Taxation Law of Australia Assignment: LAWS20060, Term 1 2019

VerifiedAdded on 2023/04/23

|11

|3758

|294

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Taxation Law assignment, addressing several key areas of Australian taxation. The assignment includes detailed explanations and applications of tax principles. Question 1 covers topics such as tax rulings, available tax offsets, tax rates, CGT exemptions, and the determination of taxable income, supported by relevant case law and examples. Question 2 focuses on general deductions, exploring permissible and non-permissible deductions, including those related to business expenses, private expenditure, child care, theft, and campaign expenses. Question 3 examines CGT events, specifically F1 and D2, and the application of the main residence clause, along with CGT calculations for shares. Question 4 deals with assessable income, differentiating between reimbursement and allowance and addressing fringe benefits. The solution thoroughly analyzes each scenario, referencing relevant legislation, tax rulings, and case law to support the arguments and conclusions.

TAXATION LAW OF AUSTRALIA

STUDENT ID:

[Pick the date]

STUDENT ID:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 1

(a) Tax Ruling TR 2018/4 covers the topic related to the effective life of various depreciating

assets with respect to the income tax consequences1.

(b) Available tax offsets have been discussed in the division 17 of Income Tax Assessment Act

1997.

(c) The highest tax rate applied on a tax resident in the 2018/19 tax year is 45%.

(d) Vehicles like cars are one of the assets which are exempted in the applicability of Capital

Gains Tax in Australia as highlighted in s. 118-5, ITAA 1997.

(e) CGT event B1 s104-15 tax highlights various aspect in relation to use and enjoyment of the

various assets which do not have any title.

(f) The formula contained in s4-10(3) ITAA 1997 describes the procedure to determine the

income tax payable of the taxpayer. The taxable income would be computed based on the

given information which then is multiplied with the applicable tax rate. Further, the net tax

payable would be determined after eliminating the present tax offsets from the income tax

liability.

(g) According to the case facts of FC of T v Day 2008 ATC 20-064 case, the employer claimed

certain charges on his employee who was a customs officer and had used legal services

against the charges in order to defend himself. However, the tax commissioner had

disallowed the respective legal expenses as non-deductible under the highlights of s. 8-1,

ITAA 1997. However, the decision of the tax commissioner had been overruled by the High

Court and it decided that the various legal expensesof the custom officer would be considered

as tax deductible under s.8-1, ITAA 1997. The court had considered two main aspect while

reaching the judgement.

The legal expenses of the custom officer had direct relation with the generation of the

assessable income because he paid various legal expenses so as to defend himself against

the various formal charges of the employer.

The legal expenses of the custom officer were not of private nature and hence, the

expenses would be considered as tax deductible under s.8-1, ITAA 1997.

1ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR%2FTR20184%2FNAT%2FATO

%2F00001

(a) Tax Ruling TR 2018/4 covers the topic related to the effective life of various depreciating

assets with respect to the income tax consequences1.

(b) Available tax offsets have been discussed in the division 17 of Income Tax Assessment Act

1997.

(c) The highest tax rate applied on a tax resident in the 2018/19 tax year is 45%.

(d) Vehicles like cars are one of the assets which are exempted in the applicability of Capital

Gains Tax in Australia as highlighted in s. 118-5, ITAA 1997.

(e) CGT event B1 s104-15 tax highlights various aspect in relation to use and enjoyment of the

various assets which do not have any title.

(f) The formula contained in s4-10(3) ITAA 1997 describes the procedure to determine the

income tax payable of the taxpayer. The taxable income would be computed based on the

given information which then is multiplied with the applicable tax rate. Further, the net tax

payable would be determined after eliminating the present tax offsets from the income tax

liability.

(g) According to the case facts of FC of T v Day 2008 ATC 20-064 case, the employer claimed

certain charges on his employee who was a customs officer and had used legal services

against the charges in order to defend himself. However, the tax commissioner had

disallowed the respective legal expenses as non-deductible under the highlights of s. 8-1,

ITAA 1997. However, the decision of the tax commissioner had been overruled by the High

Court and it decided that the various legal expensesof the custom officer would be considered

as tax deductible under s.8-1, ITAA 1997. The court had considered two main aspect while

reaching the judgement.

The legal expenses of the custom officer had direct relation with the generation of the

assessable income because he paid various legal expenses so as to defend himself against

the various formal charges of the employer.

The legal expenses of the custom officer were not of private nature and hence, the

expenses would be considered as tax deductible under s.8-1, ITAA 1997.

1ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR%2FTR20184%2FNAT%2FATO

%2F00001

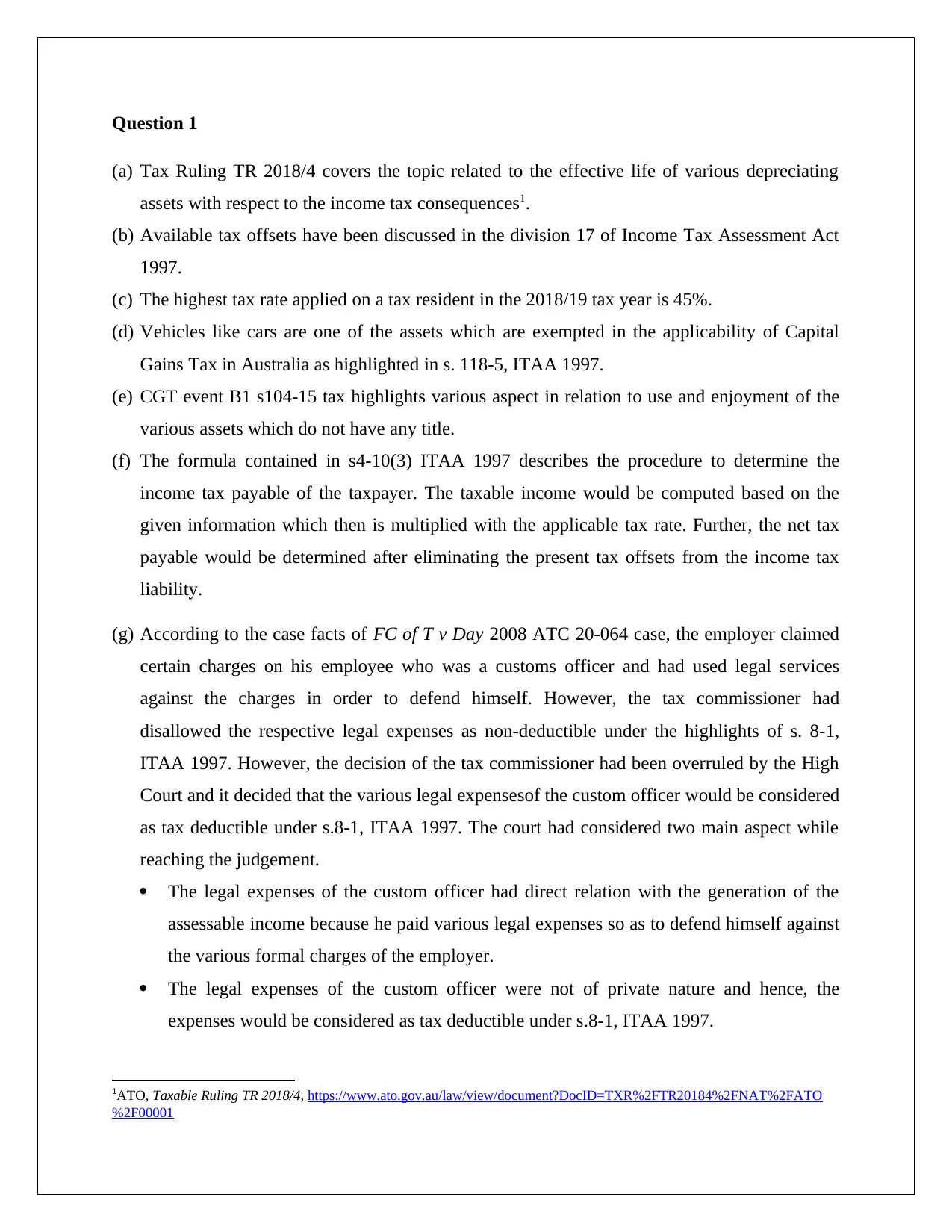

(h) Marginal rate of tax and average rate of tax are significantly different from each other. The

Marginal tax rate is the one which is imposed on the extra taxable income of the taxpayer

whereas average rate results an average tax that would be valid on to the total income of the

taxpayer. This understanding can be represented through a numerical example as shown

below.

Let the yearly taxable income of a taxpayer is $100,000. The applicable marginal tax rate for the

tax year 2018/19 is 37%. The extra income of the taxable would be taxed as per the given

marginal tax rate.

(i) Consumption tax implies a tax that is imposed by the government on the taxpayer on

consumption of some special items. One of the examples is sugar tax which is imposed on

various products that contains significant amount of sugar such as beverages, sweeteners, soft

drinks, bakery productions and so forth. The aim to reduce the consumption of goods that

have significant negative externalities associated with themselves.

Question 2

a) Section 8-1 ITAA 1997 tend to deal with general deductions which are permitted for any loss

or outgoing provided the same is incurred with regards to assessable income generation.

