a very short period of time. Furthermore,

disbursements that occur but necessarily do not correlate proportionately to management of

art cannot be approved for tax deduction (Dowling, 2014). Thus, disbursements in the current

condition can be considered for deductions after taking into account art management course

for a short period. In this case, expenditure essentially lies within the specific range.

Answer to Question (viii):

As per the taxation regulations, disbursement for dresses delivered by the employer is not

regarded under taxation arrangement. As mentioned by the Taxation Office of Australia,

presentation of art by different artists can be regarded as allowable deduction under taxation

regulation (Gallemore & Labro, 2015). According to the directives of taxation and acceptable

grant by specifically the Taxation Office of Australia, performing artists can be considered as

the ones mentioned below:

TAXATION LAW OF AUSTRALIA

Answer to Question (vii):

Particularly, during the period of tax calculation, specific disbursement for short time period

considered from the perspective of an artiste necessarily can be authorized with the following

deductions:-

- Education of unit along with software (Bauer, 2016).

- Course fee for a specific term that is inevitably for short term period for subject such

as art (Braithwaite, 2017).

- Proposed meals for a particular amount of expenditure

- Travelling cost that is driven for the particular course

Nevertheless, expenditure mentioned above can be regarded for cases of deductions. This can

also be permitted only if the expenditures are connected to administration of arts course.

However, this can be taken into account for a very short period of time. Furthermore,

disbursements that occur but necessarily do not correlate proportionately to management of

art cannot be approved for tax deduction (Dowling, 2014). Thus, disbursements in the current

condition can be considered for deductions after taking into account art management course

for a short period. In this case, expenditure essentially lies within the specific range.

Answer to Question (viii):

As per the taxation regulations, disbursement for dresses delivered by the employer is not

regarded under taxation arrangement. As mentioned by the Taxation Office of Australia,

presentation of art by different artists can be regarded as allowable deduction under taxation

regulation (Gallemore & Labro, 2015). According to the directives of taxation and acceptable

grant by specifically the Taxation Office of Australia, performing artists can be considered as

the ones mentioned below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

TAXATION LAW OF AUSTRALIA

-Performing artists indicate towards musicians

-Performing artists can indicate towards an actor (Guenther et al., 2016).

-Performing artists can be a singer

-Performing artists indicate towards different other classification of artists

-Performing artists also indicate towards performers at circus along with dancers (McGuire et

al., 2014).

Fundamentally, in the current situation, disbursements can be associated to dresses and

cosmetics of diverse performing artiste. Again, specific expenditure can be allowed as a

deduction in the process of shaping the overall earnings that are necessarily taxable for

performing artists.

Answer to Question (ix):

Basically, travelling and drifting between home and workplace can be regarded as travel for

specifically travelling purposes. However, there are specific provisions that allow for

deductions and the particular ones that are permitted declare about the travelling expenditure.

Furthermore, there are certain cases where travelling can also be carried out for official

purpose alone and again there can be cases when travelling can be carried out partially for

official purpose and partially for private purposes (Dowling, 2014). Essentially, in the current

state affairs, it might be hereby stated that travelling can be undertaken only for purposes of

work. In addition to this, disbursements carried out can be declared for deductions of tax and

determination of tax.

TAXATION LAW OF AUSTRALIA

-Performing artists indicate towards musicians

-Performing artists can indicate towards an actor (Guenther et al., 2016).

-Performing artists can be a singer

-Performing artists indicate towards different other classification of artists

-Performing artists also indicate towards performers at circus along with dancers (McGuire et

al., 2014).

Fundamentally, in the current situation, disbursements can be associated to dresses and

cosmetics of diverse performing artiste. Again, specific expenditure can be allowed as a

deduction in the process of shaping the overall earnings that are necessarily taxable for

performing artists.

Answer to Question (ix):

Basically, travelling and drifting between home and workplace can be regarded as travel for

specifically travelling purposes. However, there are specific provisions that allow for

deductions and the particular ones that are permitted declare about the travelling expenditure.

Furthermore, there are certain cases where travelling can also be carried out for official

purpose alone and again there can be cases when travelling can be carried out partially for

official purpose and partially for private purposes (Dowling, 2014). Essentially, in the current

state affairs, it might be hereby stated that travelling can be undertaken only for purposes of

work. In addition to this, disbursements carried out can be declared for deductions of tax and

determination of tax.

