Taxation Law: Analyzing Permanent Establishment and Residency Rules

VerifiedAdded on 2023/05/31

|13

|3269

|182

Case Study

AI Summary

This case study delves into various aspects of Australian taxation law, beginning with an explanation of 'Permanent Establishment' under the UK-Australia Double Tax Agreement (DTA), addressing how business profits of UK-incorporated enterprises are taxed in Australia and whether contracts made through independent agents constitute a permanent establishment. It further analyzes the residency status of Andrew McSwington, an MLB prospect, considering his time spent in Mexico and America, the source of his income earned while playing baseball, and the tax implications of rental income from a property in America. The study also examines the application of the First Strand of Myer principle, involving commercial transactions and profit-making intentions. Finally, it provides calculations for capital gains, including proceeds from the sale of rental property, shares, and collectibles, while also considering personal use assets and pre-CGT assets. The analysis references relevant sections of the ITAA 1936 and ITAA 1997, as well as pertinent case law, to provide a comprehensive understanding of the tax implications discussed.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to C:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to 1:...........................................................................................................................3

Answer to 2:...........................................................................................................................4

Answer to 3:...........................................................................................................................4

Answer to 4:...........................................................................................................................4

Answer to 3:...............................................................................................................................5

First Strand of Myer:..............................................................................................................5

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Answer to A:..........................................................................................................................8

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

Answer to question 6:.................................................................................................................9

References:...............................................................................................................................11

Table of Contents

Answer to question 1:.................................................................................................................2

Answer to A:..........................................................................................................................2

Answer to B:..........................................................................................................................2

Answer to C:..........................................................................................................................2

Answer to question 2:.................................................................................................................3

Answer to 1:...........................................................................................................................3

Answer to 2:...........................................................................................................................4

Answer to 3:...........................................................................................................................4

Answer to 4:...........................................................................................................................4

Answer to 3:...............................................................................................................................5

First Strand of Myer:..............................................................................................................5

Answer to question 4:.................................................................................................................7

Answer to question 5:.................................................................................................................8

Answer to A:..........................................................................................................................8

Answer to B:..........................................................................................................................9

Answer to C:..........................................................................................................................9

Answer to question 6:.................................................................................................................9

References:...............................................................................................................................11

2TAXATION LAW

Answer to question 1:

Answer to A:

As per the Australian Taxation Office, the word permanent establishment is explained

under in “subsection 6 (1) of the ITAA 1936”. Permanent establishment refers to carrying of

business by an Australian resident entity through the fixed place of business in another nation

(Grange et al., 2014). Permanent establishment means the business operations which is

carried on by the foreign resident entity in Australia through a fixed place of business.

Answer to B:

According to “Australian/UK DTA (Double Taxation Agreement) 1946” profits of

business of contracting nation would attract tax liability in that country only given the

enterprise is performing the business in other contracting state through the permanent

establishment situated in other country (James, 2014). Given the business is conducted in a

country in an enterprising way and the profits of that company may be held for taxation in

another country but till the extent that is attributable to that permanent establishment.

To determine the permanent establishment profits, the enterprise should be allowed to

claim an allowable deduction for expenses which is occurred from permanent establishment.

As per the explanation of “Australia/UK DTA 1946” companies that are established in UK

and performing the business in Australia then the profits should be taxed in the other country

but merely to the amount that is resultant from the permanent establishment.

Answer to C:

As per the “Article 5 (5) of the OECD” the activities of making contracts does not

lead to permanent establishment given the contracts is performed by the independent agent

that are acting on behalf of the business course.

Answer to question 1:

Answer to A:

As per the Australian Taxation Office, the word permanent establishment is explained

under in “subsection 6 (1) of the ITAA 1936”. Permanent establishment refers to carrying of

business by an Australian resident entity through the fixed place of business in another nation

(Grange et al., 2014). Permanent establishment means the business operations which is

carried on by the foreign resident entity in Australia through a fixed place of business.