There are few negative limbs (ss. 8-1(2) ITAA 1997) highlighted in this section as per which

deduction is not available for capital expenses, domestic or private expenses and expenses

related to non-assessable income production2. As per the given scenario, the interest that is

paid is related to business related borrowing since it was incurred for payment of wages. As a

result, deduction is permissible for the taxpayer in accordance with s. 8-1 ITAA 1997.

2 Austlii, Income Tax Assessment Act 1997 – Section 8-1 < http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html>

Marginal tax rate is the one which is imposed on the extra taxable income of the taxpayer

whereas average rate results an average tax that would be valid on to the total income of the

taxpayer. This understanding can be represented through a numerical example as shown

below.

Let the yearly taxable income of a taxpayer is $100,000. The applicable marginal tax rate for the

tax year 2018/19 is 37%. The extra income of the taxable would be taxed as per the given

marginal tax rate.

(i) Consumption tax implies a tax that is imposed by the government on the taxpayer on

consumption of some special items. One of the examples is sugar tax which is imposed on

various products that contains significant amount of sugar such as beverages, sweeteners, soft

drinks, bakery productions and so forth. The aim to reduce the consumption of goods that

have significant negative externalities associated with themselves.

Question 2

a) Section 8-1 ITAA 1997 tend to deal with general deductions which are permitted for any loss

or outgoing provided the same is incurred with regards to assessable income generation.

There are few negative limbs (ss. 8-1(2) ITAA 1997) highlighted in this section as per which

deduction is not available for capital expenses, domestic or private expenses and expenses

related to non-assessable income production2. As per the given scenario, the interest that is

paid is related to business related borrowing since it was incurred for payment of wages. As a

result, deduction is permissible for the taxpayer in accordance with s. 8-1 ITAA 1997.

2 Austlii, Income Tax Assessment Act 1997 – Section 8-1 < http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s8.1.html>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

b) A key negative limb identified in context of general deduction (ss. 8-1) is that no deduction

can be availed for private expenditure. Also, it is imperative that the expenses should be

related to assessable income generation3. The given scenario highlights that $ 500 worth

mobile expenses have been incurred by Julie but 40% of this expenditure is private. This

amount would not be deductible while the expenditure related to assessable income

production i.e.500*(60/100) = $ 300 can be deductible.

c) The matter of child care being deductible or not has been dealt in Lodge v. FC of T4 case. The

honorable court indicated that the these expenses were not related to assessable income

generation but are private expenses. A similar stance has been endorsed in the tax ruling TR

95/9 where it is clearly specified that any expenditure related to childcare would be held as

private expenditure even though the same may be necessary for the employee to attend

office5. Therefore, no deduction would be available for Sally in relation to $ 1,200 which is

paid to the babysitter.

.

d) The given issue of whether theft is a business expenditure or not has been dealt with in

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation6 case. It has been

ascertained in this particular case that theft related losses are common in most businesses and

hence would be business related losses. As per the scenario presented, goods stealing has

caused losses to the business which are incurred in the quest to produce assessable income.

As a result, general deduction under s. 8-1 ITAA 1997 would be available in this case7.

e) In relation to deduction of expenses, one of the key negative limbs8 is that the expense should

have a revenue nature. Also, the expense must be incurred with regards to assessable income

production. In the given case, running for elected representative would lead to creation of

assessable income in the form of salary derived. However, the nature of the campaign

3 Ibid. 2

4Lodge v. FC of T (1972) 128 CLR 171

5 ATO, Taxation Ruling TR 95/9, < https://www.ato.gov.au/law/view/document?DocID=TXR/TR959/NAT/ATO/00001>

6Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

7Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press Australia, 2017)

8 Subsection 8-1(2)ITAA 1997

can be availed for private expenditure. Also, it is imperative that the expenses should be

related to assessable income generation3. The given scenario highlights that $ 500 worth

mobile expenses have been incurred by Julie but 40% of this expenditure is private. This

amount would not be deductible while the expenditure related to assessable income

production i.e.500*(60/100) = $ 300 can be deductible.

c) The matter of child care being deductible or not has been dealt in Lodge v. FC of T4 case. The

honorable court indicated that the these expenses were not related to assessable income

generation but are private expenses. A similar stance has been endorsed in the tax ruling TR

95/9 where it is clearly specified that any expenditure related to childcare would be held as

private expenditure even though the same may be necessary for the employee to attend

office5. Therefore, no deduction would be available for Sally in relation to $ 1,200 which is

paid to the babysitter.

