ACC304 Taxation Law: Analyzing Income, Deductions, and Residency

VerifiedAdded on 2023/06/07

|12

|2099

|306

Report

AI Summary

This report provides tax advice to two clients, Elwood and Jake, on their Australian tax obligations. For Elwood, the report analyzes his residency status based on his relocation to Australia for employment, purchase of a home, and integration into the community, concluding that he and his wife are Australian residents for tax purposes. For Jake, the report assesses the taxability of various income sources, including salary, reimbursements, interest, dividends, and capital gains, and identifies allowable deductions such as work-related expenses and tax agent fees. It also discusses Jake's liability for the Medicare levy surcharge. Finally, the report explains negative gearing as an investment strategy and discusses potential future changes to negative gearing policies and their impact on investors. Desklib offers a wealth of similar assignments and study resources for students.

Running head: TAXATION LAW

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Taxation Law

Name of the Student

Name of the University

Authors Note

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1TAXATION LAW

Table of Contents

Part 1..........................................................................................................................................2

Answer to Part 2 A:....................................................................................................................4

Answer to Part 2B:.....................................................................................................................8

References:...............................................................................................................................10

Table of Contents

Part 1..........................................................................................................................................2

Answer to Part 2 A:....................................................................................................................4

Answer to Part 2B:.....................................................................................................................8

References:...............................................................................................................................10

2TAXATION LAW

Part 1

Letter of Advice

To Elwood and Inda

From Tax Consultant

Date – 9th September 2018

Dear Elwood and Inda

We would like to draw your kind towards the residential status based on the

information furnished by you. We would like to inform you that the “Taxation ruling TR

98/17” provides the interpretation of the ordinary meaning of the term resides inside the

definition of stated under “subsection 6 (1) of the ITAA 1936”. The ruling is applicable on

individuals that enters Australia with the employment contracts or those that are migrating

under the status of business residence. The status of residency forms the matter of fact and

central element in determining a taxpayer’s liability to taxation. According to the “section

995-1 of the ITAA 1936” the Australian resident represents a person who is the occupant of

Australia.

According to the information furnished, you were transferred to Australia on 1st July

with your wife and children for a minimum of three years. You bought the house in Australia

and you moved in immediately. You also registered the telephone and electricity in your

name. The “taxation ruling of TR 98/17” lay down the factors such as behaviour while

present in Australia is an important aspect in determining residential status. This includes the

character and quality of an individual’s behaviour explains the way in which a person

arranges their domestic as well as economic affairs as an element of daily order of their lives.

The commissioner in “Reid v The Commissioner of Inland Revenue (1926)” held that

Part 1

Letter of Advice

To Elwood and Inda

From Tax Consultant

Date – 9th September 2018

Dear Elwood and Inda

We would like to draw your kind towards the residential status based on the

information furnished by you. We would like to inform you that the “Taxation ruling TR

98/17” provides the interpretation of the ordinary meaning of the term resides inside the

definition of stated under “subsection 6 (1) of the ITAA 1936”. The ruling is applicable on

individuals that enters Australia with the employment contracts or those that are migrating

under the status of business residence. The status of residency forms the matter of fact and

central element in determining a taxpayer’s liability to taxation. According to the “section

995-1 of the ITAA 1936” the Australian resident represents a person who is the occupant of

Australia.

According to the information furnished, you were transferred to Australia on 1st July

with your wife and children for a minimum of three years. You bought the house in Australia

and you moved in immediately. You also registered the telephone and electricity in your

name. The “taxation ruling of TR 98/17” lay down the factors such as behaviour while

present in Australia is an important aspect in determining residential status. This includes the

character and quality of an individual’s behaviour explains the way in which a person

arranges their domestic as well as economic affairs as an element of daily order of their lives.

The commissioner in “Reid v The Commissioner of Inland Revenue (1926)” held that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3TAXATION LAW

nature of presence and time must be considered while determining whether a person lives in a

place or where they spend a portion of their life.