Answer to B:

According to “Australian/UK DTA (Double Taxation Agreement) 1946” profits of

business of contracting nation would attract tax liability in that country only given the

enterprise is performing the business in other contracting state through the permanent

establishment situated in other country (James, 2014). Given the business is conducted in a

country in an enterprising way and the profits of that company may be held for taxation in

another country but till the extent that is attributable to that permanent establishment.

To determine the permanent establishment profits, the enterprise should be allowed to

claim an allowable deduction for expenses which is occurred from permanent establishment.

As per the explanation of “Australia/UK DTA 1946” companies that are established in UK

and performing the business in Australia then the profits should be taxed in the other country

but merely to the amount that is resultant from the permanent establishment.

Answer to C:

As per the “Article 5 (5) of the OECD” the activities of making contracts does not

lead to permanent establishment given the contracts is performed by the independent agent

that are acting on behalf of the business course.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

Answer to question 2:

Answer to 1:

The definition of resident and resident of Australia is defined in “subsection 6 (1) of

the ITAA 1936”. According to the “subsection 6 (1)” an individual beside company that are

the resident of Australia comprises of person that have their domicile in Australia given the

commissioner is satisfied that the person has their permanent place of abode out of Australia

(Jover-Ledesma, 2014). As per the “subsection 6 (1)” an individual will be considered as the

Australian resident that is residing in Australia, either constantly or intermittently for at least

one-half of the income year, except the commissioner is satisfied that an individual’s place of

residence is out of Australia and he or she do not have any intention of taking up the

residency out of Australia.

Domicile is regarded as the legal concept which is stated in “Domicile Act 1982”.

However, the common rule is that an individual legally acquires the domicile of their origin

by virtue of their country of his or her birth. Citing the case of “Applegate v FCT (1979)” the

court of law upheld that permanent do not mean everlasting or forever and objectivity is

assessed each year (Kenny, 2013). The taxpayer in Applegate had the permanent place of

dwelling outside Australia.

As evident in the present case of Andrew it is understood that he was born in

Australia, Adelaide and travelled to America and Mexico to play leagues for 2 and 15 months

respectively. Andrew then came back to Australia to play for Adelaide. Citing the

explanation of “Domicile Act 1982” Andrew obtained the Domicile of their origin because

he was born in Adelaide, Australia. Furthermore, the stay of Andrew in America and Mexico

was transitory in nature.

Answer to question 2:

Answer to 1:

The definition of resident and resident of Australia is defined in “subsection 6 (1) of

the ITAA 1936”. According to the “subsection 6 (1)” an individual beside company that are

the resident of Australia comprises of person that have their domicile in Australia given the

commissioner is satisfied that the person has their permanent place of abode out of Australia

(Jover-Ledesma, 2014). As per the “subsection 6 (1)” an individual will be considered as the

Australian resident that is residing in Australia, either constantly or intermittently for at least

one-half of the income year, except the commissioner is satisfied that an individual’s place of

residence is out of Australia and he or she do not have any intention of taking up the

residency out of Australia.

Domicile is regarded as the legal concept which is stated in “Domicile Act 1982”.

However, the common rule is that an individual legally acquires the domicile of their origin

by virtue of their country of his or her birth. Citing the case of “Applegate v FCT (1979)” the

court of law upheld that permanent do not mean everlasting or forever and objectivity is

assessed each year (Kenny, 2013). The taxpayer in Applegate had the permanent place of

dwelling outside Australia.

As evident in the present case of Andrew it is understood that he was born in

Australia, Adelaide and travelled to America and Mexico to play leagues for 2 and 15 months

respectively. Andrew then came back to Australia to play for Adelaide. Citing the

explanation of “Domicile Act 1982” Andrew obtained the Domicile of their origin because

he was born in Adelaide, Australia. Furthermore, the stay of Andrew in America and Mexico

was transitory in nature.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

With respect to “subsection 6 (1) of the ITAA 1936” Andrew should be treated as the

Australian resident and also meets the criteria of “Domicile Act 1982” for having domicile in

Australia.