.

d) The given issue of whether theft is a business expenditure or not has been dealt with in

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation6 case. It has been

ascertained in this particular case that theft related losses are common in most businesses and

hence would be business related losses. As per the scenario presented, goods stealing has

caused losses to the business which are incurred in the quest to produce assessable income.

As a result, general deduction under s. 8-1 ITAA 1997 would be available in this case7.

e) In relation to deduction of expenses, one of the key negative limbs8 is that the expense should

have a revenue nature. Also, the expense must be incurred with regards to assessable income

production. In the given case, running for elected representative would lead to creation of

assessable income in the form of salary derived. However, the nature of the campaign

3 Ibid. 2

4Lodge v. FC of T (1972) 128 CLR 171

5 ATO, Taxation Ruling TR 95/9, < https://www.ato.gov.au/law/view/document?DocID=TXR/TR959/NAT/ATO/00001>

6Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

7Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press Australia, 2017)

8 Subsection 8-1(2)ITAA 1997

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenditure would not be revenue but rather capital owing to which deduction under s.8-1

iTAA 1997 is not permitted.

Question 3

a) A CGT (Capital Gains Tax) event tends to occur when an existing lease is renewed or a new

lease is granted where payment of premium is involved. This is referred to as F1 CGT

event9. The computation of CGT in this case is governed by the formula highlighted in s.

104-110 ITAA 1997 as per which deduction of incidental costs incurred in executing the

lease needs to be subtracted from the premium amount. The premium amount in the given

case is $ 5,000 and assuming that taxpayer incurs no incidental expenses, net capital gains

would $ 5,000. Further, as highlighted in ss. 115-5 ITAA 199710, the discount method cannot

be applied on any transaction covered under F1 -CGT type.

b) When an option is granted for buying of asset for a particular premium, a D2 CGT event is

triggered. The computation of CGT in this case is governed by the formula highlighted in s.

104- 40 ITAA 1997 as per which deduction of incidental costs incurred in executing the

option needs to be subtracted from the premium amount. The premium amount realized for

option granting in the given case is $ 40,000 and assuming that taxpayer incurs no incidental

expenses, net capital gains would $ 50,000. Further, as highlighted in ss. 115-5 ITAA 1997,

the discount method cannot be applied on any transaction covered under D2 CGT type.

c) The main residence clause indicated in sub division 118-B allows concession on CGT with

regards to sale of main residence. In accordance with ss. 118-145(2) ITAA 1997, it is

possible for the taxpayer to consider treating a given home as the main residence despite

being absent from the place provided the taxpayer do not have any other permanent residence

during that period. This arrangement can be continued for six years and is referred to as six

year rule. As per the relevant case facts, Jamie and Olivia purchased the house and gave iton

rent as they had to travel overseas. This overseas travel continued for 2 years during which

9 ATO, Type of CGT event, < https://www.ato.gov.au/General/Capital-gains-tax/Selling-an-asset-and-other-CGT-events/Types-

of-CGT-events/>

10 Austlii, Section 115-5 ITAA 1997 < http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.5.html>

iTAA 1997 is not permitted.

Question 3

a) A CGT (Capital Gains Tax) event tends to occur when an existing lease is renewed or a new

lease is granted where payment of premium is involved. This is referred to as F1 CGT

event9. The computation of CGT in this case is governed by the formula highlighted in s.

104-110 ITAA 1997 as per which deduction of incidental costs incurred in executing the

lease needs to be subtracted from the premium amount. The premium amount in the given

case is $ 5,000 and assuming that taxpayer incurs no incidental expenses, net capital gains

would $ 5,000. Further, as highlighted in ss. 115-5 ITAA 199710, the discount method cannot

be applied on any transaction covered under F1 -CGT type.

b) When an option is granted for buying of asset for a particular premium, a D2 CGT event is

triggered. The computation of CGT in this case is governed by the formula highlighted in s.

104- 40 ITAA 1997 as per which deduction of incidental costs incurred in executing the

option needs to be subtracted from the premium amount. The premium amount realized for

option granting in the given case is $ 40,000 and assuming that taxpayer incurs no incidental

expenses, net capital gains would $ 50,000. Further, as highlighted in ss. 115-5 ITAA 1997,

the discount method cannot be applied on any transaction covered under D2 CGT type.

c) The main residence clause indicated in sub division 118-B allows concession on CGT with

regards to sale of main residence. In accordance with ss. 118-145(2) ITAA 1997, it is

possible for the taxpayer to consider treating a given home as the main residence despite

being absent from the place provided the taxpayer do not have any other permanent residence

during that period. This arrangement can be continued for six years and is referred to as six

year rule. As per the relevant case facts, Jamie and Olivia purchased the house and gave iton

rent as they had to travel overseas. This overseas travel continued for 2 years during which

9 ATO, Type of CGT event, < https://www.ato.gov.au/General/Capital-gains-tax/Selling-an-asset-and-other-CGT-events/Types-

of-CGT-events/>

10 Austlii, Section 115-5 ITAA 1997 < http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s115.5.html>

time they did not have any other alternative permanent residence either in Australia or

abroad. As a result, despite their physical absence, the house would continue to be

recognized as main residence11 Hence, with regards to house sale any capital gains which

may arise would not be taxable.