An individual’s intention or the purpose of presence in Australia helps in

understanding whether the person lives here. A well-settled purpose such as employment

might assist the intention of residing in Australia. Another factor that coincides with your

residency status your maintenance and location of assets. The purchase of house with

registration of telephone and electricity bill by you suggest the establishment of home in

Australia.

A factor that may indicate you and your wife Inda is resident of Australia is your

presence of family and employment ties. The court’s opinion in “Peel v The Commissioners

of Inland Revenue (1927)” held that a person that comes to Australia with an employment

contract and maintains the behaviour which might reflect that the person is residing here. You

bought a home and also registered the telephone bill in your name. Your behaviour coincides

with residing in Australia.

The ruling further provides that the social and living arrangements represents the way

an individual interacts with the surroundings while their stay in Australia and might reflect

that they are residing in Australia. This includes joining sports or community functions and

enrolling children to school. The information furnished by you represents that you bought

joined the local gym and chess club. Your children also enrolled into the local school with

your wife working as part-time sales manager. The extent of your social and living

arrangement indicates that you are residing in Australia. Elwood, with reference to “section

995-1 of the ITAA 1936” you and your wife Inda will be held as Australian resident.

We hope that the advice provided above has helped you in serving your purpose. As

you and your wife Inda is an Australian residents within the ordinary meaning of “subsection

nature of presence and time must be considered while determining whether a person lives in a

place or where they spend a portion of their life.

An individual’s intention or the purpose of presence in Australia helps in

understanding whether the person lives here. A well-settled purpose such as employment

might assist the intention of residing in Australia. Another factor that coincides with your

residency status your maintenance and location of assets. The purchase of house with

registration of telephone and electricity bill by you suggest the establishment of home in

Australia.

A factor that may indicate you and your wife Inda is resident of Australia is your

presence of family and employment ties. The court’s opinion in “Peel v The Commissioners

of Inland Revenue (1927)” held that a person that comes to Australia with an employment

contract and maintains the behaviour which might reflect that the person is residing here. You

bought a home and also registered the telephone bill in your name. Your behaviour coincides

with residing in Australia.

The ruling further provides that the social and living arrangements represents the way

an individual interacts with the surroundings while their stay in Australia and might reflect

that they are residing in Australia. This includes joining sports or community functions and

enrolling children to school. The information furnished by you represents that you bought

joined the local gym and chess club. Your children also enrolled into the local school with

your wife working as part-time sales manager. The extent of your social and living

arrangement indicates that you are residing in Australia. Elwood, with reference to “section

995-1 of the ITAA 1936” you and your wife Inda will be held as Australian resident.

We hope that the advice provided above has helped you in serving your purpose. As

you and your wife Inda is an Australian residents within the ordinary meaning of “subsection

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4TAXATION LAW

6 (1) of the ITAA 1936”, both you and your wife would be held taxable for the incomes

generated from salary and rental property.

Thank You

6 (1) of the ITAA 1936”, both you and your wife would be held taxable for the incomes

generated from salary and rental property.

Thank You

5TAXATION LAW

Answer to Part 2 A:

Letter of Advice

To Jake

From Tax Consultant

Date – 9th September 2018

Dear Jake

We would like to draw your kind towards the taxable income based on the transactions

furnished by you.

a. As per “section 6 of the ITAA 1936” income derived from the personal exertion

includes the salaries, wages, allowances and gratuities that obtained in capacity of

services rendered by employee. “Section 6-5 of the ITAA 1997” states that most of

the receipts by taxpayer constitutes ordinary income. The court in “Scott v CT

(1935)” held that receipts should be treated in ordinary sense and use of mankind. The

receipt of gross salary received by you will be included in your tax return as income

from ordinary concepts.

b. According to the ATO an individual that receives the reimbursement of car expense, it

would be held as the income and the reimbursement must be included into the tax

return. The amount of reimbursement received by you will be held as the income and

would be included in your tax return for assessment purpose.

c. An element of an income character is earned when it comes to the taxpayer. The

receipt of interest derived by you from the bank account would be treated as income

under the ordinary concepts under section 6-5 of the ITAA 1997. Hence the bank

interest would be included for assessment in your tax return as ordinary income.