Answer to 2:

Given the taxpayer is the overseas resident, the taxpayer would be held liable for tax

for the ordinary and statutory income which is sourced in Australia. Denoting the judgement

in “FC of T v French (1957)” source means the place where the services are actually carried

out (Krever, 2015). Evidently, the sum of $145,000 that was paid to Andrew related to

baseball skills was sourced in Australia. Andrew will be taxable for the receipt of sign-on

fees that was sourced in Australia.

Answer to 3:

As stated under “taxation ruling of TR 98/17” benefits obtained from the sporting

indulgence would be regarded as taxable income if the receipt of payment is related to the

services provided in regard to employment or services provided. As held in “FC of T v

Reuter (1993)” the taxable income includes the wages, salaries, sign-on fees or retention

payment which is received for continuance of services (Morgan et al., 2013). The payments

would be considered taxable because it constitutes the use of personal ability in a commercial

way for the purpose of obtaining reward. Similarly, the receipt of sign on fees of $145,000 by

Andrew from his sporting involvement is an ordinary income that are taxable under “section

6-5 of the ITAA 1997”. The sum received was for commercial use of skills that was

developed and used for sporting excellence.

Answer to 4:

An individual who is a dweller of Australia would be required to pay tax for income

that is acquired from all corners of world. During Andrew’s stay in America he bought a

With respect to “subsection 6 (1) of the ITAA 1936” Andrew should be treated as the

Australian resident and also meets the criteria of “Domicile Act 1982” for having domicile in

Australia.

Answer to 2:

Given the taxpayer is the overseas resident, the taxpayer would be held liable for tax

for the ordinary and statutory income which is sourced in Australia. Denoting the judgement

in “FC of T v French (1957)” source means the place where the services are actually carried

out (Krever, 2015). Evidently, the sum of $145,000 that was paid to Andrew related to

baseball skills was sourced in Australia. Andrew will be taxable for the receipt of sign-on

fees that was sourced in Australia.

Answer to 3:

As stated under “taxation ruling of TR 98/17” benefits obtained from the sporting

indulgence would be regarded as taxable income if the receipt of payment is related to the

services provided in regard to employment or services provided. As held in “FC of T v

Reuter (1993)” the taxable income includes the wages, salaries, sign-on fees or retention

payment which is received for continuance of services (Morgan et al., 2013). The payments

would be considered taxable because it constitutes the use of personal ability in a commercial

way for the purpose of obtaining reward. Similarly, the receipt of sign on fees of $145,000 by

Andrew from his sporting involvement is an ordinary income that are taxable under “section

6-5 of the ITAA 1997”. The sum received was for commercial use of skills that was

developed and used for sporting excellence.

Answer to 4:

An individual who is a dweller of Australia would be required to pay tax for income

that is acquired from all corners of world. During Andrew’s stay in America he bought a

5TAXATION LAW

house to use it as his base during home and away season. The house was rented out by

Andrew and derived rental income. Citing the law court judgement in “FCT v Adelaide

Fruit and Produce Exchange Co Ltd” the periodic receipt that is obtained from the rental

properties would be held taxable (Sadiq & Coleman, 2013). As a result, the receipt of rental

income derived from the rental property in America will be treated as ordinary income within

the meaning of “section 6-5, ITAA 1997” and hence will attract tax liability.

Answer to 3:

First Strand of Myer:

As per the principle of Myer, extraordinary or isolated transaction that satisfies the

three specific criteria will be treated as ordinary income. The conditions include the

following;

a. There should be business functions or profitable transaction

b. Profit making purpose was prevalent while entering into the transaction

c. The profit was made in consistent with the original intention

A: Profit as a result of business operations:

A business occurs an extraordinary transaction when the activities give rise to revenue

which is not obtained from the ordinary business course. The transaction was entered into by

the business which ultimately results in meeting of requirements (Sadiq et al., 2014).