Since the house asset was held by the taxpayer for a period longer than 1 year, hence discount

method could have provided relief to the taxpayer had their been some taxable capital gains.

d) Shares are a type of CGT asset owing which their disposal would trigger a A1 CGT event. In

accordance with ss. 104-10 ITAA 199712, the amount of capital gains realized would amount

of asset selling price minus asset cost base.

Total money spent on purchasing BHP Shares = 12000*$0.45 = $5,400

Sale proceeds realized from liquidation of BHP Shares = 12000* $1.56 = $18,720

Capital gains/(losses) related to sale of BHP shares = $18,720 – $5,400 =$13,320

Total money spent on purchasing Wesfarmers Shares = 5000*$5.20 = $26,000

Sale proceeds realized from liquidation of Wesfarmers Shares = 5000* $2.10 = $10,500

Capital gains/(losses) related to sale of Wesfarmers shares =$10,500- $26,000 = -$15,500

Total Capital Gains realized from sale of both shares =-$15,500 + $13,320 = $2,180

In the given case,the discount method would not apply as the shares of both the companies have

been held for less than a year owing to which they are short term assets.

Question 4

11Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

12Austlii, Income Tax Assessment Act 1997 – SECT 104.10, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s104.10.html

abroad. As a result, despite their physical absence, the house would continue to be

recognized as main residence11 Hence, with regards to house sale any capital gains which

may arise would not be taxable.

Since the house asset was held by the taxpayer for a period longer than 1 year, hence discount

method could have provided relief to the taxpayer had their been some taxable capital gains.

d) Shares are a type of CGT asset owing which their disposal would trigger a A1 CGT event. In

accordance with ss. 104-10 ITAA 199712, the amount of capital gains realized would amount

of asset selling price minus asset cost base.

Total money spent on purchasing BHP Shares = 12000*$0.45 = $5,400

Sale proceeds realized from liquidation of BHP Shares = 12000* $1.56 = $18,720

Capital gains/(losses) related to sale of BHP shares = $18,720 – $5,400 =$13,320

Total money spent on purchasing Wesfarmers Shares = 5000*$5.20 = $26,000

Sale proceeds realized from liquidation of Wesfarmers Shares = 5000* $2.10 = $10,500

Capital gains/(losses) related to sale of Wesfarmers shares =$10,500- $26,000 = -$15,500

Total Capital Gains realized from sale of both shares =-$15,500 + $13,320 = $2,180

In the given case,the discount method would not apply as the shares of both the companies have

been held for less than a year owing to which they are short term assets.

Question 4

11Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

12Austlii, Income Tax Assessment Act 1997 – SECT 104.10, http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/

s104.10.html

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a) In accordance with tax ruling TR 1999/17, assessable income would arise based on a prize or

trophy if the receiving of this would be related to the skill or employment of the underlying

taxpayer for deriving income13. An additional requirement is that the prizes must not be just

an isolated case. It should be regular in nature and expected to be received by the taxpayer.

Based on the given facts, it is apparent that best TV advertisement would be related to the

underlying skill of the advertising agency and people involved in making the advertisement.

Further, awards of this kind tend to be periodic in nature and there is expectation on the part

of agencies to receive the same. As a result, the prize proceeds would be labeled as

assessable income for the business14

b) In order to assess if the amount received by the taxpayer would be assessable or not, it is

essential to understand the difference between reimbursement and allowance. In accordance

with tax ruling TR 92/15, allowance refers to an amount which the employee obtains

irrespective of the actual expenditure and the amount of the same on the underlying activity.

With regards to reimbursement, the situation is starkly different as the company only pays

the amount which the employee has incurred in actuality. As a result, no economic benefit is

derived by the employee in case of reimbursement which is not the case in allowance.

Considering the case facts, it is apparent that employee has received allowance of $ 500 with

regards to official trip to Sydney. Any savings from this amount would be economic benefit

for the employee owing to which the allowance would contribute to assessable income15.

c) The electronic devices which the employer provides to employee is a type of fringe benefit

which is covered under Fringe Benefit Tax Assessment Act 1986. As per s. 58X of this act,

these mobile devices are exempt from tax. Further, it is noticeable that the providing of these

devices does not result in any economic benefit as these cannot be sold to generate cash.