Answer to Part 2 A:

Letter of Advice

To Jake

From Tax Consultant

Date – 9th September 2018

Dear Jake

We would like to draw your kind towards the taxable income based on the transactions

furnished by you.

a. As per “section 6 of the ITAA 1936” income derived from the personal exertion

includes the salaries, wages, allowances and gratuities that obtained in capacity of

services rendered by employee. “Section 6-5 of the ITAA 1997” states that most of

the receipts by taxpayer constitutes ordinary income. The court in “Scott v CT

(1935)” held that receipts should be treated in ordinary sense and use of mankind. The

receipt of gross salary received by you will be included in your tax return as income

from ordinary concepts.

b. According to the ATO an individual that receives the reimbursement of car expense, it

would be held as the income and the reimbursement must be included into the tax

return. The amount of reimbursement received by you will be held as the income and

would be included in your tax return for assessment purpose.

c. An element of an income character is earned when it comes to the taxpayer. The

receipt of interest derived by you from the bank account would be treated as income

under the ordinary concepts under section 6-5 of the ITAA 1997. Hence the bank

interest would be included for assessment in your tax return as ordinary income.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6TAXATION LAW

d. “Section 6(1) of the ITAA 1936” states an Australian resident company might pay or

credit you with the un-franked dividend. These un-franked dividend does not has any

franking credit attached to it. Therefore, “under section 44 (1) of the ITAA 1936” the

un-franked dividend received by you should be declared in your tax statement for

assessment.

e. “A CGT event G1” happens when capital gains is reported from the sale of shares.

The cost base of the shares would also include the brokerage costs incurred by you.

As evident you reported capital gains from the sale of shares. The capital gains from

the sale of shares would be included in your tax return for assessment purpose as

ordinary income.

f. According to “subdivision 108-C” personal use assets is treated as the non-collectable

assets that is mainly used for the personal enjoyment. According to “section 118-

10(3)” any capital gains or loss made from the personal use asset should be

disregarded that has the cost base of $10,000. Loss made from the sale of autographed

cricket bats yielded a loss for you and hence the same should be disregarded.

g. According to the ATO an individual is allowed to claim motor vehicle expenses for

the portion of the use that is in the direction of business use. You reported a total

travel of 7,420 kilometres out of which 95% were dedicated towards business

purpose. As you have failed to maintain a log book your deductions would be limited

to 5000 kilometres based on standard rate of 66 cents per kilometre.

h. According to the “section 8-1 of the ITAA 1997” allows a taxpayer to claim

deductions for expenses incurred for work purpose. As you have reported a telephone

cost costs of $1,400 you will entitled to claim deductions for 60% of the telephone bill

since the proportion of 60% was related to your work purpose.

d. “Section 6(1) of the ITAA 1936” states an Australian resident company might pay or

credit you with the un-franked dividend. These un-franked dividend does not has any

franking credit attached to it. Therefore, “under section 44 (1) of the ITAA 1936” the

un-franked dividend received by you should be declared in your tax statement for

assessment.

e. “A CGT event G1” happens when capital gains is reported from the sale of shares.

The cost base of the shares would also include the brokerage costs incurred by you.