Furthermore, the criteria of isolated transaction are met when the first criteria of commercial

transaction are met. The requirements are met when the transaction entered is of commercial

in nature. Nevertheless, the condition is less likely to satisfy the criteria if the transaction is in

the type that the wage earner might enter in.

house to use it as his base during home and away season. The house was rented out by

Andrew and derived rental income. Citing the law court judgement in “FCT v Adelaide

Fruit and Produce Exchange Co Ltd” the periodic receipt that is obtained from the rental

properties would be held taxable (Sadiq & Coleman, 2013). As a result, the receipt of rental

income derived from the rental property in America will be treated as ordinary income within

the meaning of “section 6-5, ITAA 1997” and hence will attract tax liability.

Answer to 3:

First Strand of Myer:

As per the principle of Myer, extraordinary or isolated transaction that satisfies the

three specific criteria will be treated as ordinary income. The conditions include the

following;

a. There should be business functions or profitable transaction

b. Profit making purpose was prevalent while entering into the transaction

c. The profit was made in consistent with the original intention

A: Profit as a result of business operations:

A business occurs an extraordinary transaction when the activities give rise to revenue

which is not obtained from the ordinary business course. The transaction was entered into by

the business which ultimately results in meeting of requirements (Sadiq et al., 2014).

Furthermore, the criteria of isolated transaction are met when the first criteria of commercial

transaction are met. The requirements are met when the transaction entered is of commercial

in nature. Nevertheless, the condition is less likely to satisfy the criteria if the transaction is in

the type that the wage earner might enter in.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

B: Profit making intention while forming transaction:

Citing the case of “Cooling v FCT (1990)” the profit making purpose should not be

the sole intent of taxpayers (Woellner, 2013). If the transaction that is entered by taxpayer did

not had any profit making purpose while buying the asset, however the profit making purpose

while selling the asset. As a result, the second requirement of the first strand is not met.

C: Profit made in agreement with the original intention:

To meet the first strand of Myer, the way based on which the profit is obtained in

consistent with the original intention of making profit by the taxpayer at the time of entering

transaction.

Referring to “Westfield v Ltd (1991)” a piece of land was bought by the taxpayer with

the intent of developing the shopping centre (Robin, 2017). A possibility of selling the land

was known to the taxpayer and did not had the original intention of selling the land. The court

of law held that the profits from the land was an ordinary income because the transaction was

short of commercial intention and not from the ordinary business proceeds of the taxpayer.

As a result, the first strand of Myer is not satisfied.

The Westfield case has been quoted in contrast to the view of Myer. Contrary to the

judgement held in “FCT v Westfield (1991)” profits and gains derived from the ordinary

business course constituted income but did not followed the decision made in “Myer

Emporium Ltd v FCT (1987)” (Burton, 2017). The profits that was made by the taxpayer

was from the commercial activity and was treated as income.

The difference overemphasizes the principle held in “Myer Emporium Ltd v FC of T

(1987)” (Miller & Oats, 2016). In “Westfield v FC of T (1991)” despite the profits made

B: Profit making intention while forming transaction:

Citing the case of “Cooling v FCT (1990)” the profit making purpose should not be

the sole intent of taxpayers (Woellner, 2013). If the transaction that is entered by taxpayer did

not had any profit making purpose while buying the asset, however the profit making purpose

while selling the asset. As a result, the second requirement of the first strand is not met.

C: Profit made in agreement with the original intention:

To meet the first strand of Myer, the way based on which the profit is obtained in

consistent with the original intention of making profit by the taxpayer at the time of entering

transaction.

Referring to “Westfield v Ltd (1991)” a piece of land was bought by the taxpayer with

the intent of developing the shopping centre (Robin, 2017). A possibility of selling the land

was known to the taxpayer and did not had the original intention of selling the land. The court

of law held that the profits from the land was an ordinary income because the transaction was

short of commercial intention and not from the ordinary business proceeds of the taxpayer.

As a result, the first strand of Myer is not satisfied.

The Westfield case has been quoted in contrast to the view of Myer. Contrary to the

judgement held in “FCT v Westfield (1991)” profits and gains derived from the ordinary

business course constituted income but did not followed the decision made in “Myer

Emporium Ltd v FCT (1987)” (Burton, 2017). The profits that was made by the taxpayer

was from the commercial activity and was treated as income.