9

TAXATION LAW OF AUSTRALIA

Answer to Question (x):

Fundamentally, disbursements can be associated to travelling between places of yet another

owner/employer and the particular employer. Nevertheless, in the current conditions, costs

borne for travelling between two different employers can be considered as allowable

deduction (Bauer, 2016). Over and above this, this is primarily owing to the fact that claims

for deductions cannot be asserted for travelling between diverse employers.

Answer to Question 2:

For the purpose of verifying the overall tax liability of a particular individual, it is

indispensable to settle on whether particular individual is a resident otherwise a foreign

resident for taxation (Mitchell et al., 2016). In essence, law proviso states that a specific

overseas student belonging and who has necessarily registered in this nation Australia for

over a period of more than six months can be considered as a resident for taxation reason. In

particular, in the current scenario, it can be hereby witnessed that Manpreet can be regarded

as a resident of Australia for the purpose of taxation as the student is listed for a specific

course for a period of more than six months in any of the Australian University (Barkoczy,

2016). In addition to this, this specific individual also functions in a particular office on a part

time base and accepts a recompense of approximately $54000. However, this specific

individual also had to incur expenditure for diverse educational reasons and this is essentially

not allowed as deduction. Again, expenditure on self-education that is approximately $18000

cannot be allowed as deduction. Above all, the law states that a specific individual can claim

expenditure related to self education. Essentially, this can happen only in case if the specific

study is connected to work otherwise in case if the specific individual has received erudition

of bond that is essentially taxable according to laws. Intrinsically, the course adopted for self

education needs to have desirable advantage and interest with the current employment.

TAXATION LAW OF AUSTRALIA

Answer to Question (x):

Fundamentally, disbursements can be associated to travelling between places of yet another

owner/employer and the particular employer. Nevertheless, in the current conditions, costs

borne for travelling between two different employers can be considered as allowable

deduction (Bauer, 2016). Over and above this, this is primarily owing to the fact that claims

for deductions cannot be asserted for travelling between diverse employers.

Answer to Question 2:

For the purpose of verifying the overall tax liability of a particular individual, it is

indispensable to settle on whether particular individual is a resident otherwise a foreign

resident for taxation (Mitchell et al., 2016). In essence, law proviso states that a specific

overseas student belonging and who has necessarily registered in this nation Australia for

over a period of more than six months can be considered as a resident for taxation reason. In

particular, in the current scenario, it can be hereby witnessed that Manpreet can be regarded

as a resident of Australia for the purpose of taxation as the student is listed for a specific

course for a period of more than six months in any of the Australian University (Barkoczy,

2016). In addition to this, this specific individual also functions in a particular office on a part

time base and accepts a recompense of approximately $54000. However, this specific

individual also had to incur expenditure for diverse educational reasons and this is essentially

not allowed as deduction. Again, expenditure on self-education that is approximately $18000

cannot be allowed as deduction. Above all, the law states that a specific individual can claim

expenditure related to self education. Essentially, this can happen only in case if the specific

study is connected to work otherwise in case if the specific individual has received erudition

of bond that is essentially taxable according to laws. Intrinsically, the course adopted for self

education needs to have desirable advantage and interest with the current employment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

TAXATION LAW OF AUSTRALIA

However, in this specific case, it can be hereby mentioned that the particular course has the

need to assure the following conditions:-

-Augment the required skills that is required by a particular individual in the current

workplace

-This specific course can aid in the overall process of enhancing the entire level of earnings

from the current employment

Therefore, it can be stated that a specific individual do not have the requirement to claim for

diverse expenditure related to self-education. This does not have any kind of relation with the

current employment condition.

According to the regulations mentioned under the section that is 8-1 specifically under the

Income Tax Assessment expresses that a specific expenditure is deductible if there is

passable association between actions generating expenditure and earning. In addition to this,

expenditures/disbursements that are private or in other words domestic is not acceptable as

deduction. Moreover, a specific case reflected by the case Ronpibon Tin NL v. FC

mentioned under T (1949) supports specific stance. However, this essentially asserts that a

specific outgoing can only be allowed as tax deduction only in case where outgoing leads to

generation of taxable income. Again, there also remains expenditure that is incurred for self-

education purpose and hereby cannot be allowed for deduction for tax.