As evident you reported capital gains from the sale of shares. The capital gains from

the sale of shares would be included in your tax return for assessment purpose as

ordinary income.

f. According to “subdivision 108-C” personal use assets is treated as the non-collectable

assets that is mainly used for the personal enjoyment. According to “section 118-

10(3)” any capital gains or loss made from the personal use asset should be

disregarded that has the cost base of $10,000. Loss made from the sale of autographed

cricket bats yielded a loss for you and hence the same should be disregarded.

g. According to the ATO an individual is allowed to claim motor vehicle expenses for

the portion of the use that is in the direction of business use. You reported a total

travel of 7,420 kilometres out of which 95% were dedicated towards business

purpose. As you have failed to maintain a log book your deductions would be limited

to 5000 kilometres based on standard rate of 66 cents per kilometre.

h. According to the “section 8-1 of the ITAA 1997” allows a taxpayer to claim

deductions for expenses incurred for work purpose. As you have reported a telephone

cost costs of $1,400 you will entitled to claim deductions for 60% of the telephone bill

since the proportion of 60% was related to your work purpose.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7TAXATION LAW

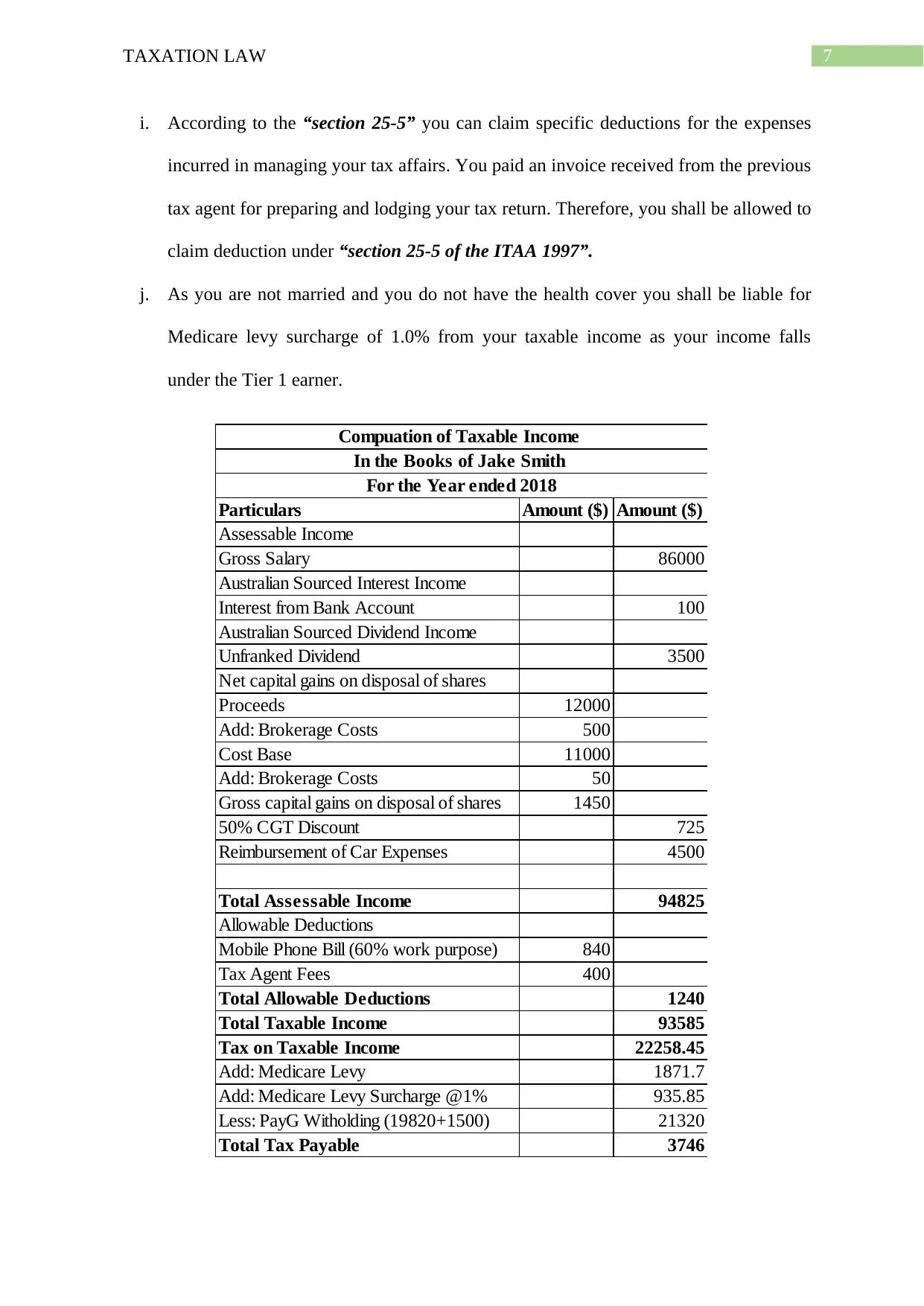

i. According to the “section 25-5” you can claim specific deductions for the expenses

incurred in managing your tax affairs. You paid an invoice received from the previous

tax agent for preparing and lodging your tax return. Therefore, you shall be allowed to

claim deduction under “section 25-5 of the ITAA 1997”.

j. As you are not married and you do not have the health cover you shall be liable for

Medicare levy surcharge of 1.0% from your taxable income as your income falls

under the Tier 1 earner.

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 86000

Australian Sourced Interest Income

Interest from Bank Account 100

Australian Sourced Dividend Income

Unfranked Dividend 3500

Net capital gains on disposal of shares

Proceeds 12000

Add: Brokerage Costs 500

Cost Base 11000

Add: Brokerage Costs 50

Gross capital gains on disposal of shares 1450

50% CGT Discount 725

Reimbursement of Car Expenses 4500

Total Assessable Income 94825

Allowable Deductions

Mobile Phone Bill (60% work purpose) 840

Tax Agent Fees 400

Total Allowable Deductions 1240

Total Taxable Income 93585

Tax on Taxable Income 22258.45