The difference overemphasizes the principle held in “Myer Emporium Ltd v FC of T

(1987)” (Miller & Oats, 2016). In “Westfield v FC of T (1991)” despite the profits made

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

from the normal business course but it hardly follows the judgement made in “Myer

Emporium Ltd v FC of T (1987)” and the profit derived by the taxpayer was in the course of

business and constitute income in nature.

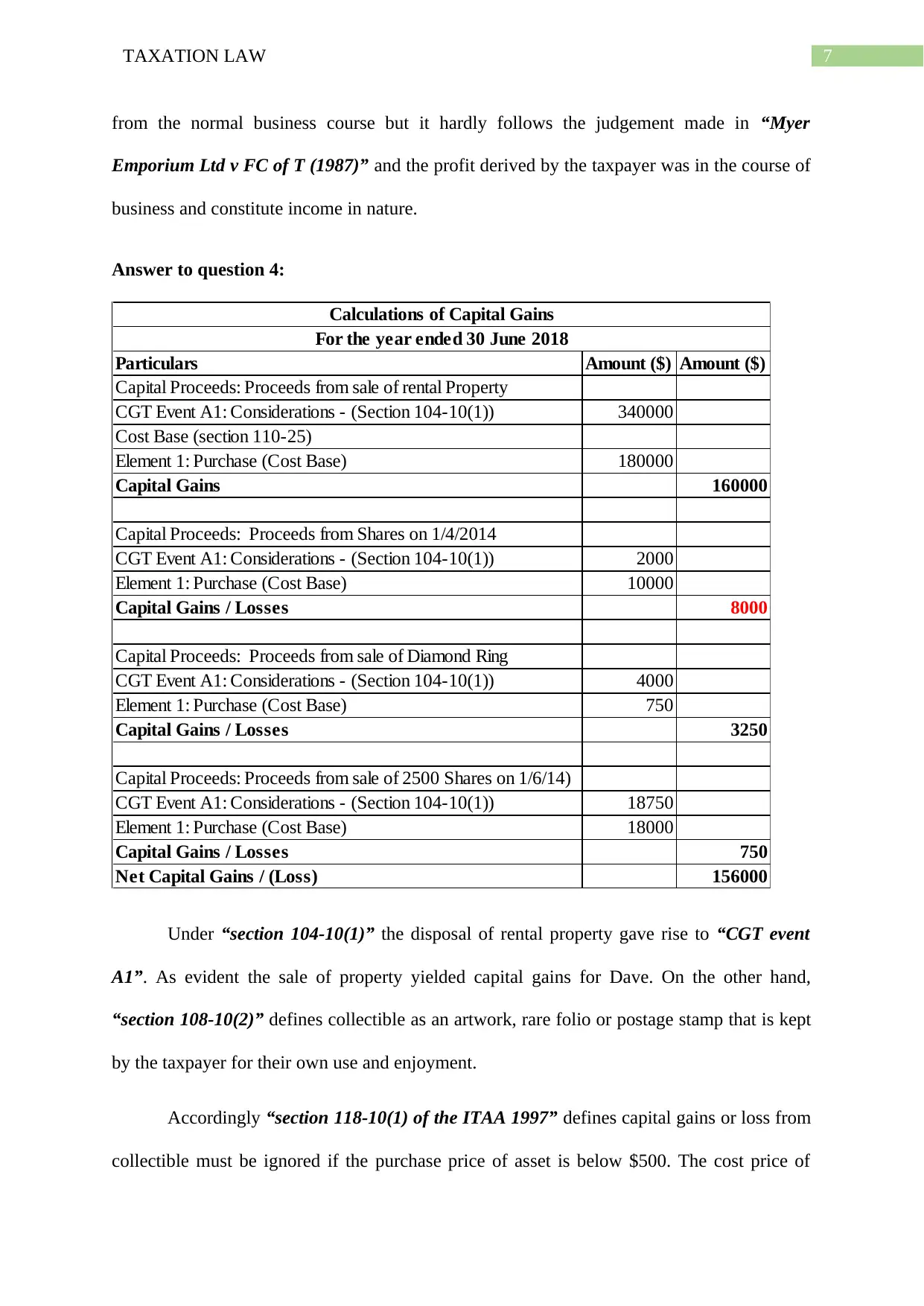

Answer to question 4:

Particulars Amount ($) Amount ($)

Capital Proceeds: Proceeds from sale of rental Property

CGT Event A1: Considerations - (Section 104-10(1)) 340000

Cost Base (section 110-25)

Element 1: Purchase (Cost Base) 180000

Capital Gains 160000

Capital Proceeds: Proceeds from Shares on 1/4/2014

CGT Event A1: Considerations - (Section 104-10(1)) 2000

Element 1: Purchase (Cost Base) 10000

Capital Gains / Losses 8000

Capital Proceeds: Proceeds from sale of Diamond Ring

CGT Event A1: Considerations - (Section 104-10(1)) 4000

Element 1: Purchase (Cost Base) 750

Capital Gains / Losses 3250

Capital Proceeds: Proceeds from sale of 2500 Shares on 1/6/14)

CGT Event A1: Considerations - (Section 104-10(1)) 18750

Element 1: Purchase (Cost Base) 18000

Capital Gains / Losses 750

Net Capital Gains / (Loss) 156000

Calculations of Capital Gains

For the year ended 30 June 2018

Under “section 104-10(1)” the disposal of rental property gave rise to “CGT event

A1”. As evident the sale of property yielded capital gains for Dave. On the other hand,

“section 108-10(2)” defines collectible as an artwork, rare folio or postage stamp that is kept

by the taxpayer for their own use and enjoyment.

Accordingly “section 118-10(1) of the ITAA 1997” defines capital gains or loss from

collectible must be ignored if the purchase price of asset is below $500. The cost price of

from the normal business course but it hardly follows the judgement made in “Myer

Emporium Ltd v FC of T (1987)” and the profit derived by the taxpayer was in the course of

business and constitute income in nature.

Answer to question 4:

Particulars Amount ($) Amount ($)

Capital Proceeds: Proceeds from sale of rental Property

CGT Event A1: Considerations - (Section 104-10(1)) 340000

Cost Base (section 110-25)

Element 1: Purchase (Cost Base) 180000

Capital Gains 160000

Capital Proceeds: Proceeds from Shares on 1/4/2014

CGT Event A1: Considerations - (Section 104-10(1)) 2000

Element 1: Purchase (Cost Base) 10000

Capital Gains / Losses 8000

Capital Proceeds: Proceeds from sale of Diamond Ring

CGT Event A1: Considerations - (Section 104-10(1)) 4000

Element 1: Purchase (Cost Base) 750

Capital Gains / Losses 3250

Capital Proceeds: Proceeds from sale of 2500 Shares on 1/6/14)

CGT Event A1: Considerations - (Section 104-10(1)) 18750

Element 1: Purchase (Cost Base) 18000

Capital Gains / Losses 750

Net Capital Gains / (Loss) 156000

Calculations of Capital Gains

For the year ended 30 June 2018

Under “section 104-10(1)” the disposal of rental property gave rise to “CGT event

A1”. As evident the sale of property yielded capital gains for Dave. On the other hand,

“section 108-10(2)” defines collectible as an artwork, rare folio or postage stamp that is kept

by the taxpayer for their own use and enjoyment.

Accordingly “section 118-10(1) of the ITAA 1997” defines capital gains or loss from

collectible must be ignored if the purchase price of asset is below $500. The cost price of

8TAXATION LAW

stamp was below $500 therefore capital gains made from the sale of stamp by Dale would be

ignored. Dale sold the diamond ring that had the cost base of $500 for 750. The capital gains

from the collectible is included for determining the net amount of capital gains for the year.

As per “section 108-20(2)” personal use asset includes mobile phone, boat, yacht or

television that are usually kept for taxpayer’s own enjoyment (Fleurbaey & Maniquet, 2018).

Capital loss made under “section 108-20(1)” from the sale of personal use asset should be

ignored. The disposal of boat yielded capital loss and the same is excluded from capital gains.