Fundamentally, there are disbursements that are essentially maintained by Manpreet on

specifically computers along with printers. In addition to this, there disbursements for mobile

phones that are subsequently utilized for work related matters. Furthermore, expenditures are

generally deductible when there remains nexus between expenditure and income generating

capability. Moreover, expenditure can also be regarded as incidental otherwise relevant for

TAXATION LAW OF AUSTRALIA

However, in this specific case, it can be hereby mentioned that the particular course has the

need to assure the following conditions:-

-Augment the required skills that is required by a particular individual in the current

workplace

-This specific course can aid in the overall process of enhancing the entire level of earnings

from the current employment

Therefore, it can be stated that a specific individual do not have the requirement to claim for

diverse expenditure related to self-education. This does not have any kind of relation with the

current employment condition.

According to the regulations mentioned under the section that is 8-1 specifically under the

Income Tax Assessment expresses that a specific expenditure is deductible if there is

passable association between actions generating expenditure and earning. In addition to this,

expenditures/disbursements that are private or in other words domestic is not acceptable as

deduction. Moreover, a specific case reflected by the case Ronpibon Tin NL v. FC

mentioned under T (1949) supports specific stance. However, this essentially asserts that a

specific outgoing can only be allowed as tax deduction only in case where outgoing leads to

generation of taxable income. Again, there also remains expenditure that is incurred for self-

education purpose and hereby cannot be allowed for deduction for tax.

Fundamentally, there are disbursements that are essentially maintained by Manpreet on

specifically computers along with printers. In addition to this, there disbursements for mobile

phones that are subsequently utilized for work related matters. Furthermore, expenditures are

generally deductible when there remains nexus between expenditure and income generating

capability. Moreover, expenditure can also be regarded as incidental otherwise relevant for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

