LAW19034: Taxation Law and Practice Assignment - Term 2, 2018

VerifiedAdded on 2023/06/09

|11

|2479

|233

Homework Assignment

AI Summary

This assignment solution addresses a case study involving Arnold and Bob Jones, brothers who operate a farm. The solution begins with a computation of the Franking Credit Account for Jones Brother Pty Ltd, detailing PAYG instalments, receipts, and distributions. It then provides a statement calculating income from livestock trading, including receipts, expenses, and net income, alongside a valuation of livestock. Furthermore, the solution computes the assessable and taxable income for Bob Jones, considering income from livestock and employment. The assignment also explores the small business restructure rollover, explaining its application to the transfer of farm assets to a unit trust. Finally, the solution discusses the use of trusts for investment and business purposes, and the tax implications for beneficiaries and trustees, particularly in Arnold's plan to establish a trust for his sons.

Running head: TAXATION LAW AND PRACTICE

Taxation Law and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law and Practice

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW AND PRACTICE

Table of Contents

Answer to question A:................................................................................................................2

Computation of Franking Credit Account..................................................................................2

Answer to question B:................................................................................................................3

Computation of Live Stock Trading Account............................................................................3

Computation of Assessable Income for Bob Jones....................................................................5

Answer to question C:................................................................................................................6

Answer to question D:................................................................................................................7

Table of Contents

Answer to question A:................................................................................................................2

Computation of Franking Credit Account..................................................................................2

Answer to question B:................................................................................................................3

Computation of Live Stock Trading Account............................................................................3

Computation of Assessable Income for Bob Jones....................................................................5

Answer to question C:................................................................................................................6

Answer to question D:................................................................................................................7

2TAXATION LAW AND PRACTICE

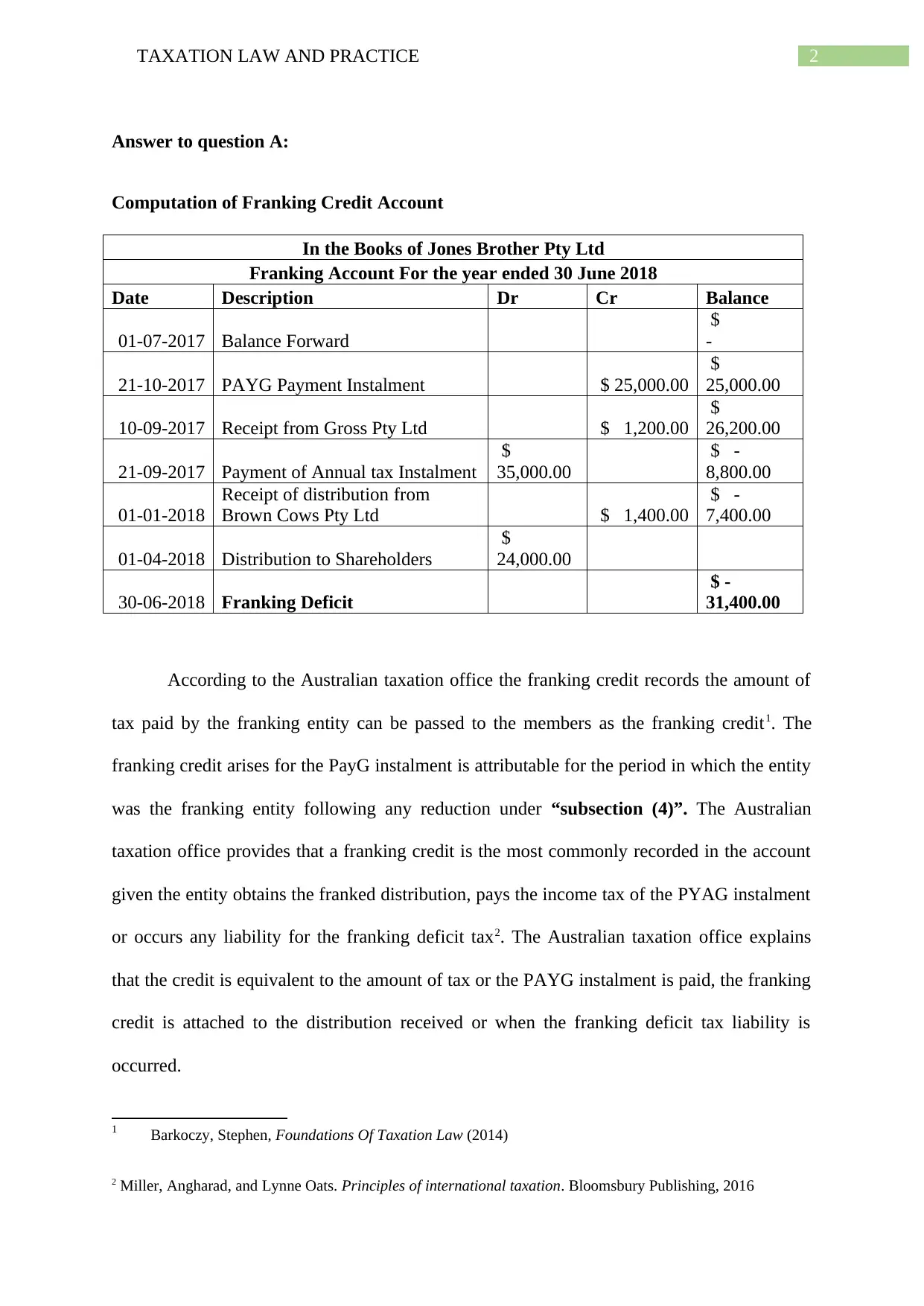

Answer to question A:

Computation of Franking Credit Account

In the Books of Jones Brother Pty Ltd

Franking Account For the year ended 30 June 2018

Date Description Dr Cr Balance

01-07-2017 Balance Forward

$

-

21-10-2017 PAYG Payment Instalment $ 25,000.00

$

25,000.00

10-09-2017 Receipt from Gross Pty Ltd $ 1,200.00

$

26,200.00

21-09-2017 Payment of Annual tax Instalment

$

35,000.00

$ -

8,800.00

01-01-2018

Receipt of distribution from

Brown Cows Pty Ltd $ 1,400.00

$ -

7,400.00

01-04-2018 Distribution to Shareholders

$

24,000.00

30-06-2018 Franking Deficit

$ -

31,400.00

According to the Australian taxation office the franking credit records the amount of

tax paid by the franking entity can be passed to the members as the franking credit1. The

franking credit arises for the PayG instalment is attributable for the period in which the entity

was the franking entity following any reduction under “subsection (4)”. The Australian

taxation office provides that a franking credit is the most commonly recorded in the account

given the entity obtains the franked distribution, pays the income tax of the PYAG instalment

or occurs any liability for the franking deficit tax2. The Australian taxation office explains

that the credit is equivalent to the amount of tax or the PAYG instalment is paid, the franking

credit is attached to the distribution received or when the franking deficit tax liability is

occurred.

1 Barkoczy, Stephen, Foundations Of Taxation Law (2014)

2 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016

Answer to question A:

Computation of Franking Credit Account

In the Books of Jones Brother Pty Ltd

Franking Account For the year ended 30 June 2018

Date Description Dr Cr Balance

01-07-2017 Balance Forward

$

-

21-10-2017 PAYG Payment Instalment $ 25,000.00

$

25,000.00

10-09-2017 Receipt from Gross Pty Ltd $ 1,200.00

$

26,200.00

21-09-2017 Payment of Annual tax Instalment

$

35,000.00

$ -

8,800.00

01-01-2018

Receipt of distribution from

Brown Cows Pty Ltd $ 1,400.00

$ -

7,400.00

01-04-2018 Distribution to Shareholders

$

24,000.00

30-06-2018 Franking Deficit

$ -

31,400.00

According to the Australian taxation office the franking credit records the amount of

tax paid by the franking entity can be passed to the members as the franking credit1. The

franking credit arises for the PayG instalment is attributable for the period in which the entity

was the franking entity following any reduction under “subsection (4)”. The Australian

taxation office provides that a franking credit is the most commonly recorded in the account

given the entity obtains the franked distribution, pays the income tax of the PYAG instalment

or occurs any liability for the franking deficit tax2. The Australian taxation office explains

that the credit is equivalent to the amount of tax or the PAYG instalment is paid, the franking

credit is attached to the distribution received or when the franking deficit tax liability is

occurred.

1 Barkoczy, Stephen, Foundations Of Taxation Law (2014)

2 Miller, Angharad, and Lynne Oats. Principles of international taxation. Bloomsbury Publishing, 2016

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW AND PRACTICE

Similarly, for Jones Brother Pty Ltd the company paid the PAYG instalment on 21st

October 2017 therefore, the sum of $25,000 will be considered as credit and should be

recorded under credit side of the franked account. The credit represents the equivalent

amount of the tax of the PAYG instalment that is paid.

Similarly, for Jones Brother Pty Ltd the company paid the PAYG instalment on 21st

October 2017 therefore, the sum of $25,000 will be considered as credit and should be

recorded under credit side of the franked account. The credit represents the equivalent

amount of the tax of the PAYG instalment that is paid.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW AND PRACTICE

According to the Australian taxation office where the income tax liability is only paid

partially, franking credits would not originate from the sum that remains outstanding3. Any

form of partial payments that was made in the direction of outstanding activity statement

liabilities would be allocated in accordance with the policy4.

Under “section 204-15 of the ITAA 1997” a franking credit originates for the entity

when a franking debit is specified under the “subsection 201-15”5. The franking credit

received from Grass Pty Ltd for Jones Brother Pty Ltd would be recorded under the credit

side. As evident from the above stated computation the franking credit account for the Jones

Brother Pty Ltd recorded a deficit balance. This franking credit account is in deficit at a

particular time because the amount of franking credit has gone past the sum of franking

credits.