As per the ATO capital gains derived from the shares or unit are treated in the similar

manner just like the other asset for the purpose of taxation (Bankman et al., 2017). Dale sole

shares on 1/4/14 which yielded capital loss. In the later part Dale sold shares that were

acquired on 3/4/1984. The capital gains made were from the pre-CGT asset therefore it is

excluded from capital gains. Additionally, Dale sold shares that was purchased on 25/5/1996

for 18750. The disposal resulted in capital and it is included capital gains.

Answer to question 5:

Answer to A:

According to “section 8-1 of the ITAA 1997” outgoings which is pre-commencement

to the revenue deriving activities and not in the ordinary business is non-deductible expenses.

The judgement in “Softwood Pulp & Paper v FCT” held that the feasibility expenses which

was occurred by the taxpayer to set up the paper producing mill was preliminary in nature

(Murphy & Higgins, 2016). Consequently, a business incurring interest on loan at the

preparatory phase would not be allowed for deduction because there is no relation with the

income generating activities. For a business to progress from the preparatory stage it is

necessary that the business activities have begun.

stamp was below $500 therefore capital gains made from the sale of stamp by Dale would be

ignored. Dale sold the diamond ring that had the cost base of $500 for 750. The capital gains

from the collectible is included for determining the net amount of capital gains for the year.

As per “section 108-20(2)” personal use asset includes mobile phone, boat, yacht or

television that are usually kept for taxpayer’s own enjoyment (Fleurbaey & Maniquet, 2018).

Capital loss made under “section 108-20(1)” from the sale of personal use asset should be

ignored. The disposal of boat yielded capital loss and the same is excluded from capital gains.

As per the ATO capital gains derived from the shares or unit are treated in the similar

manner just like the other asset for the purpose of taxation (Bankman et al., 2017). Dale sole

shares on 1/4/14 which yielded capital loss. In the later part Dale sold shares that were

acquired on 3/4/1984. The capital gains made were from the pre-CGT asset therefore it is

excluded from capital gains. Additionally, Dale sold shares that was purchased on 25/5/1996

for 18750. The disposal resulted in capital and it is included capital gains.

Answer to question 5:

Answer to A:

According to “section 8-1 of the ITAA 1997” outgoings which is pre-commencement

to the revenue deriving activities and not in the ordinary business is non-deductible expenses.

The judgement in “Softwood Pulp & Paper v FCT” held that the feasibility expenses which

was occurred by the taxpayer to set up the paper producing mill was preliminary in nature

(Murphy & Higgins, 2016). Consequently, a business incurring interest on loan at the

preparatory phase would not be allowed for deduction because there is no relation with the

income generating activities. For a business to progress from the preparatory stage it is

necessary that the business activities have begun.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to B:

The law court in “Ronpibon Tin NL v FCT (1949)” explained the “Incident and

Relevant Test”. Under this test, accordingly an expenditure would be allowed for deduction

as outgoing given the expenses are incurred in producing the assessable income and the same

must be relevant and incidental to that extent (Buenker, 2018). For an expense to qualify

within the initial part of subsection it is essential and satisfactory that the losses or outgoings

are incurred in producing taxable income. The interest on loan forms the essential feature of

generating assessable income. The court held that the interest on loan would be allowed as

deductible expenses.

Answer to C:

As evident in “FCT v Brown” the taxpayer borrowed money from bank to purchase a

deli business to operate under partnership with his wife. The business was eventually sold by

the taxpayer but he continued to pay interest on loan as the sales proceeds were inadequate to

pay off the debt. The commissioner allowed the taxpayer to claim deduction because the loan

was taken at the time of carrying on the business under partnership with the intent of

producing income.

Answer to question 6:

According to “section 8-1” a person is entitled for an allowable deduction if the

expenses incurred were in the ordinary business course for the derivation of assessable

income (Miller & Oats, 2016). A taxpayer taking loan to purchase the rental property, the

interest incurred is allowed for deduction.