Add: Medicare Levy 1871.7

Add: Medicare Levy Surcharge @1% 935.85

Less: PayG Witholding (19820+1500) 21320

Total Tax Payable 3746

Compuation of Taxable Income

In the Books of Jake Smith

For the Year ended 2018

i. According to the “section 25-5” you can claim specific deductions for the expenses

incurred in managing your tax affairs. You paid an invoice received from the previous

tax agent for preparing and lodging your tax return. Therefore, you shall be allowed to

claim deduction under “section 25-5 of the ITAA 1997”.

j. As you are not married and you do not have the health cover you shall be liable for

Medicare levy surcharge of 1.0% from your taxable income as your income falls

under the Tier 1 earner.

Particulars Amount ($) Amount ($)

Assessable Income

Gross Salary 86000

Australian Sourced Interest Income

Interest from Bank Account 100

Australian Sourced Dividend Income

Unfranked Dividend 3500

Net capital gains on disposal of shares

Proceeds 12000

Add: Brokerage Costs 500

Cost Base 11000

Add: Brokerage Costs 50

Gross capital gains on disposal of shares 1450

50% CGT Discount 725

Reimbursement of Car Expenses 4500

Total Assessable Income 94825

Allowable Deductions

Mobile Phone Bill (60% work purpose) 840

Tax Agent Fees 400

Total Allowable Deductions 1240

Total Taxable Income 93585

Tax on Taxable Income 22258.45

Add: Medicare Levy 1871.7

Add: Medicare Levy Surcharge @1% 935.85

Less: PayG Witholding (19820+1500) 21320

Total Tax Payable 3746

Compuation of Taxable Income

In the Books of Jake Smith

For the Year ended 2018

8TAXATION LAW

Your total tax liability for the income is attached in the advice. We hope that the letter

has served your purpose and we look forward to serve your again in future.

Thank You

Your total tax liability for the income is attached in the advice. We hope that the letter

has served your purpose and we look forward to serve your again in future.

Thank You

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9TAXATION LAW

Answer to Part 2B:

Negative gearing can be defined as the strategy of producing the short to medium

term losses originating from the tax deductible expenses that are greater than the investment

income. This provides the taxpayer with the exposure of potential gains and losses (Pawson

2018). The strategy can be held as popular among the taxpayer because the tax losses that

originates can be usually reduced by the investors other assessable income. This would

ultimately benefit the investors in lower annual income tax bill.