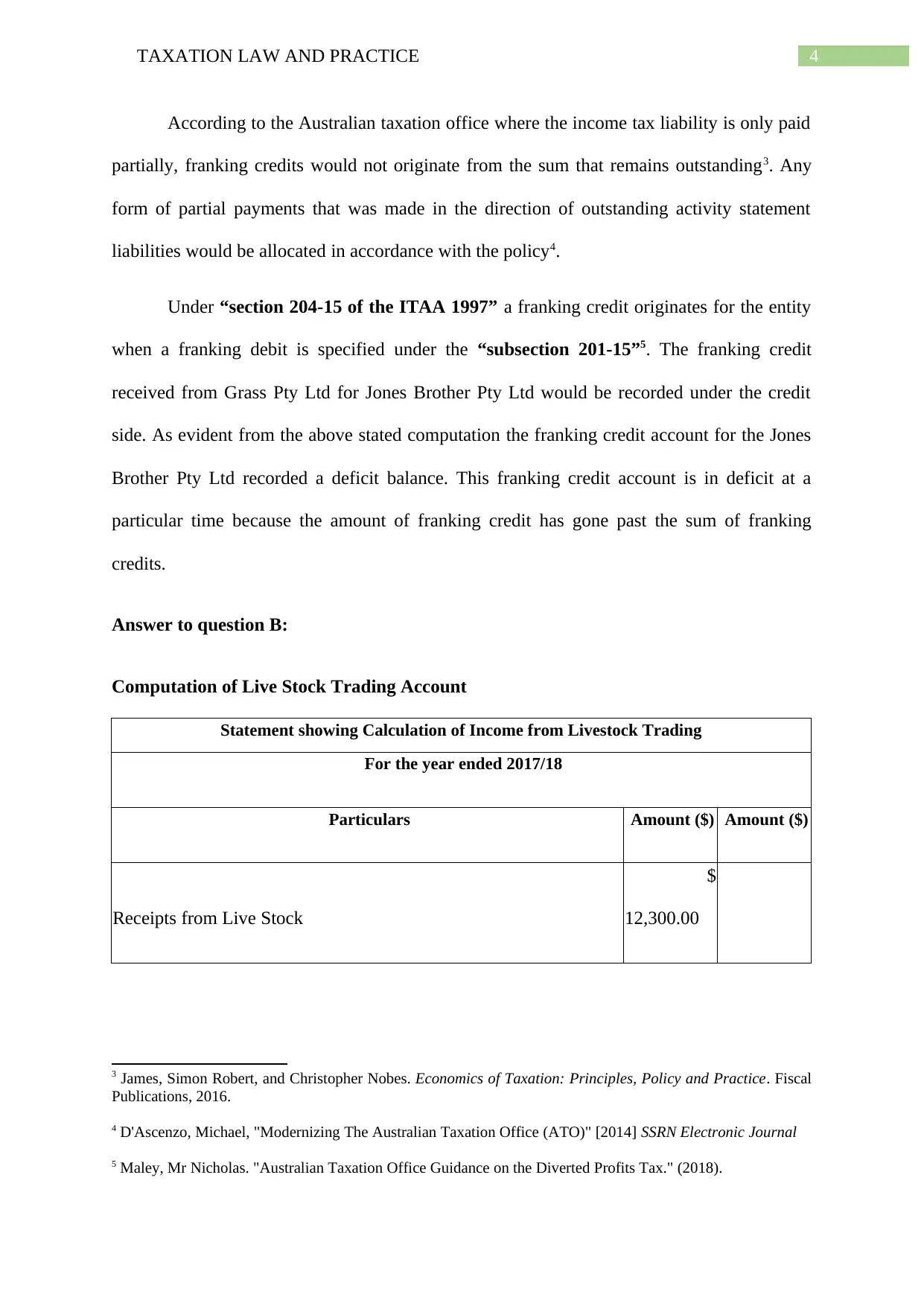

Answer to question B:

Computation of Live Stock Trading Account

Statement showing Calculation of Income from Livestock Trading

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Receipts from Live Stock

$

12,300.00

3 James, Simon Robert, and Christopher Nobes. Economics of Taxation: Principles, Policy and Practice. Fiscal

Publications, 2016.

4 D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN Electronic Journal

5 Maley, Mr Nicholas. "Australian Taxation Office Guidance on the Diverted Profits Tax." (2018).

According to the Australian taxation office where the income tax liability is only paid

partially, franking credits would not originate from the sum that remains outstanding3. Any

form of partial payments that was made in the direction of outstanding activity statement

liabilities would be allocated in accordance with the policy4.

Under “section 204-15 of the ITAA 1997” a franking credit originates for the entity

when a franking debit is specified under the “subsection 201-15”5. The franking credit

received from Grass Pty Ltd for Jones Brother Pty Ltd would be recorded under the credit

side. As evident from the above stated computation the franking credit account for the Jones

Brother Pty Ltd recorded a deficit balance. This franking credit account is in deficit at a

particular time because the amount of franking credit has gone past the sum of franking

credits.

Answer to question B:

Computation of Live Stock Trading Account

Statement showing Calculation of Income from Livestock Trading

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Receipts from Live Stock

$

12,300.00

3 James, Simon Robert, and Christopher Nobes. Economics of Taxation: Principles, Policy and Practice. Fiscal

Publications, 2016.

