Taxation Law: Analysis of Assessable Income and CGT - Exam Solution

VerifiedAdded on 2022/10/17

|9

|1691

|335

Homework Assignment

AI Summary

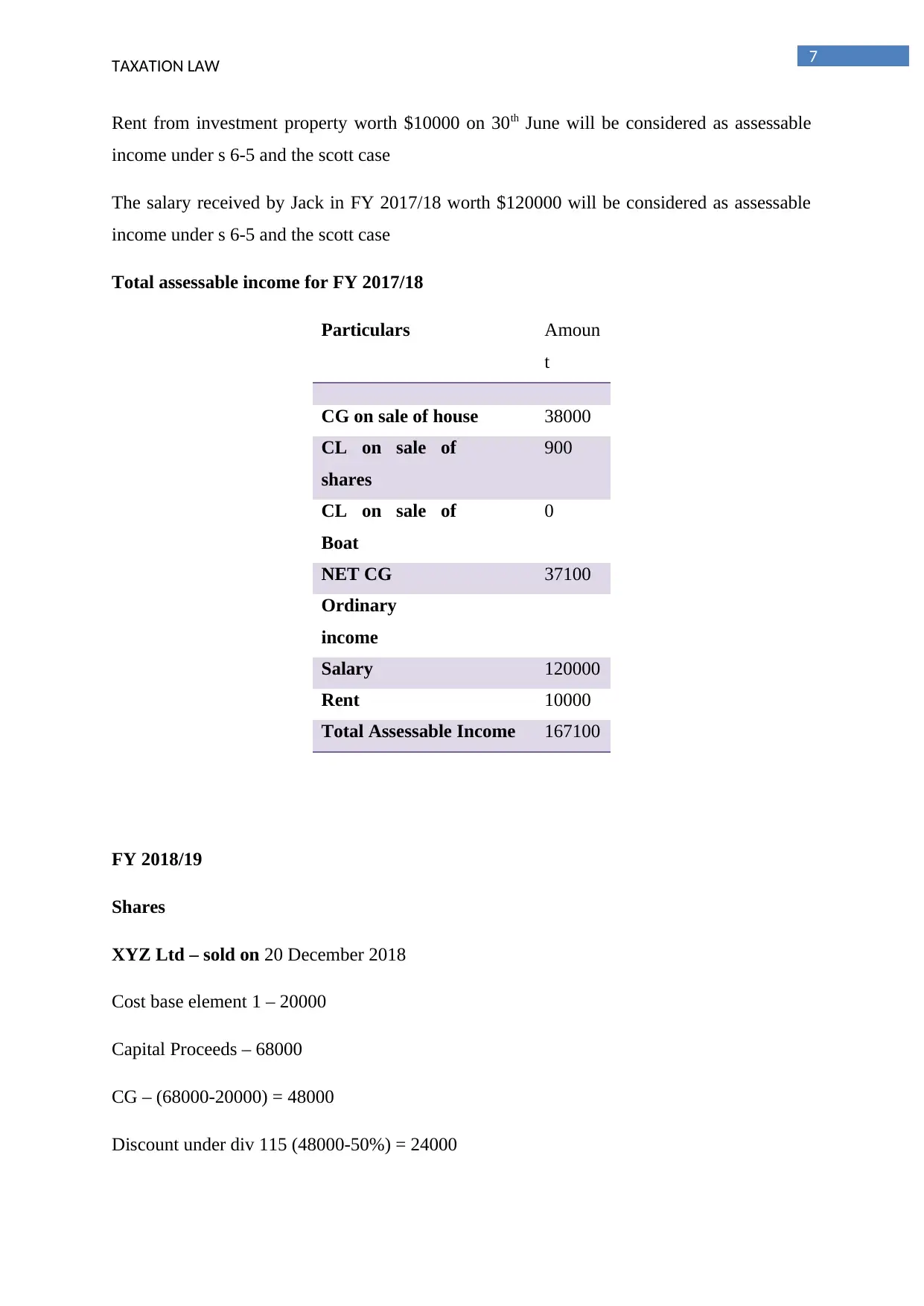

This document presents a comprehensive solution to a taxation law assignment, addressing two key questions. Question 1 examines whether a $4 million payment received by AAPL from selling trademarks constitutes assessable income, analyzing relevant case law like Scott v C of T, Eisner v Macomber, Jarrold v Boustead, Ruhamah Property Co Ltd v FC of T, and Kwikspan Purlin System Pty Ltd v FC of T. The solution concludes that the payment is a capital receipt and not assessable income. Question 2 delves into the taxation consequences for Jack, covering capital gains tax (CGT) on the sale of shares, a house, and a boat, as well as ordinary income from rent and salary. The analysis incorporates provisions from ITAA97, including sections on CGT assets, CGT events, cost base, capital proceeds, and the 50% CGT discount. The solution calculates assessable income for both the 2017/18 and 2018/19 financial years, considering both capital gains and ordinary income, with references to Arthur Murray (N.S.W.) Pty. Ltd. v. C. of T. and Scott v C of T (NSW).

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

© 2024 | Zucol Services PVT LTD | All rights reserved.