Further, these are essentially given for work purposes and have to be returned to the

13 ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

14Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company, 2017)

15 Ibid, 7.

trophy if the receiving of this would be related to the skill or employment of the underlying

taxpayer for deriving income13. An additional requirement is that the prizes must not be just

an isolated case. It should be regular in nature and expected to be received by the taxpayer.

Based on the given facts, it is apparent that best TV advertisement would be related to the

underlying skill of the advertising agency and people involved in making the advertisement.

Further, awards of this kind tend to be periodic in nature and there is expectation on the part

of agencies to receive the same. As a result, the prize proceeds would be labeled as

assessable income for the business14

b) In order to assess if the amount received by the taxpayer would be assessable or not, it is

essential to understand the difference between reimbursement and allowance. In accordance

with tax ruling TR 92/15, allowance refers to an amount which the employee obtains

irrespective of the actual expenditure and the amount of the same on the underlying activity.

With regards to reimbursement, the situation is starkly different as the company only pays

the amount which the employee has incurred in actuality. As a result, no economic benefit is

derived by the employee in case of reimbursement which is not the case in allowance.

Considering the case facts, it is apparent that employee has received allowance of $ 500 with

regards to official trip to Sydney. Any savings from this amount would be economic benefit

for the employee owing to which the allowance would contribute to assessable income15.

c) The electronic devices which the employer provides to employee is a type of fringe benefit

which is covered under Fringe Benefit Tax Assessment Act 1986. As per s. 58X of this act,

these mobile devices are exempt from tax. Further, it is noticeable that the providing of these

devices does not result in any economic benefit as these cannot be sold to generate cash.

Further, these are essentially given for work purposes and have to be returned to the

13 ATO, Taxation Ruling TR 1999/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

14Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company, 2017)

15 Ibid, 7.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

employer at the time of termination. As a result, no assessable income would be realized by

the employee as a result of this transaction.

d) In accordance with TD 93/58, any compensatory payment provided for loss of assessable

income would be considered as having income nature and hence categorized as assessable

income. Also, in situations where parties agree that some portion of the compensation is

provided for loss of income, then this portion of compensation would be treated as assessable

income in line with the verdict in Mc Laurin v. FC of T16 case. It is noteworthy that the

damages derived by the taxpayer in the given case pertains to personal injuries and therefore

are devoid of income nature. As a result, the compensatory payment of $ 10,000 is not

assessable income17.

e) A key component of assessable income tends to be statutory income18. With regards to

statutory income, a key contributor is capital gains which is considered as income of

assessable nature. As per s. 104-5 ITAA 1997, computation of any capital gains or losses is

to be carried on only when a trigger in the form of CGT event takes place19. Shares are a

form of CGT asset and currently the investor has capital gains. However, only when A1 CGT

event is triggered owing to disposal of shares, would the computation of capital gains be

carried out along with computation of CGT liability. Therefore, no assessable income would

be realized in this case till the shares are liquidated.

Question 5

The various aspect in relation to the tax residency of an individual has been described in ss. 6(1),

ITAA 193620 whereas the residency tests for individual taxpayers have been highlighted in the

tax ruling TR 98/1721. It contains four tests that would be used by an individual taxpayer in order

to find their tax residency status on yearly basis.

16Mc Laurin v. FC of T (1961) 104 CLR 381

17 Ibid. 14

18 Section 6-10 ITAA 1997

19Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

20Austlii, Income Tax Assessment Act 1936 – SECT 6, http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

21ATO, Taxation Ruling TR 98/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

the employee as a result of this transaction.

d) In accordance with TD 93/58, any compensatory payment provided for loss of assessable

income would be considered as having income nature and hence categorized as assessable

income. Also, in situations where parties agree that some portion of the compensation is

provided for loss of income, then this portion of compensation would be treated as assessable

income in line with the verdict in Mc Laurin v. FC of T16 case. It is noteworthy that the

damages derived by the taxpayer in the given case pertains to personal injuries and therefore

are devoid of income nature. As a result, the compensatory payment of $ 10,000 is not

assessable income17.

e) A key component of assessable income tends to be statutory income18. With regards to

statutory income, a key contributor is capital gains which is considered as income of

assessable nature. As per s. 104-5 ITAA 1997, computation of any capital gains or losses is

to be carried on only when a trigger in the form of CGT event takes place19. Shares are a

form of CGT asset and currently the investor has capital gains. However, only when A1 CGT

event is triggered owing to disposal of shares, would the computation of capital gains be

carried out along with computation of CGT liability. Therefore, no assessable income would

be realized in this case till the shares are liquidated.