4 D'Ascenzo, Michael, "Modernizing The Australian Taxation Office (ATO)" [2014] SSRN Electronic Journal

5 Maley, Mr Nicholas. "Australian Taxation Office Guidance on the Diverted Profits Tax." (2018).

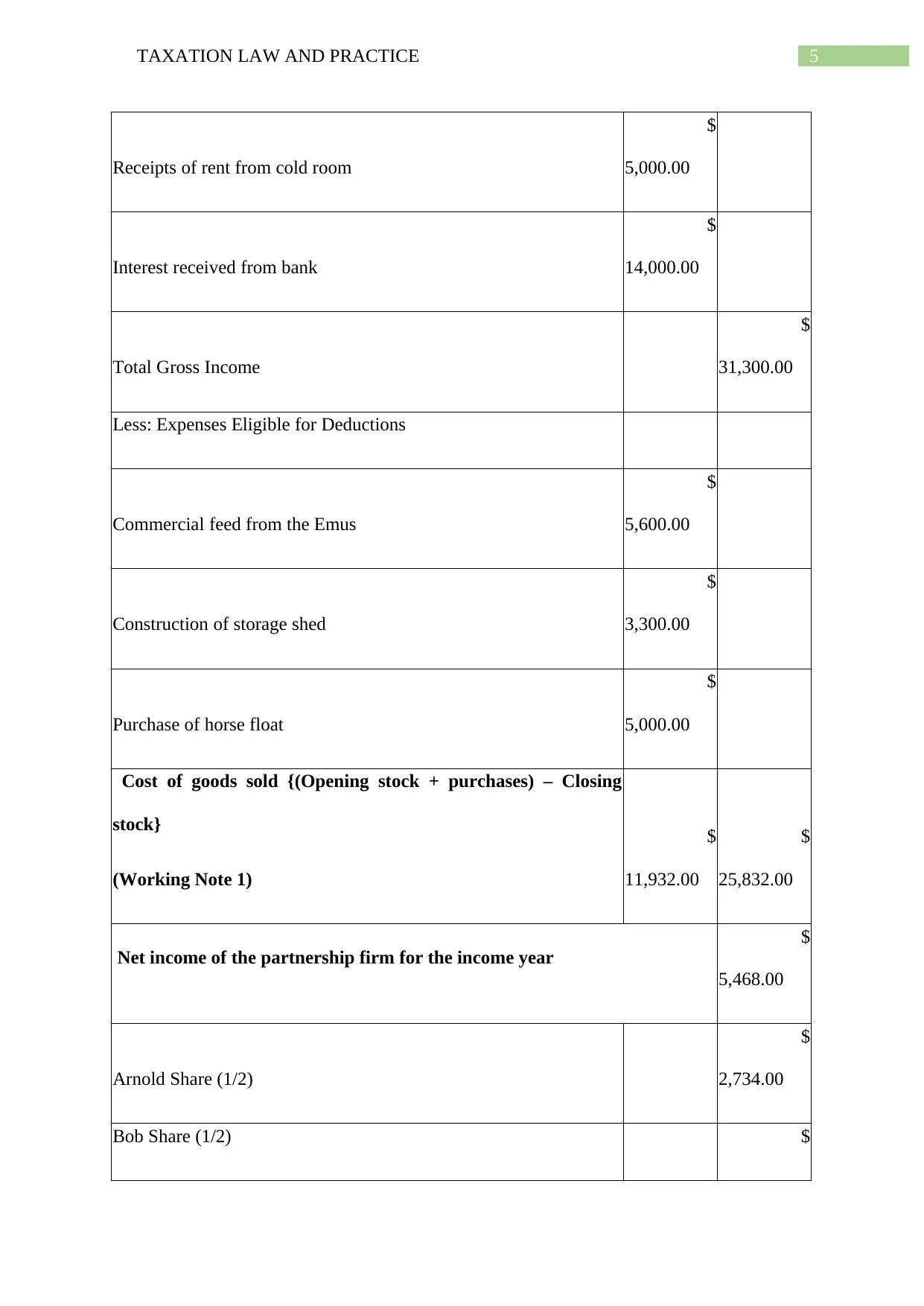

5TAXATION LAW AND PRACTICE

Receipts of rent from cold room

$

5,000.00

Interest received from bank

$

14,000.00

Total Gross Income

$

31,300.00

Less: Expenses Eligible for Deductions

Commercial feed from the Emus

$

5,600.00

Construction of storage shed

$

3,300.00

Purchase of horse float

$

5,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock}

(Working Note 1)

$

11,932.00

$

25,832.00

Net income of the partnership firm for the income year

$

5,468.00

Arnold Share (1/2)

$

2,734.00

Bob Share (1/2) $

Receipts of rent from cold room

$

5,000.00

Interest received from bank

$

14,000.00

Total Gross Income

$

31,300.00

Less: Expenses Eligible for Deductions

Commercial feed from the Emus

$

5,600.00

Construction of storage shed

$

3,300.00

Purchase of horse float

$

5,000.00

Cost of goods sold {(Opening stock + purchases) – Closing

stock}

(Working Note 1)

$

11,932.00

$

25,832.00

Net income of the partnership firm for the income year

$

5,468.00

Arnold Share (1/2)