Approximately 40% of the Australian mortgages are based on interest. Interest would

probably become Australia’s subprime. The interest on loan enables the investors borrow

more and invest in the rental property. As a result the investors not only increase gains from

Answer to B:

The law court in “Ronpibon Tin NL v FCT (1949)” explained the “Incident and

Relevant Test”. Under this test, accordingly an expenditure would be allowed for deduction

as outgoing given the expenses are incurred in producing the assessable income and the same

must be relevant and incidental to that extent (Buenker, 2018). For an expense to qualify

within the initial part of subsection it is essential and satisfactory that the losses or outgoings

are incurred in producing taxable income. The interest on loan forms the essential feature of

generating assessable income. The court held that the interest on loan would be allowed as

deductible expenses.

Answer to C:

As evident in “FCT v Brown” the taxpayer borrowed money from bank to purchase a

deli business to operate under partnership with his wife. The business was eventually sold by

the taxpayer but he continued to pay interest on loan as the sales proceeds were inadequate to

pay off the debt. The commissioner allowed the taxpayer to claim deduction because the loan

was taken at the time of carrying on the business under partnership with the intent of

producing income.

Answer to question 6:

According to “section 8-1” a person is entitled for an allowable deduction if the

expenses incurred were in the ordinary business course for the derivation of assessable

income (Miller & Oats, 2016). A taxpayer taking loan to purchase the rental property, the

interest incurred is allowed for deduction.

Approximately 40% of the Australian mortgages are based on interest. Interest would

probably become Australia’s subprime. The interest on loan enables the investors borrow

more and invest in the rental property. As a result the investors not only increase gains from

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

the rental property but also face higher debt. The sum of interest on loan is treated as the sign

of hypothetical bubble. Therefore, it implies that the property owners does not have much

equity when the property prices falls.

the rental property but also face higher debt. The sum of interest on loan is treated as the sign

of hypothetical bubble. Therefore, it implies that the property owners does not have much

equity when the property prices falls.

11TAXATION LAW

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2017). Federal Income

Taxation. Wolters Kluwer Law & Business.

Buenker, J. D. (2018). The Income Tax and the Progressive Era. Routledge.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014) principles of business taxation.

James, S. (2014). The economics of taxation.

Jover-Ledesma, G. (2014). Principles of business taxation. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. (2013). Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2015). Australian taxation law cases 2015. Pyrmont, NSW: Thomson Reuters.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Robin, H. (2017). Australian taxation law 2017. Oxford University Press.

References:

Bankman, J., Shaviro, D. N., Stark, K. J., & Kleinbard, E. D. (2017). Federal Income

Taxation. Wolters Kluwer Law & Business.

Buenker, J. D. (2018). The Income Tax and the Progressive Era. Routledge.

Burton, M. (2017). A Review of Judicial References to the Dictum of Jordan CJ, Expressed

in Scott v. Commissioner of Taxation, in Elaborating the Meaning of Income for the

Purposes of the Australian Income Tax. J. Austl. Tax'n, 19, 50.

Fleurbaey, M., & Maniquet, F. (2018). Optimal income taxation theory and principles of

fairness. Journal of Economic Literature, 56(3), 1029-79.

Grange, J., Jover-Ledesma, G., & Maydew, G. (2014) principles of business taxation.

James, S. (2014). The economics of taxation.

Jover-Ledesma, G. (2014). Principles of business taxation. [Place of publication not

identified]: Cch Incorporated.

Kenny, P. (2013). Australian tax. Chatswood, N.S.W.: LexisNexis Butterworths.

Krever, R. (2015). Australian taxation law cases 2015. Pyrmont, NSW: Thomson Reuters.

Miller, A., & Oats, L. (2016). Principles of international taxation. Bloomsbury Publishing.

Morgan, A., Mortimer, C., & Pinto, D. (2013). A practical introduction to Australian

taxation law. North Ryde [N.S.W.]: CCH Australia.

Murphy, K. E., & Higgins, M. (2016). Concepts in Federal Taxation 2017. Cengage

Learning.

Robin, H. (2017). Australian taxation law 2017. Oxford University Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.