Question 5

The various aspect in relation to the tax residency of an individual has been described in ss. 6(1),

ITAA 193620 whereas the residency tests for individual taxpayers have been highlighted in the

tax ruling TR 98/1721. It contains four tests that would be used by an individual taxpayer in order

to find their tax residency status on yearly basis.

16Mc Laurin v. FC of T (1961) 104 CLR 381

17 Ibid. 14

18 Section 6-10 ITAA 1997

19Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

20Austlii, Income Tax Assessment Act 1936 – SECT 6, http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

21ATO, Taxation Ruling TR 98/17, https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

Residency test (Through Ordinary Concepts): This test is used to test the tax residency status

of the taxpayer who are not Australian domicile holders. This test contains various factors

based on the plethora of actions of the taxpayer, professional, personal bonds and so forth22.

Domicile Test: This test isapplicable on individuals who hold Australian domicile but

residing overseas due to the personal or/and professional obligations.

183 Days Test: This test is applied on individual who are foreign tax residents and are

residing in Australia. The time period of residing in Australian and the intention of the

taxpayer to reside in Australia in near future would be considered in this test.

Commonwealth Superannuation Fund Test: This test is taken into consideration for the

taxpayer who are officers of Australian government and are residing overseas due to the

professional commitments23.

Based on the given case facts, it can be seen that Nisu is the concerned taxpayer whose tax

residency status needs to be determined here. Further, it is apparent from information that Nisu is

resident of Nepal and has resided in Australia for study. Nisu is neither an Australian resident

nor Australian officer and thus, the applicable tests would be 183 day test and residency test

under ordinary concepts.

183-day test

There are two main condition that must be satisfied by the taxpayer in order to pass this 183-day

test. According to this test, the taxpayer must be physically present in Australia for a minimum

time period of 183 days in the given tax year. The duration of stay in Australia does not need to

be continuous which means intermittent stay would also be considered. The next imperative

condition of this test is that the Tax Commissioner must not have any suspicion in relation to the

future intention of the taxpayer to not make permanent residence in Australia. In present case,

taxpayer Nisu has come in Australia for study on December 31, 2018 and the duration between

the arrival date and June 30, 2019 is not equal to or higher than 183 which implies that first main

condition of 183day test is not satisfied and hence, Nisu has not passed 183day test.

Residency Test

22 Ibid, 7.

23 Ibid, 14.

of the taxpayer who are not Australian domicile holders. This test contains various factors

based on the plethora of actions of the taxpayer, professional, personal bonds and so forth22.

Domicile Test: This test isapplicable on individuals who hold Australian domicile but

residing overseas due to the personal or/and professional obligations.

183 Days Test: This test is applied on individual who are foreign tax residents and are

residing in Australia. The time period of residing in Australian and the intention of the

taxpayer to reside in Australia in near future would be considered in this test.

Commonwealth Superannuation Fund Test: This test is taken into consideration for the

taxpayer who are officers of Australian government and are residing overseas due to the

professional commitments23.

Based on the given case facts, it can be seen that Nisu is the concerned taxpayer whose tax

residency status needs to be determined here. Further, it is apparent from information that Nisu is

resident of Nepal and has resided in Australia for study. Nisu is neither an Australian resident

nor Australian officer and thus, the applicable tests would be 183 day test and residency test

under ordinary concepts.

183-day test

There are two main condition that must be satisfied by the taxpayer in order to pass this 183-day

test. According to this test, the taxpayer must be physically present in Australia for a minimum

time period of 183 days in the given tax year. The duration of stay in Australia does not need to

be continuous which means intermittent stay would also be considered. The next imperative

condition of this test is that the Tax Commissioner must not have any suspicion in relation to the

future intention of the taxpayer to not make permanent residence in Australia. In present case,

taxpayer Nisu has come in Australia for study on December 31, 2018 and the duration between

the arrival date and June 30, 2019 is not equal to or higher than 183 which implies that first main

condition of 183day test is not satisfied and hence, Nisu has not passed 183day test.

Residency Test

22 Ibid, 7.

23 Ibid, 14.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

According to TR 98/17, there is no direct meaning of word resides in the Australian statute.

Thereby, the keen factors in relation to the taxpayer would be examined under ordinary concepts

which has been drawn from various relevant legal case laws and judgements.

Intention of taxpayer and purpose of visit: As per the judgement of FC of T v. Pechey24 case,

the purpose behind the visit is an imperative aspect as the taxpayer resided in Australia for

study and for long term (more than six month) are categorised as significant reasons leading

to tax residency of Australia.