$

2,734.00

Bob Share (1/2) $

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW AND PRACTICE

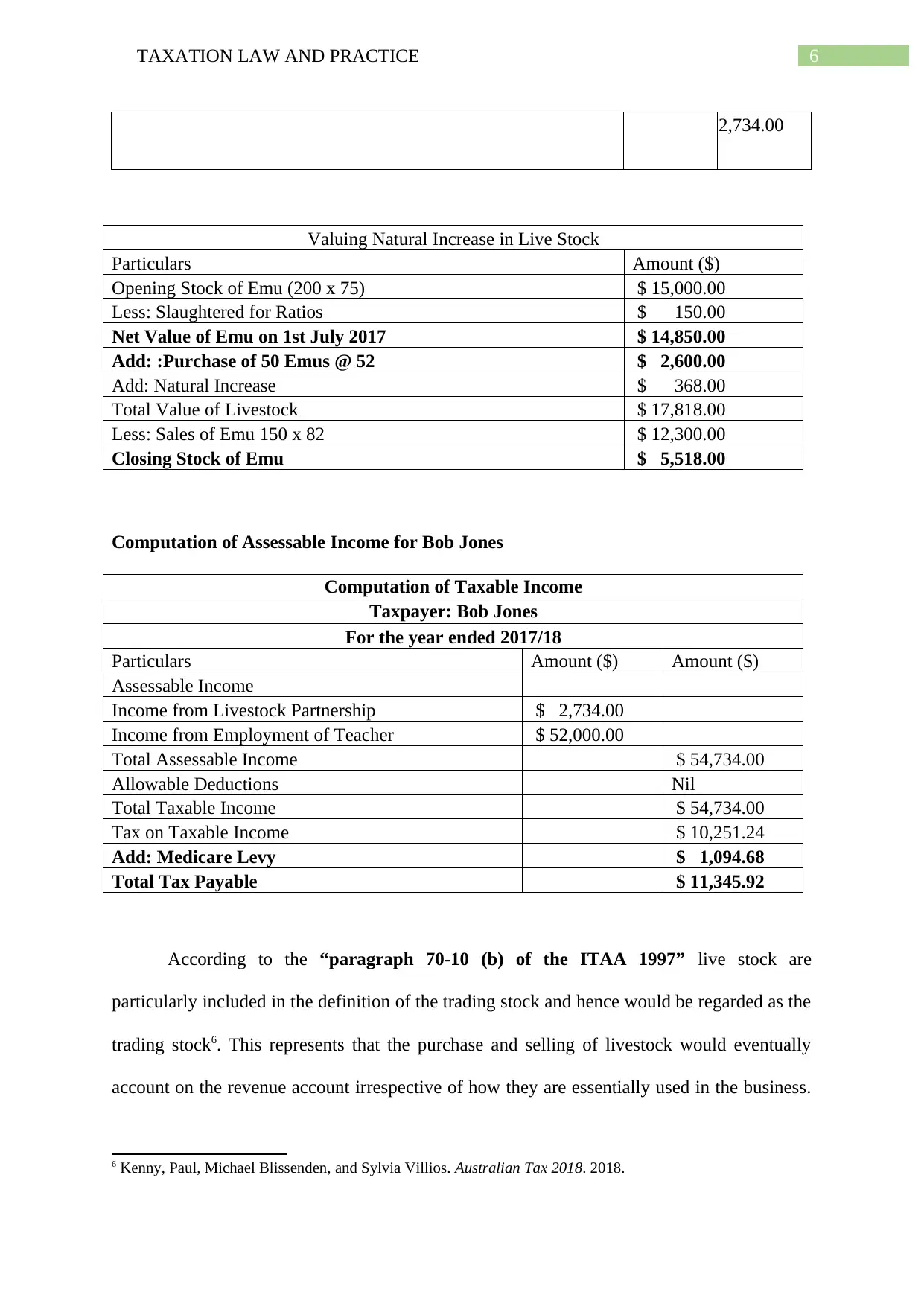

2,734.00

Valuing Natural Increase in Live Stock

Particulars Amount ($)

Opening Stock of Emu (200 x 75) $ 15,000.00

Less: Slaughtered for Ratios $ 150.00

Net Value of Emu on 1st July 2017 $ 14,850.00

Add: :Purchase of 50 Emus @ 52 $ 2,600.00

Add: Natural Increase $ 368.00

Total Value of Livestock $ 17,818.00

Less: Sales of Emu 150 x 82 $ 12,300.00

Closing Stock of Emu $ 5,518.00

Computation of Assessable Income for Bob Jones

Computation of Taxable Income

Taxpayer: Bob Jones

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Assessable Income

Income from Livestock Partnership $ 2,734.00

Income from Employment of Teacher $ 52,000.00

Total Assessable Income $ 54,734.00

Allowable Deductions Nil

Total Taxable Income $ 54,734.00

Tax on Taxable Income $ 10,251.24

Add: Medicare Levy $ 1,094.68

Total Tax Payable $ 11,345.92

According to the “paragraph 70-10 (b) of the ITAA 1997” live stock are

particularly included in the definition of the trading stock and hence would be regarded as the

trading stock6. This represents that the purchase and selling of livestock would eventually

account on the revenue account irrespective of how they are essentially used in the business.

6 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

2,734.00

Valuing Natural Increase in Live Stock

Particulars Amount ($)

Opening Stock of Emu (200 x 75) $ 15,000.00

Less: Slaughtered for Ratios $ 150.00

Net Value of Emu on 1st July 2017 $ 14,850.00

Add: :Purchase of 50 Emus @ 52 $ 2,600.00

Add: Natural Increase $ 368.00

Total Value of Livestock $ 17,818.00

Less: Sales of Emu 150 x 82 $ 12,300.00

Closing Stock of Emu $ 5,518.00

Computation of Assessable Income for Bob Jones

Computation of Taxable Income

Taxpayer: Bob Jones

For the year ended 2017/18

Particulars Amount ($) Amount ($)

Assessable Income

Income from Livestock Partnership $ 2,734.00

Income from Employment of Teacher $ 52,000.00

Total Assessable Income $ 54,734.00

Allowable Deductions Nil

Total Taxable Income $ 54,734.00

Tax on Taxable Income $ 10,251.24

Add: Medicare Levy $ 1,094.68

Total Tax Payable $ 11,345.92

According to the “paragraph 70-10 (b) of the ITAA 1997” live stock are

particularly included in the definition of the trading stock and hence would be regarded as the

trading stock6. This represents that the purchase and selling of livestock would eventually

account on the revenue account irrespective of how they are essentially used in the business.