A recent reformations in the negative gearing may provide the investors with the tax

concession. The proposed changes that may take place is the tax breaks that would cut the

negative gearing deductions by 57.3% (Eccleston et al. 2018). Such changes in the model

proposes that those investors that are under the 50% of the income distribution or those that

have modest income would continue to receive 100% deduction.

The future changes would allow the investors in claiming deductions for any

expenditure including the interest on loan as this would help them in creating an income.

Potential changes in the negative could witness a progressive rental deductions for the

investors and less wealthy investors may experience a significant fall in tax savings (Cho, Li

and Uren 2017). Future changes that may take place in the negative gearing policy is that

CGT tax discount could be halved from the present 50% to 25% and limiting the negative

gearing to new rental dwellings.

There are also potential tax benefits for an investors whose taxable income is 100k

during an income year. The taxpayer at the 30% marginal tax rate can gain the benefit of

2.5% allowance under the division 43 (Gribbin 2017). This would provide the taxpayer with

Answer to Part 2B:

Negative gearing can be defined as the strategy of producing the short to medium

term losses originating from the tax deductible expenses that are greater than the investment

income. This provides the taxpayer with the exposure of potential gains and losses (Pawson

2018). The strategy can be held as popular among the taxpayer because the tax losses that

originates can be usually reduced by the investors other assessable income. This would

ultimately benefit the investors in lower annual income tax bill.

A recent reformations in the negative gearing may provide the investors with the tax

concession. The proposed changes that may take place is the tax breaks that would cut the

negative gearing deductions by 57.3% (Eccleston et al. 2018). Such changes in the model

proposes that those investors that are under the 50% of the income distribution or those that

have modest income would continue to receive 100% deduction.

The future changes would allow the investors in claiming deductions for any

expenditure including the interest on loan as this would help them in creating an income.

Potential changes in the negative could witness a progressive rental deductions for the

investors and less wealthy investors may experience a significant fall in tax savings (Cho, Li

and Uren 2017). Future changes that may take place in the negative gearing policy is that

CGT tax discount could be halved from the present 50% to 25% and limiting the negative

gearing to new rental dwellings.

There are also potential tax benefits for an investors whose taxable income is 100k

during an income year. The taxpayer at the 30% marginal tax rate can gain the benefit of

2.5% allowance under the division 43 (Gribbin 2017). This would provide the taxpayer with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10TAXATION LAW

proportionate reduction in cost base resulting in larger assessable capital gains or smaller

capital losses.

proportionate reduction in cost base resulting in larger assessable capital gains or smaller

capital losses.

11TAXATION LAW

References:

Cho, Y., Li, S.M. and Uren, L., 2017. Negative Gearing Tax And Welfare: A Quantitative

Study For The Australian Housing Market.

Eccleston, R., Verdouw, J. and Flanagan, K., 2018. Gradual reform to capital gains, negative

gearing and stamp duty will make housing more affordable.

Gribbin, C., 2017. Negative gearing: An update ahead of the 2017-18 federal

budget. Taxation in Australia, 51(10), p.554.

Pawson, I., 2018. Reframing Australia's housing affordability problem: The politics and

economics of negative gearing. Journal of Australian Political Economy, The, (81), p.121.

References:

Cho, Y., Li, S.M. and Uren, L., 2017. Negative Gearing Tax And Welfare: A Quantitative

Study For The Australian Housing Market.

Eccleston, R., Verdouw, J. and Flanagan, K., 2018. Gradual reform to capital gains, negative

gearing and stamp duty will make housing more affordable.

Gribbin, C., 2017. Negative gearing: An update ahead of the 2017-18 federal

budget. Taxation in Australia, 51(10), p.554.

Pawson, I., 2018. Reframing Australia's housing affordability problem: The politics and

economics of negative gearing. Journal of Australian Political Economy, The, (81), p.121.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.