Personal and professional bonds: The taxpayer would be termed as tax resident of Australia

when he/she has strong personal or professional relationship in Australia in comparison of

their country of origin as evident from the judgement of the Peel v. The Commissioners of

Inland Revenue25 case.

Presence and location of the taxpayer’s assets: When the taxpayer has intention to make

Australia as permanent residence in future and in the same regards has purchased

fixed/movable assets in Australian, then this aspect would also be considered by tax

commissioner to decide the tax residency status of taxpayer.

Social involvement of taxpayer:When the social involvement of taxpayer is similar like that

in country of origin then this would also be contributed in the aspect of being tax resident of

Australia as per TR 98/1726.

In present case, Nisu has come to Australia for a significant reason i.e. study and also, the

duration of the course completion is of three years. Further, he has social involvement in

Australia which is similar to what he used to do in her country of origin (Nepal). These factors

indicatethat Nisu has pass the main pre-requisite of residency test and therefore, it can be said

that Nisu would be considered as tax resident of Australia for the income tax year 2018/19.

Bibliography

ATO, Income Tax Assessment Act 1997 – SECT 118.5,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s118.5.html

24FC of T v. Pechey75 ATC 4083

25Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

26

Thereby, the keen factors in relation to the taxpayer would be examined under ordinary concepts

which has been drawn from various relevant legal case laws and judgements.

Intention of taxpayer and purpose of visit: As per the judgement of FC of T v. Pechey24 case,

the purpose behind the visit is an imperative aspect as the taxpayer resided in Australia for

study and for long term (more than six month) are categorised as significant reasons leading

to tax residency of Australia.

Personal and professional bonds: The taxpayer would be termed as tax resident of Australia

when he/she has strong personal or professional relationship in Australia in comparison of

their country of origin as evident from the judgement of the Peel v. The Commissioners of

Inland Revenue25 case.

Presence and location of the taxpayer’s assets: When the taxpayer has intention to make

Australia as permanent residence in future and in the same regards has purchased

fixed/movable assets in Australian, then this aspect would also be considered by tax

commissioner to decide the tax residency status of taxpayer.

Social involvement of taxpayer:When the social involvement of taxpayer is similar like that

in country of origin then this would also be contributed in the aspect of being tax resident of

Australia as per TR 98/1726.

In present case, Nisu has come to Australia for a significant reason i.e. study and also, the

duration of the course completion is of three years. Further, he has social involvement in

Australia which is similar to what he used to do in her country of origin (Nepal). These factors

indicatethat Nisu has pass the main pre-requisite of residency test and therefore, it can be said

that Nisu would be considered as tax resident of Australia for the income tax year 2018/19.

Bibliography

ATO, Income Tax Assessment Act 1997 – SECT 118.5,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s118.5.html

24FC of T v. Pechey75 ATC 4083

25Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

26

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ATO, Taxable Ruling TR 2018/4, https://www.ato.gov.au/law/view/document?DocID=TXR

%2FTR20184%2FNAT%2FATO%2F00001

ATO, Taxation Ruling TR 1999/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

ATO, Taxation Ruling TR 98/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

Austlii, Income Tax Assessment Act 1936 – SECT 6,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press

Australia, 2017)

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

FC of T v. Pechey75 ATC 4083

Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company,

2017)

Lodge v. FC of T (1972) 128 CLR 171

Mc Laurin v. FC of T (1961) 104 CLR 381

Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

%2FTR20184%2FNAT%2FATO%2F00001

ATO, Taxation Ruling TR 1999/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR199917/NAT/ATO/00001

ATO, Taxation Ruling TR 98/17,

https://www.ato.gov.au/law/view/document?Docid=TXR/TR9817/NAT/ATO/00001

Austlii, Income Tax Assessment Act 1936 – SECT 6,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1936240/s6.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.10,

http://classic.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.10.html

Austlii, Income Tax Assessment Act 1997 – SECT 104.5,

http://www5.austlii.edu.au/au/legis/cth/consol_act/itaa1997240/s104.5.html

Barkoczy Stephen, Core Tax Legislation and Study Guide 2017 (Oxford University Press

Australia, 2017)

Charles Moore & Co (WA) Pty Ltd v. Federal Commissioner of Taxation (1956) 95 CLR 344

FC of T v. Pechey75 ATC 4083

Krever Richard, Australian Taxation Law Cases 2017 (THOMSON LAWBOOK Company,

2017)

Lodge v. FC of T (1972) 128 CLR 171

Mc Laurin v. FC of T (1961) 104 CLR 381

Peel v. The Commissioners of Inland Revenue (1927) 13 TC 443

Reuters, Thomson, Australian Tax Legislation (THOMSON REUTERS, 2017)

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.