TAXATION LAW OF AUSTRALIA

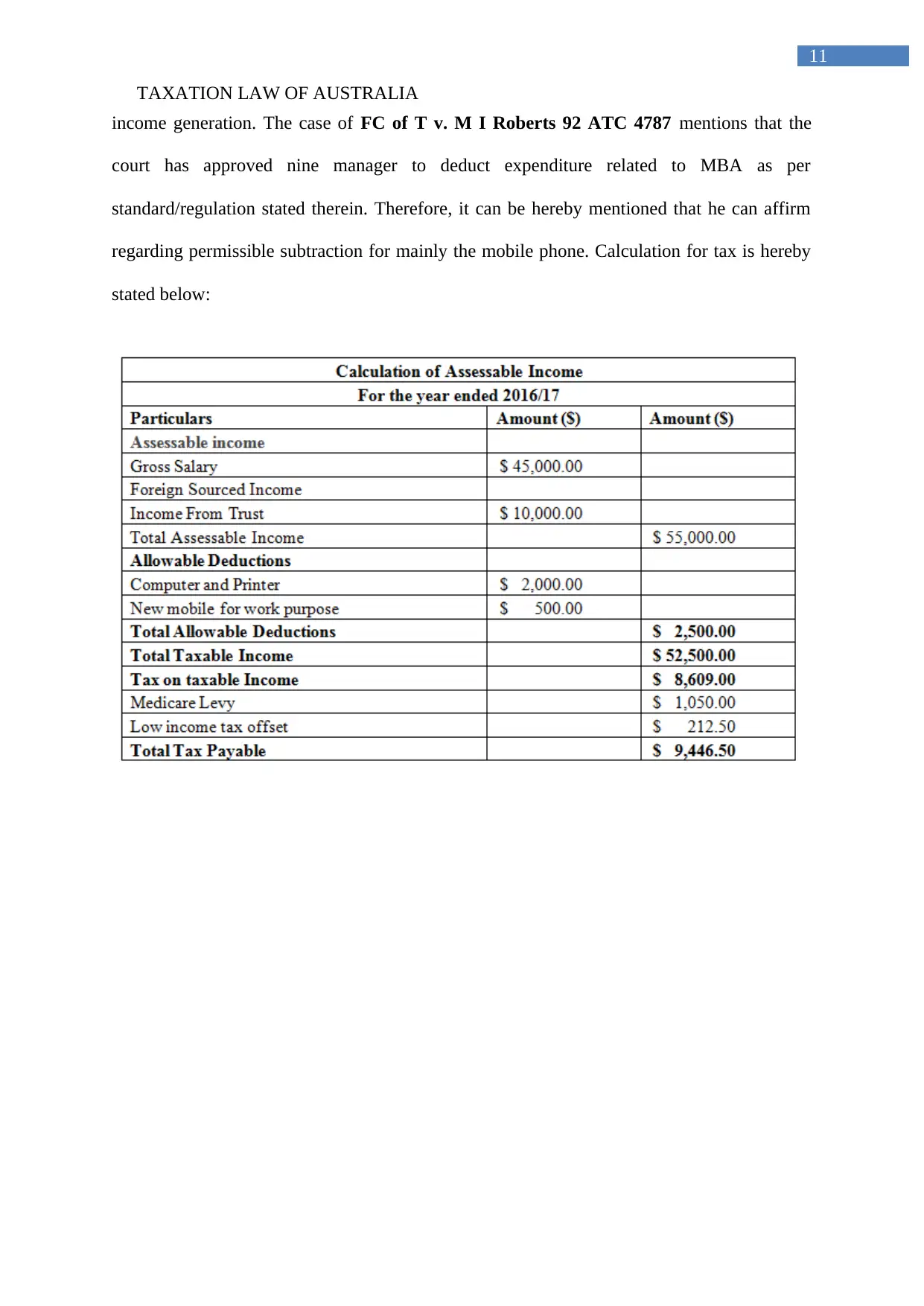

income generation. The case of FC of T v. M I Roberts 92 ATC 4787 mentions that the

court has approved nine manager to deduct expenditure related to MBA as per

standard/regulation stated therein. Therefore, it can be hereby mentioned that he can affirm

regarding permissible subtraction for mainly the mobile phone. Calculation for tax is hereby

stated below:

TAXATION LAW OF AUSTRALIA

income generation. The case of FC of T v. M I Roberts 92 ATC 4787 mentions that the

court has approved nine manager to deduct expenditure related to MBA as per

standard/regulation stated therein. Therefore, it can be hereby mentioned that he can affirm

regarding permissible subtraction for mainly the mobile phone. Calculation for tax is hereby

stated below:

12

TAXATION LAW OF AUSTRALIA

References

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bauer, A. M. (2016). Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Coxon, H. (2016). Australian Official Publications: Guides to Official Publications. Elsevier.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Guenther, D. A., Matsunaga, S. R., & Williams, B. M. (2016). Is tax avoidance related to

firm risk?. The Accounting Review, 92(1), 115-136.

Lam, D., & Whitney, A. (2016). Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), 84.

McGuire, S. T., Wang, D., & Wilson, R. J. (2014). Dual class ownership and tax

avoidance. The Accounting Review, 89(4), 1487-1516.

TAXATION LAW OF AUSTRALIA

References

Barkoczy, S. (2016). Foundations of Taxation Law 2016. OUP Catalogue.

Bauer, A. M. (2016). Tax avoidance and the implications of weak internal

controls. Contemporary Accounting Research, 33(2), 449-486.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Braithwaite, V. (Ed.). (2017). Taxing democracy: Understanding tax avoidance and evasion.

Routledge.

Coxon, H. (2016). Australian Official Publications: Guides to Official Publications. Elsevier.

Davis, A. K., Guenther, D. A., Krull, L. K., & Williams, B. M. (2015). Do socially

responsible firms pay more taxes?. The Accounting Review, 91(1), 47-68.

Dowling, G. R. (2014). The curious case of corporate tax avoidance: Is it socially

irresponsible?. Journal of Business Ethics, 124(1), 173-184.

Gallemore, J., & Labro, E. (2015). The importance of the internal information environment

for tax avoidance. Journal of Accounting and Economics, 60(1), 149-167.

Guenther, D. A., Matsunaga, S. R., & Williams, B. M. (2016). Is tax avoidance related to

firm risk?. The Accounting Review, 92(1), 115-136.

Lam, D., & Whitney, A. (2016). Taxation and property: Practical aspects of the new foreign

resident CGT witholding tax. LSJ: Law Society of NSW Journal, (21), 84.

McGuire, S. T., Wang, D., & Wilson, R. J. (2014). Dual class ownership and tax

avoidance. The Accounting Review, 89(4), 1487-1516.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.