6 Kenny, Paul, Michael Blissenden, and Sylvia Villios. Australian Tax 2018. 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW AND PRACTICE

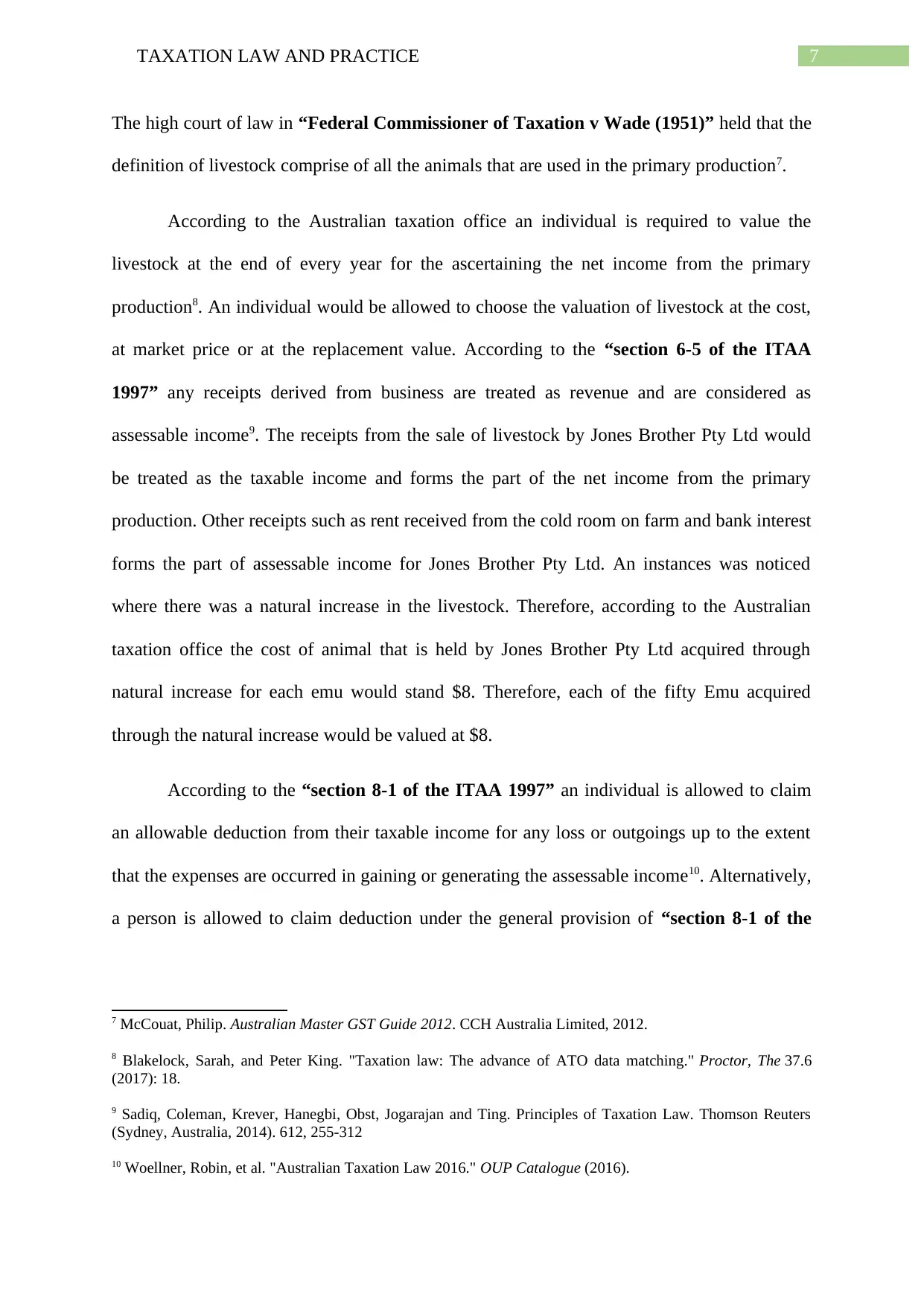

The high court of law in “Federal Commissioner of Taxation v Wade (1951)” held that the

definition of livestock comprise of all the animals that are used in the primary production7.

According to the Australian taxation office an individual is required to value the

livestock at the end of every year for the ascertaining the net income from the primary

production8. An individual would be allowed to choose the valuation of livestock at the cost,

at market price or at the replacement value. According to the “section 6-5 of the ITAA

1997” any receipts derived from business are treated as revenue and are considered as

assessable income9. The receipts from the sale of livestock by Jones Brother Pty Ltd would

be treated as the taxable income and forms the part of the net income from the primary

production. Other receipts such as rent received from the cold room on farm and bank interest

forms the part of assessable income for Jones Brother Pty Ltd. An instances was noticed

where there was a natural increase in the livestock. Therefore, according to the Australian

taxation office the cost of animal that is held by Jones Brother Pty Ltd acquired through

natural increase for each emu would stand $8. Therefore, each of the fifty Emu acquired

through the natural increase would be valued at $8.

According to the “section 8-1 of the ITAA 1997” an individual is allowed to claim

an allowable deduction from their taxable income for any loss or outgoings up to the extent

that the expenses are occurred in gaining or generating the assessable income10. Alternatively,

a person is allowed to claim deduction under the general provision of “section 8-1 of the

7 McCouat, Philip. Australian Master GST Guide 2012. CCH Australia Limited, 2012.

8 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

9 Sadiq, Coleman, Krever, Hanegbi, Obst, Jogarajan and Ting. Principles of Taxation Law. Thomson Reuters

(Sydney, Australia, 2014). 612, 255-312

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

The high court of law in “Federal Commissioner of Taxation v Wade (1951)” held that the

definition of livestock comprise of all the animals that are used in the primary production7.

According to the Australian taxation office an individual is required to value the

livestock at the end of every year for the ascertaining the net income from the primary

production8. An individual would be allowed to choose the valuation of livestock at the cost,

at market price or at the replacement value. According to the “section 6-5 of the ITAA

1997” any receipts derived from business are treated as revenue and are considered as

assessable income9. The receipts from the sale of livestock by Jones Brother Pty Ltd would

be treated as the taxable income and forms the part of the net income from the primary

production. Other receipts such as rent received from the cold room on farm and bank interest

forms the part of assessable income for Jones Brother Pty Ltd. An instances was noticed

where there was a natural increase in the livestock. Therefore, according to the Australian

taxation office the cost of animal that is held by Jones Brother Pty Ltd acquired through

natural increase for each emu would stand $8. Therefore, each of the fifty Emu acquired

through the natural increase would be valued at $8.

According to the “section 8-1 of the ITAA 1997” an individual is allowed to claim

an allowable deduction from their taxable income for any loss or outgoings up to the extent

that the expenses are occurred in gaining or generating the assessable income10. Alternatively,

a person is allowed to claim deduction under the general provision of “section 8-1 of the

7 McCouat, Philip. Australian Master GST Guide 2012. CCH Australia Limited, 2012.

8 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

9 Sadiq, Coleman, Krever, Hanegbi, Obst, Jogarajan and Ting. Principles of Taxation Law. Thomson Reuters

(Sydney, Australia, 2014). 612, 255-312

10 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

8TAXATION LAW AND PRACTICE

ITAA 1997” if the expenses are necessarily incurred in executing the business activity with

the objective of deriving assessable income11.

Similarly for Jones Brother Pty Ltd expenses on commercial feed for Emus constitute

a business expenses and hence the sum of $5,600 would be allowed for deduction under the

general provision of “section 8-1 of the ITAA 1997”. Jones Brother Pty Ltd also reports

expenses for the construction of new dam. Expenses that are incurred in the construction are

held as capital in nature. Referring the judgement of “Western Suburbs Cinemas v FCT”

capital expenses are not allowed for deduction under the general provision of “section 8-1 of

the ITAA 1997”12. Therefore, cost incurred in the construction of new dam is a capital

expenditure and no deduction is allowable.

Answer to question C:

As evident from the situation of Arnold and Bob they have decided to dispose the

farm assets in the coming income year to the unit trust. According to the Australian taxation

office the small business restructure rollover allows the small business to transfer the active

asset from one entity to another or more entities without occurring any form of income tax

liability13. The taxation office of Australia defines that the small business rollover is

application to the transfer of active assets that are CGT assets, trading stocks or the

depreciating assets. For a business to be held eligible for the rollover, the transaction should

not lead to change in the ultimate ownership of the transferred assets14. The ultimate

11 Devos, Ken. "The impact of tax professionals upon the compliance behaviour of Australian individual

taxpayers." Revenue Law Journal 22.1 (2012): 31.

12 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

14 Basu, Subhajit, Global Perspectives On E-Commerce Taxation Law (Routledge, 2016)

ITAA 1997” if the expenses are necessarily incurred in executing the business activity with

the objective of deriving assessable income11.

Similarly for Jones Brother Pty Ltd expenses on commercial feed for Emus constitute

a business expenses and hence the sum of $5,600 would be allowed for deduction under the

general provision of “section 8-1 of the ITAA 1997”. Jones Brother Pty Ltd also reports

expenses for the construction of new dam. Expenses that are incurred in the construction are

held as capital in nature. Referring the judgement of “Western Suburbs Cinemas v FCT”

capital expenses are not allowed for deduction under the general provision of “section 8-1 of

the ITAA 1997”12. Therefore, cost incurred in the construction of new dam is a capital

expenditure and no deduction is allowable.

Answer to question C:

As evident from the situation of Arnold and Bob they have decided to dispose the

farm assets in the coming income year to the unit trust. According to the Australian taxation

office the small business restructure rollover allows the small business to transfer the active

asset from one entity to another or more entities without occurring any form of income tax

liability13. The taxation office of Australia defines that the small business rollover is

application to the transfer of active assets that are CGT assets, trading stocks or the

depreciating assets. For a business to be held eligible for the rollover, the transaction should

not lead to change in the ultimate ownership of the transferred assets14. The ultimate

11 Devos, Ken. "The impact of tax professionals upon the compliance behaviour of Australian individual

taxpayers." Revenue Law Journal 22.1 (2012): 31.

12 Woellner, Robin, et al. "Australian Taxation Law 2016." OUP Catalogue (2016).

13 Saad, Natrah. "Tax knowledge, tax complexity and tax compliance: Taxpayers’ view." Procedia-Social and

Behavioral Sciences 109 (2014): 1069-1075.

14 Basu, Subhajit, Global Perspectives On E-Commerce Taxation Law (Routledge, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW AND PRACTICE

economic owners of the assets are the person that is individuals who either directly or

indirectly owns the asset.

Similarly, in the current situation of Jones Brothers Pty Ltd the rollover relief is

available since the transfer of assets to the unit trust genuinely forms part of restructure. The

rollover relief is applicable to the rollover transfer of assets active CGT assets held by the

Arnold and Bob. The transaction by Bob and Arnold does not lead to change in the economic

ownership of the transferred assets. In the present situation of Jones Brothers Pty Ltd the

ultimate economic owners of the asset are the Arnold and Bob as they directly own the assets.

The assets that are eligible for the roll-over restructuring are the active assets that are CGT

assets. They assets forms the portion of the genuine restructure of the ongoing business.

According to the Australian taxation office, assets that are generally transferred would

not result in the income tax liability originating for either of the party when conducting the

transfer15. Similarly in the situation of Arnold and Bob Jones the transfer of farm capital

assets during the process of restructure rollover would not attract any income tax liability for

either of the party at the time of transfer.

Answer to question D:

Trust are largely used for investment and for business purpose. According to the

Australian taxation office trust is referred as the obligations that are applied on the person or

the other entity to hold the property in the benefit of the beneficiaries16. The beneficiaries are

required to include in their assessable income the share of the trust income while filing tax

returns. The net income that is derived from the trust is held for assessment for the year after

taking into the consideration the allowable deductions. As evident in the current situation of

15 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

16 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

economic owners of the assets are the person that is individuals who either directly or

indirectly owns the asset.

Similarly, in the current situation of Jones Brothers Pty Ltd the rollover relief is

available since the transfer of assets to the unit trust genuinely forms part of restructure. The

rollover relief is applicable to the rollover transfer of assets active CGT assets held by the

Arnold and Bob. The transaction by Bob and Arnold does not lead to change in the economic

ownership of the transferred assets. In the present situation of Jones Brothers Pty Ltd the

ultimate economic owners of the asset are the Arnold and Bob as they directly own the assets.

The assets that are eligible for the roll-over restructuring are the active assets that are CGT

assets. They assets forms the portion of the genuine restructure of the ongoing business.

According to the Australian taxation office, assets that are generally transferred would

not result in the income tax liability originating for either of the party when conducting the

transfer15. Similarly in the situation of Arnold and Bob Jones the transfer of farm capital

assets during the process of restructure rollover would not attract any income tax liability for

either of the party at the time of transfer.

Answer to question D:

Trust are largely used for investment and for business purpose. According to the

Australian taxation office trust is referred as the obligations that are applied on the person or

the other entity to hold the property in the benefit of the beneficiaries16. The beneficiaries are

required to include in their assessable income the share of the trust income while filing tax

returns. The net income that is derived from the trust is held for assessment for the year after

taking into the consideration the allowable deductions. As evident in the current situation of

15 Braithwaite, Valerie. Taxing democracy: Understanding tax avoidance and evasion. Routledge, 2017.

16 Blakelock, Sarah, and Peter King. "Taxation law: The advance of ATO data matching." Proctor, The 37.6

(2017): 18.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW AND PRACTICE

Arnold he intends to set up the trust for their two sons. The taxation office of Australia

defines that an individual is required to pay the tax relating to the share of the trust’s net

income based on the applicable tax rates17. Furthermore, the trustee is also required to pay the

tax on behalf of their minors depending upon the share of the trust net income. The

beneficiaries are under the obligations of declaring the income in their own income tax.

The present situation of Arnold highlights that he intends to set up the trust for his two

sons therefore the beneficiaries in this circumstances are the minors would be receiving the

benefit from the trust. The minors form the part of the trustee and would be taxed at the

highest marginal tax rate18. Taking into the consideration of Arnold Jones an advice can be

made in regard to setting up of trust is that the trustee would be paying the tax for the minor

son who aged below the age of 18 years, While the other trust members such as his wife and

his son Benjamin would be liable for taxation based on the applicable individual tax rates.

17 Maley, Mr Nicholas. "Australian Taxation Office Guidance on the Diverted Profits Tax." (2018).

18 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of Australia to tax

economic activity in offshore hubs and the position of the Australian Taxation Office." The APPEA

Journal 57.1 (2017): 49-63.

Arnold he intends to set up the trust for their two sons. The taxation office of Australia

defines that an individual is required to pay the tax relating to the share of the trust’s net

income based on the applicable tax rates17. Furthermore, the trustee is also required to pay the

tax on behalf of their minors depending upon the share of the trust net income. The

beneficiaries are under the obligations of declaring the income in their own income tax.

The present situation of Arnold highlights that he intends to set up the trust for his two

sons therefore the beneficiaries in this circumstances are the minors would be receiving the

benefit from the trust. The minors form the part of the trustee and would be taxed at the

highest marginal tax rate18. Taking into the consideration of Arnold Jones an advice can be

made in regard to setting up of trust is that the trustee would be paying the tax for the minor

son who aged below the age of 18 years, While the other trust members such as his wife and

his son Benjamin would be liable for taxation based on the applicable individual tax rates.

17 Maley, Mr Nicholas. "Australian Taxation Office Guidance on the Diverted Profits Tax." (2018).

18 Fry, Martin. "Australian taxation of offshore hubs: an examination of the law on the ability of Australia to tax

economic activity in offshore hubs and the position of the Australian Taxation Office." The APPEA

Journal 57.1 (2017): 49-63.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.